Download presentation

Presentation is loading. Please wait.

1

Student Payroll: Forms and Procedures Presented by Tax Services July 2006

2

Overview Tax Residency: What’s it all about? Nonresident Alien Tax Residency Information Form & Documentation Taxing Nonresident Alien Students Student FICA Rules I-9 Overview W-4 Withholding Record Retention

3

Student Payroll: Nonresident Alien Taxation

4

Tax Residency Under U.S. tax laws, all non-U.S. citizens are considered to be either: Permanent resident aliens Resident aliens for tax purposes, or Nonresident aliens.

5

Taxation & Residency Permanent resident aliens and resident aliens for tax purposes are taxed the same as U.S. citizens Resident aliens generally are taxed on their worldwide income, the same as US Citizens Nonresident aliens are taxed under special laws Nonresident aliens are taxed only on their income from sources within the US & on certain income connected with the conduct of trade or business in the US.

6

Tax Residency - Why We Care Knowing an individuals tax residency status prior to payment is essential to accurately report the individual’s tax liability and to be in compliance with IRS tax laws.

7

Tax Residency - Why We Care If MnSCU incorrectly reports a nonresident alien’s tax withholding liability, MnSCU may be held responsible for the tax not withheld, in addition to any penalties for failure to withhold, plus the interest from the time the tax was not withheld. $ MnSCU Pays $

8

Tax Residency Tests There are two tests used to determine whether a non U.S. citizen should be treated as a U.S. resident for tax purposes: The “Green Card” test, and the Substantial Presence Test

9

Days Not Counted Exceptions to counting days towards substantial presence: AAny days the individual regularly commutes to work in the U.S. from a residence in Canada or Mexico AAny days the individual is in the U.S. for less than 24 hours when in transit between two places outside of the U.S. AAny days the individual was unable to leave the U.S. due to a medical condition that developed while he was in the U.S., and AAny days the individual was present in the U.S. as an “exempt individual”.

10

Exempt Individuals “Exempt individuals” are present in the U.S. for the primary purpose of being: a teacher or trainee generally present under a “J” or “Q” visa; includes all “J” non- student categories a student generally present under a “F”, “J”, “M” or “Q” visa a “foreign government- related” individual generally a foreign diplomat or consular officer present under an “A” or “G” visa a professional athlete generally present under a “P” visa

11

Tax Residency Information Form Student employee’s who indicate on their I-9 that they are “other alien authorized to work until xx/xx/xxxx” must fill out the Student Payroll Tax Residency Information Form. Section E applies the Substantial Presence Test for F-1/J-1 student visa holders

12

Tax Residency Information Form

14

2001F-1 Ideal Reality: Estimate or Range of Dates Aug 01 – May 02High school exchange student program 2002F-1 Above Also Known As TRIF

15

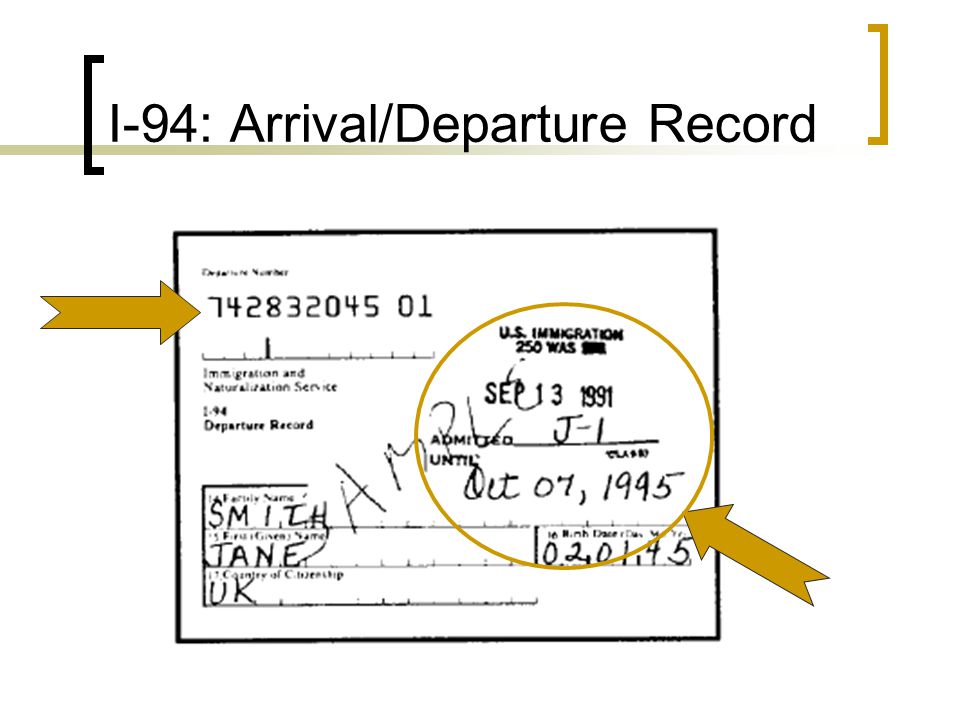

TRIF Documentation F-1 Students I-20 & Attachments I-94 Passport J-1 Students DS-2019 & Employment Letters I-94 Passport

