Download presentation

Presentation is loading. Please wait.

1

Multiple Investment Alternatives Sensitivity Analysis

2

Given two or more investment alternatives, be able to identify the mutually exclusive alternatives. Given two or more mutually exclusive investment alternatives, be able to determine the best alternative by the present worth method the annual worth method the incremental rate-of-return Given a problem description, be able the breakeven point between two or more investment alternatives. Given a cash flow, be able to perform a sensitivity analysis on one or two parameters of the cash flow.

3

NPW > 0 Good Investment EUAW > 0 Good Investment IRR > MARR Good Investment Note: If NPW > 0 EUAW > 0 IRR > MARR

4

NPW A > NPW B Choose A Must use same planning horizon EUAW A > EUAW B Choose A Same Planning Horizon implicit in computation IRR A > IRR B Choose A Must use Incremental Rate-of-Return IRR B-A < MARRChoose A

5

Suppose we have two projects, A & B A B Initial cost$50,000$80,000 Annual maintenance 1,000 3,000 Increased productivity 10,000 15,000 Life 10 10 Salvage 10,000 20,000

6

A NPW(10) = -50 + 9(P/A,10,10) + 10(P/F,10,10) 50 9 9 10 0 123...

= (P/A,10,10) + 10(P/F,10,10)")

7

A NPW(10) = -50 + 9(P/A,10,10) + 10(P/F,10,10) = -50 + 9(6.1446) + 10(.3855) 50 9 9 10 0 123...

= (P/A,10,10) + 10(P/F,10,10) = (6.1446) + 10(.3855)")

8

A NPW(10) = -50 + 9(P/A,10,10) + 10(P/F,10,10) = -50 + 9(6.1446) + 10(.3855) = $9,156 50 9 9 10 0 123...

= (P/A,10,10) + 10(P/F,10,10) = (6.1446) + 10(.3855) = $9,")

9

B 80 12 20 0 12310... NPW(10) = -80 + 12(P/A,10,10) + 20(P/F,10,10)

= (P/A,10,10) + 20(P/F,10,10)")

10

B 80 12 20 0 12310... NPW(10) = -80 + 12(P/A,10,10) + 20(P/F,10,10) = -80 + 12(6.1446) + 20(.3855)

= (P/A,10,10) + 20(P/F,10,10) = (6.1446) + 20(.3855)")

11

B 80 12 20 0 12310... NPW(10) = -80 + 12(P/A,10,10) + 20(P/F,10,10) = -80 + 12(6.1446) + 20(.3855) = $1,445

= (P/A,10,10) + 20(P/F,10,10) = (6.1446) + 20(.3855) = $1,445.")

12

NPW A > NPW B Choose A

13

50 9 9 10 0 123... A EUAW(10) = -50(A/P,10,10) + 9 + 10(A/F,10,10)

= -50(A/P,10,10) (A/F,10,10)")

14

50 9 9 10 0 123... A EUAW(10) = -50(A/P,10,10) + 9 + 10(A/F,10,10) = -50 (.1627) + 9 + 10(.0627)

= -50(A/P,10,10) (A/F,10,10) = -50 (.1627) (.0627)")

15

50 9 9 10 0 123... A EUAW(10) = -50(A/P,10,10) + 9 + 10(A/F,10,10) = -50 (.1627) + 9 + 10(.0627) = $1,492

= -50(A/P,10,10) (A/F,10,10) = -50 (.1627) (.0627) = $1,492.")

16

12 20 0 12310... B EUAW(10) = -80(A/P,10,10) + 12 + 20(A/F,10,10)

= -80(A/P,10,10) (A/F,10,10)")

17

12 20 0 12310... B EUAW(10) = -80(A/P,10,10) + 12 + 20(A/F,10,10) = -80(.1627) + 12 + 20(.0627)

= -80(A/P,10,10) (A/F,10,10) = -80(.1627) (.0627)")

18

12 20 0 12310... B EUAW(10) = -80(A/P,10,10) + 12 + 20(A/F,10,10) = -80(.1627) + 12 + 20(.0627) = $238

= -80(A/P,10,10) (A/F,10,10) = -80(.1627) (.0627) = $238.")

