Download presentation

Presentation is loading. Please wait.

1

Overview of Credit Policy and Loan Characteristics

13

2

Recent Trends in Loan Growth and Quality

Larger banks have, on average, recently reduced their dependence on loans relative to smaller banks. Real estate loans represent the largest single loan category for banks. Residential 1-4 family homes contribute the largest amount of real estate loans for banks. Commercial real estate is highest for banks with $100 million to $1 billion in assets

3

Recent Trends in Loan Growth and Quality

Commercial and industrial loans represent the second highest concentration of loans at banks Loans to individuals are greatest for banks with more than $1 billion in assets Farmland and farm loans make up a significant portion of the smallest banks’ loans

5

Recent Trends in Loan Growth and Quality

Wholesale Bank Emphasizes lending to businesses Retail Bank Emphasizes lending to individuals Primary funding is from core deposits

6

Recent Trends in Loan Growth and Quality

FDIC Bank Categories Credit Card Banks International Banks Agricultural Banks Commercial Lenders Vast majority of FDIC-insured institutions fall in this category

7

Recent Trends in Loan Growth and Quality

FDIC Bank Categories Mortgage Lenders Consumer Lenders Other Specialized Banks (less than $1 billion) All Other Banks (less than $1 billion) All Other Banks (more than $1 billion)

All Other Banks (less than $1 billion) All Other Banks (more than $1 billion)")

11

Recent Trends in Loan Growth and Quality

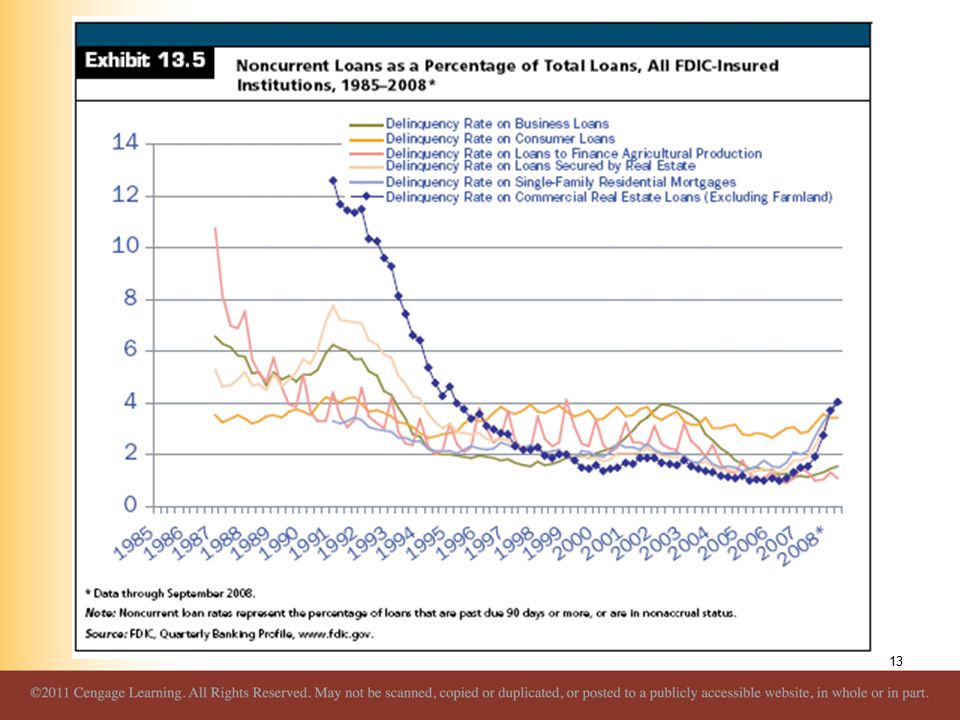

Noncurrent Loans Loans and leases past due 90 days or more and still accruing interest plus all loans and leases in a nonaccrual status Nonaccrual loans and leases are those: that are maintained on a cash basis because of deterioration in the financial position of the borrower where full payment of interest and principal is not expected where principal or interest has been in default for a period of 90 days or more, unless the obligation is both well secured and in the process of collection

12

Recent Trends in Loan Growth and Quality

Net Losses (Net Charge-offs) The dollar amount of loans that are formally charged off as uncollectible minus the dollar value of recoveries on loans previously charged off

The dollar amount of loans that are formally charged off as uncollectible minus the dollar value of recoveries on loans previously charged off.")

16

Measuring Aggregate Asset Quality

It is extremely difficult to assess individual asset quality using aggregate quality data Different types of assets and off-balance sheet activities have different default probabilities Loans typically exhibit the greatest credit risk Historical charge-offs and past-due loans might understate (or overstate) future losses depending on the future economic and operational conditions of the borrower

future losses depending on the future economic and operational conditions of the borrower.")

17

Measuring Aggregate Asset Quality

Concentration Risk Exists when banks lend in a narrow geographic area or concentrate their loans in a certain industry Country Risk Refers to the potential loss of interest and principal on international loans due to borrowers in a country refusing to make timely payments

18

Trends in Competition for Loan Business

In 1984, there were nearly 14,500 banks in the U.S. This fell to fewer than 7,300 at the beginning of 2007 Recently, the Treasury’s efforts to provide capital to banks via TARP further differentiated between strong and weaker banks, as those in the worst condition did not qualify for the capital and ultimately either failed or were forced to sell This has forced consolidation

19

Trends in Competition for Loan Business

Banks still have the required expertise and experience to make them the preferred lender for many types of loans Technology advances have meant that more loans are becoming “standardized,” making it easier for market participants to offer loans in direct competition to banks

20

Trends in Competition for Loan Business

Structured Note Loan that is specifically designed to meet the needs of one or a few companies but has been packaged for resale

21

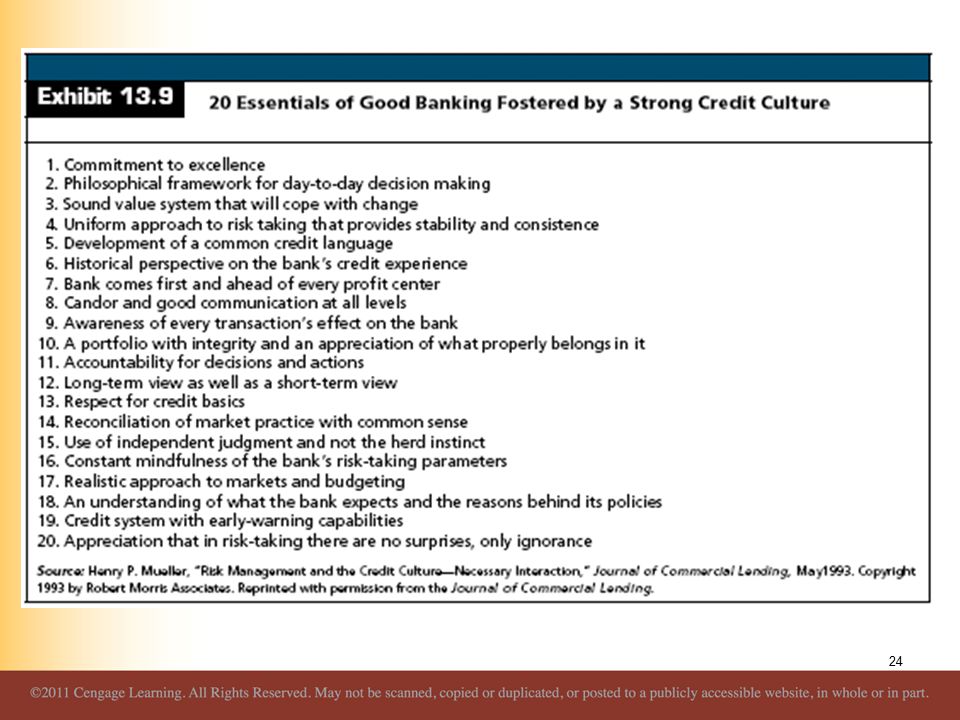

The Credit Process Loan Policy Credit Philosophy Credit Culture

Formalizes lending guidelines that employees follow to conduct bank business Credit Philosophy Management’s philosophy that determines how much risk the bank will take and in what form Credit Culture The fundamental principles that drive lending activity and how management analyzes risk

22

The Credit Process

23

The Credit Process Credit Culture

The fundamental principles that drive lending activity and how management analyzes risk Values Driven Focus is on credit quality Current-Profit Driven Focus is on short-term earnings Market-Share Driven Focus is on having the highest market share

25

The Credit Process Business Development and Credit Analysis

Market research Train employees: What products are available What products customers are likely to need How they should communicate with customers about those needs Advertising and Public Relations Officer Call Programs

26

The Credit Process Business Development and Credit Analysis

Evaluate a borrower’s ability and willingness to repay Questions to address What risks are inherent in the operations of the business? What have managers done or failed to do in mitigating those risks? How can a lender structure and control its own risks in supplying funds?

