Download presentation

Presentation is loading. Please wait.

1

LIVE IN L.A. Your all access pass to complete Wealth Management Breaking up is hard to do Glenda Baker, Senior Financial Advisor Jane Shanks, Regional Vice-President

3

Agenda The facts Divorce models Knowing your boundaries Divorce professionals Case study How to help your clients

4

Divorce: the numbers 43% of marriages end in divorce before the 50 th wedding anniversary 70% of men and 58% of women will re-marry 35 year itch: “grey divorce” is a growing trend Increasing number of clients in 2 nd and 3 rd marriages Divorce rates 2.5 times higher for people in remarriages

5

Fears among baby boomers Being alone Failing again Becoming financially destitute Never finding another to live with or marry Staying angry or bitter over time Depression Not seeing children

6

Attribution on property transfers between spouses and common-law partners

7

Property transfers after separation or divorce No tax on transfers of a capital property to a spouse/former spouse if the transfer is in settlement of marital property rights Automatic rollover at ACB, unless elect out of rollover to transfer at FMC IT – 325R2 – Property Transfers after Separation, Divorce or Annulment

8

Property Transfers - residential real estate Family Circumstances & Goals Tax Implications Ownership & Use

9

Property Transfers: Who gets the Principal Residence Exception A family is allowed to designate one property as a “principle residence” Vacation property may qualify as the principal residence: “ordinarily inhabited” Can only claim one property as the principal residence for the same years of ownership Separated couple is not automatically entitled to two principal residence exemptions Must be living separate and apart for a full calendar year

10

Property Transfers: RRSPs and RRIFs Transfers as a result of separation or divorce can be tax deferred if: Transferred directly to another registered plan Transfer is made pursuant to a court order or written separation agreement Form T2220

11

Property Transfers: RRSPs and RRIFs Planning Point If there is a significant difference in marginal tax rates, this is an effective way to satisfy equalization obligations

12

Property Transfers: TFSAs Direct transfers as a result of separation or divorce are classified as “Qualified Transfers” if: Living separate and apart Transfer is made pursuant to a court order or written separation agreement No impact on either person’s contribution room

13

Planning Point If they withdraw and then pay dollar amount, the amount is added to the unused contribution room and can be re-contributed the following year Property Transfers: TFSAs

14

Deductibility of support payments Periodic payments made pursuant to a separation agreement or court order are generally deductible Lump sum support payments generally not tax deductible

15

Deductibility of support payments James v. The Queen, 2013 TCC 164

16

Divorce models Which one is right for you?

17

Kitchen Table Do-it-yourself Couple mutually agree on settlement Once in writing must seek independent legal advice

18

May be giving up valuable rights Quick, inexpensive and less outside influences Kitchen Table

19

Litigation Each party hires a lawyer to advocate their positions Lawyer’s duty to get best deal for client If agreement can’t be reached then court will decide

20

Court proceedings are public and can be very expensive Resolution for people who can’t settle Litigation

21

Mediation Couple meet with mediator to discuss issues and negotiate settlement Mediator doesn’t take sides, make decisions or give advice Still need independent legal advice

22

No advice from mediator Both parties have opportunity to be heard and assisted by a neutral party Mediation

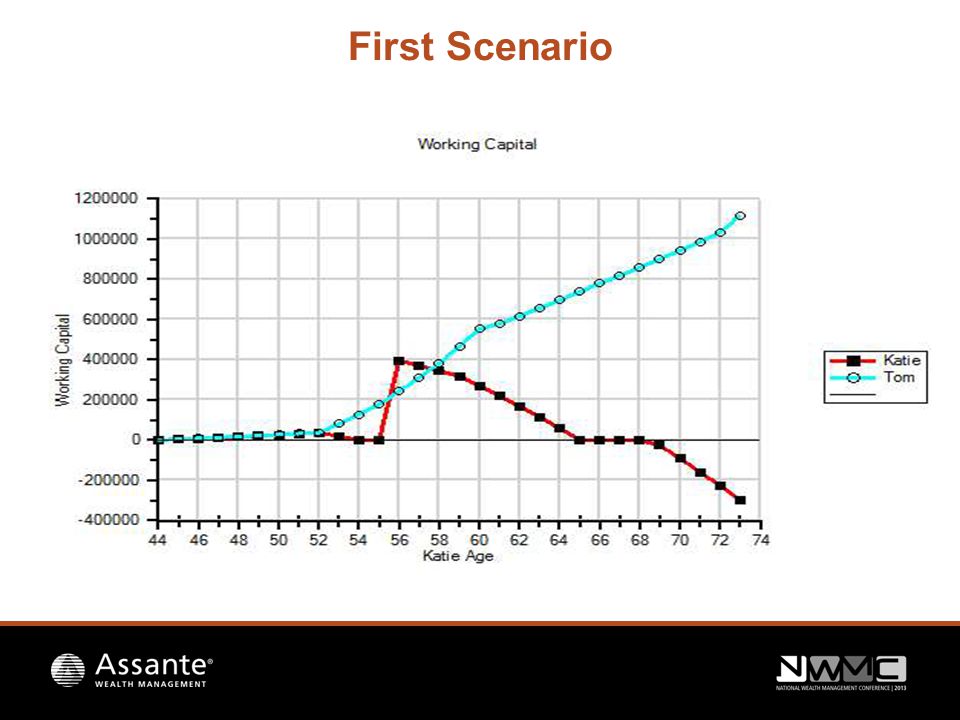

23

Collaborative Each party hires a lawyer specifically trained in collaborative process All formally agree to work together in a respectful and honest manner Encourages an understanding of each party’s interest and concerns

24

Collaborative Team must withdraw if unable to settle Couple focuses on ways to restructure so everyone’s needs are met

25

It is common for divorcing clients to ask for your help

26

Be very careful!

