Download presentation

Presentation is loading. Please wait.

1

Dividend Policies in an Unregulated Market: The London Stock Exchange, 1895-1905 Fabio Braggion (Tilburg University & CentER) Lyndon Moore (Victoria University of Wellington)

Lyndon Moore (Victoria University of Wellington)")

2

A Study of Dividend Policies at London Stock Exchange, 1895-1905

3

1895-1905 How much did companies pay?

4

A Study of Dividend Policies at London Stock Exchange, 1895-1905 How much did companies pay? Who were the payers?

5

A Study of Dividend Policies at London Stock Exchange, 1895-1905 How much did companies pay? Who were the payers? Why did they pay?

6

Motivations: History: very little knowledge of dividend policies at the turn of the Twentieth century –On Britain: Church, Baldwin and Berry (1994) on the Consett Iron Company

on the Consett Iron Company")

7

Motivations: Finance: London Stock Exchange was an interesting environment –Very Low Taxation on Dividends

8

Very low taxation on dividends… Dividends were taxed only once… at a rate of 5% Dividends were taxed only once… at a rate of 5% Capital gains were tax free Capital gains were tax free Corporate income was treated as individual income… Corporate income was treated as individual income… …Companies just deducted the income tax when paying dividends to shareholders …Companies just deducted the income tax when paying dividends to shareholders

9

Very low taxation of dividends… No different tax rates between retail investors and institutions No different tax rates between retail investors and institutions –Friendly societies were an exception but their activities appear limited Less likely the existence of dividend clienteles around dividend paying companies Less likely the existence of dividend clienteles around dividend paying companies –Heavily taxed investors own low dividend shares –Investors with low tax rates own high dividend shares (Michaely and Womack, 1995; Allen, Bernardo and Welch, 2000)

")

10

Motivations: Finance: London Stock Exchange was an interesting environment –Also: No “Prudent Man” Regulation

11

We can focus on the first explanation: –Asymmetric Information (Bhattacharya, 1979; Miller and Rock, 1985; Jensen, 1986) It is not clear whether a stock price reaction to a dividend increase or decrease is a response to 1. an asymmetric information problem 2. a reshuffling of clienteles

12

Our Work: Collected information on dividend payments, accounting data and asset prices for about 300 public companies between 1895 and 1905 Collected information on dividend payments, accounting data and asset prices for about 300 public companies between 1895 and 1905 Identify dividend payers vs. non-payers Identify dividend payers vs. non-payers First attempt to evaluate different explanations of dividend policies… we will focus on asymmetric information First attempt to evaluate different explanations of dividend policies… we will focus on asymmetric information

13

We find: More than 100 years ago companies paid out as much as now More than 100 years ago companies paid out as much as now Profitable and more mature companies were more likely to pay dividends Profitable and more mature companies were more likely to pay dividends Dividends resolved an agency problem: managers wanted to show they “behaved” Dividends resolved an agency problem: managers wanted to show they “behaved”

14

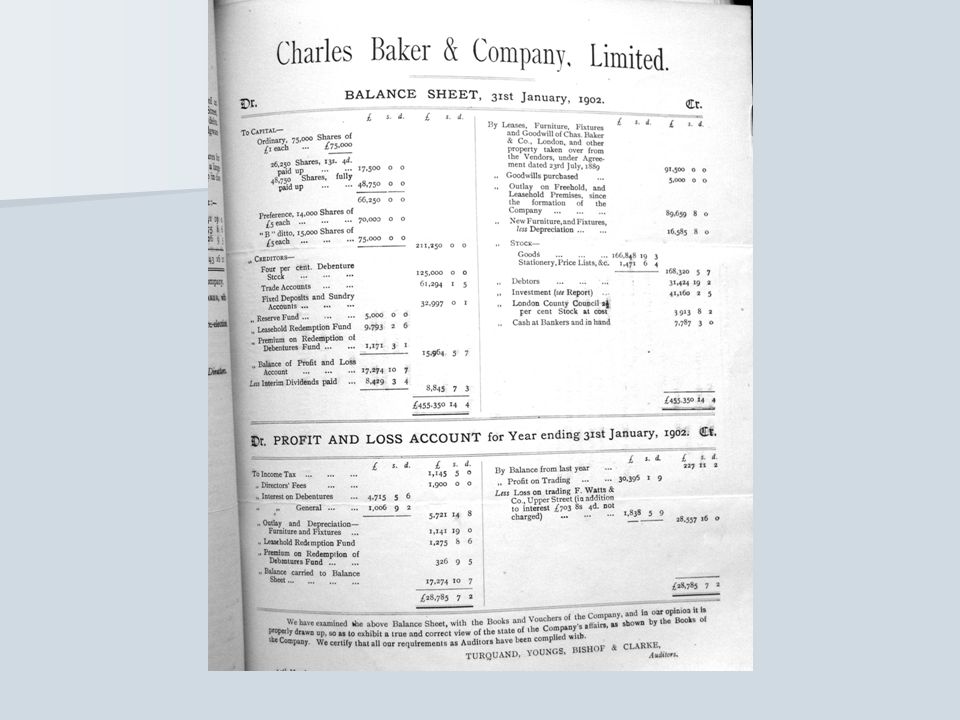

The Data About 300 British Companies quoted at the London Stock Exchange About 300 British Companies quoted at the London Stock Exchange From Annual Reports Information about: From Annual Reports Information about: –Earnings –Capital Structure –Dividend Payments –Book Value of the Assets –Dates of the Shareholders Meetings

