Download presentation

Presentation is loading. Please wait.

2

Custom duty is imposed on imports into INDIA and export out of INDIA. The Custom Act was first passed in1962 replacing Sea Customs Act,1878 while the Custom Tariff Act was passed in 1975. In 1985, the Custom Tariff Act was amended by Custom Tariff(amendment) Act, 1985.

Act,")

3

NATURE OF CUSTOM DUTY The rate at which the duty is to be imposed is specified under “ THE CUSTOM TARIFF ACT 1975”. Article 266 of the constitution provides that the proceeds from the Customs duty are to be kept by union only & are not to be shared between union and any states.

4

OBJECTIVES OF THE ACT

13

Standard Rate of Duty.Effective Rate Of Duty.Preferential Rate of Duty

26

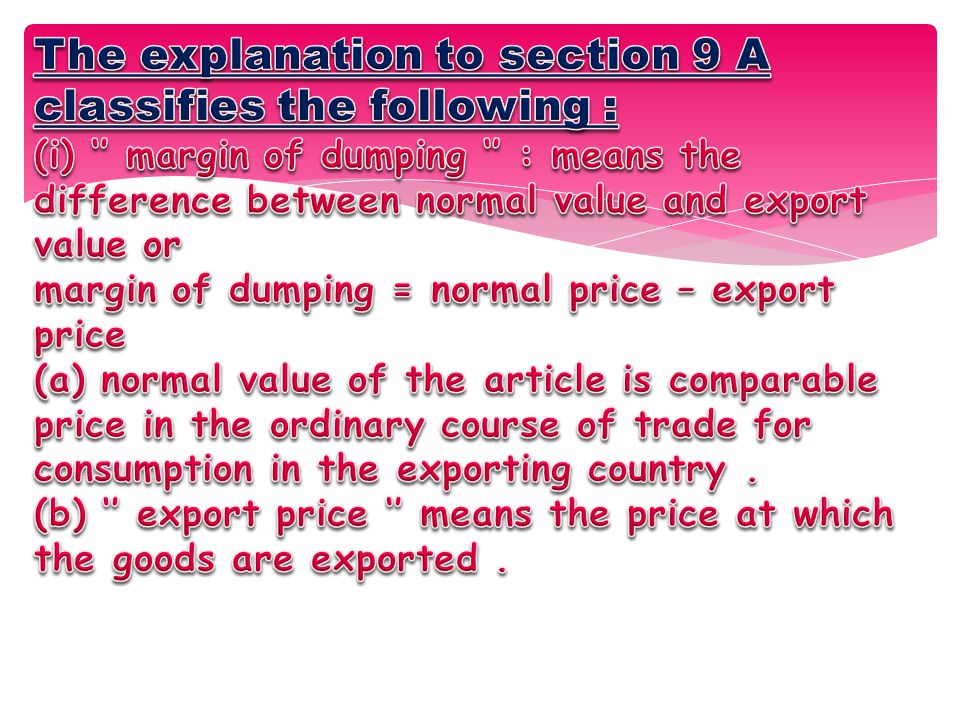

1. Legal provision Power to levy above duty u/s 6(1) of CTA, 1975 Power to levy above duty is u/s 8B of CTA 1975 Power to levy is u/s 9A of CTA 2. ConditionsConditions are left to be determined by Tariff Commission. Normally imported cheaper goods which hinder growth of domestic industry. If any article is imported into india in increased quantities and causes will threaten to cause serious injury to domestic industry. If any article is imported into india and its export price is less than its normal value. 3. Power to levy Power to levy this duty rests with Central Govt. but a recommendation from Tariff Commission is necessary. Power to levy duty rests with Central Govt. No recommendation from Tariff Commission is must Power to levy duty rests with Central Govt.. No recommendation from Tariff Commission is must Basis of difference Protective duty Safeguard duty Anti Dumping duty

of CTA, 1975 Power to levy above duty is u/s 8B of CTA 1975 Power to levy is u/s 9A of CTA 2. ConditionsConditions are left to be determined by Tariff Commission. Normally imported cheaper goods which hinder growth of domestic industry. If any article is imported into india in increased quantities and causes will threaten to cause serious injury to domestic industry. If any article is imported into india and its export price is less than its normal value. 3. Power to levy Power to levy this duty rests with Central Govt. but a recommendation from Tariff Commission is necessary. Power to levy duty rests with Central Govt. No recommendation from Tariff Commission is must Power to levy duty rests with Central Govt.. No recommendation from Tariff Commission is must Basis of difference Protective duty Safeguard duty Anti Dumping duty.")