19

EUAW A > EUAW B Choose A

20

Example: Suppose MARR is 10%. Suppose also that we can invest in T-bill @15% or we can invest in a 5 year automation plan. 100 115 NPW = 115(1.1) -1 - 100 = $4,545 100 30 51234 NPW = 30(P/A,10,5) - 100 = $13,724 AB B

= $4, NPW = 30(P/A,10,5) = $13,724 AB B.")

21

But this ignores reinvestment of T-bills for full 5-year period. 0 5 100 201,135 NPW = 201.135(P/F,10,5) - 100 = $24,889 A

= $24,889 A.")

22

Projects must be compared using same Planning Horizon

23

4,000 3 3,500 4,500 A NPW = -4 + 3.5(P/A, 10,3) + 4.5(P/F,10,3)

+ 4.5(P/F,10,3)")

24

4,000 3 3,500 4,500 A NPW = -4 + 3.5(P/A, 10,3) + 4.5(P/F,10,3) = -4 + 3.5(2.4869) + 4.5(.7513)

+ 4.5(P/F,10,3) = (2.4869) + 4.5(.7513)")

25

4,000 3 3,500 4,500 A NPW = -4 + 3.5(P/A, 10,3) + 4.5(P/F,10,3) = -4 + 3.5(2.4869) + 4.5(.7513) = 8.085 = $8,085

+ 4.5(P/F,10,3) = (2.4869) + 4.5(.7513) = = $8,085")

26

5,000 3 3,000 5,000 6 B NPW= -5 + 3(P/A,10,6) + 5(P/F,10,6)

+ 5(P/F,10,6)")

27

5,000 3 3,000 5,000 6 B NPW= -5 + 3(P/A,10,6) + 5(P/F,10,6) = -5 + 3(4.3553) + 5(.5645)

+ 5(P/F,10,6) = (4.3553) + 5(.5645)")

28

5,000 3 3,000 5,000 6 B NPW= -5 + 3(P/A,10,6) + 5(P/F,10,6) = -5 + 3(4.3553) + 5(.5645) = 10.888 = $10,888

+ 5(P/F,10,6) = (4.3553) + 5(.5645) = = $10,888")

29

Least Common Multiple Shortest Life Longest Life Standard Planning Horizon

30

A 4,000 3 3,500 4,500 4,000 6 4,500 NPW= -4 -4(P/F,10,3) + 3.5(P/A,10,6) + 4.5(P/F,10,3) + 4.5(P/F,10,6)

+ 3.5(P/A,10,6) + 4.5(P/F,10,3) + 4.5(P/F,10,6)")

31

A 4,000 3 3,500 4,500 4,000 6 4,500 NPW= -4 -4(P/F,10,3) + 3.5(P/A,10,6) + 4.5(P/F,10,3) + 4.5(P/F,10,6) = -4 +.5(P/F,10,3) + 3.5(P/A,10,6) + 4.5(P/F,10,6)

+ 3.5(P/A,10,6) + 4.5(P/F,10,3) + 4.5(P/F,10,6) = (P/F,10,3) + 3.5(P/A,10,6) + 4.5(P/F,10,6)")

32

A 4,000 3 3,500 4,500 4,000 6 4,500 NPW= -4 -4(P/F,10,3) + 3.5(P/A,10,6) + 4.5(P/F,10,3) + 4.5(P/F,10,6) = -4 +.5(P/F,10,3) + 3.5(P/A,10,6) + 4.5(P/F,10,6) = -4 +.5(.7513) + 3.5(4.3553) + 4.5(.5645)

+ 3.5(P/A,10,6) + 4.5(P/F,10,3) + 4.5(P/F,10,6) = (P/F,10,3) + 3.5(P/A,10,6) + 4.5(P/F,10,6) = (.7513) + 3.5(4.3553) + 4.5(.5645)")