16

I-20 Certificate of Eligibility for Nonimmigrant (F-1) Student

Student")

17

I-94: Arrival/Departure Record

19

DS-2019 Certificate of Eligibility for Exchange Visitor(J-1) Status

Status")

20

Passport Information Identification Page Current visa information Prior visits to US

21

Tax Residency Form Summary All student employees who indicate on their I-9 that they are “other aliens authorized to work until xx/xx/xxxx”, must fill out the Tax Residency Form Students must complete Sections A and D. If they have been in the U.S. prior to their current visit, they must also complete Section C. Student Payroll copies the student’s immigration documents & completes Sections E, F and G. Student Payroll enters the Tax Residency Year from Section E into ISRS Student Employee Setup (PR0021UG) Screen Keep the original form with the employee’s records Send a copy of the completed form and related immigration documentation to Tax Services

Screen Keep the original form with the employee’s records Send a copy of the completed form and related immigration documentation to Tax Services.")

22

Taxing Nonresident Aliens Statutory Withholding FICA Exemption Tax Treaty Benefits

23

Nonresident Aliens & W-4: May not claim exemption from income tax withholding, Request withholding as if they are single, regardless of their actual marital status, Claim only one allowance, and On line 6, write “Nonresident Alien” or “NRA” $15.30 in extra withholding is no longer required Statutory Withholding Rules

24

Students from India Article 21(2) of the United States-India Income Tax Treaty An additional withholding allowance may be claimed for a spouse if the spouse has no U.S. source gross income and may not be claimed as a dependent by another taxpayer. An additional withholding allowance for each dependent (usually a child) who has become a resident alien. Exceptions to Statutory Withholding Rules Canada and Mexico, American Samoa and Northern Mariana Islands Entitled to claim additional withholding allowances for a nonworking spouse and for dependents, the same as a U.S. citizen. South Korea May claim additional withholding allowances for a nonworking spouse and dependents present with them in the U.S.

who has become a resident alien. Exceptions to Statutory Withholding Rules Canada and Mexico, American Samoa and Northern Mariana Islands Entitled to claim additional withholding allowances for a nonworking spouse and for dependents, the same as a U.S. citizen. South Korea May claim additional withholding allowances for a nonworking spouse and dependents present with them in the U.S..")

25

FICA Exception for F, J, M & Q Nonresident Aliens IRC Section 3121(b)(19) An individual may be exempt from FICA tax withholding if he or she meets all of the following criteria: Is a nonresident alien for taxation purposes (i.e.: has not met the substantial presence test); Is present in the U.S. under a F, J, M or Q visa; Is performing services in accordance with the primary purpose of the visa’s issuance (i.e., the primary holder of the visa, the “-1”). This exemption does not apply to F, J, M or Q visa holders who become resident aliens for tax purposes (i.e., individuals who have met the substantial presence test).

. This exemption does not apply to F, J, M or Q visa holders who become resident aliens for tax purposes (i.e., individuals who have met the substantial presence test)..")

26

Tax Treaties & Income Withholding Agreement between two countries to reduce or eliminate double taxation. US has income tax treaties with over 48 different countries Each treaty is unique and may not contain the same provisions or exemptions as another tax treaty. From time to time, treaties with additional countries are signed and existing treaties revised IRS website has complete text of current tax treaties

27

Tax Treaties & Income Withholding Typically, the employee must be a nonresident alien for tax purposes to claim treaty benefits F-1 Student Tax Treaty Article/Clause Compensation during training Dependent Personal Services (Canadian) Annual maximum dollar amount and/or a time limit of presence in the U.S.

Annual maximum dollar amount and/or a time limit of presence in the U.S.")

