Download presentation

Presentation is loading. Please wait.

2

Tax Credit & HOME Essentials 2008 Brought to you by IHFA Compliance Department

3

Contact Information Web Site: www.ihfa.orgwww.ihfa.org Email: Beckym@ihfa.orgBeckym@ihfa.org Email: Andrews@ihfa.orgAndrews@ihfa.org

4

GOOD MORNING

5

Applicant to Resident 1. Initial Interview 2. Processing the Application 3. Pre-Qualification/Estimating Gross Income 4. Verifying Information 5.Completing the Tenant Income Certification

6

The Initial Interview

7

Three Reasons To Have A Sit Down Interview At Application Creates A Personal Experience Allows You To Clarify Questions The Applicant May Have Saves You Time

8

Processing The Application

9

Look For Conflicting Information Anticipating Employment/ Claiming Zero Income Having A Checking Or Savings/No Assets Discrepancies With Student Status

10

Common Findings 1.Qualifying a household with a minor as the head or co-head 2.Discrepancies between the credit report and application 3.Household members that are 18 years old not being listed as an adult when they are still a dependent in the household 4.Not counting a qualified absent household member correctly

11

Pre-Qualification/Estimating Gross Income

12

Does Our Applicant Possibly Qualify? Is The Households Gross Income Under The Max? Does The Household Violate The Student Rule?

13

Time To Verify!

14

Three Forms of Verification Third Party (Attempt Required) Second PartySelf Certification

Second PartySelf Certification")

15

Third Party Verification Form Must Go From Management, To Source, Then Back To Management All Questions On The Form Need To Be Answered If A Question Is Left Unanswered, It Must Be Completed With A Clarification Form EIV is not a valid form of third party verification for tax credit

16

What’s Missing? How many items are missing from the employment verification? What are they?

17

Second Party Documentation Pay StubsAward LettersBank StatementsLegal Documents

18

When To Use Second Party Documentation 1.After attempting 3 rd party verification for a minimum of 2 weeks 2.When verifying Social Security 3.When a third party refuses to complete the form

19

Self Certification IHFA does not accept Self Certifications of income or assets with 2 exceptions: Self Employed Persons Under $5000 in assets

20

When To Use A Self Certification Here are some examples: 1.Pregnancy 2.Non-Receipt of Child Support 3.Zero Income 4.Zero Assets

21

Break Time!

22

Calculating Income

23

Employment Verification Which is greater, the standard calculation or year to date earnings?

24

Employment Verification for Merrill Lynch $7.20*30hrs*37wks = $7992 $7.30*30hrs&15wks = $3285 $ 11,277 OR YTD Earnings from 1/1/2008 thru 2/8/2008 is $1,586 So $1,586 / 6wks = $264.33 per week $264.33 * 52wks = $13,745.33

25

Social Security & Recurring Income What is the annual income of each source?

26

Social Security for Goldman Sachs $443.30 X 12 months = $5319.60 Recurring Cash Contribution $3000 Annually

27

Total Household Income Employment - $13,745.33 Social Security - $5,319.60 Recurring Income - $3,000 Student Income - $0 Total Income $22,064.93

28

Common Findings 1.Clarifications do not accompany third party verifications that have missing information 2.Social Security COLA is added to current year award letters 3.Second party documentation does not contain enough information 4.Year-to-date earnings not being calculated 5.Lack of zero income/anticipated income affidavits 6.Child support calculations 7.WHITE OUT

29

Questions On Income Calculations

30

Calculating Assets

31

Income From Assets (Bank Accts.) What is the income from both the checking and savings accounts?

What is the income from both the checking and savings accounts")

32

Morgan Stanley & Merrill Lynch’s Assets Checking Account–6 month Average = $12,932.40 $12,932.40 X 0.0% = $0.00 Savings Account-Current Balance = $5001.50 $5,001.50 X 2.5% = $125.04

33

Cash Value of Real Property What is the Cash Value of the House?

34

Calculating The House House current market value per tax assessment: $531,500 Is there a mortgage on this property? No To find cash value of house multiply FMV by 10% $531.500 X 10% = $53,150 Subtract the cost to convert to cash (10%) by the houses FMV $531,500 - $53,150 = $478,350

by the houses FMV $531,500 - $53,150 = $478,350.")

