Download presentation

Presentation is loading. Please wait.

1

Greystone Petroleum, L.L.C. Joe M. Bridges Chairman & CEO IPAA Private Capital Conference Houstonian Conference Center January 19, 2006

2

The Greystone Story Disciplined Founded in 1995 to target acquisitions in the Lower Cretaceous and Upper Jurassic, particularly in North Louisiana Good reserve potential at low finding costs Multiple producing zones Low operating costs Long history of production Evaluated all North Louisiana and East Texas fields for criteria – Sligo Field met all Patient and Persistent Began Sligo Field evaluation in April 1995 Made first acquisition proposal for Sligo Field in May 1996 Steadfastly pursued Sligo Field for the next six years, through several commodity price cycles Shell Capital: a faithful financial partner over the years Responsive Greystone: moved quickly on the opportunity Shell Capital: ready to help yet another time First Reserve: willing to work diligently despite tight schedule Joe M. Bridges Chairman & CEO Michael A. Geffert President & COO - Co-Founders of Greystone Petroleum LLC

3

Sligo Field Acquisition The Sligo Field fit management’s experience and philosophy Acquisition took years of on-again/off-again negotiations with prior owners Management’s first purchase offer made in May 1996 Multiple offers made in ensuing years Throughout cycles, Greystone remained disciplined in acquisition strategy and return targets Keys to closing the transaction Respect for Seller’s requirements Long-term relationship with Shell Capital First Reserve’s willingness to pursue the opportunity on short notice Timeline Initial meeting with First Reserve 12 December 2001 Devon confirms willingness to sell19 December 2001 Execution of PSA18 January 2001 Wire transfer of Purchase Price 8 March 2002

4

Sligo Field Attributes Acquisition Goals: Thoroughly studied by Greystone Great natural gas reserve potential Low finding costs, benign drilling Ample acreage for expansion Under-developed well density Great gas marketing opportunities Acquisition Attributes: Sligo Field, North Louisiana 99.8% natural gas Very large original-gas-in-place Multiple producing zones Multiple recompletion and drilling opportunities High realized prices, high Btu gas Multiple pipelines & markets Sligo Field

5

Sligo Field Overview The Sligo field represented 98% of proved reserves. Greystone had a large, contiguous acreage position over the crest of Sligo field. Operated acreage was predominately 100% working interest with 85% net revenue interest, all held by production. Greystone also had working interests ranging from 10% to 50%, averaging 41%, in acreage operated by EOG Resources. Sligo Field Summary LocationBossier Ph, Louisiana Date Discovered1938 Cumulative Prod.1.6 Tcf Prod. HorizonsRodessa, Pettit, Hosston, Cotton Valley Prod. Depth1,100’ to 9,600’ OperatorsGreystone, Hunt Petroleum, EOG Acreage15,976 Gross Operated Wells107 Non-Op. Wells58 Contract OperatorBrammer Engineering

