Download presentation

Presentation is loading. Please wait.

1

John H. Cochrane University of Chicago Booth School of Business

Financial crisis John H. Cochrane University of Chicago Booth School of Business

2

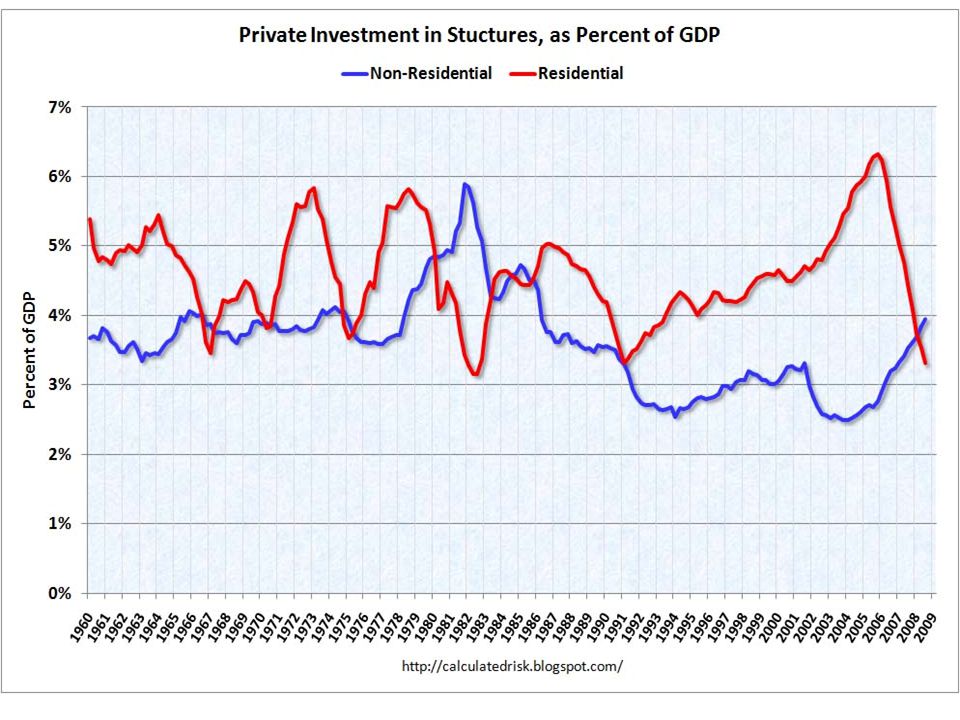

House prices, investment

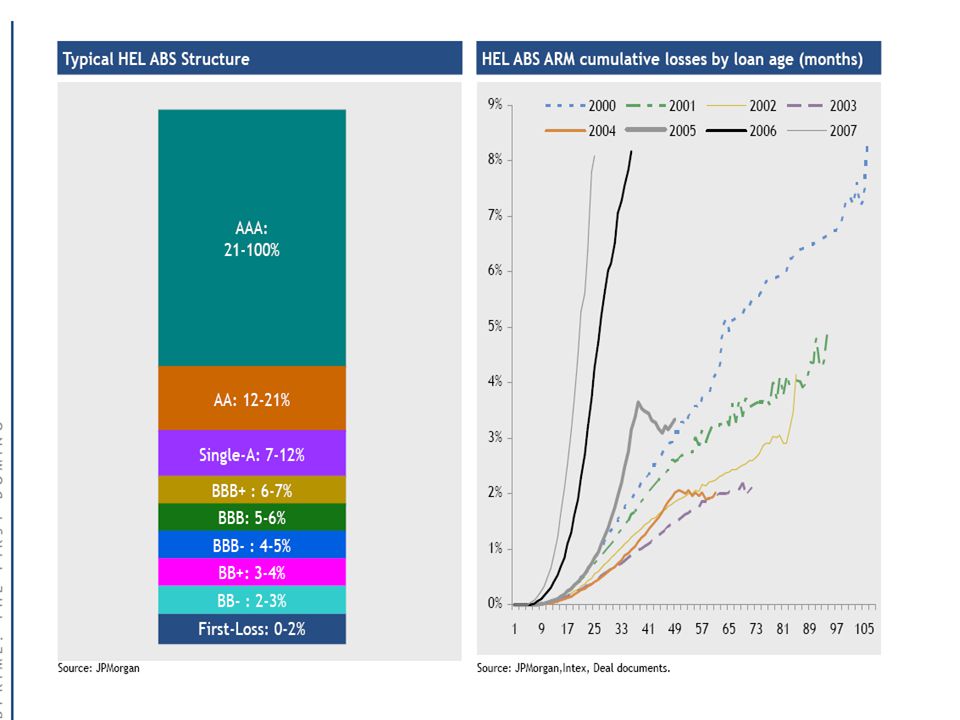

House prices rose a lot, then fell. Residential investment (home building) fell too. It often falls first in recessions Mortgage defaults start, especially in subprime and other mortgage products that basically invite homeowners to default if house prices go down Defaults wipe out low tranches fast!

fell too. It often falls first in recessions. Mortgage defaults start, especially in subprime and other mortgage products that basically invite homeowners to default if house prices go down. Defaults wipe out low tranches fast!")

8

Interest Rates

9

In normal times, CP spreads are really low!

10

A chronology of the crisis, and a sense of when things are better/worse

11

The crisis. I’m interested how much is financial, how much “illiquidity,” and how much a simple rise in credit risk and its premium. The fact that non financial AA does well and nonfinancial A2P2 is even worse than financial suggests the latter interpretation to me. The credit risk premium went up – and this is just about how investors feel, not about liquidity, leveraged investors, etc.

12

A closer view. CP rates. It differs a lot by maturity

A closer view. CP rates. It differs a lot by maturity. I found it interesting that overnight financial and nonfinancial are the same. The banks were not having special problems borrowing overnight. Again, the poor A2P2 are the ones really having problems. I think the sharp drop comes when the Fed starts buying commercial paper.

13

Lehman or Tarp? Did Lehman or the Tarp speeches set off the run? This makes the case it was the TARP speeches. (With inspiration from John Taylor) It also suggests that the function of the TARP asset purchases was just to convince the markets that the government really really was going to bail out citi, not “recapitalization so they could start lending”

It also suggests that the function of the TARP asset purchases was just to convince the markets that the government really really was going to bail out citi, not recapitalization so they could start lending")

14

