Download presentation

Presentation is loading. Please wait.

1

DEPOSIT INSURANCE IN VIETNAM

Group 9’s members: Bùi Kiều Diệu Linh Hoàng Mỹ Linh Nguyễn Phương Linh Đào Thùy Linh Nguyễn Quỳnh Loan Bùi Hải Long

2

Brief outline I/Basic knowledge about deposit insurance

II/Deposit insurance in Vietnam

3

I/Basic knowledge about deposit insurance

4

Why deposit insurance exist

Credit risk Liquidity risk Bank’s risks Deposits withdrawn without notice Bank insolvency Bank run Deposit insurance Protect depositors and prevent financial crisis Safety net

5

How it works Government run Private entities with government backing

Completely private entities

6

How it works (cont.) 119 countries with DI (IADI – June 2008)

Some countries with more than 1 DI system 1 system can cover more than 1 country

7

FDIC - fast facts Established in 1934 – after Great Depression banking crisis Insurance up to $250,000 per depositor After establishment, no depositor has lost any insured fund as a result of a failure

8

Purchase and assumption method

FDIC working method Payoff method Allow the bank to fail Liquidate its asset and pay off creditors Purchase and assumption method Find a partner to take over the bank Help merger partner with subsidized loans or buying some weaker loans

9

FDIC and its criticism With explicit insurance

Depositors are discouraged to monitor bank’s operation Bank are encouraged to perform risky activities

10

II/Deposit insurance in Vietnam

11

1. Legal framework and operation of deposit insurance

Decree No.89/1999/ND-CP Decision No.218/1999/QD-TTG Decision No.75/2000/QD-TTG Decree No.109/2005/ND-CP Decision No.13/2008/QD-TTG

12

Protecting legitimate rights and interests of depositors

Key objectives Protecting legitimate rights and interests of depositors Contributing to the maintenance of the stability of credit institutions Ensuring the safe and sound development of the banking activities

13

withdraw deposit institution licenses

Main operations of DIV i. License new deposit institutions, issue supplementary deposit institution licenses and withdraw deposit institution licenses ii. Collect insurance premium iii. Monitor, supervise and inspect the compliance with the Decree of the Government on Deposit Insurance and prudential regulations on banking operations of the insured Institution iv. Reimburse depositors within the regulated limitation of cover v. Debt collection for financial institutions in liquidation vi. Publicize and popularize the deposit insurance activities of DIV vii. Provide financial assistance for insured institutions viii. Provide financial investment from idle capital in order to protect the capital allocated by the State and cover its expenses.

15

Participants State-owned commercial banks Joint-stock commercial banks

Joint-venture commercial banks Branches of foreign banks Finance companies Finance leasing companies People’ credit funds