27

The Credit Process Business Development and Credit Analysis

Five C’s of Good Credit Character Capital Capacity Conditions Collateral

28

The Credit Process Business Development and Credit Analysis

Five C’s of Bad Credit Complacency Carelessness Communication Contingencies Competition

29

The Credit Process Business Development and Credit Analysis

Procedure Collect information for the credit file Evaluate management, the company, and the industry in which it operates Conduct a financial statement analysis Project the borrower’s cash flow and its ability to service the debt Evaluate collateral or the secondary source of repayment Write a summary analysis and making a recommendation

30

The Credit Process Credit Execution and Administration Loan Decision

Individual officer decision Committee Centralized underwriting

31

The Credit Process Credit Execution and Administration Loan Agreement

Formalizes the purpose of the loan Terms of the loan Repayment schedule Collateral required Any loan covenants States what conditions bring about a default

32

The Credit Process Credit Execution and Administration

Documentation: Perfecting the Security Interest Perfected When the bank's claim is superior to that of other creditors and the borrower Require the borrower to sign a security agreement that assigns the qualifying collateral to the bank Bank obtains title to equipment or vehicles

33

The Credit Process Credit Execution and Administration Position Limits

Maximum allowable credit exposures to any single borrower, industry, or geographic local Risk Rating Loans Evaluating characteristics of the borrower and loan to assess the likelihood of default and the amount of loss in the event of default

34

The Credit Process Credit Execution and Administration Loan Covenants

Positive (Affirmative) Indicate specific provisions to which the borrower must adhere Negative Indicate financial limitations and prohibited events

Indicate specific provisions to which the borrower must adhere. Negative. Indicate financial limitations and prohibited events.")

36

The Credit Process Credit Execution and Administration Loan Review

Monitoring the performance of existing loans Handling problem loans Loan review should be kept separate from credit analysis, execution, and administration The loan review committee should act independent of loan officers and report directly to the CEO of the bank

37

The Credit Process Credit Execution and Administration Problem Loans

Often require special treatment Modify terms of the loan agreement to increases the probability of full repayment Modifications might include: Deferring interest and principal payments Lengthening maturities Liquidating unnecessary assets

38

Characteristics of Different Types of Loans

UBPR Classifications Real Estate Loans Commercial Loans Individual Loans Agricultural Loans Other Loans and Leases in Domestic Offices Loans and Leases in Foreign Offices

39

Characteristics of Different Types of Loans

Real Estate Loans Construction and Development Loans Commercial Real Estate Multi-Family Residential Real Estate 1-4 Family Residential Home Equity Farmland Other Real Estate Loans

40

Characteristics of Different Types of Loans

Real Estate Loans Commercial Real Estate Loans Typically short-term loans consisting of: Construction and Real Estate Development Loans Land Development Loans Commercial Building Construction and Land Development Loans

41

Characteristics of Different Types of Loans

Real Estate Loans Commercial Real Estate Loans Construction Loans Interim financing on commercial, industrial, and multi-family residential property Interim Loans Provide financing for a limited time until permanent financing is arranged Land Development Loans Finance the construction of road and public utilities in areas where developers plan to build houses Developers typically repay loans as lots or homes are sold

42

Characteristics of Different Types of Loans

Real Estate Loans Commercial Real Estate Loans Takeout Commitment An agreement whereby a different lender agrees to provide long-term financing after construction is finished

43

Characteristics of Different Types of Loans

Real Estate Loans Residential Mortgage Loans Mortgage Legal document through which a borrower gives a lender a lien on real property as collateral against a debt Most are amortized with monthly payments, including principal and interest

44

Characteristics of Different Types of Loans

Real Estate Loans Residential Mortgage Loans 1-4 Family Residential Mortgage Loans Holding long-term fixed-rate mortgages can create interest rate risk for banks with loss potential if rates increase To avoid this, many mortgages now provide for: Periodic adjustments in the interest rate Adjustments in periodic principal payments The lender sharing in any price appreciation of the underlying asset at sale All of these can increase cash flows to the lender when interest rates rise

45

Characteristics of Different Types of Loans

Real Estate Loans The Secondary Mortgage Market Involves the trading of previously originated residential mortgages Can be sold directly to investors or packaged into mortgage pools

46

Characteristics of Different Types of Loans

Real Estate Loans Home Equity Loans Second Mortgage Loans Typically shorter term than first mortgages Subordinated to first mortgage Home Equity Lines of Credit (HELOC)

")

47

Characteristics of Different Types of Loans

Real Estate Loans Equity Investments in Real Estate Historically, commercial banks have been prevented from owning real estate except for their corporate offices or property involved in foreclosure Regulators want banks to engage in speculative real estate activities only through separate subsidiaries The Gramm-Leach-Bliley Act of 1999 allowed for commercial banks and savings institutions to enter into the merchant banking business

48

Characteristics of Different Types of Loans

Commercial Loans Loan Commitment/Line of Credit Formal agreement between a bank and borrower to provide a fixed amount of credit for a specified period The customer determines the timing of actual borrowing

49

Characteristics of Different Types of Loans

Commercial Loans Working Capital Requirements Net Working Capital Current assets – Current liabilities For most firms, net working capital is positive, indicating that some current assets are not financed with current liabilities

50

Characteristics of Different Types of Loans

Commercial Loans Working Capital Requirements Days Cash Cash/(Sales/365) Days Receivables AR/(Sales/365) Days Inventory Inventory/(COGS/365)

Days Receivables. AR/(Sales/365) Days Inventory. Inventory/(COGS/365)")

51

Characteristics of Different Types of Loans

Commercial Loans Working Capital Requirements Days Payable AP/(Purchases/365) Days Accruals Accruals/(Operating Expenses/365)

Days Accruals. Accruals/(Operating Expenses/365)")

52

Characteristics of Different Types of Loans

Commercial Loans Working Capital Requirements Cash-to-Cash Asset Cycle How long the firm must finance operating cash, inventory and accounts receivables from the day of first sale Cash-to-Cash Liability Cycle How long a firm obtains interest-free financing from suppliers in the form of accounts payable and accrued expenses to help finance the asset cycle

54

Characteristics of Different Types of Loans

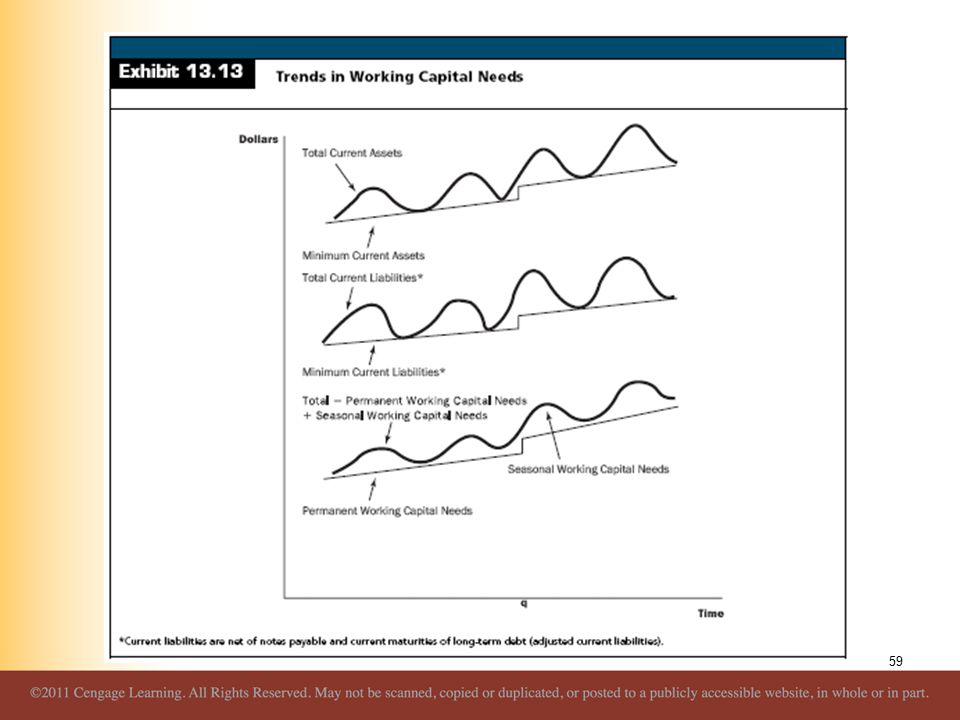

Commercial Loans Working Capital Requirements

55

Characteristics of Different Types of Loans

Commercial Loans Seasonal versus Permanent Working Capital Needs All firms need some minimum level of current assets and current liabilities The amount of current assets and current liabilities will vary with seasonal patterns