15

The Data From the Times of London: From the Times of London: –Weekly Asset Prices –Dividend Announcement dates

16

Out of this data… …we also construct: A Weekly Stock Price Index for the London Stock Exchange A Weekly Stock Price Index for the London Stock Exchange Market to Book Ratio (Tobin’s Q) Market to Book Ratio (Tobin’s Q)

Market to Book Ratio (Tobin’s Q)")

23

How Much did they Pay?

24

…. Now and Then…. …. Now and Then…. Allen and Michaely (1990s): Allen and Michaely (1990s): –25 and 85% Our Results: Our Results: –73 and 92% How Much did they Pay?

: Allen and Michaely (1990s): –25 and 85% Our Results: Our Results: –73 and 92% How Much did they Pay .")

25

Characteristics of Dividend Paying Companies (Fama & French, 2001 DeAngelo, DeAngelo and Stultz, 2006) DeAngelo, DeAngelo and Stultz, 2006) Logit regression Dependent Variable: 1 if the company paid an ordinary dividend in 1901 0 if it did not 0 if it did not

DeAngelo, DeAngelo and Stultz, 2006) Logit regression Dependent Variable: 1 if the company paid an ordinary dividend in if it did not 0 if it did not")

26

We examine… … 2643 Companies/years… … 2643 Companies/years… –573 (22%) Non-Payers –2070 (78%) Payers

Non-Payers –2070 (78%) Payers")

27

Regressors: Contemporary and one year lagged profitability Contemporary and one year lagged profitability –Earnings after interest, depreciation and taxes. Reconstructed from the information provided in the balance sheets Size: Total Assets Size: Total Assets

28

Regressors: Growth Opportunities/ Life Cycles Idea: More mature companies should be more likely to pay dividends Age of the Company: Age of the Company: –Proxied by year of incorporation Earned Equity to Total Common Equity Earned Equity to Total Common Equity Past Growth: Past Growth:

30

Interpreting the Results: Contemporaneous Earnings are the most important determinant: Contemporaneous Earnings are the most important determinant: – increasing profitability from the first to the third ROA quintile would increase firm’s probability of paying dividends from 60% to 80% The effect of Age is not very strong The effect of Age is not very strong An standard deviation increase of Earned Equity to Common Equity increases the probability of paying dividends of about 27% An standard deviation increase of Earned Equity to Common Equity increases the probability of paying dividends of about 27% Cash to Total Assets has positive sign and it is marginally statistically significant Cash to Total Assets has positive sign and it is marginally statistically significant

31

Why did they pay? Evaluating Explanations We focus on explanations based on Asymmetric Information: –Dividends as a Costly Signal: Dividends are signals for good investment opportunities in the future –Dividends and Agency Theory Dividends are a way to discipline managers, especially in low growth/cash rich companies

32

Predictions Dividends as a Signal: –A dividend initiation or increase should be followed by a rise of stock returns –A dividend cut or omission should be followed by a decline of stock returns

33

Predictions Dividends and Agency: –A dividend initiation or increase should be followed by a rise of stock returns for low q companies –A dividend initiation or increase should have no effect (or generate of moderate rise) of stock returns for high q companies –A dividend omission or decrease should be followed by a decline of stock returns for low q companies –A dividend omission or decrease should have no effect (or generate of moderate declie) of stock returns for high q companies

of stock returns for high q companies –A dividend omission or decrease should be followed by a decline of stock returns for low q companies –A dividend omission or decrease should have no effect (or generate of moderate declie) of stock returns for high q companies")

34

Again Data Because of asset prices availability we focus on 63 companies Because of asset prices availability we focus on 63 companies We observe 390 dividend announcements over the period January 1901 through December 1905 We observe 390 dividend announcements over the period January 1901 through December 1905 Out of 390 announcements we have: Out of 390 announcements we have: o44 dividend omissions o13 dividend commencements (or recommencements) o115 dividend increases o133 dividend decreases o87 dividends left unchanged

o115 dividend increases o133 dividend decreases o87 dividends left unchanged")

36

Summary of the Results A dividend decrease or omission leads to a decline of 1.4-2.4% of Stock Returns A dividend decrease or omission leads to a decline of 1.4-2.4% of Stock Returns This effect is driven by low-Q companies This effect is driven by low-Q companies No effects on High-Q companies No effects on High-Q companies –There is support for the Agency Theory of Dividends

37

Conclusions and Future Directions Solve the “liquidity problem” Solve the “liquidity problem” Evaluation of Behavioral Explanations and evidence of “Catering” Evaluation of Behavioral Explanations and evidence of “Catering” Longer run analysis and price drift Longer run analysis and price drift

Similar presentations

Optimal Dividend Policy Conflicting Theories Other Dividend Policy Issues Residual Dividend Theory Stable.>")

- more dividends more value. Follows from.>")