Download presentation

Presentation is loading. Please wait.

1

World Airline Financial Results

2

The airline industry has over the years been buffeted by both economic cycles and threats from terrorism and epidemics. Following seven years of good profitability that stemmed from a relatively long world economic upswing between 1994 and 2000, it suffered a severe setback in the 2000s with the post ‘year 2000’ downturn and the aftermath of 9/11.

3

Cumulative net losses of the world’s scheduled airlines amounted to US$20.3 billion between 1990 and 1993, but this was followed by almost $40 billion in net profits between 1995 and 2000. This highlights the cyclical nature of the industry, and the need to treat with caution comments after the Gulf War recession and 9/11 about the continued ability of the industry to finance expansion.

5

More recently, airlines have devoted much management time to the formation of alliances, some tactical, but many of a more strategic nature which require the blessing of the regulatory authorities. This is arguably the easiest way for an airline to expand in scope and achieve the critical mass to compete against larger airlines and airline groups.

6

The income statement is a historical record of the trading of a business over a specific period (normally one year). It shows the profit or loss made by the business – which is the difference between the firm’s total income and its total costs.

7

The income statement serves several important purposes: Allows shareholders/owners to see how the business has performed and whether it has made an acceptable profit (return) Helps identify whether the profit earned by the business is sustainable (“profit quality”) Enables comparison with other similar businesses (e.g. competitors) and the industry as a whole Allows providers of finance to see whether the business is able to generate sufficient profits to remain viable (in conjunction with the cash flow statement) Allows the directors of a company to satisfy their legal requirements to report on the financial record of the business

and the industry as a whole Allows providers of finance to see whether the business is able to generate sufficient profits to remain viable (in conjunction with the cash flow statement) Allows the directors of a company to satisfy their legal requirements to report on the financial record of the business.")

8

Example Business Ltd Income Statement20012000 Year Ended 31 December£'000 Revenue21,45019,780 Cost of sales13,46512,680 Gross profit7,9857,100 Distribution costs3,2102,985 Administration expenses2,1801,905 Operating profit2,5952,210 Finance costs156120 Profit before tax2,4392,090 Tax expense746580 Profit attributable to shareholders1,6931,510 The structure and format of a typical income statement is illustrated below:

9

CategoryExplanation RevenueThe revenues (sales) during the period are recorded here. Sometimes referred to as the “top line” – revenue shows the total value of sales made to customers Cost of sales The direct costs of generating the recorded revenues go into “cost of sales”. This would include the cost of raw materials, components, goods bought for resale and the direct labour costs of production. The lines in the income statement can be briefly described as follows:

10

Gross profitThe difference between revenue and cost of sales. A simple but very useful measure of how much profit is generated from every £1 of revenue before overheads and other expenses are taken into account. Is used to calculate the gross profit margin (%) Distribution & administration expenses Operating costs and expenses that are not directly related to producing the goods or services are recorded here. These would include distribution costs (e.g. marketing, transport) and the wide range of administrative expenses or overheads that a business incurs. Operating profitA key measure of profit. Operating profit records how much profit has been made in total from the trading activities of the business before any account is taken of how the business is financed. Finance expensesInterest paid on bank and other borrowings, less interest income received on cash balances, is shown here. A useful figure for shareholders to assess how much profit is being used up by the funding structure of the business. Profit before taxCalculated as operating profit less finance expenses

Distribution & administration expenses Operating costs and expenses that are not directly related to producing the goods or services are recorded here. These would include distribution costs (e.g. marketing, transport) and the wide range of administrative expenses or overheads that a business incurs. Operating profitA key measure of profit. Operating profit records how much profit has been made in total from the trading activities of the business before any account is taken of how the business is financed. Finance expensesInterest paid on bank and other borrowings, less interest income received on cash balances, is shown here. A useful figure for shareholders to assess how much profit is being used up by the funding structure of the business. Profit before taxCalculated as operating profit less finance expenses.")

13

The statements that are covered are the profit and loss or income statement, the balance sheet, and the cash flow statement. The value added statement and Cash Value Added (Economic Value Added) is also explained

is also explained.")

