Download presentation

Presentation is loading. Please wait.

1

MicroinsuranceinBrazil

2

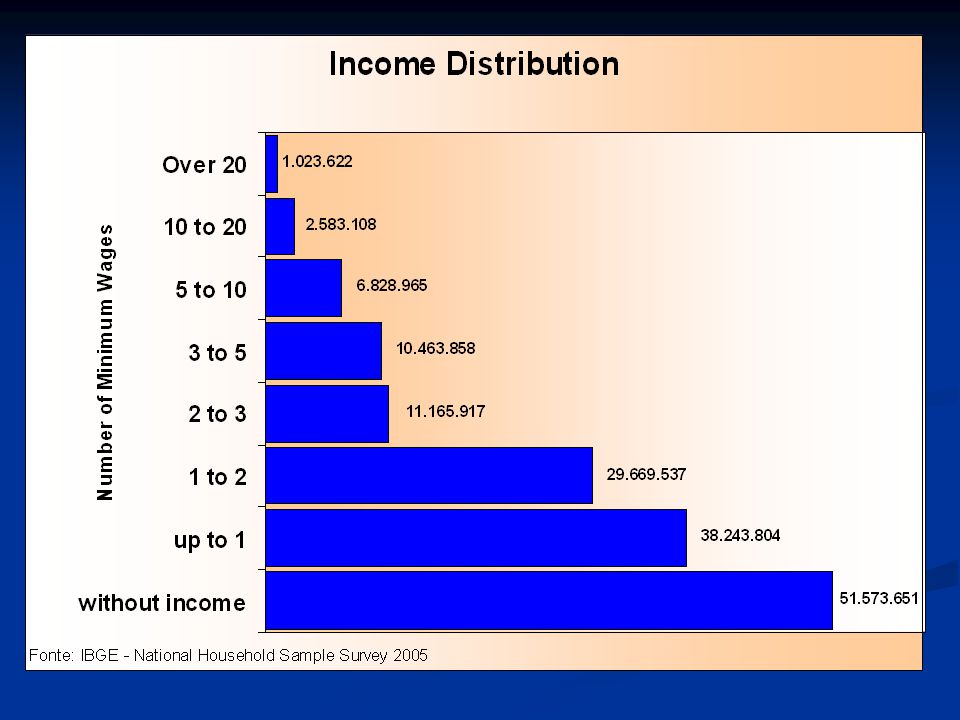

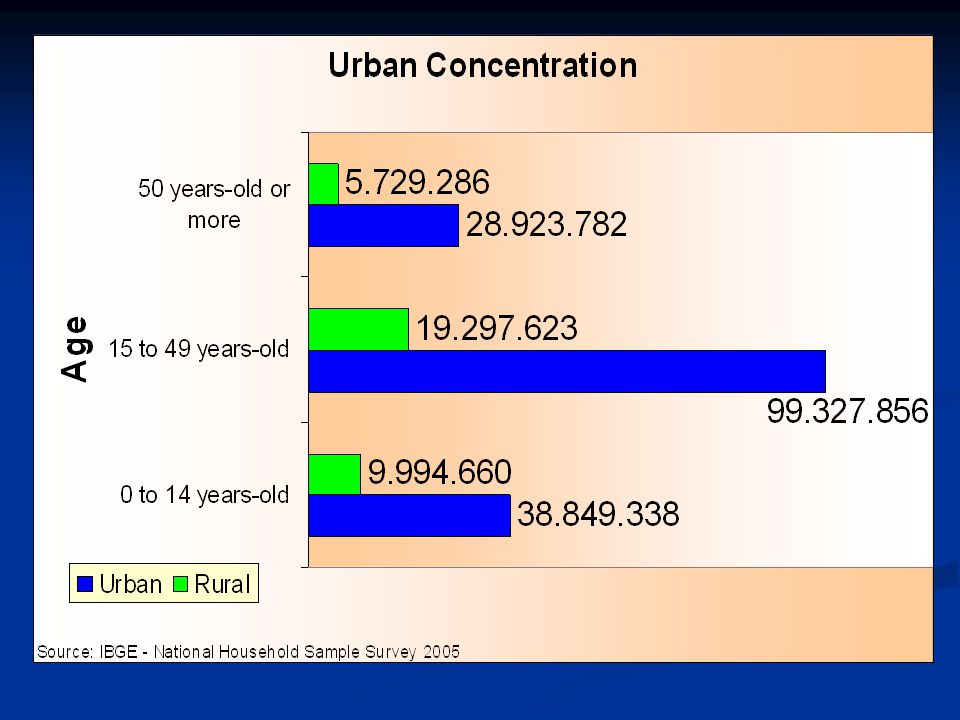

Brazilian Population Outlook

7

Brazilian Insurance Market Overview

8

1,00% 2,53% 3,10% 1994 1995 2006 Insurance, Open Private Pension Funds and Capitalization Sectors Participation in the GDP 2,97% 2000

9

Market Overview MarketNumber Insurance Companies 115 Open Pension Funds 26 Capitalization Companies 18 Insurance Agents (Individuals) 39.518 Insurance Agencies (Companies) 22.131

Insurance Agencies (Companies)")

10

Market Premium Evolution ( millions R$)... 1,00% 1994 1995 32.758 52.308 56.927 64.607 2005 2000... 19952006 1999 2004 28.259 16.331 10.035 US$ 29,676 MM - 2006 US$ 2,1771...

