Download presentation

Presentation is loading. Please wait.

3

Introduction. Scheme of Sales Tax Act, 1990. Provisions of Section 40 B of the Sales Tax Act, 1990. Ingredients of Section 40 B 1. Material Evidence. Definitions of Material Evidence Case Law 2. Reason to Believe. Meaning of Reason to Believe Citations on “Reason to Believe” 3. Tax Evasion Definition of 'Tax Evasion' Investopedia Explains 'Tax Evasion Judgment of Supreme Court of Pakistan on Tax Evasion 4. Tax Fraud Definition of Tax Fraud Investopedia Explains 'Tax Fraud' Provision of Tax Fraud Under Section 2(37) Relevant citation on Tax Fraud 5. In Writing Citations on “In Writing Remedies:- I. Constitutional Remedy II. Departmental Remedy Examples:- Orders/Notices under section 40B The Sales Tax Act, 1990. Judgments of Lahore High Court, Lahore. Conclusion

Relevant citation on Tax Fraud 5. In Writing Citations on In Writing Remedies:- I. Constitutional Remedy II. Departmental Remedy Examples:- Orders/Notices under section 40B The Sales Tax Act, Judgments of Lahore High Court, Lahore. Conclusion.")

4

1.Under the Sales Tax Act, 1990, the liability to collect and or pay tax by a registered person arises at two stages. The first stage arises at the time of purchases/acquisition of taxable supplies/inputs, by the said person; the tax paid then is known as ‘’input tax’’ under section 2(14) of the Sales Tax Act, 1990. The second stage arises when upon utilization of taxable inputs, the registered persons makes taxable supplies; the tax paid thereon is known as ‘’output tax’’ under section 2(20) of the Sales Tax Act, 1990.

of the Sales Tax Act, The second stage arises when upon utilization of taxable inputs, the registered persons makes taxable supplies; the tax paid thereon is known as ‘’output tax’’ under section 2(20) of the Sales Tax Act,")

5

2.In the above sequence of events, the liability to taxation of the registered person is determined for a tax period, under section 7 of the Act. Therein the input tax already paid is deducted from the output tax, subject to the bar contained viz impermissible adjustment in section 8 of the Sales Tax Act, 1990; the net amount arising thereby is paid, along with the monthly return in the treasury, as per section 6 of the Sales Tax Act, 1990. 3.This chain of supplier and recipient, under the Sales Tax Act, 1990, is an elaborative scheme regulated by various provisions of the mentioned statute wherein the law treats each registered person, within the mentioned chain, to be the agent of the exchequer who collects and pay the tax at each stage of value addition till the time taxable supplies either reach the end consumer and or are exported.

6

4.It is pertinent to mention that on determination of net liability under section 7, the registered person cannot claim input tax of such items which have been declared to inadmissible in terms of section 8 the Sales Tax Act, 1990. The basic scope of inadmissibility, under the mentioned section, is to prohibit the use of input tax paid on any activity which is other than the taxable activity under the Sales Tax Act, 1990. 5.It is also relevant to mention that in the event a registered person, in the afore referred chain of supply, collects the tax but does not deposit the same in the treasury, commits the act of ‘’tax fraud’’ as defined under section 2(37) of the Sales Tax Act, 1990; it is thus liable for both civil and criminal actions as provided in the Sales Tax Act, 1990.

of the Sales Tax Act, 1990; it is thus liable for both civil and criminal actions as provided in the Sales Tax Act,")

7

6.That, it is pertinent to mention that if any tax payer is black listed/suspended/ blocked, the FBR website does not even allow uploading data in respect of the said listed suspended/blocked tax payers. No input tax credit of the said supplier can then be claimed viz the mentioned taxable suppliers. It is therefore clear that input tax on purchases made from an active tax payer only can be claimed under the system. Even in case of small difference between sales tax paid by the suppliers vis-à-vis claimed by the buyer, a disallowed.

8

40B. Posting of 2[ Inland Revenue] Officer.—Subject to such conditions and restrictions, as deemed fit to impose, the 3 [Board], may post Officer of 2 [Inland Revenue] to the premises of registered person or class of such persons to monitor production, sale of taxable goods and the stock position: Provided that if a 4 [Commissioner}, on the basis of material evidence, has reasons to believe that a registered person is involved in evasion of Sales Tax or tax fraud, he may, by recording the reason in writing, post an Officer of 2 [Inland Revenue] to the premises of such registered person to monitor production or sale of taxable goods and the stocks position.