27

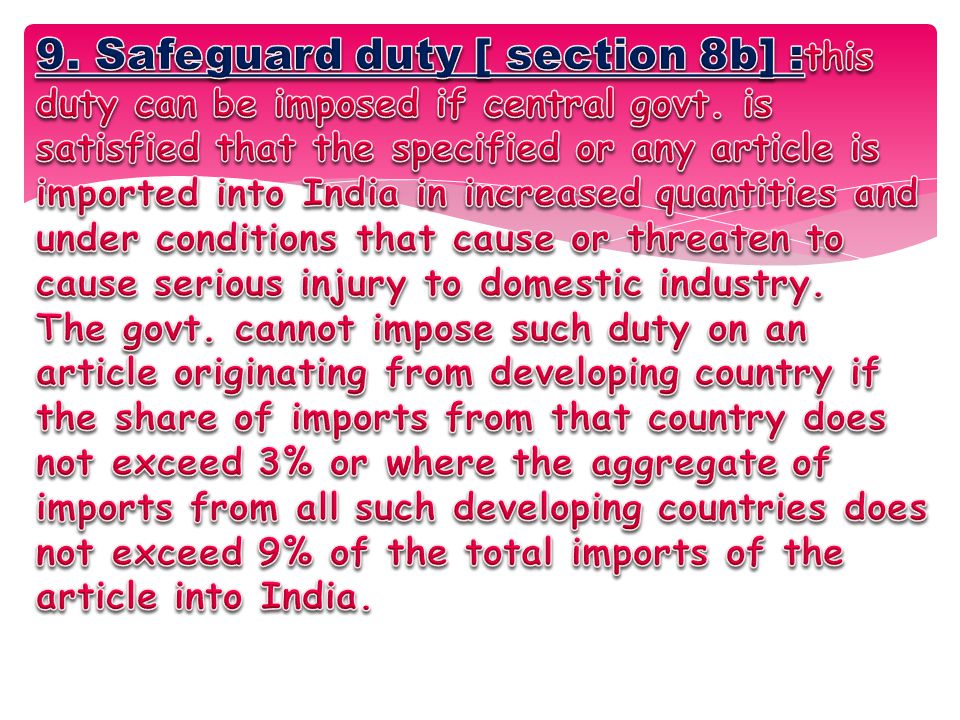

4.Period The power to decide and specify upto which date such duty shall be in force is with Central Govt. Unless revoked earlier by Central Govt., such duty shall cease to have effect on the expiry of 4 years from the date of its imposition. Unless revoked earlier by Central Govt., such duty shall cease to have effect on the expiry of 5 years from the date of its imposition. 5. Conditions of Developing Country No such conditions. Only recommendations of Tariff Commission is necessary. The Govt. can’t impose such duty if imports from a developing country of that article do not exceed 3% or where the aggregate of imports from such developing countries does not exceed 9% of total imports of that article in india No such condition but the condition of export price being less than normal value exists

28

CVD ON SUBSIDISED ARTICLES ANTI – DUMPINNG DUTY Relevant Section Sec 9 of CTA Sec 9 of CTA Sec 9A of CTA Sec 9A of CTA Basic objectives Check subsidization – which results from Govt. practice in which govt. confers an advantage to the domestic producers by way of financial contribution. Check dumping which results due to price discriminatory practices adopted by the exporter on his own. Maximum amount Amount of subsidy Margin of dumping [normal value –export value ] Provisional impositions Maximum for a period of 4 months No period specified

Similar presentations

6 th Lecture, 14-11-2013.>")

>")

,2014 BY CA SRINIVASAN ANAND G.>")

No prohibition: generic condemnation. Anti-Dumping Agreement. No duty of enacting anti-dumping legislation and adopting anti-dumping measures.>")