Download presentation

Presentation is loading. Please wait.

1

It’s Crunch Time, Ben! The Financial Accelerator EH 447, 2008/9 Week 4-2 Albrecht Ritschl

2

“The Great Depression is the Holy Grail of Macroeconomics” Ben Bernanke, Essays on the Great Depression (2000)

")

3

Key economic concepts Yield differentials / credit spread : interest rate differential between two bonds of same maturity. –This type of spread measures credit default risk (if both bonds in same country and currency) Yield spread between corporate bonds and Treasury bonds

Yield spread between corporate bonds and Treasury bonds.")

4

Key economic concepts (cont’d) Cost of Credit Intermediation (CCI) –Information asymmetries between borrowers and lenders (Stiglitz & Weiss, 1981, extensive literature) –“Bad” mimic “good” borrowers –Credit rationing as an attempt to minimize incentive problems –CCI as result of monitoring, building long term relationships, enforcement cost etc

Cost of Credit Intermediation (CCI) –Information asymmetries between borrowers and lenders (Stiglitz & Weiss, 1981, extensive literature) – Bad mimic good borrowers –Credit rationing as an attempt to minimize incentive problems –CCI as result of monitoring, building long term relationships, enforcement cost etc")

5

Key economic concenpts (cont’d) Debt deflation, Irving Fisher (1933) Debt contracts written in nominal units [$, £ etc., w/o price index clauses] Price fall of underlying asset causes negative equity may cause firesale in case of debt default Feeds back on price declines of underlying asset

![Key economic concenpts (cont’d) Debt deflation, Irving Fisher (1933) Debt contracts written in nominal units [$, £ etc., w/o price index clauses] Price fall of underlying asset causes negative equity may cause firesale in case of debt default Feeds back on price declines of underlying asset](http://images.slideplayer.com/15/4607805/slides/slide_5.jpg "Key economic concenpts (cont’d) Debt deflation, Irving Fisher (1933) Debt contracts written in nominal units [$, £ etc., w/o price index clauses] Price fall of underlying asset causes negative equity may cause firesale in case of debt default Feeds back on price declines of underlying asset")

6

Debt deflation (cont’d) But if nominal debt is so bad, then why are such contracts written in the first place (instead e.g. of a profit share)? Gale and Hellwig (1985): because of high cost of / difficulties in verifying debtor’s true profits Even easier if debtor provides collateral

. Gale and Hellwig (1985): because of high cost of / difficulties in verifying debtor’s true profits Even easier if debtor provides collateral.")

7

Bernanke (1983) Great Depression aggravated by financial market problems Debt deflation of values of collateral (much like 2007-? housing slump) Nominal debt contract more risky, CCI Resort to complicated risk sharing contracts (then again, CCI ) or Just reduce lending, even to solvent customers, to reduce CCI

Nominal debt contract more risky, CCI Resort to complicated risk sharing contracts (then again, CCI ) or Just reduce lending, even to solvent customers, to reduce CCI.")

