Download presentation

Presentation is loading. Please wait.

1

ADAPTED FOR THE SECOND CANADIAN EDITION BY: THEORY & PRACTICE JIMMY WANG LAURENTIAN UNIVERSITY FINANCIAL MANAGEMENT

2

CHAPTER 16 CAPITAL MARKET FINANCING: HYBRID AND OTHER SECURITIES

3

CHAPTER 16 OUTLINE Warrants Convertible Securities A Final Comparison of Warrants and Convertibles Reporting Earnings When Warrants or Convertibles Are Outstanding Securitization Credit Derivatives The 2007 Credit Crisis Copyright © 2014 by Nelson Education Ltd. 16-3

4

Copyright © 2014 by Nelson Education Ltd. 16-4

5

Warrants A warrant is a long-term call option issued along with a bond. Warrants are generally detachable from the bond and trade separately. When warrants are exercised, the issuing firm receives additional equity capital, and the original bonds remain outstanding. Copyright © 2014 by Nelson Education Ltd. 16-5

6

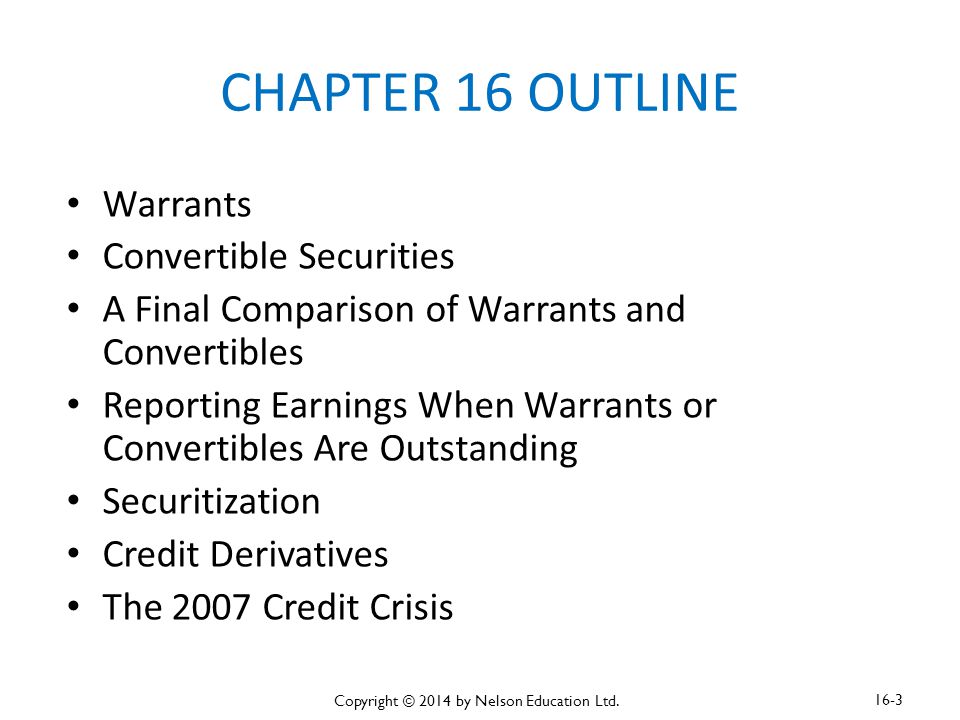

Initial Market Price of a Bond With Warrants Current stock price P0 = $20 Coupon rate of a regular 20-year annual payment bond without warrants rd=10% (i.e., ongoing rate) 20 warrants with a strike price of $25 each are attached to bond. The bond has an 8% coupon rate. The total package is sold for $1,000. Copyright © 2014 by Nelson Education Ltd. 16-6

7

Step 1: Find the Bond Price N I/YR PV PMT FV 20 10 80 1,000 Solve for bond price = -830 Because the 8% coupon rate is lower than the one (10%) associated with a regular bond without warrants, its price is lower than the regular bond price. Copyright © 2014 by Nelson Education Ltd. 16-7

8

Step 2: Calculate V Warrants V Package = V Bond + V Warrants = $1,000 V Warrants = $1,000 – V Bond = $1,000 – $830 = $170 V warrants = $170 = W(20) W = $170 / 20 = $8.50 Copyright © 2014 by Nelson Education Ltd. 16-8