35

Total Income From Assets Asset Income from Asset Checking = $12,932.40 $0 Savings = $5001.50 $125.04 Real Estate = $478,350 $0 Total = $496,283.90 $125.04 Multiply by total assets by the passbook rate of 2%. $496,283.90 X 2% = $9925.68 The HIGHER of the two calculations is used for the households qualification

36

Common Findings 1.Using current value on a checking account 2.Filling out the Under $5000 Asset form incorrectly 3.Using previous year information on IRA’s, stocks, etc. 4.Disposing of assets for less than fair market value 5.Not following up on the interest rate for each account when over $5000 6.WHITE OUT

37

Questions About Assets

38

Tenant Income Certification

41

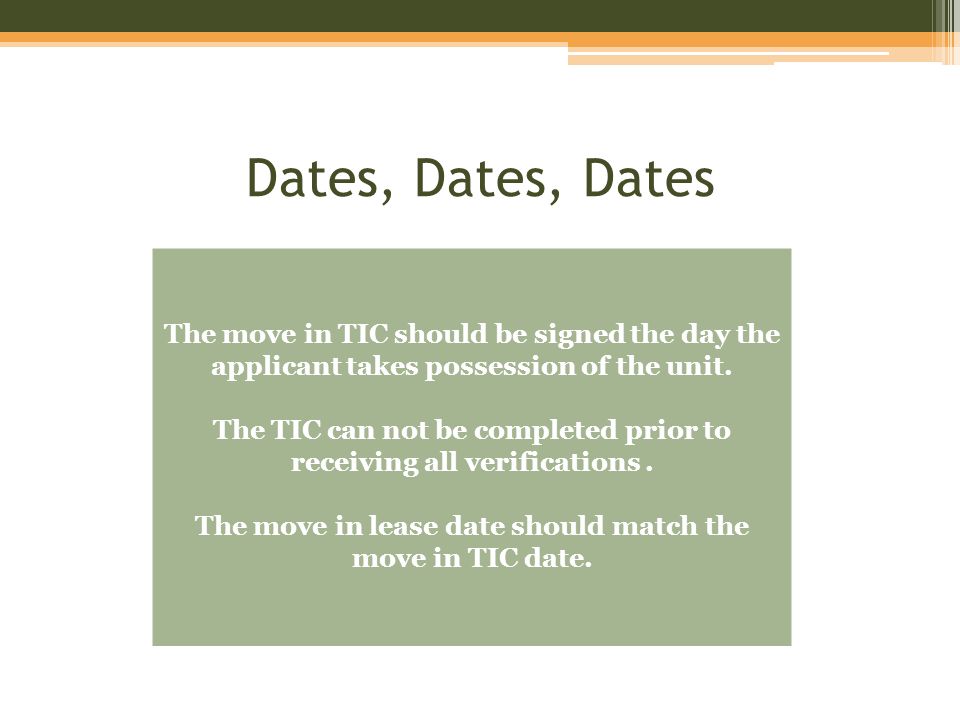

Dates, Dates, Dates The move in TIC should be signed the day the applicant takes possession of the unit. The TIC can not be completed prior to receiving all verifications. The move in lease date should match the move in TIC date.

42

Common Findings 1.Missing/incorrect BIN’s 2.Missing/incorrect income and rent limits 3.Rental assistance line not completed 4.Tax credit & HOME boxes not marked appropriately 5.Full time student status incorrect per household member (K-12) 6.Assets not listed on TIC correctly 7.Income listed under wrong column/combining income 8.Effective dates and signature dates incorrect

6.Assets not listed on TIC correctly 7.Income listed under wrong column/combining income 8.Effective dates and signature dates incorrect")

43

Adding A Household Member Post M/I

44

The Sister Joins The Household Shortly after your new residents move in, you notice someone coming and going from the unit on a constant basis that was not on the Certification and did not sign the lease. You inquire with the resident who this new person is and find out a relative has joined the household. It has only been a few weeks after they certified for affordable housing. What do you do?

45

Re-qualify The Household 1.Have new household member complete an application. 2.Verify income and assets. 3.Add income of new resident to original move in income. 4.Does this household still qualify for affordable housing?

46

Income Breakdown 1.Unemployment Compensation – $150 X 52 weeks = $7800 2. Student Income - $16,000 – $14,080 = $1,920 3. Bank Verification – Checking – $855.43 X 0% = $0 Savings - $603.38 X 2% = $12.07 CD - $11,000 X 4% = $440 CD - $10,000 X 4% = $400 Income from Assets= $852.07

47

Does The Household Still Qualify? Initial Households Qualifying Gross Income $31,990.61 New Household Members Income $ 10,572.07 New Total = $42,562.68 Max Income For 5 People = $39,480 The household no longer qualifies as low income.

48

Questions????????

49

LUNCH BREAK

50

Welcome Back

51

Re-Certification 1.IHFA is still requiring re-certifications on all households, but is currently researching the 100% waiver. 2.Re-certifications must be completed annually based on the residents move in date. 3.The effective date of a timely re- certification is the anniversary of the move in date.