33

A 4,000 3 3,500 4,500 4,000 6 4,500 NPW= -4 -4(P/F,10,3) + 3.5(P/A,10,6) + 4.5(P/F,10,3) + 4.5(P/F,10,6) = -4 +.5(P/F,10,3) + 3.5(P/A,10,6) + 4.5(P/F,10,6) = -4 +.5(.7513) + 3.5(4.3553) + 4.5(.5645) = 14.159 = $14,159

+ 3.5(P/A,10,6) + 4.5(P/F,10,3) + 4.5(P/F,10,6) = (P/F,10,3) + 3.5(P/A,10,6) + 4.5(P/F,10,6) = (.7513) + 3.5(4.3553) + 4.5(.5645) = = $14,159")

34

5,000 3 3,000 5,000 6 B NPW= -5 + 3(P/A,10,6) + 5(P/F,10,6)

+ 5(P/F,10,6)")

35

5,000 3 3,000 5,000 6 B NPW= -5 + 3(P/A,10,6) + 5(P/F,10,6) = -5 + 3(4.3553) + 5(.5645)

+ 5(P/F,10,6) = (4.3553) + 5(.5645)")

36

5,000 3 3,000 5,000 6 B NPW= -5 + 3(P/A,10,6) + 5(P/F,10,6) = -5 + 3(4.3553) + 5(.5645) = 10.888 = $10,888

+ 5(P/F,10,6) = (4.3553) + 5(.5645) = = $10,888")

37

NPW A > NPW B Choose A

38

4,000 3 3,500 4,500 A EUAW = -4(A/P,10,3) + 3.5 + 4.5(A/F,10,3) = -4(.4021) + 3.5 + 4.5(.3021) = 3.251 = $3,251 Note: NPW = 3,251(P/A,10,6) = 3,251(4.3553) = $14,159

(A/F,10,3) = -4(.4021) (.3021) = = $3,251 Note: NPW = 3,251(P/A,10,6) = 3,251(4.3553) = $14,159")

39

5,000 3 3,000 5,000 6 B EUAW = -5(A/P,10,6) + 3 + 5(A/F,10,6) = -5(.2296) + 3 + 5(.1296) = 2.500 = $2,500 Note: NPW = 2,500(P/A,10,6) = $10,888

(A/F,10,6) = -5(.2296) (.1296) = = $2,500 Note: NPW = 2,500(P/A,10,6) = $10,888")

40

Equivalent Uniform Annual Worth method implicitly assumes that you are comparing alternatives on a least common multiple planning horizon

41

Two alternatives for a recreational facility are being considered. Their cash flow profiles are as follows. Using a MARR of 10%, select the preferred alternative.

42

1 2 3 4 5 11 5 4 3 2 1 EUAW A = -11(A/P,10,5) + 5 - 1(A/G,10,5) = -11(.2638) + 5 - 1(1.8101) =.2881 = $288

(A/G,10,5) = -11(.2638) (1.8101) =.2881 = $288")

43

1 2 3 5 4 3 2 EUAW B = -5(A/P,10,3) + 2 + 1(A/G,10,3) = -5(.4021) + 2 + 1(.9366) =.9261 = $926

(A/G,10,3) = -5(.4021) (.9366) =.9261 = $926")