9

Impact on the Package Value from Warrant Prices After issue, if the warrant price goes up to $10 each, the package will be worth: V = $830 + 20($10) = $1,030. Since this is $30 more than the selling price, the firm could have set lower interest payments whose PV would be smaller by $30 per bond, or it could have offered fewer warrants and/or set a higher strike price. Copyright © 2014 by Nelson Education Ltd. 16-9

10

Exercising Warrants Assume that the warrants expire 10 years after issue. When would you expect them to be exercised? Generally, a warrant will sell in the open market at a premium above its value if exercised (it can’t sell for less). Therefore, warrants tend not to be exercised until just before expiration. Copyright © 2014 by Nelson Education Ltd. 16-10

. Therefore, warrants tend not to be exercised until just before expiration. Copyright © 2014 by Nelson Education Ltd")

11

Exercising Warrants (cont’d) In a stepped-up strike price (also called a stepped-up exercise price), the strike price increases in steps over the warrant’s life. Because the value of the warrant falls when the strike price is increased, step-up provisions encourage in-the-money warrant holders to exercise just prior to the step-up. Since no dividends are earned on the warrant, holders will tend to exercise voluntarily if a stock’s payout ratio rises enough. Copyright © 2014 by Nelson Education Ltd. 16-11

12

Will the Warrants Bring in Additional Capital When Exercised? When exercised, each warrant will bring in an amount equal to the strike price, $25. This is equity capital, and holders will receive one share of common stock per warrant. The strike price is typically set some 20% to 30% above the current stock price when the warrants are issued. Copyright © 2014 by Nelson Education Ltd. 16-12

13

Expected Return to the Bond-With- Warrant Holders (And Cost to the Issuer) To take the privilege, you need to estimate when the warrants are likely to be exercised and the expected stock price on that exercise date. Although warrants give investors the right to buy stock at a predetermined price, investors make certain concession by accepting a lower return on the securities purchased with less protection. Copyright © 2014 by Nelson Education Ltd. 16-13

14

Benefits to the Issuing Firm The issuing firm obtains more money in addition to the funds received from the original issue of bonds because investors have to pay for the stock when they exercise the warrant. Gains by being able to sell the bond at a lower cost of capital than is incurred by selling straight bonds Copyright © 2014 by Nelson Education Ltd. 16-14

15

Use of Warrants in Financing There is some dilution of EPS when warrants are exercised because of the increase in the number of outstanding shares. Both the par value and the capital surplus of the firm increase. The debt stays on the balance sheet. Copyright © 2014 by Nelson Education Ltd. 16-15

16

Convertible Securities A bond or preferred stock that can be exchanged for a common stock at the option of the holder Convertible normally has a call feature that enables the issuing company to force investors to turn in the bond for a given number of shares of stock at a specified price. Copyright © 2014 by Nelson Education Ltd. 16-16

17

Assume the Following Convertible Bond Data: 20-year, 8.5% annual coupon, callable convertible bond will sell at its $1,000 par value; straight debt issue would require a 10% coupon. Call protection = 5 years and call price = $1,100. Call the bonds when conversion value > $1,200, but the call must occur on the issue date anniversary. P 0 = $20; D 0 = $1.00; g = 8% Conversion ratio = CR = 40 shares. Copyright © 2014 by Nelson Education Ltd. 16-17

18

What Conversion Price (PC) is Built into the Bond? Like with warrants, the conversion price is typically set 20% to 30% above the stock price on the issue date. P c = Par value # Shares received = $1,000 40 = $25 Copyright © 2014 by Nelson Education Ltd. 16-18

19

What is (1) the Convertible’s Straight Debt Value And (2) the Implied Value of the Convertibility Feature? PVFV 20 10 85 1,000 Solution: -872.30 I/YR PMT N Straight debt value: Copyright © 2014 by Nelson Education Ltd. 16-19

20

Implied Convertibility Value Because the convertibles will sell for $1,000, the implied value of the convertibility feature is: $1,000 – $872.20 = $127.70 The convertibility value corresponds to the warrant value in the previous example. Copyright © 2014 by Nelson Education Ltd. 16-20

21

What is the Formula for the Bond’s Expected Conversion Value in Any Year? Conversion value = CV t = CR(P 0 )(1 + g) t. For t = 0: CV 0 = 40($20)(1.08) 0 = $800 For t = 10: CV 10 = 40($20)(1.08) 10 = $1,727.14 Copyright © 2014 by Nelson Education Ltd. 16-21