8

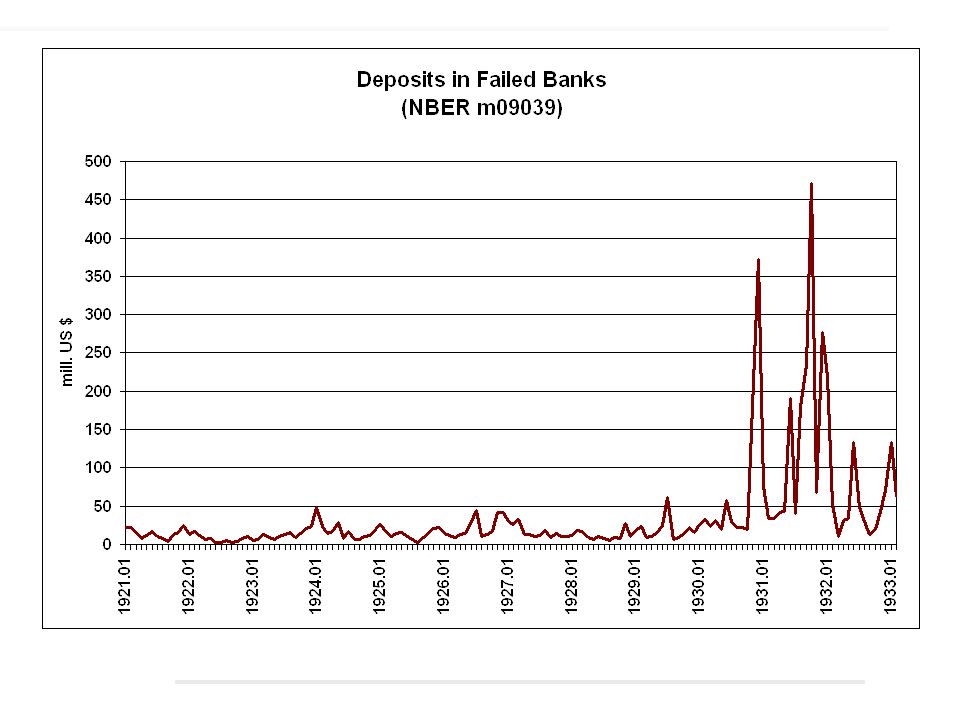

Bank of the United States Collapse, 12/1930

13

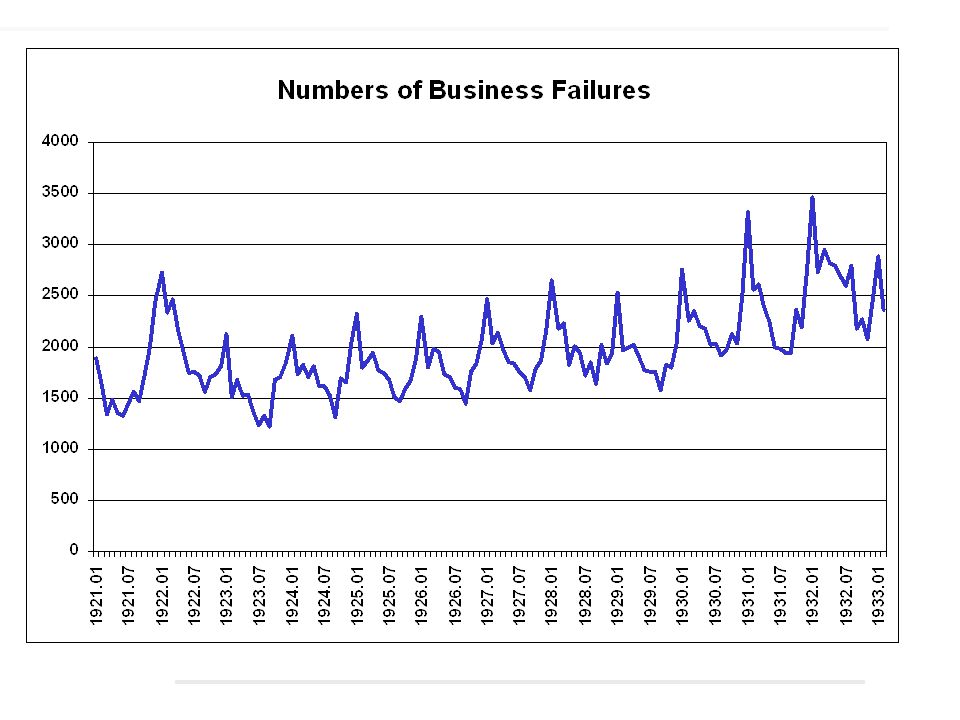

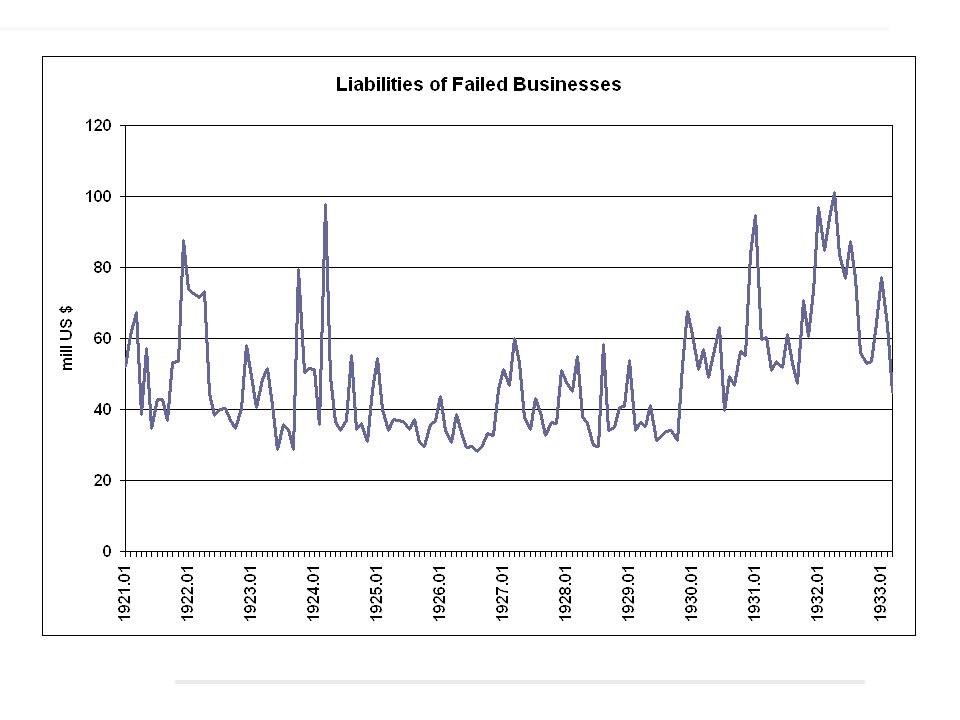

Some finer points Financial channel is not about 1929 Most banking problems not endogenous to fall in output Instead caused by exogenous events This is most important for comparison to 2008 Output may be endogenous to banking