44

EUAW B > EUAW A Choose B

45

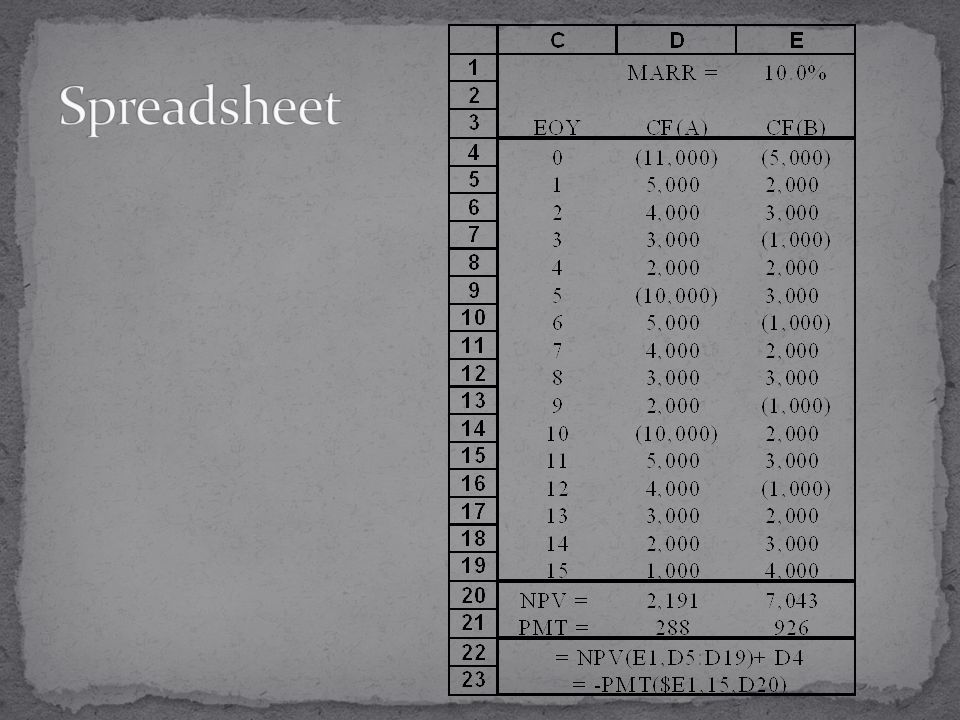

1 2 3 4 5 11 5 4 3 2 1 A B 1 2 3 5 4 3 2 Use Net Present Worth and least common multiple of lives to compare alternatives A & B.

46

1 2 3 4 5 11 5 4 3 2 1 A B 1 2 3 5 4 3 2 Use Net Present Worth and least common multiple of lives to compare alternatives A & B. NPW A = 288(P/A,10,15) = 288(7.6061) = $2,191

= 288(7.6061) = $2,191.")

47

1 2 3 4 5 11 5 4 3 2 1 A B 1 2 3 5 4 3 2 Use Net Present Worth and least common multiple of lives to compare alternatives A & B. NPW A = 288(P/A,10,15) = 288(7.6061) = $2,191 NPW B = 926(P/A,10,15) = 926(7.6061) = $7,043

= 288(7.6061) = $2,191 NPW B = 926(P/A,10,15) = 926(7.6061) = $7,043.")

49

Suppose we have two investment alternatives A 100 110 1 IRR A = 10% B 200 226 1 IRR B = 13%

50

Suppose we have two investment alternatives AB 100 110 200 226 11 IRR A = 10%IRR B = 13% IRR B > IRR A Choose B

51

Suppose we have two investment alternatives AB 100 110 200 226 11 IRR A = 10%IRR B = 13% IRR B > IRR A Choose B

52

Investment alternative B costs $200. If we forego B for $100 invested in A, we have an extra $100 which can be invested at MARR. If MARR = 20%,

53

Investment alternative B costs $200. If we forego B for $100 invested in A, we have an extra $100 which can be invested at MARR. If MARR = 20%, A 100 110 1 IRR A = 15% + 100 120 1 = 200 230 1

54

B 200 226 1 IRR B = 13% IRR A > IRR B Choose A 200 230 1 A IRR A = 15%

55

Suppose we have $100,000 to spend and we have two mutually exclusive investment alternatives both of which yield returns greater than MARR = 15%. A 50,000 60,000 1 IRR A = 20% B 90,000 106,200 1 IRR B = 18%

56

A 50,000 60,000 1 IRR A = 20% B 90,000 106,200 1 IRR B = 18% IRR A > IRR B Choose A

57

A 50,000 60,000 1 IRR A = 20% B 90,000 106,200 1 IRR B = 18% IRR A > IRR B Choose A

58

A 50,000 60,000 1 NPW A = -50 + 60(1.15) -1 = $2,170 B 90,000 106,200 1 NPW B = -90 + 106.2(1.15) -1 = $2,350 NPW B > NPW A Choose B

