Download presentation

Presentation is loading. Please wait.

2

Debt and Equity are not the only securities that firms issue. Instead, you can think of them as extreme points on a continuum of securities: ◦ Convertible Bonds ◦ Preferred Stock ◦ Convertible Preferred Stock Financial engineering in investment banks is about creating new securities, often combining features of debt and equity to solve a particular contracting problem

5

A convertible bond is like a straight bond with the option of converting it to a pre- specified number of shares ◦ Coupon Payments ◦ Face Value ◦ Maturity

6

Conversion Ratio ◦ The number of shares into which each bond can be converted Conversion Price ◦ The effective price an investor is paying per share if they convert their bond

8

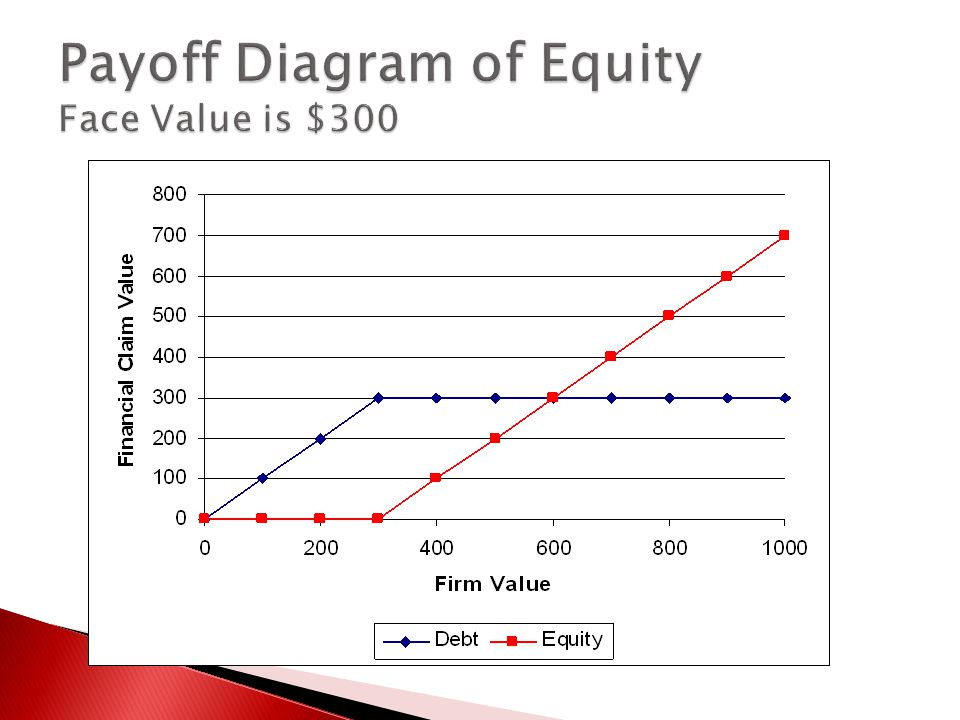

Assume that the $300 in debt our firm issued also included the option to convert the debt into 15 shares of stock Assume that there are currently 20 equity shares outstanding What is the conversion price? At what firm value will the stock have this price?

14

When issued, what would the convertible debt have sold for relative to the straight debt? ◦ The debt holders get all of the security of straight debt plus the option to convert. ◦ Therefore, convertible debt with the same face value and coupon rate will sell for more than straight debt.

15

Some firms issue convertibles thinking they are cheap debt ◦ Firms can raise the same amount of money as issuing straight debt but have a lower coupon rate ◦ What are they missing?

16

Other firms issue convertibles because they think they are issuing cheap Equity ◦ Firms can essentially issue equity and get investors to pay more for the convertible debt than straight equity ◦ What are managers forgetting?

17

Disagreements about risk ◦ If investors think the firm is more risky than the managers, they will over pay for the option component Reduce the incentive to risk shift ◦ If bondholders now get some of the upside, the return to equity holders of increasing the risk of the firm is lower

18

Graham, John R., and Campbell Harvey, 2001, Journal of Financial Economics

19

Should they convert before the bond matures? What do they get by converting early? What do they lose by converting early?