(1 + g) t. For t = 0: CV 0 = 40($20)(1.08) 0 = $800 For t = 10: CV 10 = 40($20)(1.08) 10 = $1, Copyright © 2014 by Nelson Education Ltd")

22

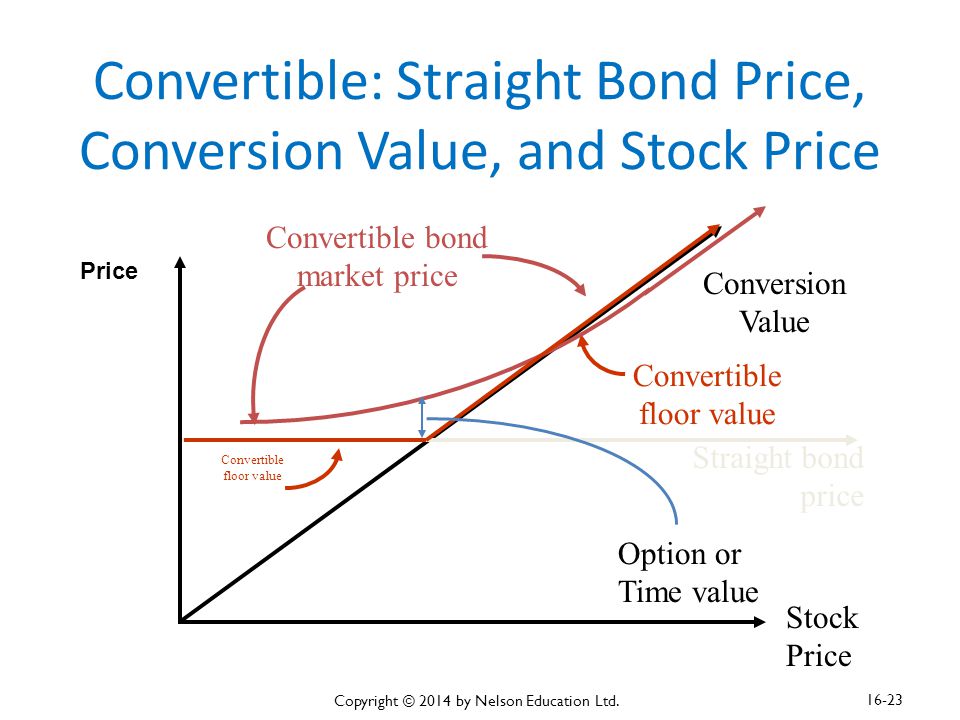

What is Meant By The Floor Value of a Convertible? What is the Floor Value at T = 0? At T = 10? The floor value is the higher of the straight debt value and the conversion value. Straight debt value 0 = $872.30 CV 0 = $800 Floor value at Year 0 = max[SV, CV] = max[872.3, 800] = $872.30 Copyright © 2014 by Nelson Education Ltd. 16-22

23

Convertible: Straight Bond Price, Conversion Value, and Stock Price Stock Price Straight bond price Conversion Value Convertible floor value Convertible bond market price Option or Time value Price Copyright © 2014 by Nelson Education Ltd. 16-23

24

What Is Meant By the Floor Value of a Convertible? What is the Floor Value at T = 0? At T = 10? (cont’d) At t = 10, straight debt value 10 = $907.83 CV 10 = $1,727.14 Floor value 10 = $1,727.14 A convertible will generally sell above its floor value prior to maturity because convertibility constitutes a call option that has value. Copyright © 2014 by Nelson Education Ltd. 16-24

At t = 10, straight debt value 10 = $ CV 10 = $1, Floor value 10 = $1, A convertible will generally sell above its floor value prior to maturity because convertibility constitutes a call option that has value. Copyright © 2014 by Nelson Education Ltd")

25

Copyright © 2014 by Nelson Education Ltd. 16-25

26

If the Firm Intends to Force Conversion on the First Anniversary Date After CV > $1,200, When is the Issue Expected to Be Called? PVFV 8 -800 0 1200 Solution: n = 5.27 I/YR PMT N Bond would be called at t = 6 since call must occur on anniversary date. Use the growth rate of 8% and the current version value of $800 for the calculation. Copyright © 2014 by Nelson Education Ltd. 16-26