-1 = $2,170 B 90, ,200 1 NPW B = (1.15) -1 = $2,350 NPW B > NPW A Choose B")

59

Remember, we have $100,000 available in funds so we could spend an additional $50,000 above alternative A or an additional $10,000 above alternative B. If we assume we can make MARR or 15% return on our money, then

60

if we invest in A, we have an extra $50,000 which can be invested at MARR (15%). A 50,000 60,000 1 i = 20% 50,000 57,500 1 i = 15% += 100,000 117,500 1 i c = 17.5%

61

If we invest in B, we have an extra $10,000 which can be invested at MARR (15%). B 90,000 106,200 1 i = 18% 10,000 11,500 1 i = 15% += 100,000 117,700 1 i c = 17.7%

62

B 100,000 117,700 1 IRR B = 17.7% IRR cB > IRR cA Choose B 100,000 117,500 1 A IRR A = 17.5%

66

Break Even & Sensitivity

67

Suppose that by investing in a new information system, management believes they can reduce inventory costs. Your boss asks you to figure out if it should be done.

68

Suppose that by investing in a new information system, management believes they can reduce inventory costs. After talking with software vendors and company accountants you arrive at the following cash flow diagram. 1 2 3 4 5 100,000 25,000 i = 15%

69

Suppose that by investing in a new information system, management believes they can reduce inventory costs. After talking with software vendors and company accountants you arrive at the following cash flow diagram. 1 2 3 4 5 100,000 25,000 NPW = -100 + 25(P/A,15,5) = -16,196 i = 15%

= -16,196 i = 15%.")

70

Suppose that by investing in a new information system, management believes they can reduce inventory costs. After talking with software vendors and company accountants you arrive at the following cash flow diagram. 1 2 3 4 5 100,000 25,000 NPW = -100 + 25(P/A,15,5) = -16,196 i = 15%

= -16,196 i = 15%.")

71

Boss indicates $25,000 per year savings is too low & is based on current depressed market. Suggests that perhaps $40,000 is more appropriate based on a more aggressive market. 1 2 3 4 5 100,000 40,000

72

Boss indicates $25,000 per year savings is too low & is based on current depressed market. Suggests that perhaps $40,000 is more appropriate based on a more aggressive market. 1 2 3 4 5 100,000 40,000 NPW = -100 + 40(P/A,15,5) = 34,086

= 34,086.")

73

Boss indicates $25,000 per year savings is too low & is based on current depressed market. Suggests that perhaps $40,000 is more appropriate based on a more aggressive market. 1 2 3 4 5 100,000 40,000 NPW = -100 + 40(P/A,15,5) = 34,086

= 34,086.")

74

Tell your boss, new numbers indicate a go. Boss indicates that perhaps he was a bit hasty. Sales have fallen a bit below marketing forecast, perhaps a 32,000 savings would be more appropriate 1 2 3 4 5 100,000 32,000

75

Tell your boss, new numbers indicate a go. Boss indicates that perhaps he was a bit hasty. Sales have fallen a bit below marketing forecast, perhaps a 32,000 savings would be more appropriate 1 2 3 4 5 100,000 32,000 NPW = -100 + 32(P/A,15,5) = 7,269

= 7,269.")

76

Tell your boss, new numbers indicate a go. Boss indicates that perhaps he was a bit hasty. Sales have fallen a bit below marketing forecast, perhaps a 32,000 savings would be more appropriate 1 2 3 4 5 100,000 32,000 NPW = -100 + 32(P/A,15,5) = 7,269

= 7,269.")

77

Tell your boss, new numbers indicate a go. Boss leans back in his chair and says, you know....

78

I’ll do anything, just tell me what numbers you want to use!