56

Characteristics of Different Types of Loans

Commercial Loans Seasonal versus Permanent Working Capital Needs Permanent Working Capital The minimum level of current assets minus the minimum level of adjusted current liabilities Adjusted Current Liabilities Current liabilities net of short-term bank credit and current maturities of long-term debt

57

Characteristics of Different Types of Loans

Commercial Loans Seasonal versus Permanent Working Capital Needs Seasonal Working Capital Difference in total current assets and adjusted current liabilities

58

Characteristics of Different Types of Loans

Commercial Loans Seasonal Working Capital Loans Finance a temporary increase in net current assets above the permanent requirement Loan is seasonal if the need arises on a regular basis and if the cycle completes itself within one year Loan is self-liquidating if repayment derives from sales of the finished goods that are financed

60

Characteristics of Different Types of Loans

Commercial Loans Short-Term Commercial Loans Short-term funding needs are financed by short-term loans, while long-term needs are financed by term loans with longer maturities

61

Characteristics of Different Types of Loans

Commercial Loans Open Credit Lines Used to meet many types of temporary needs in addition to seasonal needs Informal Credit Line Not legally binding but represent a promise that the lender will advance credit Formal Credit Line Legally binding even though no written agreement is signed A commitment fee is charged for making credit available, regardless of whether the customer actually uses the line

62

Characteristics of Different Types of Loans

Commercial Loans Asset-Based Loans Loans Secured by Accounts Receivable The security consists of paper assets that presumably represent sales The quality of the collateral depends on the borrower’s integrity in reporting actual sales and the credibility of billings

63

Characteristics of Different Types of Loans

Commercial Loans Asset-Based Loans Loans Secured by Accounts Receivable Accounts Receivable Aging Schedule List of A/Rs grouped according to the month in which the invoice is dated Lockbox Customer’s mail payments go directly to a P.O. Box controlled by the bank The bank processes the payments and reduces the borrower’s balance but charges the borrower for handling the items

64

Characteristics of Different Types of Loans

Commercial Loans Highly Levered Transactions Leveraged Buyout (LBO) Involves a group of investors, often part of the management team, buying a target company and taking it private with a minimum amount of equity and a large amount of debt Target companies are generally those with undervalued hard assets

Involves a group of investors, often part of the management team, buying a target company and taking it private with a minimum amount of equity and a large amount of debt. Target companies are generally those with undervalued hard assets.")

65

Characteristics of Different Types of Loans

Commercial Loans Highly Levered Transactions Leveraged Buyout (LBO) The investors often sell specific assets or subsidiaries to pay down much of the debt quickly If key assets have been undervalued, the investors may own a downsized company whose earnings prospects have improved and whose stock has increased in value The investors sell the company or take it public once the market perceives its greater value

The investors often sell specific assets or subsidiaries to pay down much of the debt quickly. If key assets have been undervalued, the investors may own a downsized company whose earnings prospects have improved and whose stock has increased in value. The investors sell the company or take it public once the market perceives its greater value.")

66

Characteristics of Different Types of Loans

Commercial Loans Highly Levered Transactions Arise from three types of transactions LBOs in which debt is substituted for privately held equity Leveraged recapitalizations in which borrowers use loan proceeds to pay large dividends to shareholders Leveraged acquisitions in which a cash purchase of another related company produces an increase in the buyer’s debt structure

67

Characteristics of Different Types of Loans

Commercial Loans Highly Levered Transactions An HLT must involve the buyout, recapitalization, or acquisition of a firm in which either: The firm’s subsequent leverage ratio exceeds 75 percent The transaction more than doubles the borrower’s liabilities and produces a leverage ratio over 50 percent The regulators or firm that syndicates the loans declares the transaction an HLT

68

Characteristics of Different Types of Loans

Commercial Loans Term Commercial Loans Original maturity greater than 1 year Typically finance: Depreciable assets Start-up costs for a new venture Permanent increase in the level of working capital

69

Characteristics of Different Types of Loans

Commercial Loans Term Commercial Loans Lenders focus more on the borrower’s periodic income and cash flow rather than the balance sheet Term loans often require collateral, but this represents a secondary source of repayment in case the borrower defaults

70

Characteristics of Different Types of Loans

Commercial Loans Term Commercial Loans Balloon Payments Most of the principal is due at maturity Bullet Payments All of the principal is due at maturity

71

Characteristics of Different Types of Loans

Commercial Loans Revolving Credits A hybrid of short-term working capital loans and term loans Typically involves the commitment of funds for 1 – 5 years At the end of some interim period, the outstanding principal converts to a term loan During the interim period, the borrower determines how much credit to use Mandatory principal payments begin once the revolver is converted to a term loan

72

Characteristics of Different Types of Loans

Agricultural Loans Proceeds are used to purchase seed, fertilizer and pesticides and to pay other production costs Farmers expect to repay the debt with the crops are harvested and sold Long-term loans finance livestock, equipment, and land purchases The primary source of repayment is cash flow from the sale of livestock and harvested crops in excess of operating expenses

73

Characteristics of Different Types of Loans

Consumer Loans Installment Require periodic payments of principal and interest Credit Card Non-Installment For special purposes Example: Bridge loan for the down payment on a house that is repaid from the sale of the previous house

74

Characteristics of Different Types of Loans

Venture Capital A broad term use to describe funding acquired in the earlier stages of a firm’s economic life Due to the high leverage and risk involved banks generally do not participate directly in venture capital deals Some banks have subsidiaries that finance certain types of equity participations and venture capital deals, but their participation is limited

75

Characteristics of Different Types of Loans

Venture Capital Venture capital firms attempt to add value to the firm without taking majority control Often, venture capital firms not only provide financing but experience, expertise, contacts, and advice when required

76

Characteristics of Different Types of Loans

Venture Capital Types of Venture Financing Seed or Start-up Capital Early stages of financing Highly levered transactions in which the venture capital firm will lend money for a percentage stake in the firm Rarely, if ever, do banks participate at this stage

77

Characteristics of Different Types of Loans

Venture Capital Types of Venture Financing Later-Stage Development Financing: Expansion and replacement financing Recapitalization or turnaround financing Buy-out or buy-in financing Mezzanine financing Banks do participate in these rounds of financing, but if the company is overleveraged at the onset, the banks will be effectively excluded from these later rounds of financing

78

Evaluating Commercial Loan Requests and Managing Credit Risk

14

79

Evaluating Commercial Loan Requests and Managing Credit Risk

Important Questions Regarding Commercial Loan Requests What is the character of the borrower and quality of information provided? What are the loan proceeds going to be used for? How much does the customer need to borrow? What is the primary source of repayment, and when will the loan be repaid? What is the secondary source of repayment; that is, what collateral, guarantees, or other cash inflows are available?

80

Fundamental Credit Issues

There are two types of loan errors Type I Error Making a loan to a customer who will ultimately default Type II Error Denying a loan to a customer who would ultimately repay the debt

81

Fundamental Credit Issues

Character of the Borrower and Quality of Data Provided The most important issue in assessing credit risk is determining a borrower’s commitment and ability to repay debts in accordance with the terms of a loan agreement The best indicators are the borrower’s financial history and personal references

82

Fundamental Credit Issues

Character of the Borrower and Quality of Data Provided Audited financial statements are preferred in determining the quality of the data because accounting rules are well established so that an analyst can better understand the underlying factors that affect the entries But just because a company has audited financial statements, however, does not mean the reported data are not manipulated

83

Fundamental Credit Issues

Use of Loan Proceeds Loan proceeds should be used for legitimate business operating purposes, including seasonal and permanent working capital needs, the purchase of depreciable assets, physical plant expansion, acquisition of other firms, and extraordinary operating expenses Speculative asset purchases and debt substitutions should be avoided

84

Fundamental Credit Issues

How Much Does the Borrower Need? The Loan Amount Borrowers often request a loan before they clearly understand how much external financing is actually needed and how much is available internally The amount of credit required depends on the use of the proceeds and the availability of internal sources of funds

85

Fundamental Credit Issues

How Much Does the Borrower Need? The Loan Amount For a shorter-term loan, the amount might equal the temporary seasonal increase in receivables and inventory net of that supported by increased accounts payable With term loans, the amount can be determined via pro forma analysis which is the projecting or forecasting of a company’s financial statements into the future

86

Fundamental Credit Issues

The Primary Source and Timing of Repayment Loans are repaid from cash flows: Liquidation of assets Cash flow from normal operations New debt issues New equity issues

87

Fundamental Credit Issues

The Primary Source and Timing of Repayment Specific sources of cash are generally associated with certain types of loans Short-term, seasonal working capital loans are normally repaid from the liquidation of receivables or reductions in inventory

88

Fundamental Credit Issues

The Primary Source and Timing of Repayment Specific sources of cash are generally associated with certain types of loans Term loans are typically repaid out of cash flows from operations, specifically earnings and noncash charges in excess of net working capital needs and capital expenditures needed to maintain the existing fixed asset base

89

Fundamental Credit Issues

The Primary Source and Timing of Repayment The primary source of repayment on the loan can also determine the risk of the loan The general rule is not to rely on the acquired asset or underlying collateral as the primary source of repayment

90

Fundamental Credit Issues

Secondary Source of Repayment: Collateral Collateral must exhibit three features Its value should always exceed the outstanding principal on a loan The lower the loan-to-value (LTV) ratio, the more likely a the lender can sell the collateral for more than the balance due and reduce loses Borrowers are “upside-down” on a loan if the value of the collateral is less than the outstanding loan balance

ratio, the more likely a the lender can sell the collateral for more than the balance due and reduce loses. Borrowers are upside-down on a loan if the value of the collateral is less than the outstanding loan balance.")