The bond spread widens to historic proportions

The bond spread widens to historic proportions. Let’s look a bit deeper…

15

We worry about a crisis because “firms can’t borrow

We worry about a crisis because “firms can’t borrow.” But of course most firms do not depend terribly on bank financing, they can issue bonds. Also, bond issues do go straight to investors – you and I can buy the Vanguard corporate bond fund if prices are good. So, what happened to these rates? The credit spread opened to huge amounts, not seen since 1982 and near Depression levels. Interestingly though it’s because government and short rates fell not so much because corporate rates rose, at least until Tarp. There is nothing that “recapitalizing the banks” will do about this.

16

The huge credit spread doesn’t seem that affected by the momentous events moving around short-term rates

17

A bit of an update though without the nice vertical bars

18

The Fed is easing like crazy. (More Fed policy later)

The Fed is easing like crazy. (More Fed policy later). Notice 3 month bills below fed funds, and notice 3 month bills actually hitting zero in Dec I think the “flight to quality” represented here is a big part of the crisis.

. Notice 3 month bills below fed funds, and notice 3 month bills actually hitting zero in Dec I think the flight to quality represented here is a big part of the crisis.")

19

CDS is the modern way to measure credit spreads

CDS is the modern way to measure credit spreads. This is percent per year you have to pay for bond insurance (-200 = 2%). By summer 09 the crisis is over .

. By summer 09 the crisis is over .")

20

“Arbitrage” Many markets saw “arbitrages” open up. These aren’t true arbitrages; one end is always more illiquid than the other, or has some counterparty risk, etc. But these are prices that usually are very close to each other. In each case, the leg of the arbitrage that needs cash, needs funding, or needs borrowing is underpriced. In each case, the price difference is still small enough that “long only” investors don’t really bother that much. Why does this matter? It’s certainly a sign of illiquid markets – the usual arbitrageurs are maxed out, can’t borrow, can’t raise equity -- so strategies that try to manage risk by “we’ll sell on the way down’’ rather than buy real put options will fall apart at times like these.