52

What To Do With A Re-certification The first year re-certification is the best time to look for tenant fraud by comparing the re- certification paperwork to the original move in documents. Example: Resident certifies that they will not be seeking employment and less than two months later they obtain employment. At re- certification you find this on the employment verification. You would need to go back and see if this income source would have disqualified them for affordable housing.

53

Due Diligence and Tenant Fraud IHFA can not emphasize enough the importance of having an in-depth, all- inclusive application to cover owners and management from non- compliance. The IRS has stated that as long as O/A’s ask the appropriate questions at move in, then any findings are considered tenant fraud if those questions were answered untruthfully by the resident. Refer to Ch. 25 of the 8823 Guidebook

54

Questions

55

Student Status Vs. Student Income

56

Student Status 1. The IRS defines a full time student as anyone that attends a educational institution for 5 or more months in a CALENDAR year. (K-12 included) 2. Full-time student status is defined by the educational institution being attended. 3.All adult full-time students must have their status verified by a third party. (It is highly suggested to verify PT also)

2. Full-time student status is defined by the educational institution being attended. 3.All adult full-time students must have their status verified by a third party. (It is highly suggested to verify PT also).")

57

Household Of ALL Full-Time Students Households that consist of all full-time students do not qualify for Affordable Housing UNLESS they meet ONE of the four exemptions: 1.They are receiving assistance under Title IV of the Social Security Act 2. They are in a job training program receiving assistance under JTPA or a similar program 3. They are a single parent with children all of whom are students and such parents and children are not dependents of another individual. New Revenue Ruling 4. Married and able to file a joint tax return

58

Student Income What Income Counts? Grants & Scholarships What Income Is Excluded? Loans When Don’t You Count A Students Income? When They Are Over 23 WITH Dependents

59

NAUR & Miscellaneous

60

NAUR or the140% Rule 1.The 140% rule is a building or BIN rule. 2.The rule states that once a households income exceeds 140% of the max income limit, the next available unit must be rented to a low income household. 3.A 100% affordable property should not be affected by this rule as the next unit is always to be rented to a low income household.

61

Example Low Income 2 Bedroom Low Income 2 Bedroom Market 2 Bedroom Low Income 2 Bedroom Market 1 Bedroom Low Income 1 Bedroom Market 1 Bedroom Low Income 1 Bedroom

62

Swapping Unit Percentages 1. Swapping unit percentages is a good way of keeping households under 140%. 2. Swapping percentages can be done throughout the property, but must match unit size per the property’s regulatory agreement. 3. The only time a Market unit can be swapped for a low income unit is when it is in the same building/BIN and the market unit is the same size or smaller.

63

Vacant Unit Rule The vacant unit rule states that affordable units can be vacant and still credit eligible as long as the units are rent ready and reasonably being marketed. Any unit not turned in 30 days will be considered a violation of the VUR by IHFA.

64

Extended Use Agreement After the property’s initial 15 year compliance period, the extended use agreement begins. This agreement is between the owner and IHFA. A couple changes that start during the 16 th year are: - Reviews are done every three years and only 10% of units and files will be looked at. - Annual monitoring fees are reduced to 2/3 their original amount.

65

Common Findings 1.Full-time employee units not being utilized properly. 2.A full-time employee unit is considered common space and an owner can not charge for its use. 3.Transferring a resident that has exceeded 140%.

66

Break Time

67

Tax Credit With HOME When layering the HOME program with tax credit, some additional rules apply. Here are three major differences between HOME & Tax Credit: 1.HOME requires a 1 year initial lease term and specific HOME lease verbiage. 2.HOME requires 3 rd party verification of all household assets. 3. HOME requires all household members be legal residents of the United States and provide a copy of their Social Security card or resident alien card.

68

HOME Properties HOME properties must use the same income and asset procedures as tax credit. HOME income limits are not always the same as tax credit income limits and must be referenced separately. HOME rents are calculated based on their designation as either High HOME or Low HOME.

69

High and Low HOME Rent Calculations High HOME: Maximum HOME rents are the lesser of: the Section 8 Fair Market Rent OR 65% rent amount per bedroom size. Low HOME: Maximum HOME rents are the lesser of: 30% of the tenants monthly income OR 50% rent amount per bedroom size. CFR 24 Section 92.252(f)

.")

70

Low HOME Rent Calculation A households income is verified to be $12,000 annually. $12,000 / 12 months = $1000 $1000 X 30% = $300 The 50% rent limit for this county is $525 What rent amount do you use?

71

Open Forum

72

Thanks For Coming!

Similar presentations