16

Insured Deposits Maximum coverage Premium Type of insured deposits

17

2. Difficulties and challenges of DIV

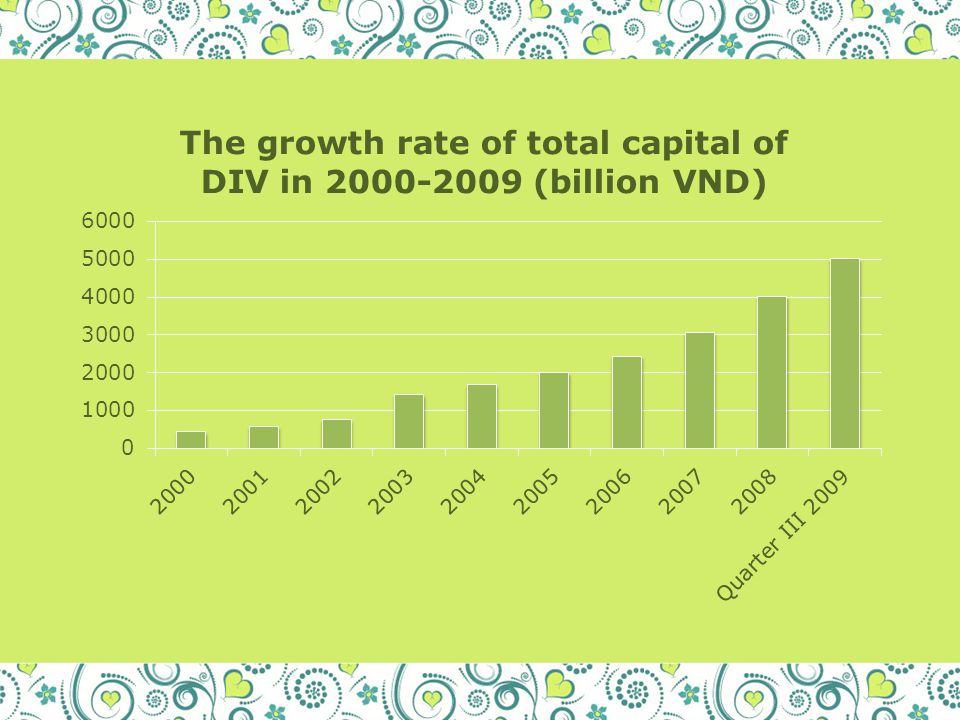

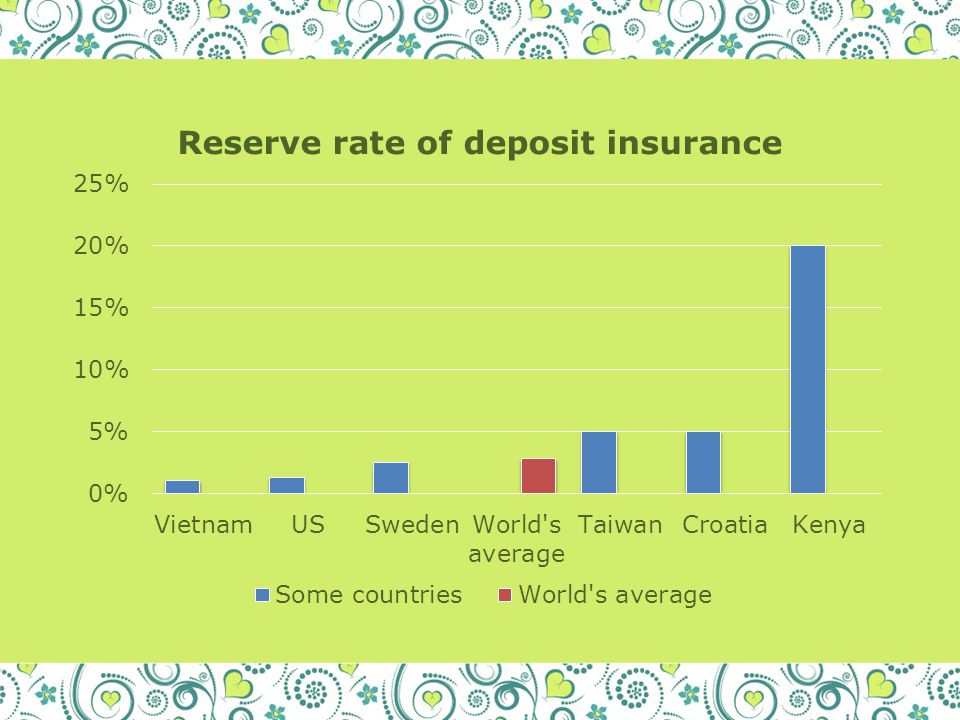

The deposit insurance fee in Vietnam is now apply at the same rate of 0.15% of the total balance amount, which is not reasonable The percentage of deposit insurance in Vietnam is quite low compare to other countries According to international practice, the percentage of the deposit insurance reserve (deposit insurance fund / total insured deposits) is usually 2.5% - 3%. This rate in our country is about 1% 6000 billions VND is only 2 times minimum charter capital of a joint-stock commercial banks, which is not enough when bank run happens.

is usually 2.5% - 3%. This rate in our country is about 1% 6000 billions VND is only 2 times minimum charter capital of a joint-stock commercial banks, which is not enough when bank run happens.")

19

Maximum payment rate of deposit insurance in Vietnam is currently too low to ensure the confidence of the lender when the event occurs In addition, the DIV does not cover deposits in foreign currencies or gold (the banking system is keeping about 30 billion USD and 100 tones of gold (5 billion USD)

")

20

3. Measures to take The state bank and DIV should increase the deposit insurance reserve. In the long term DIV may increase the maximum payment to ensure depositors’ confidence The DIV should move from payoff method to purchase and assumption method DIV should be independent to state bank activity DIV should charge insurance fee according to risk level

21

Q&A Thank you for listening

Similar presentations