28

Form 8233: For Claiming Treaty Benefits

29

Form 8233: For Claiming Treaty Benefits Completing Form 8233

30

Form 8233: Page 2 Jane Lee12/1/2005 Campus Contact Student Payroll12/5/2005 Must be mailed within 5 days from the withholding agent signature date

31

8233 Statement Attachment Peoples Republic of China 1. I was a resident of the Peoples Republic of China on the date of my arrival in the United States. I am not a United States citizen. I have not been lawfully accorded the privilege of residing permanently in the United States as an immigrant. 2. I am present in the United States solely for the purpose of my education or training. 3. I will receive compensation for personal services performed in the United States. This compensation qualifies for exemption from withholding of federal income tax under the tax treaty between the United States and the Peoples Republic of China in an amount not in excess of $5000 for any taxable year. 4. I arrived in the United States on 8/25/2005. I am claiming this exemption only for such period of time as is reasonably necessary to complete the education or training. Tax year treaty being claimed for 2006 ______________; Under penalties of perjury, I declare that I have prepared this form and to the best of my knowledge and belief, it is true, correct, and complete. Signature of nonresident alien individual______ Jane Lee _ Date 12/1/2005 ________________________________________

32

Completing Form 8233 Review 8233 & Statement Attachment Sign & Date 8233 Must be mailed to IRS within 5 days of signing Copy 8233 & Attachment: IRS Tax Services Employee Campus

33

Student Payroll Employment Forms

34

Employment Forms Form I-9, Employment Eligibility Verification Form W-4, Employee’s Withholding Allowance Certificate

35

Tax Form Management General form information Form maintenance & documentation Form storage suggestions Record retention requirements

36

Form I-9 Employment Eligibility Verification Form

37

Form I-9, Employment Eligibility Verification Department of Homeland Security USCIS: United States Citizenship & Immigration Services Law: The Immigration & Control Act Code of Federal Regulations Sec 274 U.S. Employers & Employees Last updated: 1991

38

Employee’s responsibility Complete Section I; Prior to the close of business on the first day of employment services Employer’s responsibility Review employment authorization documentation prior to the close of business on 3 rd day of employment services & complete I-9 Form I-9, Employment Eligibility Verification

39

I-9: Section 1 SMITHJOHN A 12 ANYWHERE AVENUE 1A SOMEWHERE MN 55101 123-45-6789 01/01/1984

40

Section 2: Form I-9, Employment Eligibility Verification Review Documentation 1.Authorization to work in U.S. 2.Establish identity Must match Record Document Information Employer must sign & date

41

I-9: Section 2, Verification F-1/J-1 Students = 3 Documents F-1 Documentation SEVIS Form I-20, I-94, Arrival/Departure Passport Personal Info Include visa stamp

42

I-9 Documentation List of acceptable documents List A: Employment Eligibility & ID Lists B & C: Combination Timely verification Must be verified within 3 days of start date Reasonableness If appears genuine, accept document

43

Documents that Establish Both Identity & Employment Eligibility And Form I-766, Employment Authorization Document

44

LIST B: Establishing Identity

45

LIST C: Establishing Employability The combination of documents from List B and List C verifies the I-9

46

LIST C: Common Error A Social Security Card that reads: Is NOT an acceptable List C document. You must ask to see another document to verify employability. “Valid for work only with DHS Authorization”

47

I-9: Section 3, Re-Verification Re-Verification When work authorization documents reach expiration date

48

I-9 Record Retention I-9’s must be on hand for: All current employees Three years after employee’s hire date or 1 year after employee’s termination date whichever is later

49

I-9 Record Recommendations In case of audit, I-9’s must be retrievable in 3 days Recommend keeping I-9’s separate from other payroll documentation

50

W-4 Withholding Certificate

51

W-4 General Rules What to do if no W-4? S-0 Validity: Any unauthorized change or addition to Form W-4 makes it invalid. Including: Taking out any language by which the employee certifies that the form is correct A Form W-4 is also invalid if, by the date an employee gives it to you, he or she indicates in any way that it is false. When you get an invalid Form W-4, do not use it to figure federal withholding. Tell the employee that it is invalid and ask for another one.

52

W-4: Claiming Exemption IRS Code section 3402(n): An employee may claim exemption from income tax withholding if he or she: 1)Had no income tax liability last year and 2)Expects to have no tax liability this year. Exemption is good for one year only W-4 must be submitted by February 15th If the employee does not provide a new Form W-4, the employer must withhold tax as if the employee were single with zero withholding allowances.