14

The Profit and Loss Account or Statement of Earnings summarises the revenues and expenses of the airline for the accounting period: Revenue Conversion of real assets into cash. Under the accrual basis of accounting, cash receipts are allocated to the period in which the related service took place.

15

Expenditure Conversion of cash into real assets. Expenses are charged to Profit and Loss Account in the same accounting period as the one in which the related revenue is recognised. Certain large expenses will need to be charged over a number of years, since these assets will provide the potential to generate revenue over a period that extends well beyond the current accounting period: Aircraft and other fixed assets. Major aircraft and engine overhauls. Software development costs. Slots and new route start-up costs. Goodwill through the acquisition of other companies.

16

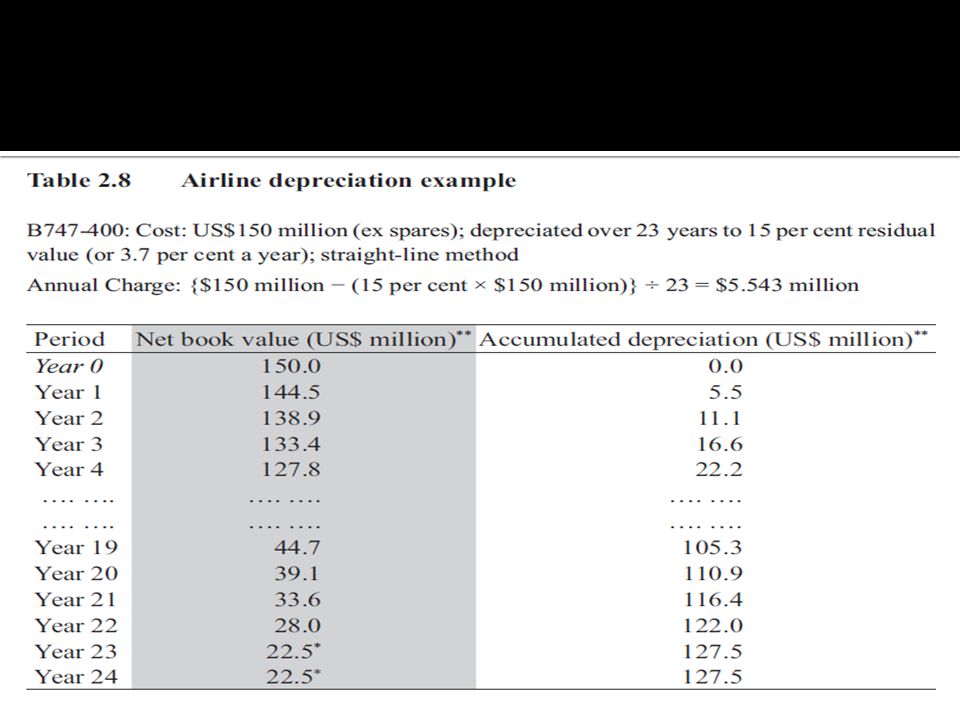

This process of allocation is called depreciation for tangible assets such as aircraft, and amortisation for intangible assets such as goodwill, software or the rights to routes or slots.

17

The Profit and Loss Account or Income Statement can be divided into: Trading or operating account. Profit and loss account or income statement. Appropriation account or statement of earned surplus.

18

The trading or operating account generally excludes interest paid or received, and any gains or losses from sales of assets, which appear in the profit and loss account.

19

From the presentation of BA’s operating account in Table 2.1 it can be seen that some detail is provided of the breakdown of both revenues and expenses. The importance of cargo in scheduled service revenues can also be calculated (6.9 per cent in 2005/2006 compared to 8.1 per cent in 1994/1995).

..")

21

The large increase in ‘other revenues’ occurred mainly as a result of the inclusion of fuel surcharges on air fares and cargo rates. Most airlines include these in passenger and cargo revenues but they could be identified separately or netted off against fuel expenses.

22

BA’s 2005/2006 operating profit recovered with a 27 per cent increase from the previous year with both passenger and cargo yields up, as well as a 0.8 per cent point improvement in passenger load factor. It was also helped by keeping unit costs in check, in spite of the large increase in fuel costs.

