Download presentation

Presentation is loading. Please wait.

1

GAAP and Accrual Accounting By Violeta Mercado

2

Address: Recognition Measurement Disclosure Generally Accepted Accounting Principles (GAAP)

")

3

The Financial Accounting Standards Board FASB The body that developed Generally Accepted Accounting Principles (GAAP)

")

4

The Seven Key Components of The General Purpose of External Financial Reporting - GAAP Income Statement Balance Sheet Statement of cash flow Statement of Retained Earnings Statement of Comprehensive Income Footnotes Disclosure and Supplement Schedules Auditor’s Opinion

5

GAAP Principles Methods Procedures & Pronouncements issued by Committee on Accounting Procedure (CAP) Accounting Principles Board (APB) Financial Accounting Standards Board (FASB). The FASB Codification is the sole authoritative source for such GAAP and includes guidance from the above sources. For publicly traded entities, the SEC has additional reporting guidelines.

6

Authoritative GAAP FASB –Accounting standard codification compilation of pronouncements issued by FASB, APB, CAP. Non – Authoritative FASB concepts, AICPA Issues paper, IFRS. SEC Guidance – Considered part of Authoritative GAAP for public companies.

7

Topics that Financial Accounting Standards Board (FASB) Accounting Standards Codification not include. Other comprehensive basis of accounting Cash basis Income tax basis Regulatory accounting principles

8

Securities and Exchange Commission (SEC). The agency that enforces Generally Accepted Accounting Principles. GAAP

9

Accounting Principles Board- (APB) The entity that published thirty-one opinions, some of which are now part of the Codification.

The entity that published thirty-one opinions, some of which are now part of the Codification.")

10

Accrual Basis of Accounting GAAP, and therefore the financial statements, reflect the accrual basis of accounting rather than the cash basis of accounting. Both U.S. and international GAAP reflect the accrual basis of accounting. Under the accrual basis, revenues are recognized when earned, regardless of the period of cash collection. Expenses are recognized when incurred, regardless of the period of cash payment. The accrual basis of accounting is preferred over the cash basis of accounting because it reflects a better association of revenues and expenses with the appropriate accounting period. The accrual basis of accounting recognizes all resource changes when they occur. The cash basis of accounting limits the recognition of resource changes to cash flows.

11

Accrual Basis Accounting Recognizes and reports the economic activities of the firm in the period the activity was INCURRED, REGARDLESS of when the cash activity takes places. Accrual Basis accounting is the HEART and SOUL of the matching concept and financial reporting.

12

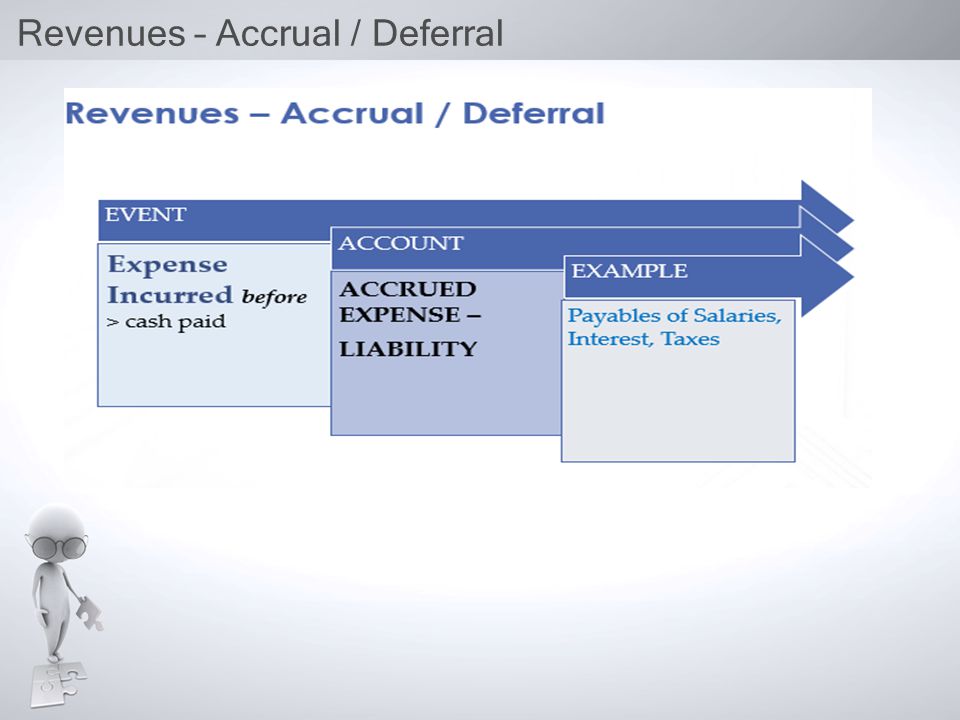

Revenues – Accrual / Deferral

16

Process

17

Theme of Accruals and Deferrals

18

Current Assets Are in the form of cash, or Will be converted into cash, or Consumed within one year or The operating cycle of the business, whichever is longer.

19

Long-term assets Assets that are not classified as current assets. Long-term assets are reported on the balance sheet and represent a company's property, equipment, and other capital assets (reduced by depreciation) expected to be useable for more than one year.

expected to be useable for more than one year..")

Similar presentations

. 2. Study the conceptual.>")