91

Fundamental Credit Issues

Secondary Source of Repayment: Collateral Collateral must exhibit three features The lender should be able to easily take possession of the collateral and have a ready market for its sale A lender must be able to clearly mark the collateral as its own Careful loan documentation is required to “perfect” the bank’s interest in the collateral If collateral is not readily available, a personal guarantee may be required

92

Fundamental Credit Issues

Secondary Source of Repayment: Collateral The borrower’s cash flow is the preferred source of loan repayments Liquidating collateral is secondary There are significant transactions costs associated with foreclosure Bankruptcy laws allow borrowers to retain possession of the collateral long after they have defaulted When the bank takes possession of the collateral, it deprives the borrower of the opportunity to salvage the company

93

Evaluating Credit Requests: A Four-Part Process

Overview of management, operations, and the firm’s industry Common size and financial ratio analysis Analysis of cash flow Projections and analysis of the borrower’s financial condition

94

Evaluating Credit Requests: A Four-Part Process

Overview of Management, Operations, and the Firm’s Industry Gather background information on the firm’s operations Write a Business and Industry Outlook report Examine the nature of the borrower’s loan request and the quality of the financial data provided

95

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Common size ratio comparisons are valuable because they adjust for size and thus enable comparisons across firms in the same industry or line of business

97

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Most analysts differentiate between at least four categories of ratios: Liquidity ratios Indicate a firm’s ability to meet its short-term obligations and continue operations. Activity ratios Signal how efficiently a firm uses assets to generate sales

98

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Most analysts differentiate between at least four categories of ratios: Leverage ratios Indicate the mix of the firm’s financing between debt and equity and potential earnings volatility Profitability ratios Provide evidence of the firm’s sales and earnings performance

100

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Liquidity Ratios Current Ratio CA / CL Quick Ratio (Cash + A/R) / CL

/ CL.")

101

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Activity Ratios Days Cash Cash/Average Daily Sales Days Inventory on Hand Inventory/Average Daily Cost of Goods Sold Inventory Turnover COGS / Average Inventory

102

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Activity Ratios Days Accounts Receivable Collection Period A/R / Average Daily Sales Days Cash-to-Cash Cycle Days Cash + Days A/R + Days Inventory on Hand

103

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Activity Ratios Days Accounts Payable Outstanding A/P / Average Daily Purchases Purchases COGS + ΔInventory Sales-to-Asset Ratio Sales/Net Fixed Assets

104

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Leverage Ratios Debt to Tangible Net Worth Total Liabilities/Tangible Net Worth Debt to Total Assets Total Debt/Total Assets Times Interest Earned EBIT/Interest Expense EBIT Earnings Before Taxes + Interest Expense

105

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Leverage Ratios Fixed Charge Coverage (EBIT + Lease Payments)/(Interest Expense + Lease Payments) Net Fixed Assets to Tangible Net Worth Net Fixed Assets/Tangible Net Worth Dividend Payout Cash Dividends Paid/Net Income

/(Interest Expense + Lease Payments) Net Fixed Assets to Tangible Net Worth. Net Fixed Assets/Tangible Net Worth. Dividend Payout. Cash Dividends Paid/Net Income.")

106

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Profitability Analysis Profit Margin (PM) Net Income/Sales 1 – Expenses/Sales 1 – (COGS/Sales) – (Operating Expenses/Sales) – (Other Expenses/Sales) – (Taxes/Sales)

Net Income/Sales. 1 – Expenses/Sales. 1 – (COGS/Sales) – (Operating Expenses/Sales) – (Other Expenses/Sales) – (Taxes/Sales)")

107

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Profitability Analysis Asset Utilization (AU) Sales/Total Assets Return on Assets Net Income/Total Assets PM × AU

Sales/Total Assets. Return on Assets. Net Income/Total Assets. PM × AU.")

108

Evaluating Credit Requests: A Four-Part Process

Common Size and Financial Ratio Analysis Profitability Analysis Equity Multiplier (EM) Total Assets/Equity Return on Equity (ROE) Net Income/Equity ROA × EM Sales Growth Demonstrates whether a firm is expanding or contracting

Total Assets/Equity. Return on Equity (ROE) Net Income/Equity. ROA × EM. Sales Growth. Demonstrates whether a firm is expanding or contracting.")

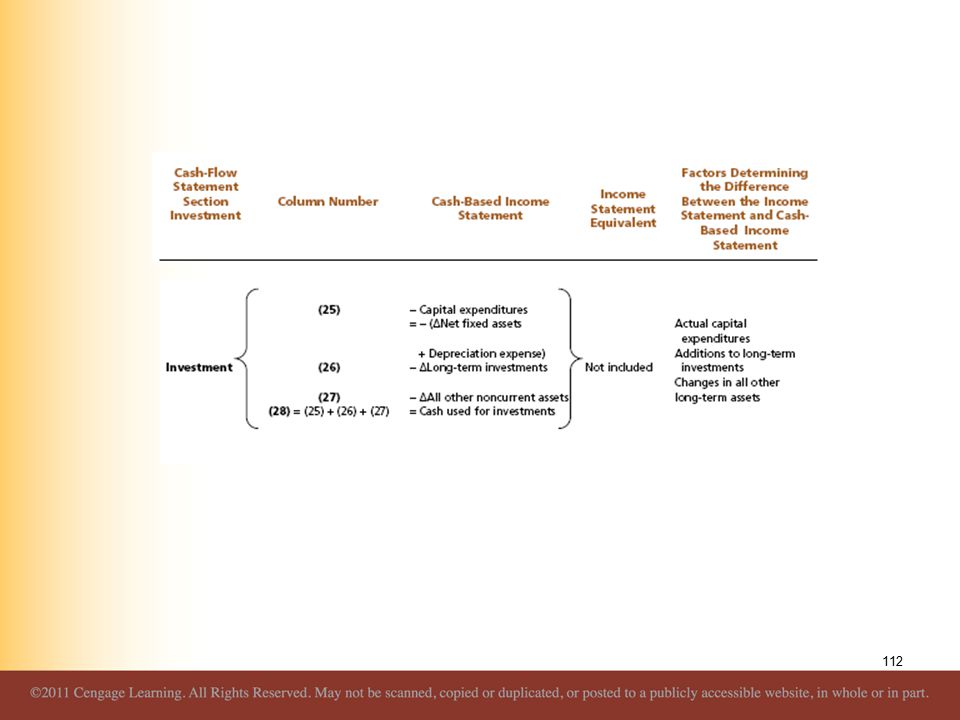

110

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis Cash-Based Income Statement Modified form of a direct statement of cash flows

114

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis Cash-Flow Statement Format Operations Section Income statement items and the change in current assets and current liabilities (except bank debt) Investments Section The change in all long-term assets

Investments Section. The change in all long-term assets.")

115

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis Cash-Flow Statement Format Financing Section Payments for debt and dividends, the change in all long-term liabilities, the change in short-term bank debt, and any new stock issues Cash Section The change in cash and marketable securities

116

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis Cash-Flow Statement Format where: Ai = the dollar value of the ith type of asset (A) Lj = the dollar value of the jth type of liability (L) NW = the dollar value of net worth

Lj = the dollar value of the jth type of liability (L) NW = the dollar value of net worth.")