6

Sligo Field Decline

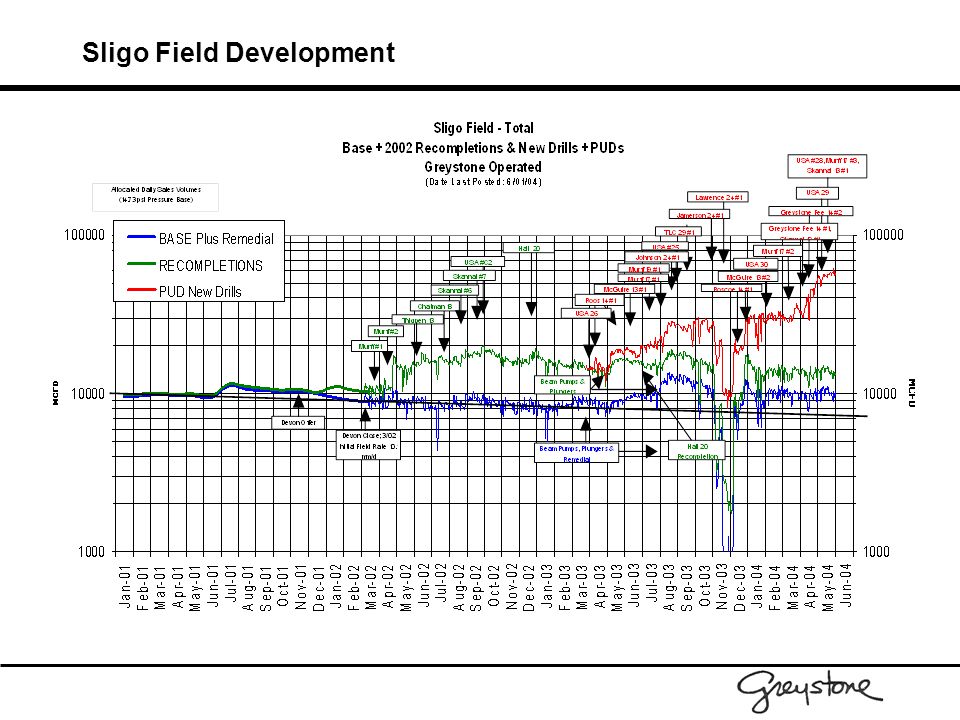

7

Sligo Field Development

9

Sligo Field Gas Marketing Greystone owned the gathering infrastructure on operated acreage. Facilities improvements included a pipeline purchased to connect both ends of the field, a pipeline purchased to improve sales delivery points, numerous pipeline and compressor horsepower additions and a 40 MMcfd refrigeration unit that enabled Greystone to meet even the most stringent pipeline specifications without third party processing. Greystone had contracted 89 MMcfd of delivery capacity, 44 MMcfd firm and 45 MMcfd interruptible. Greystone’s system improvements and improved flexibility substantially enhanced realized pricing and therefore acquisition economics. Natural Gas Markets Delivery PointsPipelines KoranGulf South TGT(Lonewa) TGT(Henry Hub) SNG(Perryville) MRT(Perryville) Transco(Henry Hub) CenterPointTGT MRT CPEGT TET Gulf South RegencySNG(Driscoll) Tennessee(Bear Creek)

TGT(Henry Hub) SNG(Perryville) MRT(Perryville) Transco(Henry Hub) CenterPointTGT MRT CPEGT TET Gulf South RegencySNG(Driscoll) Tennessee(Bear Creek).")

10

Sligo Field Divestiture Chesapeake Energy (ticker: CHK, exchange: New York Stock Exchange) News Release - 11-May-2004 Chesapeake Energy Corporation Announces Agreement to Acquire $425 Million of Natural Gas Properties OKLAHOMA CITY, May 11 /PRNewswire-FirstCall/ -- Chesapeake Energy Corporation (NYSE: CHK) today announced that it has entered into an agreement to acquire natural gas assets in the Ark-La-Tex region of northern Louisiana through the $425 million acquisition of the equity interests of Houston-based, privately-held Greystone Petroleum LLC. Greystone's major asset is its 16,100 gross acre contiguous leasehold position over the crest of the giant Sligo Field located in Bossier Parish, Louisiana. Discovered in 1938, Sligo has produced 1.6 tcfe of natural gas from the Rodessa, Pettit, Hosston and Cotton Valley formations at depths of 4,100 feet to 9,600 feet. Chesapeake has identified approximately 70 proved undeveloped and 75 probable and possible locations on the acreage. After allocating approximately $65 million of the purchase price to unevaluated leasehold and mid-stream gas assets, Chesapeake's acquisition cost per thousand cubic feet of gas equivalent (mcfe) of proved reserves will be $1.68. Including anticipated future drilling costs for fully developing the proved, probable and possible reserves, the company estimates that its all-in acquisition cost will be $1.94 per mcfe. The proved reserves have a reserves-to-production index of 13.0 years, are 98% gas, are 93% operated, and have current lease operating expenses of $0.39 per mcfe. Greystone's very low lease operating expenses (approximately $0.35 per mcfe below the industry average) create unusually high economic value per mcfe of proved reserves. Greystone was formed in 1995 by Joe M. Bridges and Michael A. Geffert who later were joined as equity holders by the private equity firm First Reserve Corporation to help fund Greystone's acquisition of interests in the Sligo Field in 2002. Greystone was advised in the sale to Chesapeake by Simmons & Company International and Griffis & Associates.

of proved reserves will be $1.68. Including anticipated future drilling costs for fully developing the proved, probable and possible reserves, the company estimates that its all-in acquisition cost will be $1.94 per mcfe. The proved reserves have a reserves-to-production index of 13.0 years, are 98% gas, are 93% operated, and have current lease operating expenses of $0.39 per mcfe. Greystone s very low lease operating expenses (approximately $0.35 per mcfe below the industry average) create unusually high economic value per mcfe of proved reserves. Greystone was formed in 1995 by Joe M. Bridges and Michael A. Geffert who later were joined as equity holders by the private equity firm First Reserve Corporation to help fund Greystone s acquisition of interests in the Sligo Field in Greystone was advised in the sale to Chesapeake by Simmons & Company International and Griffis & Associates..")

11

Greystone Oil & Gas LLP Joe M. BridgesMichael A. Geffert Managing Partner 1616 South Voss Road, Suite 400 Houston, Texas 77057

Similar presentations

>")