79

1 2 3 4 5 100,000 A NPW = -100 + A(P/A,15,5) > 0

> 0")

80

1 2 3 4 5 100,000 A NPW = -100 + A(P/A,15,5) > 0 A > 100/(A/P,15,5) > 29,830

> 0 A > 100/(A/P,15,5) > 29,830")

81

A < 29,830 A > 29,830 1 2 3 4 5 100,000 A

82

SiteFixed Cost/YrVariable Cost A=Austin $20,000 $50 S= Sioux Falls60,000 40 D=Denver80,00030 TC = FC + VC * X

83

Break-Even Analysis 0 50,000 100,000 150,000 200,000 250,000 05001,0001,5002,0002,5003,0003,5004,000 Volume Total Cost Austin S. Falls Denver

84

A firm is considering a new product line and the following data have been recorded: Sales price$ 15 / unit Cost of Capital$300,000 Overhead$ 50,000 / yr. Oper/maint.$ 50 / hr. Material Cost$ 5 / unit Production 50 hrs / 1,000 units Planning Horizon 5 yrs. MARR 15% Compute the break even point.

85

Profit Margin = Sale Price - Material - Labor/Oper. = $15 - 5 - $50 / hr = $ 7.50 / unit 50 hrs 1000 units

86

Profit Margin = Sale Price - Material - Labor/Oper. = $15 - 5 - $25 / hr = $ 7.50 / unit 50 hrs 1000 units 1 2 3 4 5 300,000 7.5X 50,000

87

Profit Margin = Sale Price - Material - Labor/Oper. = $15 - 5 - $25 / hr = $ 7.50 / unit 50 hrs 1000 units 1 2 3 4 5 300,000 7.5X 50,000 300,000(A/P,15,5) + 50,000 = 7.5X 139,495 = 7.5X X = 18,600

+ 50,000 = 7.5X 139,495 = 7.5X X = 18,600.")

88

Suppose we consider the following cash flow diagram: NPW = -100 + 35(P/A,15,5) = $ 17,325 1 2 3 4 5 100,000 35,000 i = 15%

= $ 17, ,000 35,000 i = 15%")

89

Suppose we don’t know A=35,000 exactly but believe we can estimate it within some percentage error of + X. 1 2 3 4 5 100,000 35,000(1+X) i = 15%

i = 15%.")

90

Then, EUAW = -100(A/P,15,5) + 35(1+X) > 0 35(1+X) > 100(.2983) X > -0.148 1 2 3 4 5 100,000 35,000(1+X) i = 15%

+ 35(1+X) > 0 35(1+X) > 100(.2983) X > ,000 35,000(1+X) i = 15%")

91

NPV vs. Errors in A (20,000) (10,000) 0 10,000 20,000 30,000 40,000 50,000 -0.30-0.20-0.100.000.100.20 Error X NPV

(10,000) 0 10,000 20,000 30,000 40,000 50, Error X NPV.")

92

Now suppose we believe that the initial investment might be off by some amount X. 1 2 3 4 5 100,000(1+X) 35,000 i = 15%

35,000 i = 15%.")

93

NPV vs Initial Cost Errors (20,000) (10,000) 0 10,000 20,000 30,000 40,000 50,000 -0.30-0.20-0.100.000.100.20 Error X NPV

(10,000) 0 10,000 20,000 30,000 40,000 50, Error X NPV")

94

NPV vs Errors (20,000) (10,000) 0 10,000 20,000 30,000 40,000 50,000 -0.30-0.20-0.100.000.100.20 Error X NPV Errors in initial cost Errors in Annual receipts

(10,000) 0 10,000 20,000 30,000 40,000 50, Error X NPV Errors in initial cost Errors in Annual receipts")

95

Now suppose we believe that the planning horizon might be shorter or longer than we expected. 1 2 3 4 5 6 7 100,000 35,000 i = 15%

96

NPV vs Planning Horizon (30,000) (20,000) (10,000) 0 10,000 20,000 30,000 40,000 50,000 01234567 NPV PH

(20,000) (10,000) 0 10,000 20,000 30,000 40,000 50, NPV PH")

97

NPV vs Errors (20,000) (10,000) 0 10,000 20,000 30,000 40,000 50,000 -0.30-0.20-0.100.000.100.20 Error X NPV Errors in initial cost Errors in Annual receipts n=3 n=7 Planning Horizon MARR

(10,000) 0 10,000 20,000 30,000 40,000 50, Error X NPV Errors in initial cost Errors in Annual receipts n=3 n=7 Planning Horizon MARR")

98

Suppose our net revenue is composed of $50,000 in annual revenues which have an error of X and $20,000 in annual maint. costs which might have an error of Y (i=15%). 1 2 3 4 5 100,000 50,000(1+X) 20,000(1+Y)

,000 50,000(1+X) 20,000(1+Y).")