117

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis Cash-Flow Statement Format Cash Flow From Operations is defined as: where: ΔA1 = ΔCash

118

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis Cash-Flow Statement Format

119

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis Cash-Flow Statement Format Sources of Cash Increase in any liability Decrease in a non-cash asset New issue of stock Additions to surplus Revenues

120

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis Cash-Flow Statement Format Uses of Cash Decrease in any liability Increase in a non-cash asset Repayments/Buy back stock Deductions from surplus Cash Expenses Taxes Cash Dividends

121

Evaluating Credit Requests: A Four-Part Process

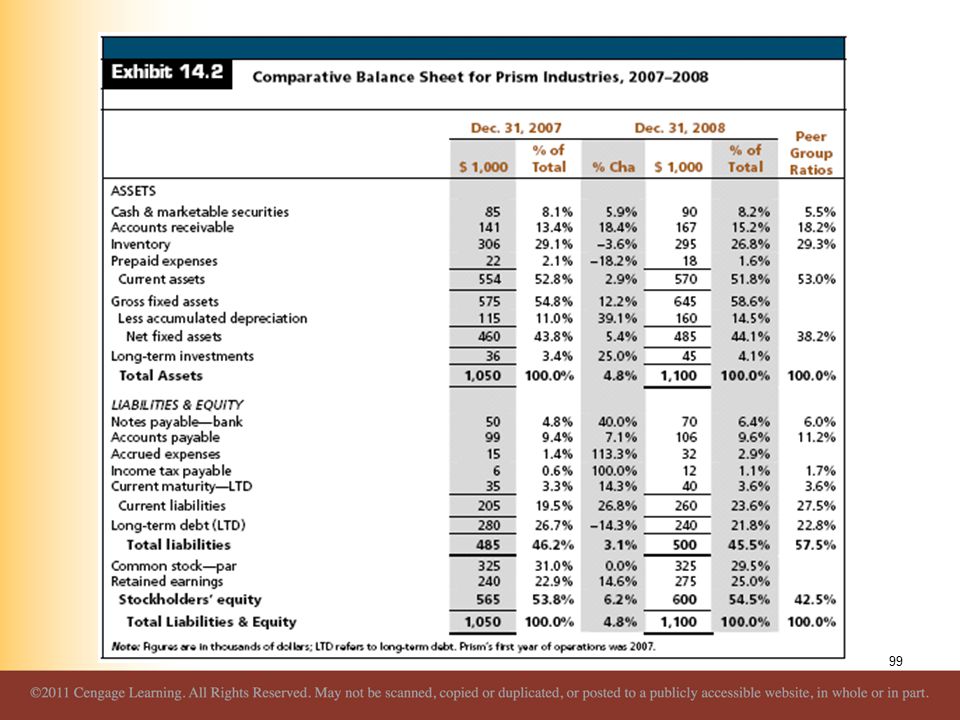

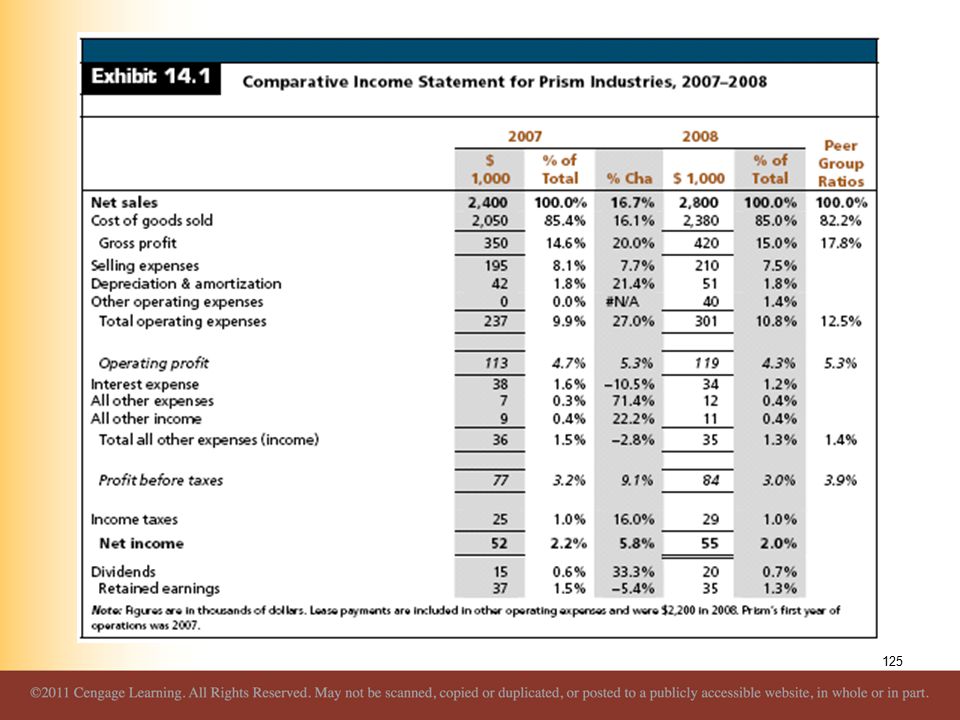

Cash-Flow Analysis For Prism Industries Cash Flow From Operations Recall Exhibits 14.1, 14.2, & 14.3 Cash Purchases for 2008: Cash Purchases = -(COGS + ΔInventory – ΔAccounts Payable)

")

122

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis For Prism Industries Cash Flow From Investing Activities ΔNet Fixed Assets = ΔGross Fixed Assets – ΔAccumulated Depreciation Or ΔNet Fixed Assets = Capital Expenditures – Depreciation where: Capital Expenditures = ΔNet Fixed Assets + Depreciation

123

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis For Prism Industries Cash Flow From Financing Activities Although cash-flow statements group payments for financing below the investment section, this is somewhat misleading because payments for financing generally take precedence over capital expenditures and increases in long-term investments

124

Evaluating Credit Requests: A Four-Part Process

Cash-Flow Analysis For Prism Industries Change in Cash Equals cash flow from operations adjusted for discretionary expenditures, cash used for investments, payments for financing, and external financing

129

Evaluating Credit Requests: A Four-Part Process

Financial Projections Pro Forma projections of the borrower’s condition reveal: How much financing is required When the loan will be repaid Use of the loan

130

Evaluating Credit Requests: A Four-Part Process

Financial Projections Pro Forma Assumptions Salest+1 = Salest × (1 + gSales) where: gSales = Projected Sales Growth COGSt+1 = Salest+1 × COGS % of Sales Accounts Receivablet+1 = Days A/R Outstanding × Average Daily Salest+1 Inventoryt+1 = COGSt+1/Inventory Turnover

where: gSales = Projected Sales Growth. COGSt+1 = Salest+1 × COGS % of Sales. Accounts Receivablet+1 = Days A/R Outstanding × Average Daily Salest+1. Inventoryt+1 = COGSt+1/Inventory Turnover.")

131

Evaluating Credit Requests: A Four-Part Process

Financial Projections Pro Forma Assumptions Accounts Payablet+1 = Days A/P Outstanding × Average Daily Purchasest+1 Or Accounts Payablet+1 = Days A/P Outstanding × [(COGSt+1 + ΔInventoryt+1)/365]

/365]")

132

Evaluating Credit Requests: A Four-Part Process

Financial Projections Projecting Notes Payable to Banks Rarely will the balance sheet “balance” in the initial round of pro forma forecasts To reconcile this, there must be a balancing item or “plug” figure

133

Evaluating Credit Requests: A Four-Part Process

Financial Projections Projecting Notes Payable to Banks When projected assets exceed projected liabilities plus equity, additional debt (assumed to be in the form of notes payable) is required When projected assets are less than projected liabilities plus equity, no new debt is required and existing debt could be reduced or excess funds invested in marketable securities

is required. When projected assets are less than projected liabilities plus equity, no new debt is required and existing debt could be reduced or excess funds invested in marketable securities.")