14

U.S. crisis 1929: a timeline Since 1928: NYSE stock market boom August 1929: Upswing in real investment stops 24 and 29 October 1929: stock market crash Towards end of 1929: –Decline in output, price levels –Stock market quite resilient after initial shock –Bold steps by Fed to lower interest rates

15

U.S. crisis 1930: a timeline Throughout 1930: further slide into depression, very low interest rates June 1930: protectionist Hawley/Smoot tariff December 1930: Bank of U.S. fails, increased failures of rural banks

16

U.S. crisis 1931-32: a timeline Mid-1931: renewed banking panics (banking troubles also in Ctrl Europe) Sept 1931: another wave of panic (after UK’s departure from Gold Standard) Dec 1932: yet another panic (after UK, F default on wartime credits, F withdrawal of gold from NY)

Sept 1931: another wave of panic (after UK’s departure from Gold Standard) Dec 1932: yet another panic (after UK, F default on wartime credits, F withdrawal of gold from NY).")

17

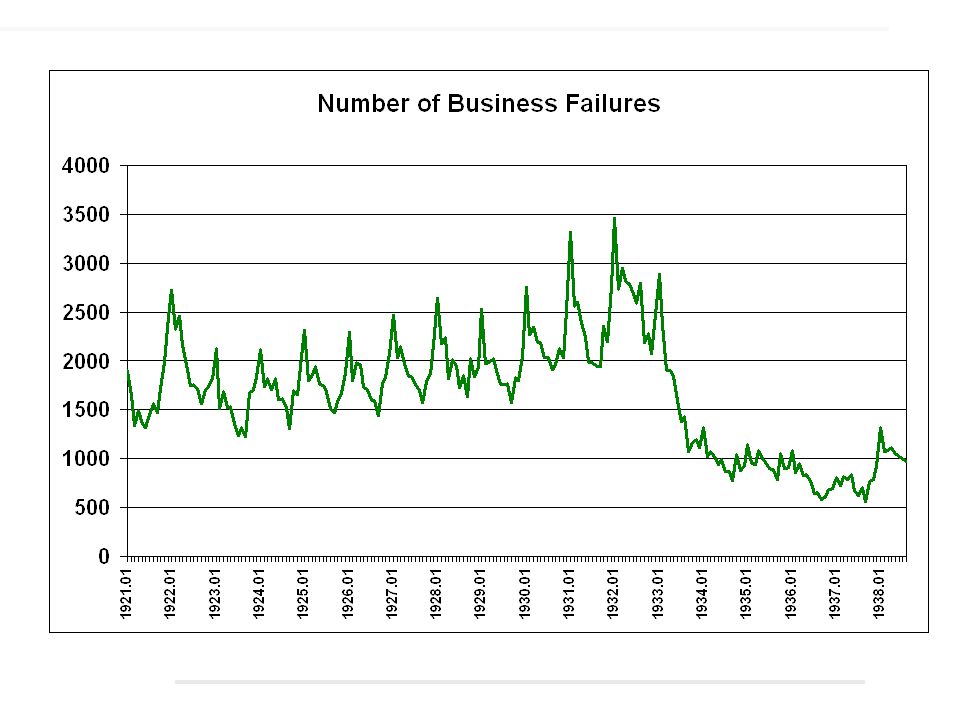

U.S. crisis 1933: a timeline March 1933: Emergency Banking Act (Bank Holidays, reopening of banks after federal inspection) June 1933: (2 nd ) Glass-Steagall Act (separation of deposit and investment banking, federal deposit insurance, state banking system, far-reaching regulation) Steep upswing sets in

June 1933: (2 nd ) Glass-Steagall Act (separation of deposit and investment banking, federal deposit insurance, state banking system, far-reaching regulation) Steep upswing sets in.")

18

International banking crisis 1931 Austrian Creditanstalt crisis in May German banking crisis in July –Bank run / bank holidays –Forced merger of two of top 5 banks –Part nationalisation of top 5 banks –Run on currency / capital controls –Hoover 1-year moratorium on reparations and foreign debt

19

Consequences of 1931 banking crisis UK loans frozen in Austria, Germany –Contributed to UK departure from Gold Standard in September US loans frozen German reparations suspended –Sent France, Belgium into depression 1932: UK, F default on WW1 loans from US –Causal for renewed U.S. banking crisis of early 1933

20

Conclusions on 1929/32 Causes not so clear Catastrophic depression and deflation Banking crisis only towards the end of depression Strong European element in banking crisis Special features: Gold Standard, reparations

Similar presentations

>")