27

…tell clients how much support they will receive/pay …tell clients what assets they should receive …share information about one spouse to the other …provide legal, accounting or valuation advice – unless you have those credentials What can’t you do? DO NOT

28

Identify conflicts of interest Provide statements for assets as of date of separation and ACB (to owner) Help them understand that their financial life will change (now 2 households) Underwrite any new insurance needs once determined Separate clients’ file (his/hers) Refer to Divorce Professionals DO What can you do?

Help them understand that their financial life will change (now 2 households) Underwrite any new insurance needs once determined Separate clients’ file (his/hers) Refer to Divorce Professionals DO What can you do")

29

Divorce Professionals Family law lawyers Collaborative lawyers Family health professionals Child counsellors Mediators Business valuators Accountants Financial divorce professionals (FDS/CDFA)

")

30

Role of Financial Divorce Professionals Helps each spouse establish needs and hopes for the future Examines financial issues, does not provide legal advice Assists spouses in gathering documents Provides financial analysis taking into consideration inflation and tax consequences Counsels clients on developing realistic budgets

31

Role of Financial Divorce Professionals Assists lawyer in designing a settlement proposal that will maximize both spouses’ satisfaction Provides insight into pension plans, investments and insurance Determines assets that may not be divided Educates clients about tax and other financial consequences of retaining or giving up certain assets

32

Role of Financial Divorce Professionals Hands back clients to their financial advisor for implementation of settlement, future planning and asset management Provides unbiased presentations that show short-term and long-term financial impact of a proposed settlement Offers insight into pros and cons of various settlement proposals

33

Case Study Tom and Katie are splitting up!

34

Background Information Tom Aged 42 Engineer Salary $150K Tom Aged 42 Engineer Salary $150K Katie Aged 44 Stay at home Mom Katie Aged 44 Stay at home Mom 11-year relationship 2 children, ages 9 and 11 11-year relationship 2 children, ages 9 and 11 They have been separated over 2 years and have not yet completed a separation

35

Background Information Katie realizes she will have to go back to work at some point Tom knows that he has not been paying the right amount of child or spousal support Both Tom and Katie realize that Katie will need to upgrade her skills before re-entering the workforce Katie has told us she has huge trust issues

36

See any red flags so far?

37

What do they want? Ask and listen! Tom wants to keep his pension Katie wants to keep the house Tom wants to shorten the number of years he pays child support They both want their kids to maintain their activities and four years of post-secondary education

38

Gather information Provide them with a checklist of documents needed Assist with the completion of legal reports Form 13.1 Financial Statement Net Family Property Statement Future Budgets Order Pension Valuation Statement

39

Case Study A financial divorce professional identifies beyond the division of assets today to see what effect it will have on each party in their new life

40

What did the process look like? Detailed Calculations: Back spousal support Back child support Tax consideration Child tax credit consideration Detailed Calculations: Back spousal support Back child support Tax consideration Child tax credit consideration Compiled and analyzed all the information Completed the draft Net Family Proper Statement Ran scenarios based on their desired goals and division of assets

41

Our findings in Round 1 Yikes! We ran several scenarios around the back support issues, the equalization and their goals

42

Round 1 Mid-point spousal support for maximum time and back support at mid-point Katie returns to work after 1 year and education upgrade Equalization to Tom of $90K less back child support owing of $14K and spousal support of $22K

43

Round 1 Katie stays in house until youngest child finishes school Tom keeps pension and purchases a house using equalization payment for his down payment Katie’s education expense from her RRSP under the Life Long Learning Plan

44

Round 1 Outcome Tom has some minor cash flow shortages in the first couple of years but is fine and does not ever run out of money Katie is OK until age 69 then she runs out of money

45

First Scenario

47

Their Reaction Katie was shocked that she would owe Tom money in equalization Tom was shocked at the back support numbers They both broke down…crying…

48

What next? Remind them of their priorities and goals, short term and long term Brain storm other options

49

Long and short of it In our 15 th scenario we were able to reach an agreement and it became the financial settlement Here’s what it looked like…

50

Final Scenario – Net Worth

51

Final Scenario – Working Capital

52

What did this look like for each of them?

53

Pays spousal support for four more years at the mid-range for his salary Child support as per guidelines Forgoes equalization payment Tom No back support paid

54

Keeps his pension Shares day care expenses proportionately to his income when Katie returns to work Postpones buying a house until support payments are finished Tom RESP contributions set up proportionately to income

55

Tom He never runs out of money

56

Katie Child support and spousal support increases as per guidelines She does not have to pay Tom an equalization payment Keeps the house with the intention to sell when youngest leaves home Takes money from her RRSP to pay for education

57

Katie She never runs out of money

58

Conclusion Tom and Katie reached an agreement on a settlement that they helped orchestrate. It was based on their interests and needs. They commented that our neutral voice helped them to reach a settlement that they both felt comfortable with now and 25 years from now.

59

Conclusion

60

Thank you For advisor use only All charts and illustrations in this presentation are for illustrative purposes only. They are not intended to predict or project investment results. Assante Wealth Management’s advisory services are offered through Assante Financial Management Ltd., Assante Capital Management Ltd. and Assante Estate and Insurance Services Inc. Assante Estate and Insurance Services Inc. is owned by Assante Financial Management Ltd. and Assante Wealth Management (Canada) Ltd. ®The Assante symbol and Assante Wealth Management are registered trademarks of CI Investments Inc., used under licence.

Ltd. ®The Assante symbol and Assante Wealth Management are registered trademarks of CI Investments Inc., used under licence..")

Similar presentations

?>")

, 200 Park.>")

of the Income Tax Act which.>")