21

Borrow dollars, buy Euros, lend euros, buy dollars forward

Borrow dollars, buy Euros, lend euros, buy dollars forward. 20bp is huge, because you can lever this up arbitrarily. But…”borrow dollars!” 20bp is not enough to attract long-only money.

22

Average Daily (Bond–CDS) Basis: by Rating

Date A BBB BB 9/12/2008 54bp 105bp 126bp 12/16/2008 282 388 760 10/8/2009 51 100 123 Source: J.P.Morgan Buy corporate and CDS vs. buy Treasuries. But buying corporate needs cash or repo financing, now hard to do. (Also illiquid, and CDS counterparty risk)

")

23

A normal treasury yield curve

24

On the run/off the run spread explodes!

Yield vs. duration of all outstanding treasury bonds and bills, crsp mbx database

25

Credit quantities What matters to the economy of course is whether it’s hard to borrow. It’s important to distinguish “sand in the gears,” financial dysfunction, from simple shift in the supply curve or greater credit risk. If that’s the case, fixing the banks won’t help, nor is it obvious we should help. Not every fall in quantity is a wedge between demand and supply, not every project should be funded Which kinds of debt fell, and what can we tell about supply vs. demand vs. wedge between the two opening up?

26

D.2 Borrowing by Sector ($Billion, SAAR)

Flow of funds data—private borrowing collapses Home Consumer Business S&L Federal financial Date Total Mortgage credit Corp Govt sectors Foreign D.2 Borrowing by Sector ($Billion, SAAR) 2007 2536 659 137 1252 783 186 237 1791 170 2008 1870 -58 40 551 347 43 1239 888 -129 2008Q4 2011 -196 -76 113 56 -3.5 2155 554 -429 2009Q4 956 -370 -81 -283 94 115 1485 -1533 -547 Massive decline in private borrowing, massive increase in government! Which markets and channels show this huge decline? Why? Is this “supply and demand” or “something’s wrong”?

Q Q Massive decline in private borrowing, massive increase in government! Which markets and channels show this huge decline Why Is this supply and demand or something’s wrong")

27

Flow of new lending r r “Something’s wrong” Broken intermediary?

Loan Loan “Something’s wrong” Broken intermediary? Capital constrained banks? In banks or securitized debt markets? “Supply and demand” Higher risk aversion, greater chance of default Less demand to borrow, invest in recession?

28

Commerical paper issuance

Commerical paper issuance. Asset-backed falls apart in 2007 with the blowup of SPVs. Financial falls apart post Lehman/TARP. Nonfinancial keeps going! In fact, it increases. Savers want to put money somewere, it was easy for large safe companies to borrow commercial paper in the middle of the crisis. Newspaper hyperbole “credit markets froze” miss this fact.

29

Quantities. Yes, financial declined (and all maturities declined a lot), but you’d expect to see much worse given all the complaining.

, but you’d expect to see much worse given all the complaining..")

30

US Non-Agency MBS Issuance

Falls off a cliff. And in 07 (along with ABS), long before TARP etc. The originate to sell model ended. If you want to see credit quantities affected by the financial crisis this is it. These are mortgage backed securities that don’t go through FannieFreddie, thus don’t get the government guarantee. Jumbos are an example.

, long before TARP etc. The originate to sell model ended. If you want to see credit quantities affected by the financial crisis this is it. These are mortgage backed securities that don’t go through FannieFreddie, thus don’t get the government guarantee. Jumbos are an example.")

35

Scale of Dealer Deleveraging in Corporate Bonds over 2007 and 2008

A sense of how important the run in repo is Source: Primary Dealer Survey, Federal Reserve Bank of New York

36

What about the Banks? Do the banks want to lend, can’t because of capital constraints? Or do the banks not want to lend, (they can’t sell loans anymore), and no amount of capital will change that fact? Distinguish “banks” (many were surely in trouble) from “banking system” (can competitors come in and take over) Bottom line: I think the evidence favors #2, and TARP purchases did not spur lending.

, and no amount of capital will change that fact Distinguish banks (many were surely in trouble) from banking system (can competitors come in and take over) Bottom line: I think the evidence favors #2, and TARP purchases did not spur lending.")

37

Fact: Banking system did not “delever” to any great extent

38

Again, we do not see a huge decline in loans at banks

39

Once again, no huge decline in lending

Once again, no huge decline in lending. Actually, given the severity of the recession, it’s surprising how little lending went down.