53

W-4: New IRS Rule in 2005 Withholding agents are no longer required to send copies of W-4’s to IRS, unless specifically requested MN Dept of Revenue still requires copies W-4’s with over 10 allowances Exempt W-4’s where employee regularly earns over $400 a biweekly pay period

54

Withholding Allowances: Employee Advice IRS Withholding Calculator http://www.irs.gov/individuals/article/0,,id=96196,00.html Most recent pay stubs, most recent tax return Calculator will determine correct withholding allowances to claim on Form W-4 Link on Tax Services website – Student Tax Assistance section

55

Withholding Allowances: Employee Advice IRS Publication 919: How Do I Adjust My Tax Withholding? http://www.irs.gov/pub/irs-pdf/p919.pdf Detailed instructions and worksheets for computing tax withholding

56

W-4 Record Retention Form W-4 remains in effect until the employee gives you a new one. If an employee gives you a Form W-4 that replaces an existing Form W-4, begin withholding no later than the start of the first payroll period ending on or after the 30th day from the date when you received the replacement Form W-4.

57

W-4 Record Retention A Form W-4 claiming exemption from withholding is valid for only one calendar year Request new W-4 each year from: Employees claiming exemption NRA’s with 8233’s W-4’s must be kept on file for 7 years after the last applicable tax year

58

W-4 Record Retention: Example Ann is hired in 2001 & fills out a 2001 W-4 In 2004, Ann fills out a new W-4 The 2001 W-4 was used to figure Ann’s withholding for 2001, 2002, 2003 and part of 2004. The 2001 W-4 must be kept until 2011

59

Summary: I-9 & W4 I-9 Keep I-9’s for 3 years after hire date or 1 year after termination, which ever is later. Reverify I-9 when employment authorization expires W-4 Current and terminated employees: Keep all W-4’s for 7 years past applicable year If missing or invalid W-4: Withhold S-0 Current Employees: Keep most recent I-9 & W-4 form on file

60

Retention: Payroll Forms 7 Years past applicable tax year Timesheets W-4 Forms TRIF 8233 Forms Contracts

61

Tax and Student Employees Student FICA Exception Payday Tax Reports Graduate Assistants Taxable Tuition Benefit

62

Student FICA Exception IRC Section 3121(b)(10) To be eligible for the student FICA exception the student must: Work for the institution at which they are enrolled, and Be enrolled for at least half-time and regularly attending classes. This exemption is available during breaks between sessions if the breaks do not exceed 5 weeks. The student is not eligible for this exception if they regularly work more than 30 hours per week.

63

Student FICA Exception Rule Changed 4/1/2005 Full time employees are not exempt Employees who regularly work 40 hours a week = full time, career employees >30 Hour a week = full time Tracking Supervisor Hire Form ISRS Report PR0212CP Hours Worked

64

Student FICA Exception Issue Pay Period Controller (PR0002UG), Academic Terms and the Student FICA Exception The Term associated with a pay period will be used by the ISRS Student Payroll Module to determine the student worker’s enrollment for purposes of the Student FICA Exception.

, Academic Terms and the Student FICA Exception The Term associated with a pay period will be used by the ISRS Student Payroll Module to determine the student worker’s enrollment for purposes of the Student FICA Exception.")

65

Guidelines for Associating Pay Periods to Academic Terms If the pay period straddles terms, the pay period may be tied to either term's enrollment. Summer term ends 8/20, Fall term starts 8/21, and pay period 04 starts 8/9 and ends 8/22. Since pay period 04 straddles Summer and Fall terms, the institution can tie this pay period to either Summer or Fall term. If the pay period falls completely in a between- term break of 5 weeks or less, use the enrollment data for the term prior to the break. Summer term ends 7/28, Fall term starts 8/28 and pay period 04 starts 8/9 and ends 8/22. Because pay period 04 falls completely in the between-term break, it must be tied to Summer term enrollment.

66

Guidelines for Associating Pay Periods to Academic Terms If the pay period straddles a break and a term, the current term's enrollment data must be used. Summer term ends 7/28, Fall term starts 8/21, pay period 04 starts 8/9 and ends 8/22. Pay period 04 must be tied to Fall term enrollment since it is the only term that includes any portion of the pay period. If the pay period falls in an academic break of more than 5 weeks, the Student FICA Exception is not allowed. Please contact Tax Services with questions

67

Payday Tax Reports & Checks Student Payroll Calendar (see website) By the Wednesday prior to PayDay Tax Reports PR0009GR & PR0010GR should be sent to printer named: BW350A Tax Checks should be mailed to OOC

By the Wednesday prior to PayDay Tax Reports PR0009GR & PR0010GR should be sent to printer named: BW350A Tax Checks should be mailed to OOC")

68

Graduate Assistant Tuition Reductions Determining Taxable Tuition Reductions

69

Internal Revenue Code Section 117 (d) paragraphs 1 & 2 of the Internal Revenue code provides that “gross income shall not include any qualified tuition reduction provided to an employee for education below the graduate level”. Section 117 (d) paragraph 5 extends the provisions of paragraphs 1 & 2 to “graduate assistants engaged in teaching and research”. Section 117 (c) limits the exclusion from income to tuition reductions that do not have a service requirement as a condition of receiving the tuition reduction.

paragraph 5 extends the provisions of paragraphs 1 & 2 to graduate assistants engaged in teaching and research . Section 117 (c) limits the exclusion from income to tuition reductions that do not have a service requirement as a condition of receiving the tuition reduction..")