24

The remainder of the profit and loss or income statement includes finance costs (e.g., interest payable), finance income (e.g., interest received) and any profits or losses from the sale of fixed assets. Table 2.1 above shows that in 2005/2006 BA’s interest charges declined along with their debt reduction.

25

The other new and significant item in the income statement relates to pensions: an additional amount has to be deducted from profits to make a contribution to the shortfall in pension scheme assets compared to actuarial assumptions on pension obligations that is not already reflected in ‘employee costs’. It should be added that under IFRS BA now include the cost of share options granted to employees (since 2002) under ‘employee costs’, £ 1.8 million being introduced in 2005/2006 for the first time.

under ‘employee costs’, £ 1.8 million being introduced in 2005/2006 for the first time..")

26

Traffic revenue for 2005 comprised €11,314 million from the carriage of passengers and 20 per cent or €2,590 million from freight and mail. Changes in stocks are included as a separate item, in addition to the cost of materials purchased from outside suppliers. This approach is adopted by many European airlines, but not by BA, US or Asian carriers.

27

Lufthansa gives a cost breakdown in footnotes to the main income statement. In 2005, the total cost of materials and services (€9.0 billion): €4,591 million for the cost of materials, of which €2,662 million was for fuel; and €4,416 million for services,€2,542 was for airport and en-route navigation charges, and €142 million from operating leases. The income statement also includes the financial (non-operating) result broken down into income from subsidiaries and associates, net interest and asset write-downs, minority interests and taxes.

: €4,591 million for the cost of materials, of which €2,662 million was for fuel; and €4,416 million for services,€2,542 was for airport and en-route navigation charges, and €142 million from operating leases. The income statement also includes the financial (non-operating) result broken down into income from subsidiaries and associates, net interest and asset write-downs, minority interests and taxes..")

29

With the growth of aircraft operating leases, an increasingly important inconsistency is the treatment of aircraft ownership costs. With owned aircraft, depreciation is treated as an operating cost and interest on any related finance is not. If the same aircraft is acquired under an operating lease, both depreciation and interest (combined as the rental cost) are included as operating costs. This distorts operating profit comparisons.

are included as operating costs. This distorts operating profit comparisons..")

30

Other potential areas of distortion are depreciation policies, major maintenance of aircraft (which may be all included as an expense in one year, or capitalised and amortised over a number of years), and foreign exchange gains or losses. These may be further explained in the notes to the accounts.

31

Agents’ commission is generally recorded as an expense,4 but some airlines deduct it from revenues. Frequent flyer points or credits can also be treated in a number of ways, the most common being to defer the incremental costs of providing the free travel awards.

32

BA uses this approach for its Executive Club and Airmiles loyalty programmes, including incremental passenger service charges, security, fuel, catering and lost baggage insurance in accrued costs. Alternatively, a part of the revenue can be deferred and recognised when the free travel is provided (for a fuller explanation of how FFPs are accounted for, see Appendix 2.1 at the end of this chapter).

..")

33

Finally, there are two ways of treating corporation tax: either full or partial provisioning. The first way assumes that profits will eventually be taxed, and that any generous tax allowances applicable in the year under question will only defer the tax liability to future years.

34

A full provision for corporation tax at the applicable rate (the marginal rate in 2005 being 30 per cent in the UK, and ranges from only 12 per cent in Ireland to almost 40 per cent in the US, Germany and Japan5) is made in the profit and loss account, even though this is not the tax actually charged for that year.

is made in the profit and loss account, even though this is not the tax actually charged for that year.")

Similar presentations

and what a firm owes (liabilities) Asset = Liability.>")

![17-1 Learning Objectives After studying this chapter, you should be able to: [1] Indicate the usefulness of the statement of cash flows. [2] Distinguish.](/20/5984334/big_thumb.jpg "17-1 Learning Objectives After studying this chapter, you should be able to: [1] Indicate the usefulness of the statement of cash flows. [2] Distinguish.>")

Accounting for Government Grants. Scope This Statement does not deal with: (i) the special problems arising in accounting for government grants.>")