41

Bank –held debt is a small part of credit markets.

L.1 Credit Market Debt Outstanding 2006 2008 Description Pct Q2 Total credit market assets held by : 45347 100 51019 Household sector 3865 8.5 4140 8.1 Nonfinancial corporate 329 0.7 169 0.3 noncorporate 109 0.2 129 State and local 1471 3.2 1473 2.9 Federal 281 0.6 294 Rest of world 6198 13.7 7775 15.2 Monetary Authority 779 1.7 538 1.1 Commercial banking 8019 17.7 8950 17.5 Savings institutions 1519 3.3 1607 3.1 Credit unions 623 1.4 686 1.3 Property-casualty insurance 814 1.8 835 1.6 Life insurance 2806 6.2 2937 5.8 Private pension funds 705 757 1.5 State and local retirement 770 812 Federal retirement 84 108 Money market mutual funds 1561 3.4 2233 4.4 Mutual funds 1932 4.3 2314 4.5 Closed end funds 172 0.4 161 Exchange traded funds 21 0.0 43 0.1 GSE 2591 5.7 2995 5.9 Agency and GSE-backed Mortgage pools 3837 4762 9.3 ABS 4069 9.0 4257 8.3 Finance companies 1627 3.6 1639 REITS 295 232 0.5 Broker dealers 583 694 Funding corporations 289 480 0.9 Bank –held debt is a small part of credit markets. Even if the “banks don’t lend”, does this matter? Source: FRB Sept 18 Flow of funds

42

This is what all assets and liabilities of commercial banks look like, from which the next slide is drawn

43

Banks did not delever, they actually expanded

Banks did not delever, they actually expanded! Banks also did not conserve captal, paying dividends, bonuses, and making acquisitions. Controversies: Much expansion came from existing lines of credit, not new lending. Much came by taking on SPV assets from unwinding of shadow system, not new lending. And many borrowers did report trouble getting loans.

44

Banks Can And Do Raise Capital!

Firm Writedown & Loss Capital Raised Citigroup Inc.* 60.8 71.1 Wachovia Corporation* 52.7 11 Merrill Lynch & Co. 52.2 29.9 Washington Mutual Inc. 45.6 12.1 UBS AG 44.2 28 HSBC Holdings Plc 27.4 5.1 Bank of America Corp. 21.2 20.7 JPMorgan Chase & Co. 18.8 19.7 Morgan Stanley* 15.7 14.6 IKB Deutsche Industriebank AG 14.8 12.2 Royal Bank of Scotland Group Plc 14.1 23.1 Lehman Brothers Holdings Inc. 13.8 13.9 Credit Suisse Group AG 10.4 3 Deutsche Bank AG 6.1 Wells Fargo & Company 10 5.8 Credit Agricole S.A. 8.8 8.5 Barclays Plc 7.6 17.9 Canadian Imperial Bank of Commerce 7.2 2.8 Fortis* 7.1 Bayerische Landesbank 6.9 HBOS Plc 6.8 ING Groep N.V. 6.7 4.6 Societe Generale 6.6 9.4 Mizuho Financial Group Inc. National City Corp. 5.4 8.9 Natixis 5.3 11.8 Indymac Bancorp Inc 4.9 Goldman Sachs Group Inc. 10.6 …… … TOTAL 590.8 434.2 Banks Can And Do Raise Capital! The “debt overhang” story is not absolute. When banks lose money they can and do go out and raise more capital. (This being impossible is a central part of the “capital constraint” story) (source: Bloomberg.com)

(source: Bloomberg.com)")

45

Banks Can and Do Raise Capital II

Source :Anil Kashyap Includes Treasury Purchase

46

Banks can and do fail, with operations taken over and continuing under new ownership. A bank failing does not mean it cannot process new loans. In fact, sometimes it can do it better. Two lists from the internet #1 Northern Rock #2 Bear Stearns #3 ANB Financial #4 First Integrity Bank #5 Roskilde Bank #6 IndyMac #7 First Heritage Bank #8 First National Bank of Nevada #9 IKB (basically insolvent after gov't intervention) #10 Silver State #11 Fannie Mae #12 Freddie Mac #13 Lehman Brothers #14 AIG #15 Washington Mutual JPMorgan Chase Bear Stearns Bank of America Merrill Lynch Washington Mutual Wells Fargo Wachovia 5/3 Bank First Charter Bank PNC Financial Services National City Corp.