20

Pays dividends ◦ Amounts are often stipulated at the time of issue ◦ Other times they are paid at the discretion of the Board of Directors but must be paid before common stock dividends are paid Carries a par value Higher priority in bankruptcy than common equity, lower priority than debt May or may not carry voting rights Dividends are not tax deductible Convertible Preferred Shares offer the option to convert to common

22

Lessee ◦ Uses the asset ◦ Makes payments for its use ◦ Maintenance of asset if negotiated at time of lease Lessor ◦ Receives the payments ◦ Owns the asset

23

Eades and Marston (2002)

")

25

Long Term Debt Capital Leases Operating Leases % of Firms Using 88.1%52.6%99.9% % of Firm’s Market Value 14.2%1.6%8.0% % of Fixed Claims 52.4%6.3%41.2% Use of Debt and Leases by U.S. Firms SIC Codes 2000 to 5999 in the years 1981 to 1992. (Graham, Lemmon, and Schallheim, 1998)

.")

26

Operating Leases ◦ Off Balance Sheet ◦ Tend to be for periods shorter than the economic life of the asset ◦ Often cancelable Capital Leases ◦ On Balance Sheet ◦ Equipment is an asset of the firm, lease payments are a liability

27

Capital Lease (meets one of the following) ◦ Automatic transfer of ownership ◦ Purchase option at significantly below expected residual value ◦ Lease lasts at least 75% of economic life of asset ◦ The present value of the lease represents at least 90% of the assets value

◦ Automatic transfer of ownership ◦ Purchase option at significantly below expected residual value ◦ Lease lasts at least 75% of economic life of asset ◦ The present value of the lease represents at least 90% of the assets value")

28

A lease is a true lease for the IRS if: 1.Lessor makes minimum 20% equity investment 2.Equipment has residual value of at least 20% 3.Purchase price close to fair value 4.Transaction expected to generate profit 5.No lessee investment 6.Rents must be reasonably stable 7.Must be a market for the equipment at conclusion of lease beyond the lessee

29

Cash Flows – what are the incremental cash flows from a lease relative to a purchase ◦ Lease Payments ◦ Purchase price of asset ◦ Depreciation tax shield ◦ Residual Price ◦ Operating Profits? Discount Rate ◦ What is the appropriate discount rate for a lease? ◦ Should it be a before tax or after tax rate?

30

You are considering the purchase of a $10 million piece of equipment. ◦ It would be depreciated using 5 year MACRS. ◦ The asset would have zero residual value at the end of the five years. ◦ The pre-tax cost of debt is 10%. ◦ The firm’s effective marginal tax rate is 20% What constant lease payment over the same five years would be equivalent to purchasing the asset?

31

5 year MACRS Schedule: What are the annual incremental cash flows? Year 0Year 1Year 2Year 3Year 4Year 5 20%32%19.2%11.52% 5.76% Year 0Year 1Year 2Year 3Year 4Year 5 Asset Purchase Depreciation Depreciation Tax Shield Incremental Cash Flow

32

What is the present value of the cash flows? What annual payment would have an equivalent present value? Is this annual payment amount before taxes or after taxes?

33

What if the lessee and lessor have different tax rates? ◦ What if the lessee had a low tax rate (20%) but the lessor had a 35% tax rate? ◦ There is $113K to split between the lessor and lessee Who captures the tax differential? ◦ Bargaining power between lessee and lessor ◦ Is there a shortage of potential lessees or lessors?

but the lessor had a 35% tax rate. ◦ There is $113K to split between the lessor and lessee Who captures the tax differential. ◦ Bargaining power between lessee and lessor ◦ Is there a shortage of potential lessees or lessors .")

34

What if the lessee and lessor have different depreciation schedules? ◦ In an effort to cut the budget deficit, some lawmakers have called for longer depreciation schedules for large oil companies. If the depreciation schedule were firm- dependent rather than asset-specific, ◦ What change in ownership structure of these assets would we observe? ◦ Would the deficit reduction be realized?

35

Transactions costs / convenience Lower cost of repossession Differential maintenance costs Obsolescence risk Differential sources of capital Accounting / capital budgeting differences

Similar presentations