Download presentation

Presentation is loading. Please wait.

1

XBRL Instance Documents

2

Financial Information Reported By a Specific Entity For a Specific Period of Time In a Specific Currency ▪ How precise is the currency being reported What taxonomy schema is the element defined in

3

Rules and Syntax for XBRL Instance Documents XBRL taxonomies ▪ Defines the elements and relationships for financial reporting concepts ▪ Taxonomy Schema for each specific reporting purpose ▪ Commercial & Industrial type company ▪ Banking type company ▪ … ▪ Linkbases ▪ Relationships between the elements 3

4

Instance Document Contains the data items which represent the financial data in financial reports ▪ Financial Statements ▪ Disclosures Taxonomy Defines elements and relationships ▪ Schema for a particular reporting group ▪ Banking & Savings ▪ Brokers & Dealers ▪ Commercial & Industrial ▪ Insurance ▪ Real Estate ▪ Linkbases ▪ Presentation, Calculation, Reference, Label & Dimension

5

Source: Charlie Hoffman, http://xbrl.squarespace.com/journal/2009/6/21/high-level-model-of-xbrl.html

6

Attributes include: What entity is the data for (contextRef) What period of time is the data for (contextRef) What currency is being reported (UnitRef) What precision is the currency in (decimals) Which taxonomy is the fact defined in (namespace prefix) 6

What period of time is the data for (contextRef) What currency is being reported (UnitRef) What precision is the currency in (decimals) Which taxonomy is the fact defined in (namespace prefix) 6")

7

XBRL Element NameDefinitionCardinality xbrlAn XBRL instance documentRequired root element schemaRef Identifies an XBRL taxonomy schema & links it to this XBRL instance document1.. N context Establishes the "reporting context" of an XBRL instance document (a complex element)1.. N Must contain: id attribute (a unique identifier); entity (to identify the reporting entity); period (to identify the reporting period) unit Identifies the numerical unit of measure (e.g. USD) (a complex element)0.. N Must contain: id attribute (a unique identifier); measure (to identify the unit of measure) An XBRL itemAt least one reported XBRL item1.. N Must contain: contextRef attribute (to identify the context that applies to this item); For numeric items: unitRef attribute (to identify the unit of measure that applies to this item); decimals attribute (to designate the reporting precision that applies to this item) 7

1.. N Must contain: id attribute (a unique identifier); entity (to identify the reporting entity); period (to identify the reporting period) unit Identifies the numerical unit of measure (e.g. USD) (a complex element)0.. N Must contain: id attribute (a unique identifier); measure (to identify the unit of measure) An XBRL itemAt least one reported XBRL item1.. N Must contain: contextRef attribute (to identify the context that applies to this item); For numeric items: unitRef attribute (to identify the unit of measure that applies to this item); decimals attribute (to designate the reporting precision that applies to this item) 7.")

8

1. Root Element NameSpace Declarations 2. References Schema Declarations 3. Context Who’s financial data What Period 4. Unit Currency Shares 5. Items Elements of the Financial Statement

9

Element Name = xbrl All namespace declarations XBRL usually will contain many ▪ xmlns:us-gaap=“http://fasb.org/us-gaap/2013-01-31 ”http://fasb.org/us-gaap/2013-01-31 ▪ xmlns:link=“http://www.w3.org/2003/linkbase” ▪ xmlns:xbrli=“http://www.xbrl.org/2003/instance” ▪ xmlns:xlink=“http://www.w3.org/1999/xlink” ▪ xmlns:iso4217=“http://www.xbrl.org/2003/iso4217 “http://www.xbrl.org/2003/iso4217

10

xbrli Content and structure of XBRL instance link Content and structure of linkbases iso4217 Standard currency codes xlink Xlink schema US GAAP taxonomy 10

11

Was maintained by XBRL-US organization Now maintained by FASBFASB Namespaces and Schema URI’s Namespaces and Schema URI 11

12

Used to link a taxonomy schema to the instance document Must be at least one Taxonomy Reference used to validate the Instance Document First Child Element schemaRef ▪ Attributes: ▪ xlink:type=“simple” ▪ xlink:href=“URI”

13

Element Name = Context id attribute ▪ Used later to associate meta-data with financial reporting item ▪ Can be anything, but must start with a letter ▪ Like a namespace prefix Complex element with 4 parent elements Entity ▪ Uniquely identifies the entity Period ▪ Instant ▪ Duration Scenario ▪ What types of facts ▪ Actual, Restated, Budgeted, etc. Segment ▪ Information about segment being reported

14

Entity (Parent Element) Identifier (Child Element) (attribute) scheme ▪ Depends on reporting purpose ▪ SEC identifier, NYSE symbol, etc. SEC CIK id