#10 Silver State #11 Fannie Mae #12 Freddie Mac #13 Lehman Brothers #14 AIG #15 Washington Mutual. JPMorgan Chase. Bear Stearns. Bank of America. Merrill Lynch. Washington Mutual. Wells Fargo. Wachovia. 5/3 Bank. First Charter Bank. PNC Financial Services. National City Corp.")

47

Macroeconomics and finance

Is there anything for our simple models that tie macro to asset pricing to do? Or do we throw everything out and only study frictions? A: Frictions are frosting, but there is a lot of cake. Many long-only unconstrained investors were “marginal” and tried to sell. Consumption: Risk aversion rises following recent losses. (“habits”). Investment: Investment falls when stock prices (q) falls.

. Investment: Investment falls when stock prices (q) falls.")

48

Rising risk aversion U(C) X C

X C")

49

SPC is the Cambell/Cochrane measure of consumption relative to habit.

When SPC falls, prices fall, risk premia rise

50

Q theory says investment falls when stock market falls

Q theory says investment falls when stock market falls. This needs no frictions or constraints

51

The Fed

53

The Fed is no longer just setting the funds rate and letting others adjust. The Fed was trying to influence rates in many markets. A good issue for monetary economics is whether it actually raises rates in individual markets or just ends up supplying more money and treasury debt

54

“Expansion of balance sheet” = printing money, lending it out

“Expansion of balance sheet” = printing money, lending it out. A trillion extra dollars! Bernanke: “Milton Friedman, we won’t make the same mistake again”

55

More detail on the many new facilities

57

Balance sheet of the Federal Reserve. Millions of dollars

Balance sheet of the Federal Reserve. Millions of dollars. Data source: Federal Reserve Release H.4.1. Aug 8, 2007 Sep 3, 2008 Oct 22, 2008 Securities 790,820 479,726 490,617 Repos 18,750 109,000 80,000 Loans 255 198,376 698,050 Discount window 255 19,089 107,561 TAF 150,000 263,092 PDCF 102,377 AMLF 107,895 Other credit 90,323 Maiden Lane 29,287 26,802 Other F.R. assets 41,957 100,524 519,713 Factors supplying reserve funds 902,993 939,307 1,839,042 Currency in circulation 814,626 836,836 856,821 Reverse repos 30,132 41,756 95,987 Treasury general 4,670 5,606 55,625 Treasury supplement 558,987 Reserve balances 6,794 3,831 220,762 Factors absorbing reserve funds Off balance sheet Securities lent to dealers 120,790 226,357

58

Stocks You know the stock market cratered and then recovered.

60

A reminder that lower p/d means a higher risk premium, quite sensible in a huge recession and the same as the higher credit spread. P/D didn’t change that much because D fell like a stone.

61

Earnings may be a better divisor, since price decline anticipates lower dividends next year. This means less of a screaming buy, higher ER

62

Both actual and implied volatility rose sharply. 80%

Both actual and implied volatility rose sharply. 80%! Lots of signs of distress, forced selling, illiquidity (negative serial correlation). Vol = 20 day backward looking average volatility of daily S&P500 index

. Vol = 20 day backward looking average volatility of daily S&P500 index.")

63

Vol = 20 day backward looking average volatility of daily S&P500 index

64

People thought volatility was temporary. “Safer in long run”

Source: CBOE.com

65

Does the crash mean that free markets failed

Does the crash mean that free markets failed? New instruments, toxic derivatives, financial innovation gone amok, etc.

67

Unused slides

68

Ideas

69

What is the worry? Home prices decline → defaults → mortgages worth less → banks insolvent Who cares? Great depression story 1: (Friedman) Banks fail → M1 declines Great depression story 2: (Bernanke) Banks fail → No banks to make loans -> savers can’t meet borrowers.

Banks fail → M1 declines. Great depression story 2: (Bernanke) Banks fail → No banks to make loans -> savers can’t meet borrowers.")

70

A credit crunch: Banking system cannot make new loans.

Interest rate Supply (savings) System Doesn’t Work Demand (investment, mortgages) Loans

System. Doesn’t. Work. Demand (investment, mortgages) Loans.")