9

1. Material Evidence 2. Reasons to Believe 3. Evasion of Sales Tax 4. Tax Fraud 5. In Writing

10

Definitions “Evidence having some logical connection with the consequential facts or the issues. Cf. relevant evidence”.

11

Black Law Dictionary “ MATERIAL EVIDENCE: - Such as is relevant and goes to the substantial matters in dispute, or has a legitimate and effective influence, or bearing on the decision of the case. Materiality, with reference to evidence does not have the same signification are relevancy.

12

Babylon English “Proof or testimony that has significant relationship with the facts or issue of a case or enquiry and can affect its conclusion or outcome”. “Material Evidence that could affect the decision of a court case”. Wharton “Material evidence (Law), evidence which conduces to the proof or disproof of a relevant hypothesis”.

, evidence which conduces to the proof or disproof of a relevant hypothesis ..")

13

[ (1993)67 tax 311 (H.C. Kar) ] Pakistan Educational Society VS Government of Pakistan The Lordship of Karachi High Court defines the material evidence as under:- “Basic, cardinal, central, compelling, consequential, essential, extensive, far-reaching, fundamental, indispensible, momentous, necessary, paramount, pertinent, pivotal, prevalent, primary, principal, relevant, remarkable, salient, signal, significant, substantial, valuable, vital, weighty, worth considering.”

] Pakistan Educational Society VS Government of Pakistan The Lordship of Karachi High Court defines the material evidence as under:- Basic, cardinal, central, compelling, consequential, essential, extensive, far-reaching, fundamental, indispensible, momentous, necessary, paramount, pertinent, pivotal, prevalent, primary, principal, relevant, remarkable, salient, signal, significant, substantial, valuable, vital, weighty, worth considering. .")

14

Definition “Reason to believe' means “an incident or statement having sufficient circumstantial evidence or support to substantiate the truth” by Mr. Amitava- Indian Scholar

15

“Basis for belief, body of evidence, chain of evidence, clue, data, datum, documentation, evidence, exhibit, fact, facts, grounds, grounds for belief, indication, item of evidence, manifestation, mark, material grounds, muniments, mute witness, piece of evidence, premises, proof, relevant fact, sign, symptom, token”.

16

PLD 1952 FC 19 Moulvi Fazlul Qader Choudhry vs Crown PLD 1971 SC 174 Nisar Ahmad vs The State 1994 SCMR 1283 ; Government of Sindh vs Raeesa Farooq PLD 1968 SC 349 Ch. Abdul Malik vs The State

17

1995 SCMR 1249 Ch. Shujat Hussain VS State The Lordship of Supreme Court speaks about reasons to believe as under:- “The term " reason to believe " can be classified at a higher padestal than mere suspicion and allegation but not equivalent to proved evidence. Even the strongest suspicion cannot transform in " reason to believe ".

18

Definition:- “An illegal practice where a person, organization or intentionally avoids paying his/her/its true tax liability. Those caught evading taxes are generally subject to criminal charges and substantial penalties”.

19

There is a difference between tax minimization/avoidance and tax evasion. All citizens have the right to reduce the amount of taxes they pay as long as it is by legal means

20

1993 SCMR 1267 Commissioner Of Income Tax VS Sultan Ali Jeoffrey

21

The Lordship of Supreme Court deduces the meaning of Tax Evasion as under:- " Evasion " with reference to taxation laws ‑‑‑ Meaning. Evasion with reference to taxation laws means to illegally manipulate things in such a manner that the tax payable under law cannot be assessed. By an act of evasion the assessee can reduce his tax liability or completely eliminate it. Evasion of tax or duty is always in breach of the applicable and binding law. In taxation laws evasion will mean adoption of such deceitful mechanism and manipulation not permitted by law which may result in reduction or elimination of legal tax liability. In the field of taxation, tax avoidance and tax evasion are two different terminologies conveying completely different meaning. Cont…

22

Tax avoidance occurs when a person in a legitimate manner as provided by law adopts a course by which the tax liability is reduced or eliminated. In doing so the assessee seeks his remedy and mechanism within the provisions of law. Avoidance of tax is not tax evasion and it carries no ignominy with it, for it is sound law and, certainly not bad morality for anybody to so arrange his affairs as to reduce the brunt of taxation to a minimum. Avoidance of tax by adopting legal methods will not amount to evasion of tax. But the moment avoidance is sought by illegal contrivance, deceitful methods and adopting a course not permissible in law, it turns into evasion.