70

Graduate Assistant Tuition Reductions A tuition reduction is tax free to a graduate student under the following circumstances: The student is engaged in teaching or research, and The tuition reduction does not represent compensation for service.

71

Documenting Teaching/Research Positions It is recommended that all assistantships which qualify as teaching or research have the following Supporting Documentation: Teaching or Research as a descriptors in the job title- i.e. Biology Graduate Research Assistantship Job description that lists duties which are appropriate for job title.

72

Compensation for Services The tuition reduction is considered compensation for service if the graduate assistant must perform some service for which they are not otherwise compensated. To the extent the tuition reduction represents compensation for services, the fair market value of the portion of the tuition reduction that represents compensation is taxable.

73

Determination of Taxable Benefit Fair Market Value of Tuition How does the graduate assistants’ hourly rate compare with wages for the same work in the local private sector? Comparison choices given by IRS Wages paid by college to students performing same work and not receiving tuition benefits Wages paid by college to employees who are not students performing same work Wages paid by other educational organizations to students or employees performing same work Supporting Documentation Fair Wage Comparison based on one or more of the above

74

Example 1 The graduate student is employed by the university as an office assistant and receives an hourly salary plus a tuition reduction of $1,000 per year. The tuition reduction is taxable because the graduate student is not engaged in teaching or research. Whether the graduate student is being paid fair market value is irrelevant since the graduate student is not engaged in teaching or research.

75

Example 2 Deb, a graduate student at a MnSCU State University, is engaged as a teaching assistant, for which she receives a salary of $6,000 per year plus a tuition reduction of $1,000 a year. Adjunct faculty who teach the same number of credits and have comparable qualifications receive a salary of $6,000 per year. The graduate student’s salary is reasonable compensation when compared to the adjunct salary so the tuition reduction is tax-free.

76

Student Payroll Setup of Taxable Tuition Reductions Use FA Award Code 10189 to record taxable tuition reductions. Student Payroll must use the Taxable Benefit Browse screen (PR0026UI) to list the student employees who have had an Award ID of 10189 (Grad Assist Tuit Waiver-Taxable) applied to their account.

to list the student employees who have had an Award ID of (Grad Assist Tuit Waiver-Taxable) applied to their account..")

77

Student Payroll Setup of Taxable Tuition Reductions Use the Taxable Benefit Entry screen (PR0026UG) to set up the distribution time period and amount. Taxable Benefits must be set up to be spread across the pay periods for that period of time which the graduate student is reasonable expected to be employed by a MnSCU institution. Note: If the reduction is distributed into summer session when graduate student is not enrolled in classes, the reduction will be subject to FICA as would any regular wages.

78

Reporting Taxable Tuition Reductions Taxable benefits must be reported on Form W-2 and are subject to the usual employment taxes. In general, graduate assistants will be exempt from FICA under the student FICA exemption. Student Payroll must use the Taxable Benefit Screen, PR0026UG, to distribute the taxable benefits to the graduate students’ wages. Taxable benefits must be distributed during the same semester as awarded.

79

Tax Services Website Tax Services Website: http://www.financialreporti ng.mnscu.edu/Tax_Se rvices/index.html Nonresident Alien Manuals Student Payroll Student FICA Tax Guidelines Sales Tax Student Tax Assistance Bonds: Tax-Exempt Financing & Reporting Employee Expense Reimbursement Policy Unrelated Business Income Tax (UBIT) Nonresident Entertainer Tax (MN) Phone Bills & Taxes Auto, Boat and Airplane Charitable Donations

Nonresident Entertainer Tax (MN) Phone Bills & Taxes Auto, Boat and Airplane Charitable Donations")

80

Contact Information Ann Page, 651-632-5007 Ann.Page@so.mnscu.edu Ann.Page@so.mnscu.edu Steve Gednalske, 651-632-5016, Steve.Gednalske@so.mnscu.edu Steve.Gednalske@so.mnscu.edu Tax Services Website: http://www.financialreporting.mnscu. edu/Tax_Services/index.html

Similar presentations

>")

University of Washington Student Fiscal Services.>")

>")

University of Washington Student Fiscal Services.>")

Elizabeth Giron (Foreign National Tax Specialist)>")