71

View 2: A crunch, but in debt markets not banks.

72

View 3: Investor Fear + Recession

Supply Of risky debt Interest rate Demand Loans A fall in loans need not mean a credit crunch

73

Which is it? Banking system wants to lend, but cannot.

-Secretly undercapitalized, can’t get new capital. “Recapitalizing” banks would fix everything Banking system doesn’t want to lend because it can’t sell in dysfunctional debt markets. Nobody wants to lend because investors don’t want to hold risk.

74

Summary: Bank constraint vs. Credit market Or risk premium view

Loan Loan Little decline in banking system lending. Banks can and do raise equity. Banks can and do fail / get taken over. Treasury purchase/debt guarantee did not stop it in tracks. “Recapitalized banks” pay dividends, buy other banks. High risk premiums in nonfinancial, non-intermediated assets. Obvious huge problem in credit markets Nothing without Govt guarantee or direct purchase is selling

75

Summary so far: Huge risk premium in debt markets = Large demand for Treasury debt Risk premium: “precautionary savings”, lower “aggregate demand” = more demand for treasury or guaranteed debt. Policy #1 (basically good) : Fed and Treasury Accommodate demand for Treasury Debt/money Together they issue Trillions of Treasury/money to buy assets Act as missing intermediary Provide desired Gov’t debt without needing deflation

: Fed and Treasury Accommodate demand for Treasury Debt/money. Together they issue Trillions of Treasury/money to buy assets. Act as missing intermediary. Provide desired Gov’t debt without needing deflation.")

76

Policy #1 danger Fed is running the world’s biggest hedge fund.

Can we reverse all this without inflation? Will the Fed be the only intermediary for a generation? Is the Fed buying good, especially new, debt at market prices? True blue free-market objections

77

Bad Policy Ideas TARP to buy troubled assets on the open market

TARP to buy assets from banks at artificial prices Bank “recapitalization” without quick workout. Forced mortgage renegotiation: a $150,000 unemployment subsidy Bailout Contagion. S&L Government, Pension Funds, … Policy uncertainty, changing the rules of the game. Who will buy now? Government running the banks / credit system for a long time. Fiscal “stimulus.” “Do something.” It’s ok to be negative. The major danger is political, not economic.

78

Policy. Will the Treasury Plan work?

Supply Price Treasury Hope: Small purchase raises price a lot Finance experience: Huge purchase to move prices a little Demand Mortgage-backed securities

79

Credit Crunch – “undercapitalized” mechanics

1. Before 2. After Risk 100 10 Equity Equity 95 ! 5 90 90 Loan (Assets) = Debt = Debt 3. No new loans! 3. “Deleverage?” New loan 5 5 50 95 5 Sell. 50 90 New debt 45 5 = = 45

= Debt. = Debt. 3. No new loans! 3. Deleverage New. loan Sell New debt = = 45.")

80

Solutions? 4. “Recapitalize” 4. “Failure” = recapitalization 1. New

Equity 55 10 New loan 90 5 45 70 70 20 =? 2. New debt Fail, = = 95 50 90 = WaMu JPMorgan

81

What went wrong / needs to be fixed?

Amazing amount of overnight / short financing $100 $100 Joe Yes Not $100 Joe $1.10 $1 Joe $99 Sue $1.10 $99 Sue $1 Joe $98 Bob $1.10

82

Swaps, brokerage, etc. $100 $100 2. Value = 80 3. Value = 80 $100 Joe $1 $99 Sue $1 $99 Sue Who stops ? $98 Bob $1 1. Will this last? 2. Abandon Mark to Market? 3. Dynamic capital standards!

83

A credit crunch: banking system cannot make new loans.

Deposits, CDs, Stock Mortgage Demand (investment) Financial system (intermediary) Supply (saving) The financial system can slice, dice and transfer risk, but cannot bear risk. People must bear risk. A credit crunch: banking system cannot make new loans. Interest rate Supply Banking System Demand Loans

Financial system. (intermediary) Supply (saving) The financial system can slice, dice and transfer risk, but cannot bear risk. People must bear risk. A credit crunch: banking system cannot make new loans. Interest. rate. Supply. Banking. System. Demand. Loans.")

Similar presentations

“Shadow banking is a term used to describe banking institutions, practices.>")