Download presentation

Presentation is loading. Please wait.

1

Team #1 Andrew McDaniel Brad Schaefer Brandon Christian Robert Pace Ryan Schafer

2

Chief Business and Economics Characteristics The industry is driven by an infusion of technological innovation and long term sustainability. This is achieved through: Factory specialization Economies of scale Lowers costs for research and development Lowers costs to implement improvements 93% of Intel’s revenue is made in the micro processor market

3

Driving Forces of Change The changing market for applicable technology What technology are people using to complete tasks? What can make these tasks easier or more efficient for people? PCs vs. Tablets X86 vs chip sets

4

Driving Forces of Change Changing demands for technology Meet the needed demand Not necessarily about improving technology But about innovating a product to add value to the consumer DRAM/ SRAM memory vs. x86 processors Memory was the main focus of Intel x86 processors were a small division Switched focus to processing chips due to the boom of the PC market

5

Competitive Forces Intel has many competitors in the technological industry. They are: 1 st in the semiconductor industry 1 st in the x86 micro processing industry 4 th in the chipset industry (smart phones/tablets) Shift from PC purchases to tablet/ smart phone purchases

Shift from PC purchases to tablet/ smart phone purchases.")

6

Competitor Positions in the Industry Intel’s main stream of revenue comes through the micro processor industry Their sole competitor is AMD (Advance Micro Devices) They own 20% of the micro processing market vs. Intel’s 80% Samsung is leading the flash memory market and flat panel display market Intel has chosen not to compete in this market

7

Competitor Positions in the Industry In the semiconductor industry, Intel’s main competitors are SEC (Japan) 5.8% of the market share Toshiba (Japan) 4.7% of the market share Samsung (South Korea) 4.4% of the market share Texas Instruments (U.S.) 4.4% of the market share Intel currently has 16.1% of the market share

5.8% of the market share Toshiba (Japan) 4.7% of the market share Samsung (South Korea) 4.4% of the market share Texas Instruments (U.S.) 4.4% of the market share Intel currently has 16.1% of the market share")

8

Predictions of Competitive Moves To be successful, AMD will adapt a new, unified strategy just as Intel did during startup Attempt to acquire a secure customer base Sustain business in the long-run AMD will become more customer centric Find the needs that Intel does not meet and try to cater towards these Foster survival in the Industry

9

Predictions of Competitive Moves AMD will try to appeal to their customers through a lower cost approach They will also target the end-consumers to appeal to basic needs vs. expensive cutting edge technology

10

Key Success Factors Long-run success is valued much higher than quick profits This can be achieved through Factory specialization Economies of scale Consumer relations The ability to add customer value to innovative technological processes at a low cost Must focus on added customer benefits

11

Industry Attractiveness Will be attractive if: The entrant can overcome large start up costs Can meet the changing technological needs of consumers that key competitors are not focusing their resources on Can achieve economies of scale Can gain and compile knowledge of technological production

12

Strategic Effectiveness Invests Highly in R&D Department Continually Invests 15-20% of Revenue More than its competitors Recently developed the atom processor for IPhones and tablets Seeks the brightest talent to join the company 80,000 employees in over 28 countries Listed in Fortune 100’s companies to work for Only 2% turnover

13

Strategic Effectiveness Global Presence Operations in 63 countries Worlds largest Chip supplier Continue to Improve Manufacturing efficiency High raw material costs Tendency to oversupply market, needs to become more efficient

14

Revenue and R&D Intel Consistency Invests 15-20% of Revenue into Research

15

SWOT Analysis StrengthsWeaknesses Economies of scale Market Position/Brand Image Advanced Technological abilities Strong Management Dependence on Microsoft OS Over Supplying the market Customer Concentration OpportunitiesThreats Launching the Atom processor Partnerships Growing Global market Increasing Competition Volatile Industry High Raw Material Costs High Product Prices

16

Intel’s Options High market Pressure Large size and resources give power. Issue: Post-PC age Lowered stock prices Need for new technology Best option: Internal Changes “Build on previous investments & techniques” Refine strategy Creating new business value increasing efficiency design, office, manufacturing, enterprise, and services.

17

Locked in? Not locked into old strategy Growing industry Key is differentiation Strategy & products

18

Competitive Advantage 4 factors: Political Economic Social Technological Invention & Innovation Invention: Creation of new products and processes through the development of new knowledge of existing knowledge Innovation: The intentional commercialization of invention by producing and marketing a new good or service, or by using a new method of production.

19

Competitive Advantage Cont. Expanding business territory Developing new products Entering new technological markets “We are transforming from a company with a primary focus on the design and manufacture of semiconductor chips for PCs and servers to a computing company that delivers complete solutions in the form of hardware and software platforms and supporting services”

20

Intel Strategy Invention & Innovation Standardization: Development of new products. Improvements to existing ones. Combine and optimize: Manufacturing process technology Product design Leading-edge capacity Design tools Masks and packaging in-house

21

New Strategic Additions Business Scope: optimizing the whole business infrastructure including: applications, computing, storage, networking, and facilities Support: Design, Office, Manufacturing, Enterprise, and Services. Key Performance Indicators: Cost per service unit, Resource Utilization Service Quality steady achievement and innovation

22

New Strategic Additions Cont. Goal approach method: Total transformation NOT incremental changes. Investment decision model: compares current data center capabilities to a “best achievable model.” remove the conventional improvement mindset only focuses on incremental improvements “Using a new unit-costing financial model that enables us to benchmark ourselves and prioritize our investments” Broaden capability scope by identifying further groundbreaking innovations.