134

Evaluating Credit Requests: A Four-Part Process

Financial Projections Sensitivity Analysis Best Case Scenario Assumes optimistic improvements in planned performance and the economy are realized Worst Case Scenario Assumes the environment with the greatest potential negative impact on sales, earnings, and the balance sheet Most Likely Scenario Assumes the most reasonable sequence of economic events and performance trends

135

Evaluating Credit Requests: A Four-Part Process

Risk-Classification Scheme After evaluating the borrower’s risk profile along all dimensions, a loan is placed in a rating category ranked according to the degree of risk

137

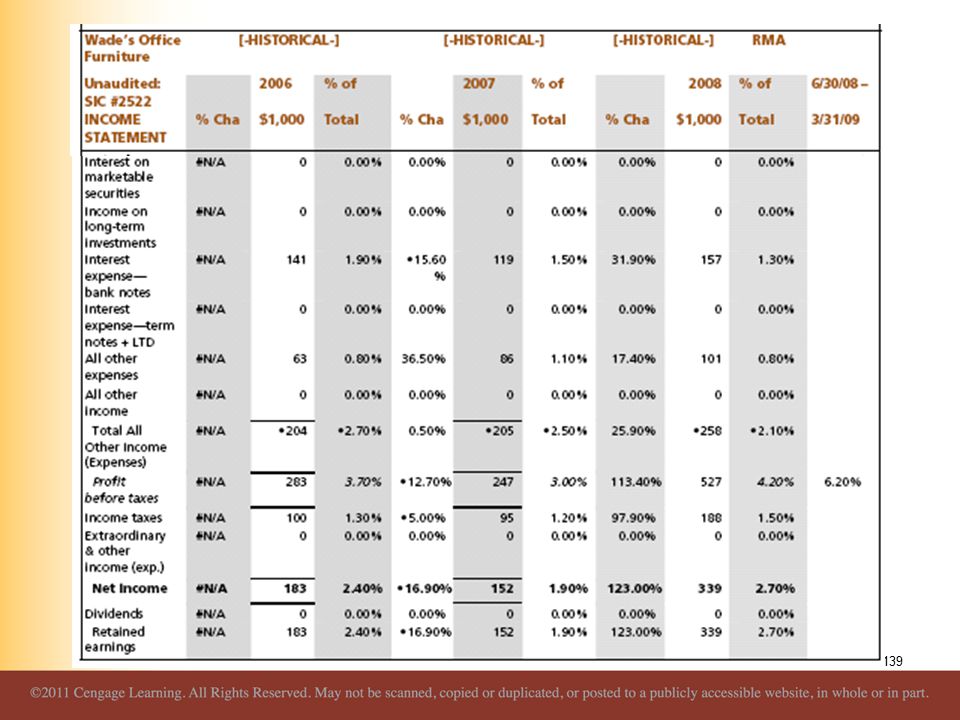

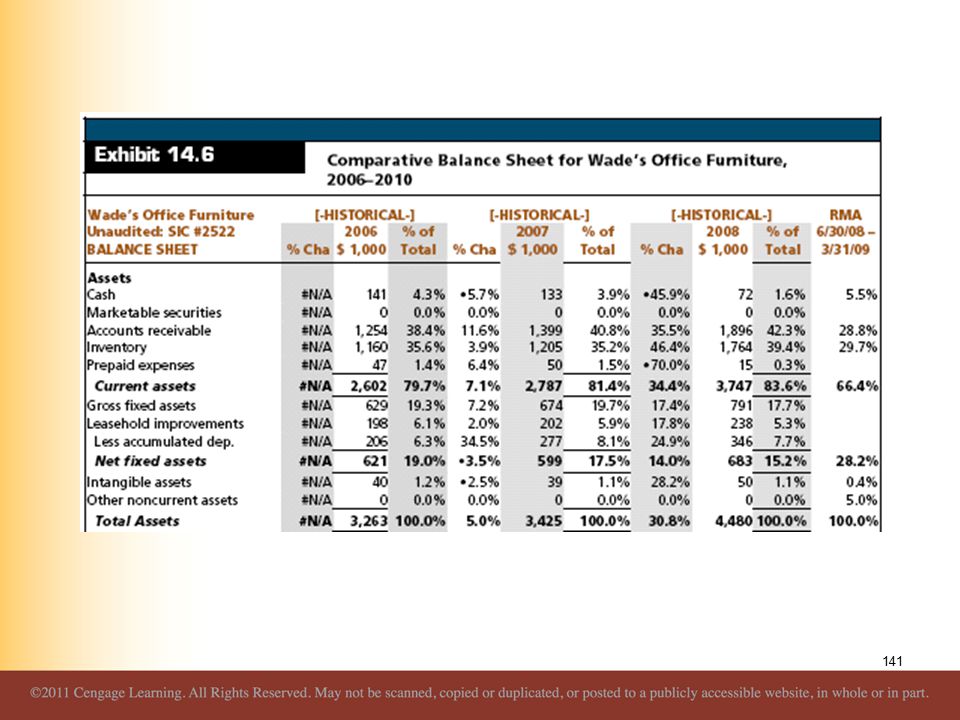

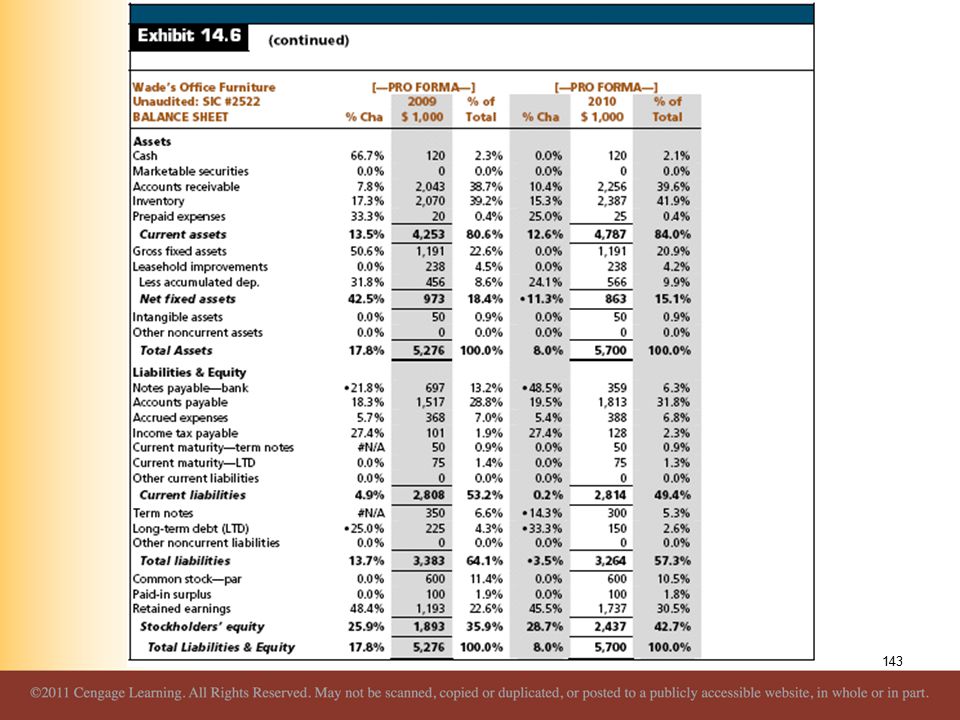

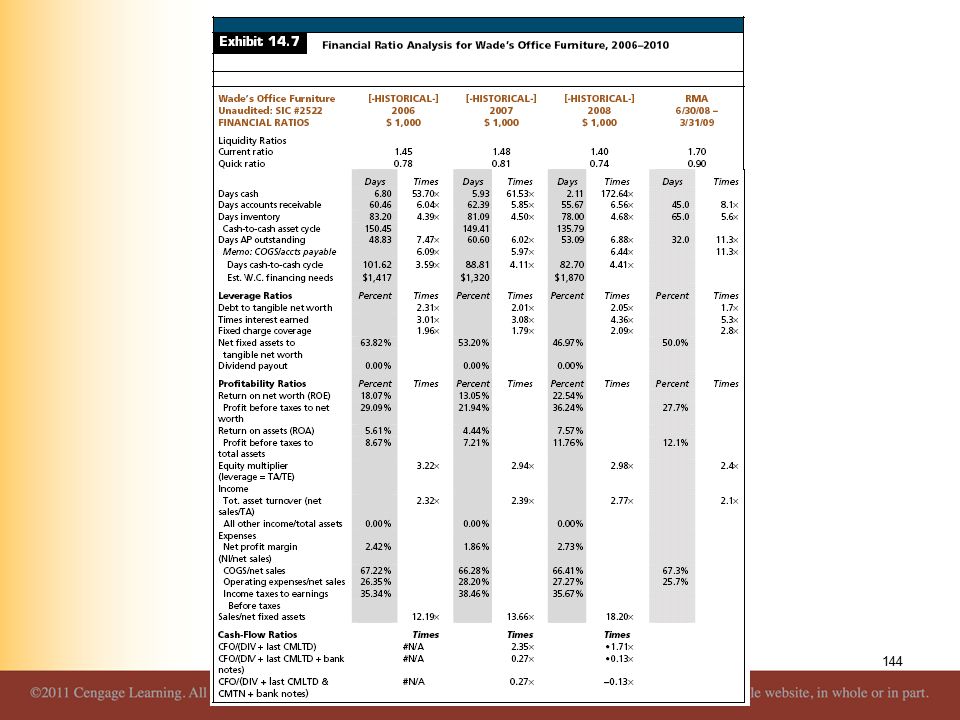

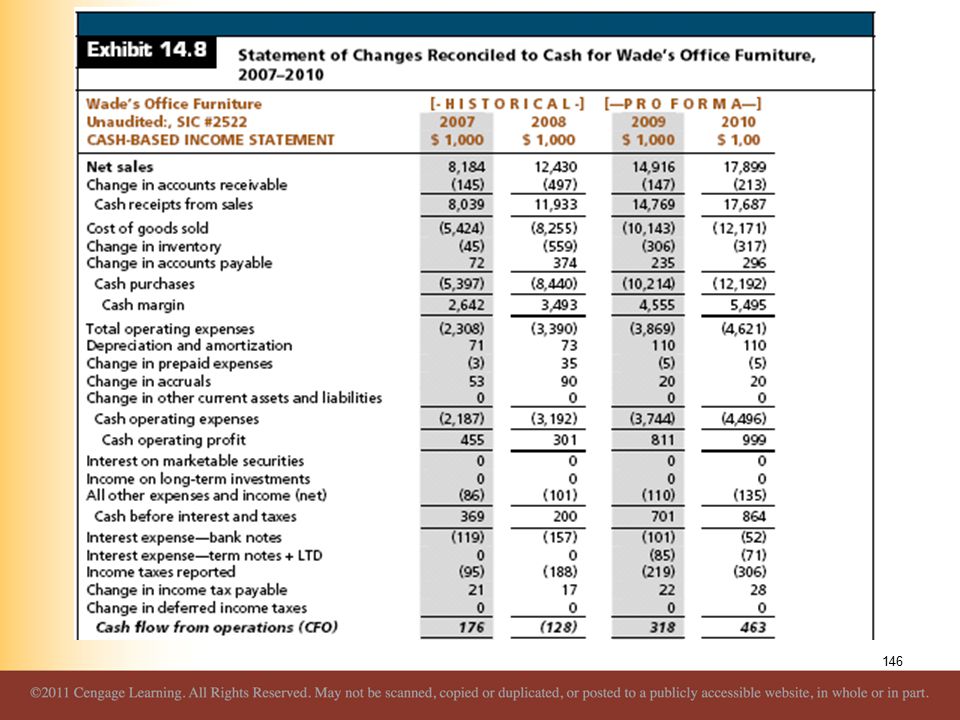

Credit Analysis Application: Wade’s Office Furniture

See Exhibits

151

Managing Risk with Loan Sales and Credit Derivatives

Many financial institutions have changed their business models, switching to the originate-to-distribute (OTD) model Under the OTD model, firms make loans and thereby collect fees, then either sell parts of the loan through participations or package the loans into pools and sell them in the marketplace

model. Under the OTD model, firms make loans and thereby collect fees, then either sell parts of the loan through participations or package the loans into pools and sell them in the marketplace.")

152

Managing Risk with Loan Sales and Credit Derivatives

Larger institutions also form loan syndicates in which one firm serves as a principal in negotiating terms with a borrower who has significant credit needs, but then engages other firms to take part of the credit and thus share the risk Lead Bank The institution that actually underwrites the original loan and sells the participation

153

Managing Risk with Loan Sales and Credit Derivatives

There are several inherent risk in loan participations or loan sales General credit risks There is an inherent potential conflict between the originating institution and the investor The loan originator might see the up-front fees and premium to the loan value as an excellent source of revenue that might not be as attractive if these loans were subsequently held in portfolio

154

Managing Risk with Loan Sales and Credit Derivatives

Underwriting Loan Sales, Participations, and Syndications The lead lending institution and the participating investor are required to underwrite the loans as if they were making the loans themselves and placing them on their own books

155

Managing Risk with Loan Sales and Credit Derivatives

Shared National Credits (SNC) Loan or loan commitment of $20 million or more made generally by three or more unaffiliated supervised institutions under a formal lending agreement The various regulatory agencies established the SNC program in 1977 to monitor and review the risk structure of large syndicated loans

Loan or loan commitment of $20 million or more made generally by three or more unaffiliated supervised institutions under a formal lending agreement. The various regulatory agencies established the SNC program in 1977 to monitor and review the risk structure of large syndicated loans.")

156

Managing Risk with Loan Sales and Credit Derivatives

Shared National Credits (SNC)

")

157

Managing Risk with Loan Sales and Credit Derivatives

Credit Enhancements Can take many forms Key terms of credit enhancements potentially include: Excess cash flow Many securitized assets are placed in pools in which the required payments to investors are less than the contractual payments of borrowers Thus, even if some borrowers do not make the required payments, there is sufficient cash flow to continue to pay investors

158

Managing Risk with Loan Sales and Credit Derivatives