99

Suppose our net revenue is compose of $50,000 in annual revenues which have an error of X and $20,000 in annual maint. costs which might have an error of Y (i=15%). 1 2 3 4 5 100,000 50,000(1+X) 20,000(1+Y) You Solve It!!!

,000 50,000(1+X) 20,000(1+Y) You Solve It!!!.")

100

EUAW = -100(A/P,15,5) + 50(1+X) - 20(1+Y) > 0 50(1+X) - 20(1+Y) > 29.83 1 2 3 4 5 100,000 50,000(1+X) 20,000(1+Y)

+ 50(1+X) - 20(1+Y) > 0 50(1+X) - 20(1+Y) > ,000 50,000(1+X) 20,000(1+Y)")

101

EUAW = -100(A/P,15,5) + 50(1+X) - 20(1+Y) > 0 50(1+X) - 20(1+Y) > 29.83 50X - 20Y > -0.17 X > 0.4Y - 0.003 1 2 3 4 5 100,000 50,000(1+X) 20,000(1+Y)

+ 50(1+X) - 20(1+Y) > 0 50(1+X) - 20(1+Y) > X - 20Y > X > 0.4Y ,000 50,000(1+X) 20,000(1+Y)")

102

Unfavorable Favorable + 10%

103

Suppose we work for an entity in which the MARR is not specifically stated and there is some uncertainty as to which value to use. Suppose also we have the following cash flows for 3 mutually exclusive alternatives. tA 1t A 2t A 3t 0(50,000)(75,000)(100,000) 118,000 25,000 32,000 218,000 25,000 32,000 318,000 25,000 32,000 418,000 25,000 32,000 518,000 25,000 32,000

(75,000)(100,000) 118,000 25,000 32, ,000 25,000 32, ,000 25,000 32, ,000 25,000 32, ,000 25,000 32,000.")

104

tA 1t A 2t A 3t 0(50,000)(75,000)(100,000) 118,000 25,000 32,000 218,000 25,000 32,000 318,000 25,000 32,000 418,000 25,000 32,000 518,000 25,000 32,000 MARR =NPV 1 NPV 2 NPV 3 4.0%30,133 36,296 42,458 6.0%25,823 30,309 34,796 8.0%21,869 24,818 27,767 10.0%18,234 19,770 21,305 12.0%14,886 15,119 15,353 14.0%11,795 10,827 9,859 16.0%8,937 6,857 4,777 18.0%6,289 3,179 69 20.0%3,831 (235)(4,300)

(75,000)(100,000) 118,000 25,000 32, ,000 25,000 32, ,000 25,000 32, ,000 25,000 32, ,000 25,000 32,000 MARR =NPV 1 NPV 2 NPV 3 4.0%30,133 36,296 42, %25,823 30,309 34, %21,869 24,818 27, %18,234 19,770 21, %14,886 15,119 15, %11,795 10,827 9, %8,937 6,857 4, %6,289 3, %3,831 (235)(4,300)")

105

NPV vs. MARR (10,000) 0 10,000 20,000 30,000 40,000 50,000 0.0%5.0%10.0%15.0%20.0% MARR NPV NPV1 NPV2 NPV3

0 10,000 20,000 30,000 40,000 50, %5.0%10.0%15.0%20.0% MARR NPV NPV1 NPV2 NPV3.")

Similar presentations

projects. Firm ’ s capital budgeting decisions define.>")

Click here for Streaming Audio To Accompany Presentation.>")

2001 Contemporary Engineering Economics 1 Chapter 7 Present Worth Analysis Describing Project Cash Flows Initial Project Screening Method Present Worth.>")