23

Definition:- “Tax fraud occurs when an individual or business entity willfully and intentionally falsifies information on a tax return in order to limit the amount of tax liability. Tax fraud essentially entails cheating on a tax return in an attempt to avoid paying the entire tax obligation. Examples of tax fraud include claiming false deductions; claiming personal expenses as business expenses; and not reporting income”.

24

Tax fraud involves the deliberate misrepresentation or omission of data on a tax return. In the United States, taxpayers are bound by a legal duty to voluntarily file a tax return and to pay the correct amount of income, employment and excise taxes. Failure to do so by falsifying or withholding information is against the law and constitutes tax fraud. Tax fraud is investigated by the Internal Revenue Service Criminal Investigation (CI) unit.

unit..")

25

(37) "tax fraud" means knowingly, dishonestly or fraudulently and without any lawful excuse (burden of proof of which excuse shall be upon the accused) -- (i) doing of any act or causing to do any act; or (ii) omitting to take any action or causing the omission to take any action,(including the making of taxable supplies without getting registration under this Act; (iii) falsifying (or causing falsification) the sales tax invoice) in contravention of duties or obligations imposed under this Act or rules or instructions issued thereunder with the intention of understating the tax liability (or underpaying the tax liability for two consecutive tax periods or overstating the entitlement to tax credit or tax refund to cause loss of tax;

tax fraud means knowingly, dishonestly or fraudulently and without any lawful excuse (burden of proof of which excuse shall be upon the accused) -- (i) doing of any act or causing to do any act; or (ii) omitting to take any action or causing the omission to take any action,(including the making of taxable supplies without getting registration under this Act; (iii) falsifying (or causing falsification) the sales tax invoice) in contravention of duties or obligations imposed under this Act or rules or instructions issued thereunder with the intention of understating the tax liability (or underpaying the tax liability for two consecutive tax periods or overstating the entitlement to tax credit or tax refund to cause loss of tax;")

26

2004 PTD 868 Al Hilal Motors Stores VS Collector Sales Tax & Others.

27

Their Lordships of Karachi High Court spells about the ratio of Tax Fraud as under:- “The provisions contained in section 2(37) defining the expression ‘’tax-fraud’’ without realizing that in order to attract the above provision, the initial burden lies on the Department to show that an assessee, knowingly, dishonestly or fraudulently and without any lawful excuse has done any act or has caused to be done or has omitted to take any action or has caused the omission to take any action in contravention of duties or obligations imposed under this Act or rules or instruction issued thereunder with the intention of understanding the tax liability or underpaying the tax liability. Once this burden is discharged by the Department, only then, the burden is shifted to the assessee to establish that the act done was without any knowledge on his part or without any intention of dishonesty or fraud and was done with any lawful excuse”.

28

After the insertions of Article 10A through 18 th Amendment in the Constitution of Islamic Republic of Pakistan now due process of law has become the fundamental right of every citizen of Pakistan. Due process of law includes notice of hearing, reply of the person and then an reasoned order in writing. All orders/notices should be in written form.

29

2007 S C M R 1328 CAPITAL DEVELOPMENT AUTHORITY VS Mrs. SHAHEEN FAROOQ “Verbal order has no sanctity in law and such orders are alien to the process of the law and the Courts. All orders passed and acts performed, particularly, by the State/public functionaries adversely affecting anyone must be in writing, as section 24-A(1) of the General Clauses Act, 1897 envisages that the powers shall be exercised reasonably, fairly and justly and subsection (2) further makes it necessary that the authority passing orders shall, so far as necessary or appropriate, give reasons for making the orders and unless the order is in writing, the reasons and fairness etc. thereof cannot be ascertained/ adjudged”.

of the General Clauses Act, 1897 envisages that the powers shall be exercised reasonably, fairly and justly and subsection (2) further makes it necessary that the authority passing orders shall, so far as necessary or appropriate, give reasons for making the orders and unless the order is in writing, the reasons and fairness etc. thereof cannot be ascertained/ adjudged ..")