27

What is the Convertible’s Expected Cost of Capital to the Firm? Input the cash flows in the calculator and solve for IRR = 11.8%. 01234560123456 1,000 -85 -85 -85 -85 -85 -85 -1,269.50 -1,354.50 CV 6 = 40($20)(1.08) 6 = $1,269.50. Copyright © 2014 by Nelson Education Ltd. 16-27

(1.08) 6 = $1, Copyright © 2014 by Nelson Education Ltd")

28

Does the Cost of the Convertible Appear to Be Consistent With the Costs of Debt and Equity? For consistency, need r d < r c < r s Why? Copyright © 2014 by Nelson Education Ltd. 16-28

29

Check the Values: Since r c is between r d and r s, the costs are consistent with the risks. r d = 10% and r c = 11.8% r s = D 0 (1 + g) P0P0 + g = $1.00(1.08) $20 + 0.08 = 13.4% Copyright © 2014 by Nelson Education Ltd. 16-29

P0P0 + g = $1.00(1.08) $ = 13.4% Copyright © 2014 by Nelson Education Ltd")

30

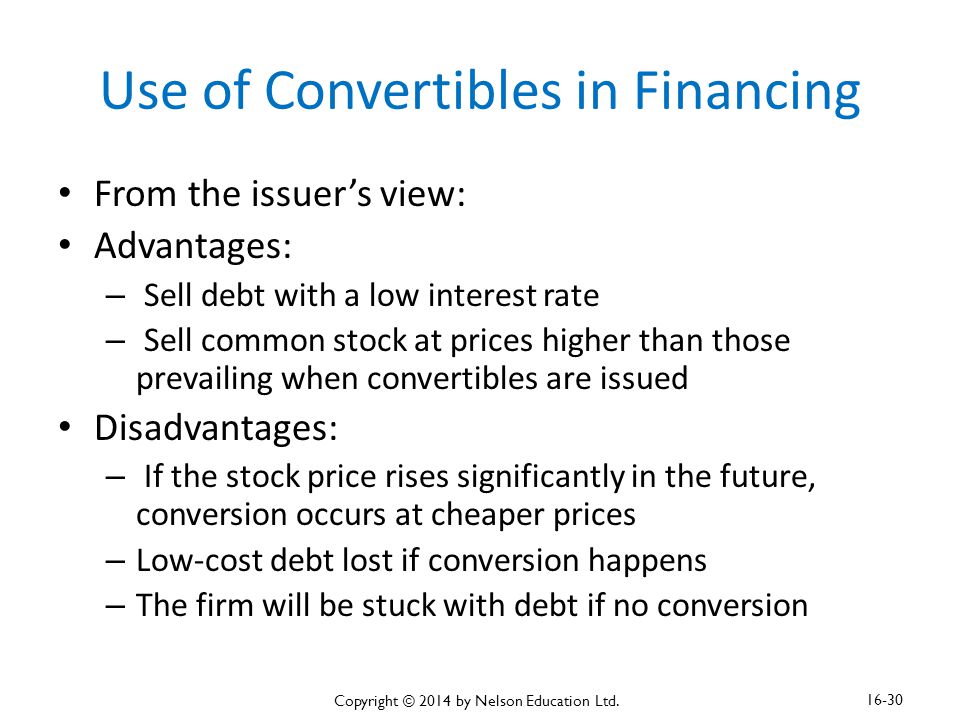

Use of Convertibles in Financing From the issuer’s view: Advantages: – Sell debt with a low interest rate – Sell common stock at prices higher than those prevailing when convertibles are issued Disadvantages: – If the stock price rises significantly in the future, conversion occurs at cheaper prices – Low-cost debt lost if conversion happens – The firm will be stuck with debt if no conversion Copyright © 2014 by Nelson Education Ltd. 16-30

31

Convertibles and Agency Costs Conflict between bondholders and shareholders: asset substitution (“bait and switch”) To protect themselves, debtholders will charge a higher interest rate regardless of the risk of a project. This agency cost can be reduced by using convertibles at lower rates. Copyright © 2014 by Nelson Education Ltd. 16-31

32

A Final Comparison of Warrants and Convertibles Warrants bring in new capital, while convertibles do not. Most convertibles are callable, while warrants are not. Warrants typically have shorter maturities than convertibles, and expire before the accompanying debt. Copyright © 2014 by Nelson Education Ltd. 16-32

