Download presentation

Presentation is loading. Please wait.

1

BUSINESS INTERRUPTION: STRATEGIC CONSIDERATIONS FOR CATASTROPHIC LOSSES Jay W. Brown Hilary C. Borow Beirne, Maynard & Parsons, L.L.P. 1300 Post Oak Blvd., Suite 2400 Houston, Texas 77056 Fax: 713.960.1527 Telephone: 713.623.0887 March 2006

2

Business Interruption (BI) Coverage What it covers?What it covers? Whether it covers?Whether it covers? When it covers?When it covers?

3

What it covers?What it covers? If the policy pays, what is the payment based on?

6

Huh?

7

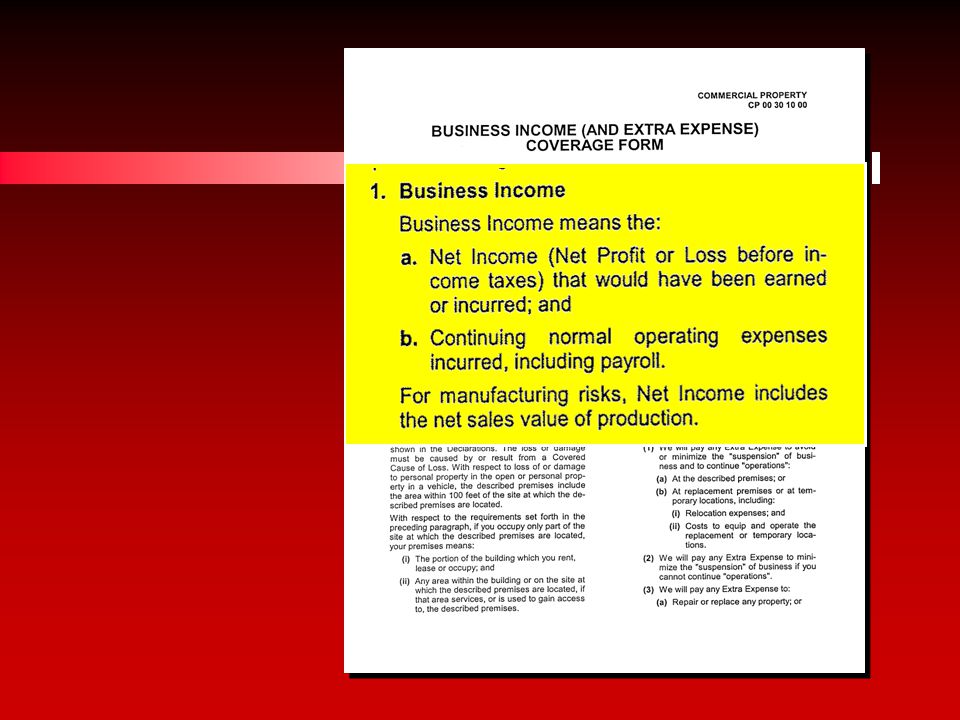

The Concept: Gross Earnings Coverage (earnings before taxes) (earnings before taxes)

(earnings before taxes)")

8

ISO ’ s business income coverage forms are essentially gross earnings-type forms. In the U.S., gross earnings coverage is the most commonly encountered type of BI insurance.

9

Gross earnings-type business interruption insurance covers the reduction in the net income, plus continuing normal expenses.

10

Compensation for reduced earnings. Expenses no longer incurred during the interruption are not covered. Continuing expenses, such as payroll, lease expenses, and expenses that continue to be incurred regardless of the business’ condition, are covered. Result:

11

Theoretical Goal: To protect the earnings an insured would have enjoyed had there been no interruption.

12

Rationale: To indemnify the insured for losses sustained from the inability to use the premises.

13

What is paid?What is paid? An estimate is paid — How much income would have been received if no loss had occurred?

14

Basis for estimate: The actual experience of the business prior to loss. The probable experience during the period of interruption had no loss occurred. What is paid?What is paid?

15

The fundamental BI coverage calculus is a projection... Ask: What if... ? provides a wonderfully fertile field....

16

Business projections can vary widely.... room for disagreement. Lurking not so far behind BI claim negotiations... “The Hammer.”

17

Article 21.55 — Prompt Payment Deadlines.