23

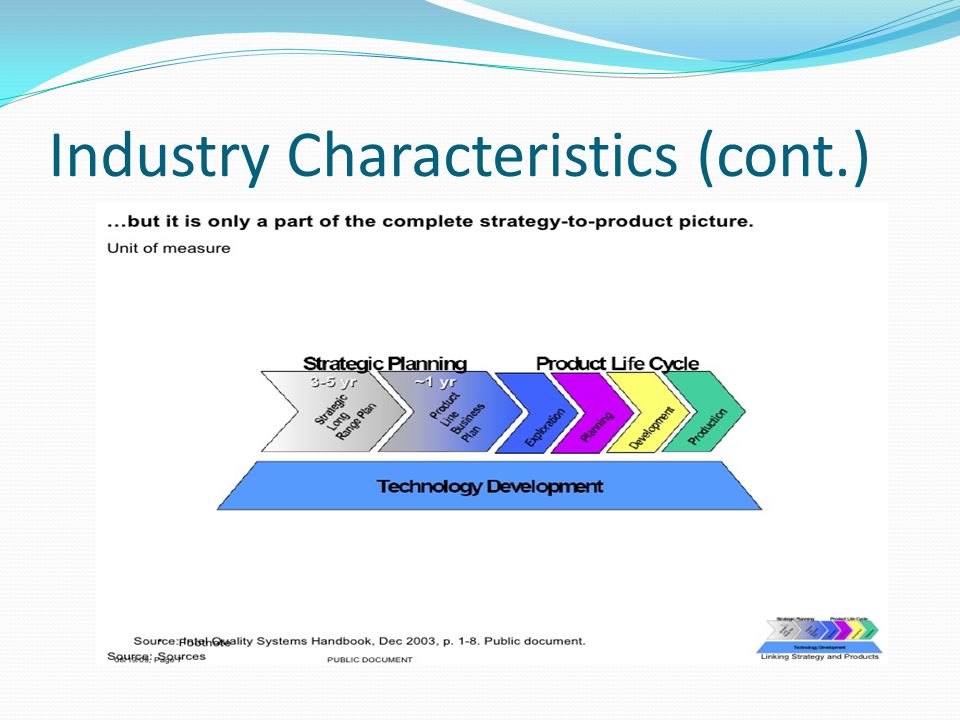

Industry Characteristics Strong Corporate Governance and Ethical Values Provide consumers, vendors, distributors, ect. With only the best products Unparalleled amount of time and money spent on developing and producing new products

24

Industry Characteristics (cont.)

")

26

Industry Changes Driving Forces Cloud Computing -Shift from a product focus to a service orientation Two Differences between Cloud Computing and other computing services 1.) Scalability 2.) Elasticity

Scalability 2.) Elasticity")

27

Industry Changes Driving Forces (cont.) Most cloud computing services are located in North America Europe has launched a $170 million public-private partnership -To help build the internet of the future with cloud computing as its key component China has launched a five year plan - integrating cloud computing as part of its initiative to develop strategic new industries

Most cloud computing services are located in North America Europe has launched a $170 million public-private partnership -To help build the internet of the future with cloud computing as its key component China has launched a five year plan - integrating cloud computing as part of its initiative to develop strategic new industries")

28

Competitive Forces at Work Constant Need to Keep up with the updating of technology. -Becomes outdated and antiquated after 6-8 months

29

Companies in the Strongest/Weakest Competitive Position Intel is in the best competitive position -Revenue of $53 billion last year -Reinvestment of %10 Billion back into the company for R&D Expansion throughout most of the World

30

Companies in the Strongest/Weakest Competitive Position (cont.)

")

31

AMD is the weaker company -Provides consumers with less products -Has lesser portion of the market - Has not expanded across world as well as Intel

32

Keys to Competitive Success Creating a demand for a product when there was not one before -Or; A Blue Ocean Intel is a technology node ahead of their competitors -How? Transitioning to lower Geometries

33

Industry Attractiveness and Prospects for Above Average Profitability Ranked 51 on Forbes Fortune 500 Reinvested $10.1 Billion into R&D Stock prices are on the rise about $23 a share Constant return with quarterly dividend payouts Corporate expansion and mergers through out the world

34

Economic Factors Intel’s Business cycle Product life cycle Accurately forecasting demand

35

Political factors Code of conduct CSR Suppliers Privacy of information Legal Issues

36

Social Factors Diverse workforce Leadership and development programs Education programs STAY WITH IT Initiative

37

Technological Factors Innovation is KEY NISSAN using the Intel® Atom™ processor Exploit the market Tap into new markets

38

Competitive Factors Competitors AMD, IBM, Oracle, TI, and Samsung Stay on track with Moore’s Law Hard to imitate Exclusive business with DigiPoS EPoS software

39

Geographical factors Santa Clara, California (HQ) Washington City, Oregon Foreign Markets Pros and cons Possible access to innovation by operating in countries with different cultures

Washington City, Oregon Foreign Markets Pros and cons Possible access to innovation by operating in countries with different cultures")

Similar presentations