15

2007-11-06 or... 2007-01-01 2007-12-31 or... element can be used Must use yyyy-mm-dd format

16

Unit (Parent Element) id attribute Used as a reference Same as Context element Measure element Value describing unit of measure USD EUR JPY xbrli:shares

id attribute Used as a reference Same as Context element Measure element Value describing unit of measure USD EUR JPY xbrli:shares")

17

Currency <xbrli:unit id=“USD” iso4217:USD Shares xbrli:shares

18

iso4217:USD xbrli:shares 18

19

Single Fact being reported Element name comes from US GAAP taxonomy Determine element names from viewerfrom viewer Attributes contextRef (points to context id for fact being reported) unitRef (points to unit id for fact being reported) decimals ▪ To how many decimal places is a fact accurate or precision ▪ How many digits are significant label ▪ How should element be named in report* *When doing homework for chapter 4 use the label attribute

unitRef (points to unit id for fact being reported) decimals ▪ To how many decimal places is a fact accurate or precision ▪ How many digits are significant label ▪ How should element be named in report* *When doing homework for chapter 4 use the label attribute")

20

in thousanddecimals="-3" in milliondecimals="-6" accurate valuedecimals="INF" or decimals="2" percentdecimals="2" Source: http://www.xbrlwiki.info/index.php?title=Best_Practices_on_Data_Definitions

21

Source: Charlie Hoffman, http://xbrl.squarespace.com/journal/2009/6/ 22/xbrl-instance-graphic.html

22

Use to find element names to use for tagging data and disclosures There are 16,000+ elements! Financial Statement and Disclosures In choosing an element: Choose the element with the narrowest definition of the fact you are reporting If more than one element is available use the element that is part of the financial statement vs. a disclosure element If using a disclosure element, use software to move it as a financial statement line element. Types of elements: Abstract – do not use as a tag in instance doc. Financial Reporting Concepts For each element (not abstract items) Labels ▪ Standard ▪ Documentation ▪ Total References ▪ To authoritative literature Properties ▪ Element name ▪ Namespace ▪ Type (monetary, shares, etc.) ▪ Normal Balance (debit or credit) ▪ Time (instant or period)

Labels ▪ Standard ▪ Documentation ▪ Total References ▪ To authoritative literature Properties ▪ Element name ▪ Namespace ▪ Type (monetary, shares, etc.) ▪ Normal Balance (debit or credit) ▪ Time (instant or period).")

23

23

24

24

25

Schedule of Investments Used to supplement investment holdings for unaffiliated investments Industry Entry Points Commercial and Industrial Banking and Savings Institutions Brokers and Dealers Insurance Real Estate 25

26

Non-GAAP Record of Credit Rating Taxonomy U.S. Mutual Fund Risk/Return Taxonomy Management Reports Management Discussion and Analysis Document and Entity Informaiton 26

27

....

28

Source:

29

29

30

Reference relationships between elements and external regulations or standards Label elements are connected to human readable labels Presentation How elements appear Calculation How elements are used in calculations Dimensions How to create tables for footnote disclosures

31

<reference xlink:type="resource" xlink:role="http://www.xbrl.org/2003/role/presentationRef" xlink:label="CashFlowsFromUsedInOperationsTotal_ref"> IAS 7 14 <reference xlink:type="resource" xlink:role="http://www.xbrl.org/2003/role/measurementRef" xlink:label="CashF lowsFromUsedInOperationsTotal_ref"> IAS 7 18 a

32

<label xlink:type="resource" xlink:role="http://www.xbrl.org/2003/role/label" xlink:label="ifrs_AssetsTotal_lbl" xml:lang="en">Assets, Total <label xlink:type="resource" xlink:role="http://www.xbrl.org/2003/role/label" xlink:label="ifrs_AssetsTotal_lbl" xml:lang="de">Vermögenswerte, Gesamt <label xlink:type="resource" xlink:role="http://www.xbrl.org/2003/role/label" xlink:label="ifrs_AssetsTotal_lbl" xml:lang="pl">Aktywa, Razem

33

uses parent-child relations to organize elements Assets Current ▪ Cash ▪ Receivables ▪ Accounts ▪ Interest ▪ Inventory Long-Term ▪ Property, Plant and Equipment ▪ Intangible Assets ▪ Notes Receivable The “order” attribute of the presentationArc specifies the order in which child concepts should appear with respect to their sibling concepts.