18

Whether it is covered? 3 Requirements for BI Coverage... Absolutely, positively must have all three.* * With one exception.

19

Core Coverage Grant:

20

3 Requirements: A.Must be direct physical damage to insured property caused by covered peril.

21

3 Requirements: A.Must be direct physical damage to insured property caused by covered peril. B.That physical damage must itself result in an interruption of insured’s business that causes actual monetary loss.

22

3 Requirements: A.Must be direct physical damage to insured property caused by covered peril. B.That physical damage must itself result in an interruption of insured’s business that causes actual monetary loss. C.The monetary loss must occur during the “Period of Restoration” — defined by the policy.

23

A Closer Look...

24

A Closer Look: A.Must be direct physical damage to insured property caused by covered peril.

25

2 Causation Links: covered peril physical property damage causes physical damage business interruption causes causes

26

BI must result directly from covered physical damage — not simply from the covered peril.

27

Example... Hurricane Wanda is bearing down on Galveston for the Labor Day weekend. Dangerous hurricane causes hotel cancellations, exodus of tourists, but only minor property damage.

28

Wallis case — In property damage claims, an insured can recover only for damage from covered perils. The insured has BOP to segregate. If the insured is unable to meet this burden to segregate, no recovery. Wallis v. United Services Automobile Ass’n., 2 S.W.3d 300 (Tex. App.–San Antonio 1999, pet. denied). Practice pointer...

. Practice pointer....")

29

With a catastrophic loss – the BI may be due to many factors. Some business loss may be caused by the peril itself, and some business loss is caused by the property damage.

30

Do not mix apples and oranges. Practice pointer...

31

Do not “lump in” BI due to covered property damages with the concurrent BI loss due to related factors. Practice pointer...

32

The insured must show: Practice pointer... The physical damage, which must itself be covered property damage, caused the loss of income.

33

Consider a refinery or manufacturing facility... Time-consuming maintenance items are “saved up” for scheduled shut- downs. With your catastrophic loss, show the specific BI due solely to the down time for repairs for the covered property damage caused by the catastrophe – not for the other main-tenance items that lengthened the shutdown. Practice pointer...

34

Total vs. Partial Suspension Most policies require a “necessary suspension” of business. The word “suspension” historically has not been a defined term in BI policies.

35

Majority Rule = Complete cessation of business is required. Texas follows the majority.

36

Example... Royal Indemnity Insurance Co. v. Mikob Properties Facts: Lakeside apartment complex, one building destroyed by fire; other two buildings had minor damage. Debris piles, ongoing construction, tenants leave.

37

Example... Mikob Properties argued the value of their quiet picturesque lakeside location was diminished.

38

Court held: Tenants’ voluntary exodus from other buildings was not a “necessary suspension of operations or tenancy,” b/c other buildings remained available for rent.

39

Many BI claims fail due to a lack of complete cessation of business operations. Keetch — Mount St. Helen’s eruption Practice pointer...

40

Complete cessation will no longer be required in many future claims. Coverage Forecast: Practice pointer...

41

Total vs. Partial Suspension Most policies require a “necessary suspension” of business. The word “suspension” historically has not been a defined term in BI policies.

42

Form CP 00 30 10 00 is a newer ISO BI form. An old term now has a new definition:

44

Complete cessation of business is not required with the newest ISO forms. “ Suspension ” includes “ slow down or cessation ” of business activities. Caveat: Newer ISO forms still not in widespread use.

45

C.The monetary loss must occur during the “ Period of Restoration. ”

46

When is the “ Period of Restoration ” ? “ Period of Restoration ” is a defined term, with a beginning...

47

Begins: 72 hours after physical loss (for BI claim). and an end... Period of Restoration...

. and an end... Period of Restoration...")

48

Ends: “The date when the property... should be repaired, rebuilt, or replaced with reasonable speed and similar quality;....”

49

Period of Restoration... Not: The actual time required to rebuild. (Although the actual time to rebuild would be probative.)

.")

50

Period of Restoration... is a hypothetical concept: Assuming, hypothetically, the property is rebuilt or repaired with reasonable speed, by when will it be completed?

51

Duane Reade, Inc. case: A drugstore operated within the World Trade Center. Example...