30

PLD 1979 Lahore 699 Munawar-ud-Din VS Federation of Pakistan “It is a well established position of law and practice that the public functionaries have to pass all orders in writing. It is necessary for the purpose of record and responsibility and to judge their validity”. Since it is specifically provided in section 38 that the action specified therein can be taken by any Officer authorized in this behalf by the Board or Collector, thereof, it is held that such authorization should precede the action and shall always be in writing failing which all the actions taken under section 38 shall be treated as illegal and void”.

31

2004 PTD 2952(K.H.C) N.P. Water Proof Textile Mills (Pvt.) Limited Vs Federation of Pakistan “It is further held that all matters where a public officer is supposed to pass an order which can be exposed to the scrutiny of Appellate Courts /Superior Courts in exercise of Judicial review of administrative actions the orders must always be in writing”.

Limited Vs Federation of Pakistan It is further held that all matters where a public officer is supposed to pass an order which can be exposed to the scrutiny of Appellate Courts /Superior Courts in exercise of Judicial review of administrative actions the orders must always be in writing ..")

32

Constitutional Remedies Remedies under the statute

33

Article 18 of the Constitution of Islamic Republic of Pakistan ensures that the right to freedom of trade business and profession can not be taken away from any citizen. Reliance is placed on:- o 2008 CLC 1132 o 2005 PTD 2442 o 2011 SCMR 848

34

Appeal under section 46 of the Sales Tax Act, 1990.

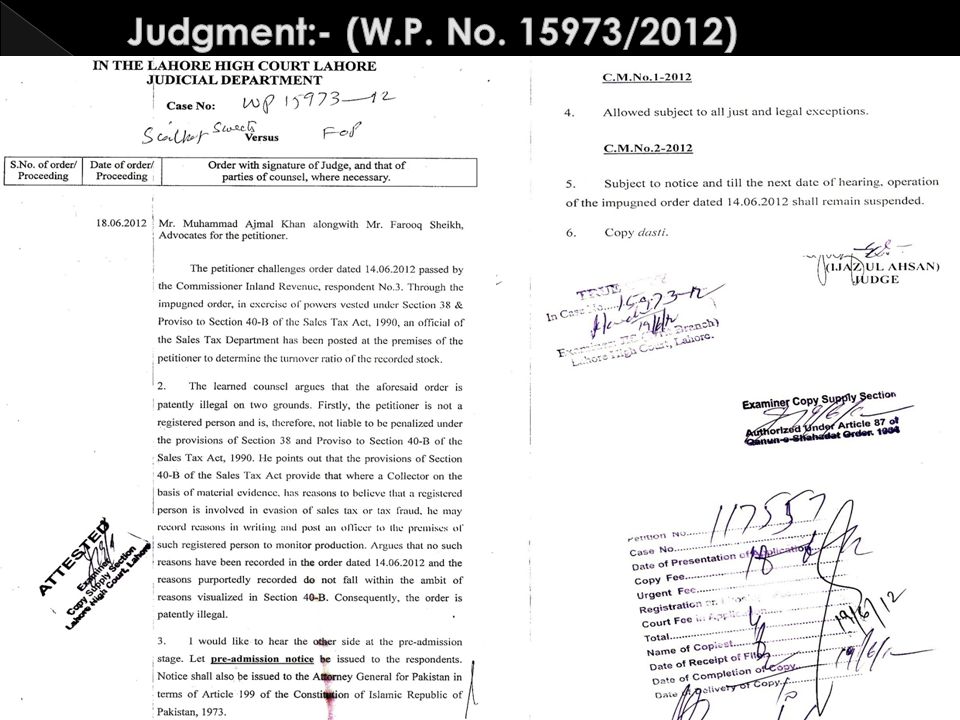

35

Orders/Notices Judgments of Lahore High Court, Lahore.

Similar presentations

n Role of the IRS n Audits of tax returns n Requests for rulings n Due dates.>")

>")

![Service Tax Voluntary Compliance Encouragement Scheme, 2013 [Chapter VI of Finance Act, 2013] Amnesty Scheme – Updated with Department Clarification.](/20/6206440/big_thumb.jpg "Service Tax Voluntary Compliance Encouragement Scheme, 2013 [Chapter VI of Finance Act, 2013] Amnesty Scheme – Updated with Department Clarification.>")

>")