34

http://snipr.com/lc15r [www_sec_gov]

![[www_sec_gov]](http://images.slideplayer.com/14/4260373/slides/slide_34.jpg "[www_sec_gov]")

35

Gross Profit = Revenue – CGS Linkbase Gross Profit Revenue (1) CGS (-1) Lower level elements sum up to or are subtracted from upper level elements

CGS (-1) Lower level elements sum up to or are subtracted from upper level elements")

36

weight is a required attribute on calculationArc elements; it must have a non-zero decimal value; for summation-item arcs, the weight attribute indicates the multiplier to be applied to a numeric item value (content) when accumulating numeric values from item elements to summation elements; a value of "1.0" means that 1.0 times the numeric value of the item is applied to the parent item; a weight of "-1.0" means that 1.0 times the numeric value is subtracted from the summation item; there are also rules that are applied to the calculation of elements possessing opposite balance attribute values ('credit' and 'debit');attributecalculationArcelements summation-itemarcsnumeric itemcontentbalance

when accumulating numeric values from item elements to summation elements; a value of 1.0 means that 1.0 times the numeric value of the item is applied to the parent item; a weight of -1.0 means that 1.0 times the numeric value is subtracted from the summation item; there are also rules that are applied to the calculation of elements possessing opposite balance attribute values ( credit and debit );attributecalculationArcelements summation-itemarcsnumeric itemcontentbalance")

37

<link:calculationArc order="6.0" weight="1.0" xlink:arcrole="http://www.xbrl.org/2003/arcrole/summation-item" xlink:from="lbl_AssetsCurrent" xlink:to="lbl_

38

Used to create tables Simple Pivot type Utilizes the Context element to define the table using: Segment element which defines: Axes Dimension Characteristics of a fact (e.g. deferred revenue from x) Domains Contains a set of members Members Column Headers (horizontal axis) Line Items Row Header (vertical axis)

Domains Contains a set of members Members Column Headers (horizontal axis) Line Items Row Header (vertical axis).")

39

Four Levels: Implemented based on company size Each Footnote disclosure is required to have a contextRef for the entire reporting period ( ) Level 1 ▪ First year filer ▪ Block Tagging ▪ Each complete footnote along with formatting is tagged within XBRL Instance Level 2 ▪ Second year filers ▪ Tag each accounting policy within the Significant Accounting Policies footnote, along with formatting Level 3 ▪ Second year filers ▪ Tag each table, along with its formatting Level 4 ▪ Second year filers ▪ Tag each monetary value, % and number in the footnotes. 39

40

The rest of the footnote The rest of the footnote This is what the footnote looks like This is what the footnote looks like 40