52

Drugstore contended the Period of Restoration was the actual time that would be required to rebuild the entire complex that would ultimately replace the World Trade Center. The insurer argued the Period of Restoration ended when the drugstore could have been rebuilt at some other location.

53

For the insurer: Obtain firm, bona fide bids from qualified contractors to rebuild the premises at a specific price by a time certain. Practice pointer...

54

For the insured: When rebuilding, document any and all reasons for any delays. The time actually required to rebuild will be strong evidence of the time it should have taken to rebuild. Practice pointer...

55

Since the Period of Restoration is a hypothetical concept, the property does not have to be actually repaired or rebuilt to recover. A business owner may wish to retire or permanently close the business at that time, but can still collect on the BI claim. Practice pointer...

56

Actions By Civil Authority A typical provision:

57

Examine the Language...

58

Covers: Insured’s own property not damaged, but BI loss due to order of civil authorities b/c of damage to other property.

59

A tall building with the bottom floor completely burned out. Order of Civil Authority: No one shall enter the building. Insured is an upper-floor tenant whose own premises were not damaged. Example...

60

Impairment of Ingress/Egress: Provides coverage for BI due to insured peril preventing ingress or egress.

61

Requirements for Ingress/Egress Coverage: Ingress or egress must be wholly impaired. Not sufficient that ingress or egress is simply more difficult.

62

Requirements for Ingress/Egress Coverage: Ingress or egress must be wholly impaired. Not sufficient that ingress or egress is simply more difficult. The event preventing ingress/egress must be an insured peril.

63

Requirements for Ingress/Egress Coverage: Ingress or egress must be wholly impaired. Not sufficient that ingress or egress is simply more difficult. The event preventing ingress/egress must be an insured peril. Lack of ingress/egress must be the cause of the BI loss. Physical damage may not be required – policies differ.

64

Extra Expense (EE) Coverage What it covers?What it covers? When it covers?When it covers?

Coverage What it covers What it covers When it covers When it covers")

65

What EE covers?What EE covers? Extra expenses necessary to remain in business or shorten down time, incurred because of the property loss.

66

Costs of renting temporary space to continue operations after the premises destroyed by fire. Example...

67

Three key criteria for EE coverage: Must be necessary Timing: incurred during period of restoration “but for” cause: but for a covered property loss, no EE incurred.

68

Conceptually EE rewards the insured for mitigating the BI loss: EE avoid or minimize downtime EE promotes continued operations of business.

69

Tropical Storm Allison floods basement of Bank of America building downtown. Destroys electrical supply to entire building. Law firm must relocate to continue functioning -- $ in EE. Relocation EE covered? Example...

70

No. Reason: Property damage itself not due to covered peril – usual exclusion for flood losses. Relocation expense covered?

71

Auto Dealership Destroyed by Tornado Costs to rebuild, repair dealer showroom?... No. Clean up debris costs? Security watches because of unsecured doors, windows? Example...

72

Overtime for EEs to assist in restoring operations? Hot meals brought in – reduced employee time away from job site? Unusual Advertising Expenses: “We are still in business!”

73

In summary... Consider actual claim. BI from a downtown Houston business due to Tropical Storm Frances.

74

Facts: The flooding formed a virtual moat around downtown Houston, severely curtailing access. A covered peril – a tropical storm. Insured suffered covered property damage – two blown out upper story windows, soaked carpets. Ingress/egress to downtown was severely hampered.

75

BI Coverage? No.

76

Reasons for no coverage: Ingress and egress were not completely impaired, just made considerably more difficult. There was no loss of ingress/egress to “The premises” – once you were downtown you could get there easy and go right in. No complete cessation of business – diminished operations continued. Policy required the loss of ingress/egress to be caused by damage to the property.

77

BUSINESS INTERRUPTION: STRATEGIC CONSIDERATIONS FOR CATASTROPHIC LOSSES Jay W. Brown Hilary C. Borow Beirne, Maynard & Parsons, L.L.P. 1300 Post Oak Blvd., Suite 2400 Houston, Texas 77056 Fax: 713.960.1527 Telephone: 713.623.0887 March 2006

Similar presentations

/principal. A GIA is a standard, typical document in the construction.>")