11

MARKET GROWTH OPENING OF THE REINSURANCE MARKET- 2007. PRODUCT DIVERSIFICATION THE MODERNIZATION OF THE REGULATORY AND SUPERVISORY PROCESS Brazilian Market Perspectives

12

Microinsurance or “Seguro Popular” in Brazil: Included in the Brazilian Government policy for micro-finances

13

Government Policy for Microinsurance General Insurance: products for the low- income people and for the formal and informal “micro-entrepeneurs” (SUSEP) Rural Area: products to protect “low-income family farmers” (MDA – Ministry of Agrarian Development)

Rural Area: products to protect low-income family farmers (MDA – Ministry of Agrarian Development)")

14

SUSEP’s First Actions End of 2003 – internal discussions aiming at the design of simple and low-cost products September/2004 - Circular SUSEP 267/2004 – “popular” group life insurance product November/2006 - Circular SUSEP 306/2006 - “popular” automobile product

15

Parallel Incentives Alternative distribution channels: “bankassurance”, internet, call-centers, utility lines prviders and concessionaries such as electricity and gas and phone Ombudsman Rule Financial Education Program 2004 - Decree 5,172 - lowered the IOF (Financial Transactions’ Tax) for life insurance from 7% to 2%, reaching 0% in 2006

for life insurance from 7% to 2%, reaching 0% in 2006")

16

Life Products Characteristics Main target: banks’ clients with monthly income under 3 min wages Basic Coverage: death by any cause Additional Coverage: funeral, “cesta básica” or “typical family food basket”, drugstore coverage. Lowest Premiums: R$ 6 (US$ 3) / Coverage: ≤ R$ 3,000 (US$1,500)

/ Coverage: ≤ R$ 3,000 (US$1,500).")

17

Automobile Products Characteristics Vehicles from 10 to 20 years-old More strict acceptance criteria Few additional coverages compared to traditional products Higher deductible for partial indemnity Lower Premiums compare to traditional plans

18

Other Lines Characteristics Fire and other non-life coverages (Multiple Peril) There are no specific rules on MI No data segregation in the reports sent by the insurer to SUSEP. The same product may be used for all kinds of consumers Distribution channels differentiate the target public

19

Farm Family Life Insurance Farm Family Life Insurance - jointly designed by Bank of Brazil and MDA (2004), for family farmers associated to the National Agriculture Strengthening Program for Family Farmers (PRONAF) on agricultural funding operations (mandatory enrollment) Coverage: Death and Extra Indemnity Coverage: Death and Extra Indemnity Distribution Channel: BB’s agencies Distribution Channel: BB’s agencies Capital Limit: R$ 600,00 to R$ 40.000,00 Capital Limit: R$ 600,00 to R$ 40.000,00 Premium: R$ 2,80/year for R$600,00: Death and R$ 600,00:Extra Indemnity Premium: R$ 2,80/year for R$600,00: Death and R$ 600,00:Extra Indemnity

, for family farmers associated to the National Agriculture Strengthening Program for Family Farmers (PRONAF) on agricultural funding operations (mandatory enrollment) Coverage: Death and Extra Indemnity Coverage: Death and Extra Indemnity Distribution Channel: BB’s agencies Distribution Channel: BB’s agencies Capital Limit: R$ 600,00 to R$ ,00 Capital Limit: R$ 600,00 to R$ ,00 Premium: R$ 2,80/year for R$600,00: Death and R$ 600,00:Extra Indemnity Premium: R$ 2,80/year for R$600,00: Death and R$ 600,00:Extra Indemnity")

20

Distribution Channels In Brazil it is not mandatory to have a broker intermediation when commercializing an insurance product. The brokerage fee is mandatory. Social and professional associations and labour unions, … Utility lines providers and concessionaires of public services, such as electricity and gas and phone Call-centers and internet The retail banks are the main distribution channels: more than 90% of Life MI products through bankassurance, including ATM’s

21

Main Results Life Insurance good performance inspired other lines (Automobile, Fire,) The biggest retail banks commercialize MI life products The biggest life insurers are domestic and part of big national conglomerates, including big retail bank

The biggest retail banks commercialize MI life products The biggest life insurers are domestic and part of big national conglomerates, including big retail bank")

22

Main Results SUSEP’s rules stimulated discussions on MI and sensitized the industry – the theme was unknown before 2004 Insurers preferred to design their own products, focus on low-income people Industry discovered low-income segment: “The poor are insurable”

23

Main Conclusions Products did not change so much. The commercialization focus changed Importance of the dialogue with industry for developing a new sector Tax relief has positive effects on MI lines seen that reduces insurance costs Flexibility for distribution channels – fundamental role in the consumer market growth

24

Main Conclusions Ombudsman Rule: important mechanisms to safeguard the consumers rights, especially of the less fortunate ones Financial Education should be encourage, leading to a conscious consumer Brazilian market has few informal schemes when compared to other countries, facilitating supervision

25

SUSEP’s Challenges Segregate MI statistical data creating no additional onus for insurers Maintain an adequate regulatory environment, balancing: promotional aspects X prudential requirements Raise the perception level of other stakeholders

26

SUSEP’s Challenges Engage in dialogue with other Brazilian supervisors and policymakersfor convergence, Engage in dialogue with other Brazilian supervisors and policymakers for convergence, i.e.: i.e.: Cooperation exchange Tax relief for other lines (Receita Federal) Encourage new lines, focus on rural lines (MDA) Promote financial education for low-income people (Ministry of Education)

Encourage new lines, focus on rural lines (MDA) Promote financial education for low-income people (Ministry of Education)")

27

Thank you Obrigada Regina L. G. Simões codin@susep.gov.br

Similar presentations

AND GENDER.>")

By: Joana J.David Maseru, 11-12 October 2005.>")

Strengthening rural entrepreneurship by connecting the local production with other economic.>")

FINANCIAL SYSTEM “SFN” – an overview Federal Constitution sets the rules for operations and regulation of the Brazilian.>")