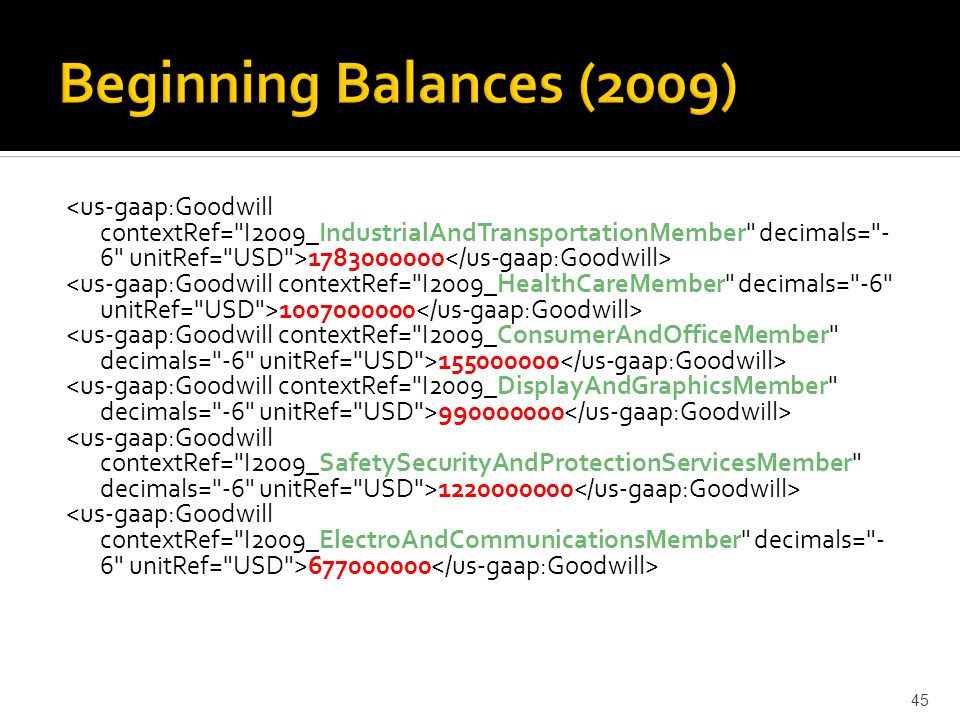

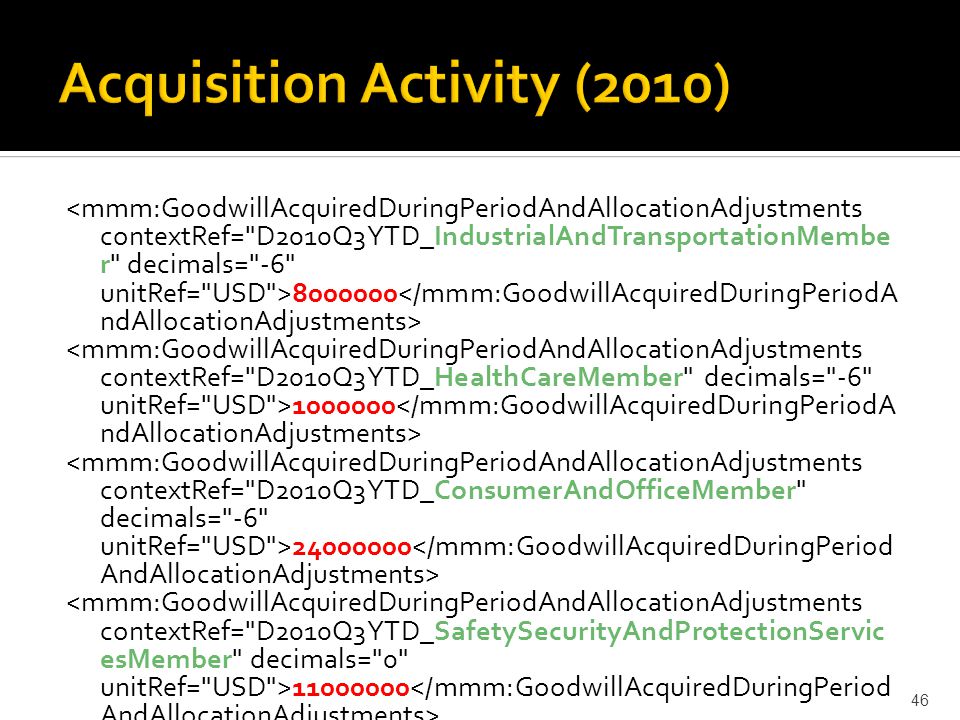

41

Note 3: Purchased goodwill related to the five acquisitions which closed in the first nine months of 2010 totaled $43 million, less than $1 million of which is deductible for tax purposes. The acquisition activity in the following table also includes the impacts of contingent consideration for pre-2009 acquisitions, which increased goodwill by $1 million. The amounts in the “Translation and other” column in the following table primarily relate to changes in foreign currency exchange rates. The goodwill balance by business segment as of December 31, 2009 and September 30, 2010, follow: 41

42

Note 3: Purchased goodwill related to the five acquisitions which closed in the first nine months of 2010 totaled $43 million, less than $1 million of which is deductible for tax purposes. The acquisition activity in the following table also includes the impacts of contingent consideration for pre-2009 acquisitions, which increased goodwill by $1 million. The amounts in the “Translation and other” column in the following table primarily relate to changes in foreign currency exchange rates. The goodwill balance by business segment as of December 31, 2009 and September 30, 2010, follow: 42

43

43000000 1000000 43

44

Goodwill table from footnote Goodwill table from footnote 44

45

1783000000 1007000000 155000000 990000000 1220000000 677000000 45

46

8000000 1000000 24000000 11000000 46

47

15000000 -11000000 6000000 4000000 26000000 -17000000 47

48

1806000000 997000000 185000000 994000000 1257000000 660000000 48

49

SEC Requires filers to use an extension taxonomy Includes only those elements that a company uses for their financial reporting Naming Convention ▪ Shortcompnayname:ccyy-mm-dd

50

Extending XBRL New element names Each Company has its preferred 1. Line Item Name 2. Hierarchy of line items on the F/S 3. Unique items that do not correspond to an element in the taxonomy Items 1 & 2 do NOT impact comparability and reuse 50

51

1. Follow U.S. GAAP taxonomy whenever possible 2. If you don’t see an element in the F/S section, look in the disclosures 3. If you don’t like the label, use the U.S. GAAP element anyway and add a label to the label linkbase (i.e. don’t make up elements because you don’t like the label) 4. For footnotes use proper tags for respective levels 51

4. For footnotes use proper tags for respective levels 51.")

Similar presentations

Embeds XBRL within HTML or XHTML document HTML/XHTML tags used for rendering information.>")