Credit Enhancements Key terms of credit enhancements potentially include: Reserve accounts The originating institution creates a trust for losses up to an amount allocated for a reserve which is used to make up any deficits in payments by borrowers Collateralization One or more parties pledge collateral against the loan

159

Managing Risk with Loan Sales and Credit Derivatives

Credit Enhancements Key terms of credit enhancements potentially include: Loan guarantees One or more parties pledge personal or business assets or are contractually bound to meet the obligations of the borrower if that party defaults Credit insurance Any party can purchase credit insurance, provided either privately or by a governmental unit, for loans that provide payments for losses stemming from default

160

Managing Risk with Loan Sales and Credit Derivatives

Credit Enhancements Key terms of credit enhancements potentially include: Credit derivatives Instruments or contracts that derive their value from the underlying credit risk of a loan or bond

161

Managing Risk with Loan Sales and Credit Derivatives

Credit Default Swaps (CDS) CDS contracts are relatively unregulated derivative instruments based on the underlying payments and values of fixed-income securities These contracts are privately negotiated instruments between a buyer and a seller and are traded in over-the-counter markets

CDS contracts are relatively unregulated derivative instruments based on the underlying payments and values of fixed-income securities. These contracts are privately negotiated instruments between a buyer and a seller and are traded in over-the-counter markets.")

162

Managing Risk with Loan Sales and Credit Derivatives

Credit Default Swaps (CDS) The buyer pays a premium and thus the CDS is similar to an insurance contract The buyer often owns the underlying debt and uses the CDS as a hedge The seller of the CDS plays a role similar to that of the insurance company Sellers generally do not own the debt and provide longer-term protection If an adverse event occurs the seller pays the buyer the change in value of the underlying asset

The buyer pays a premium and thus the CDS is similar to an insurance contract. The buyer often owns the underlying debt and uses the CDS as a hedge. The seller of the CDS plays a role similar to that of the insurance company. Sellers generally do not own the debt and provide longer-term protection. If an adverse event occurs the seller pays the buyer the change in value of the underlying asset.")

163

Managing Risk with Loan Sales and Credit Derivatives

Credit Default Swaps (CDS)

")

164

Managing Risk with Loan Sales and Credit Derivatives

Credit Default Swaps (CDS) There are several credit events that potentially trigger a payment from the seller of a CDS to the buyer: Failure to pay principal and interest payments in a timely manner Restructuring of the debt in such a way that the lender (investor in the debt) is negatively affected Bankruptcy or insolvency in which the debt is not paid Acceleration of the principal and interest payments prior to the scheduled date(s) Repudiation or moratorium in which the debt issuer rejects or refuses to pay the debt

There are several credit events that potentially trigger a payment from the seller of a CDS to the buyer: Failure to pay principal and interest payments in a timely manner. Restructuring of the debt in such a way that the lender (investor in the debt) is negatively affected. Bankruptcy or insolvency in which the debt is not paid. Acceleration of the principal and interest payments prior to the scheduled date(s) Repudiation or moratorium in which the debt issuer rejects or refuses to pay the debt.")

165

Managing Risk with Loan Sales and Credit Derivatives

Credit Default Swaps (CDS) The credit crisis of 2007–2008 caused many sellers of credit default swaps to make large and unexpected payments for default

The credit crisis of 2007–2008 caused many sellers of credit default swaps to make large and unexpected payments for default.")