33

A Final Comparison of Warrants and Convertibles (cont’d) Warrants usually provide for fewer common shares than do convertibles. Bonds with warrants typically have much higher flotation costs than do convertible issues. Bonds with warrants are often used by small start-up firms. Copyright © 2014 by Nelson Education Ltd. 16-33

34

A Final Comparison of Warrants and Convertibles (cont’d) Company with good future prospects can issue stock “through the back door” by issuing convertible bonds. – Avoids negative signal of issuing stock directly – Since prospects are good, bonds will likely be converted into equity, which is what the company wants to issue. Copyright © 2014 by Nelson Education Ltd. 16-34

35

Reporting Earnings When Warrants or Convertibles are Outstanding Two possible methods for reporting EPS when warrants/convertibles are outstanding: – basic EPS: number of shares actually outstanding – diluted EPS: all those “sweeteners” are exercised Diluted EPS is a hypothetical number. Investors are concerned with the “what if” questions on the dilution of earnings by option securities. Copyright © 2014 by Nelson Education Ltd. 16-35

36

Securitization A process of pooling and repackaging of assets such as mortgages into securities, which are sold to investors. Securities have greater liquidity. Refers to publicly traded financial instruments rather than to privately placed instruments. Copyright © 2014 by Nelson Education Ltd. 16-36

37

Asset Securitization Usually financial institutions are the companies called originator Originator sets up special purpose vehicle (SVP) that issues securities to investors Cash flows, such as interest and principal payments from the underlying assets, are then bundled and passed through to the holders of the securitized assets. After selling the asset to their affiliates, originators still act as the servicing agent. Copyright © 2014 by Nelson Education Ltd. 16-37

38

Copyright © 2014 by Nelson Education Ltd. 16-38

39

Asset-Backed Securities (ABS) Asset securitizations provide investors a wider choice of investable assets and more diverse portfolios to meet their needs. Examples include: – automobile loans – credit card receivables – equipment leases – residential mortgages – commercial papers Copyright © 2014 by Nelson Education Ltd. 16-39

40

Housing Market Asset securitization is extremely important in the housing market because banks free up capital in order to make more mortgages. While loan originators are free from illiquidity tied with mortgages, prepayment risk is an issue. Copyright © 2014 by Nelson Education Ltd. 16-40

41

Benefits for Investors Investors get access to financial assets such as car loans and mortgages that were not investable before. They can achieve portfolio diversification effect. They are able to choose a specific level of investment risk (choice of different tranches). Copyright © 2014 by Nelson Education Ltd. 16-41

. Copyright © 2014 by Nelson Education Ltd")

42

Credit Derivatives Is a contract that transfers credit risk from buyer to another seller It reduces credit risk for the banks, enabling them to increase the amount they can lend. Copyright © 2014 by Nelson Education Ltd. 16-42

43

Credit Default Swap Done to ensure payment in case of default by company The protection buyer makes a quarterly payment to the protection seller. The protection seller will make a lump sum payment to the protection buyer in case of default. Copyright © 2014 by Nelson Education Ltd. 16-43

44

Copyright © 2014 by Nelson Education Ltd. 16-44

45

Collateralized Debt Obligation (CDO) Bank CDOs are backed by loans, Credit enhancement: – Subordination: Senior tranches are established that have payment priority over junior tranches; the senior tranches have less default risk. – Cash collateral and cash reserves: Hold cash sufficient to pay some portion of the obligations. Copyright © 2014 by Nelson Education Ltd. 16-45

46

Copyright © 2014 by Nelson Education Ltd. 16-46

47

Credit Hedges Banks bundle their loans and asset securitization together as a means of passing the risk and return of corporate loans onto investors. Copyright © 2014 by Nelson Education Ltd. 16-47

48

The 2007 Credit Crisis Occurred when the flow of funds from investors slowed significantly. Banks could not raise enough funds for borrowers. Asset securitizations, CDOs, and credit derivatives are complicated, and people have misunderstood and misused them, contributing to the problems on the market. Copyright © 2014 by Nelson Education Ltd. 16-48

49

Lessons from Credit Derivatives Flawed correlation forecasts can have disastrous consequences. Relatively risky illiquid assets can be combined into new, lower-risk securities to attract investors and increase the availability of capital. As securities become more complex, they can outpace the market’s ability to properly assess their risk-return trade-off, which may result in huge losses. Copyright © 2014 by Nelson Education Ltd. 16-49

Similar presentations

>")