166

Evaluating Consumer Loans

15

167

Evaluating Consumer Loans

Today, many banks target individuals as the primary source of growth in attracting new business Consumer loans differ from commercial loans Quality of financial data is lower Primary source of repayment is current income

170

Types of Consumer Loans

Evaluating Consumer Loans An analyst should addresses the same issues discussed with commercial loans: The use of loan proceeds The amount needed The primary and secondary source of repayment

171

Types of Consumer Loans

Evaluating Consumer Loans Consumer loans differ so much in design that no comprehensive analytical format applies to all loans

172

Types of Consumer Loans

Installment Loans Require the periodic payment of principal and interest

173

Types of Consumer Loans

Installment Loans Direct Negotiated between the bank and the ultimate user of the funds Indirect Funded by a bank through a separate retailer that sells merchandise to a customer

174

Types of Consumer Loans

Installment Loans Revenues and Costs from Installment Loans Consumer installment loans can be extremely profitable Costs $100 - $250 to originate loan Typically yield over 5% (loan income minus loan acquisition costs, collections costs and net charge-offs)

")

175

Types of Consumer Loans

Credit Cards and Other Revolving Credit Credit cards and overlines tied to checking accounts are the two most popular forms of revolving credit agreements In 2007, over 92% of households had credit cards (average of 13 cards)

")

176

Types of Consumer Loans

Credit Cards and Other Revolving Credit Most banks operate as franchises of MasterCard and/or Visa Bank pays a one-time membership fee plus an annual charge determined by the number of its customers actively using the cards

177

Types of Consumer Loans

Debit Cards, Smart Cards, and Prepaid Cards Debit Cards Widely available When an individual uses the card, their balance is immediately debited Banks prefer debit card use over checks because debit cards have lower processing costs

178

Types of Consumer Loans

Debit Cards, Smart Cards, and Prepaid Cards Smart Card Contains a memory chip which can store information and value Programmable such that users can store information and add or transfer value to another smart card Only modest usage in the U.S.

179

Types of Consumer Loans

Debit Cards, Smart Cards, and Prepaid Cards Prepaid Card A hybrid of a debit card Customers prepay for services to be rendered and receive a card against which purchases are charged Use of phone cards, prepaid cellular, toll tags, subway, etc. are growing rapidly

180

Types of Consumer Loans

Credit Card Systems and Profitability Card issuers earn income from three sources: Cardholders’ annual fees Interest on outstanding loan balances Discounting the charges that merchants accept on purchases

181

Types of Consumer Loans

Credit Card Systems and Profitability Despite high charge-offs, credit cards are attractive because they provide higher risk-adjusted returns than do other types of loans

184

Types of Consumer Loans

Overdraft Protection and Open Credit Lines Overdraft Protection Against Checking Accounts A type of revolving credit A bank authorizes qualifying individuals to write checks in excess of actual balances held in a checking account up to a pre-specified limit

185

Types of Consumer Loans

Overdraft Protection and Open Credit Lines Open Credit Lines The bank provides customers with special checks that activate a loan when presented for payment

186

Types of Consumer Loans

Home Equity Loans Grew from virtually nothing in the mid-1980s to over $350 billion in 2008 They meet the tax deductibility requirements of the Tax Reform Act of 1986, which limits deductions for consumer loan interest paid by individuals, because they are secured by equity in an individual's home

187

Types of Consumer Loans

Home Equity Loans Some allow access to credit line by using a credit card Borrowers pay interest only on the amount borrowed, pay 1 to 2 percent of the outstanding principal each month, and can repay the remaining principal at their discretion

188

Types of Consumer Loans

Non-Installment Loans aka Bridge Loan Requires a single principal and interest payment Typically, the individual’s borrowing needs are temporary and repayment is from a well-defined future cash inflow

189

Subprime Loans One of the hottest growth areas during the early 2000s

Subprime loans are higher-risk loans labeled “B,” “C,” and “D” credits They have been especially popular in auto, home equity, and mortgage lending Typically have the same risk as loans originated through consumer finance companies

190

Subprime Loans Many subprime lenders make loans to individuals that a bank would not traditionally make and keep on-balance sheet Subprime lenders charge higher rates and have more restrictive covenants

191

Subprime Loans What Happens When Housing Prices Fall

Subprime loans can be attractive when housing values are rising Individuals who are overextended and cannot make their monthly payments, can often sell the home or refinance and withdraw equity to pay the debts if the price increases are sufficiently high The opposite occurs when housing prices fall

192

Subprime Loans What Happens When Housing Prices Fall

During 2007–2008, banks were forced to charge-off historically high amounts of mortgage loans as delinquencies and foreclosures skyrocketed

195

Consumer Credit Regulations

Equal Credit Opportunity Makes it illegal for lenders to discriminate on the basis of race, religion, sex, marital status, age, or national origin

196

Consumer Credit Regulations

Prohibited Information Requests The applicant's marital status Whether alimony, child support, and public assistance are included in reported income A woman's childbearing capability and plans Whether an applicant has a telephone

197

Consumer Credit Regulations

Credit Scoring Systems Acceptable if they do not require prohibited information and are statistically justified Can use information about age, sex, and marital status as long as these factors contribute positively to the applicant's creditworthiness

198

Consumer Credit Regulations

Credit Reporting Lenders must report credit extended jointly to married couples in both spouses' names Whenever lenders reject a loan, they must notify applicants of the credit denial within 30 days and indicate why the request was turned down

199

Consumer Credit Regulations

Truth In Lending Regulations apply to all individual loans up to $25,000 where the borrower's primary residence does not serve as collateral

200

Consumer Credit Regulations

Truth In Lending Requires that lenders disclose to potential borrowers both the total finance charge and an annual percentage rate (APR) Historically, consumer loan rates were quoted as: Add-On Rates Discount Rates Simple Interest Rates

Historically, consumer loan rates were quoted as: Add-On Rates. Discount Rates. Simple Interest Rates.")

202

Consumer Credit Regulations

Fair Credit Reporting Fair Credit Reporting Act Enables individuals to examine their credit reports provided by credit bureaus If any information is incorrect, the individual can have the bureau make changes and notify all lenders who obtained the inaccurate data

203

Consumer Credit Regulations

Fair Credit Reporting There are three primary credit reporting agencies: Equifax Experian Trans Union Unfortunately, the credit reports that they produce are quite often wrong

204

Consumer Credit Regulations

Fair Credit Reporting Credit Score Like a bond rating for individuals Based on several factors Payment History Amounts Owed Length of Credit History Types of Credit New Credit

207

Consumer Credit Regulations

Community Reinvestment Act CRA prohibits redlining and encourages lenders to extend credit within their immediate trade area and the markets where they collect deposits

208

Consumer Credit Regulations

Community Reinvestment Act Financial Institutions Reform, Recover, and Enforcement Act of 1989 raised the profile of the CRA by mandating public disclosure of bank lending policies and regulatory ratings of bank compliance

209

Consumer Credit Regulations

Community Reinvestment Act Regulators must also take CRA compliance into account when evaluating a bank's request to charter a new bank, acquire a bank, open a branch, or merge with another institution

210

Consumer Credit Regulations

Bankruptcy Reform Individuals who cannot repay their debts on time can file for bankruptcy and receive court protection against creditors

211

Consumer Credit Regulations

Bankruptcy Reform Individuals can file for bankruptcy under: Chapter 7 Individuals liquidate qualified assets and distribute the proceeds to creditors Chapter 13 An individual works out a repayment plan with court supervision

212

Consumer Credit Regulations

Bankruptcy Reform In 2005, Congress passed bankruptcy reform legislation that made it more difficult for individuals to completely avoid repaying their debts In particular, an individual whose income exceeds the state median has to file for Chapter 13 and will repay at least a portion of his or her debts

213

Credit Analysis Objective of consumer credit analysis is to assess the risks associated with lending to individuals

214

Credit Analysis When evaluating loans, bankers cite the Cs of credit:

Character Capital Capacity Conditions Collateral

215

Credit Analysis Two additional Cs Customer Relationship Competition

A bank’s prior relationship with a customer reveals information about past credit experience Competition Lenders periodically react to competitive pressures Competition should not affect the accept/reject decision

216

Credit Analysis Policy Guidelines Acceptable Loans Automobile Boat

Home Improvement Personal-Unsecured Single Payment Cosigned

217

Credit Analysis Policy Guidelines Unacceptable Loans

Loans for speculative purposes Loans secured by a second lien Other than home improvement or home equity loans Any participation with a correspondent bank in a loan that the bank would not normally approve

218

Credit Analysis Policy Guidelines Unacceptable Loans

Loans to a poor credit risk based on the strength of the cosigner Single payment automobile or boat loans Loans secured by existing home furnishings Loans for skydiving equipment and hang gliders

219

Credit Analysis Evaluation Procedures: Judgmental and Credit Scoring

Subjectively interpret the information in light of the bank’s lending guidelines and accepts or rejects the loan Assessment can be completed shortly after receiving the loan application and visiting with the applicant

220

Credit Analysis Evaluation Procedures: Judgmental and Credit Scoring

Grades the loan request according to a statistically sound model that assigns points to selected characteristics of the prospective borrower

221

Credit Analysis Evaluation Procedures: Judgmental and Credit Scoring

If the total points exceeds the accept threshold, the officer approves the loan If the total is below the reject threshold, the officer denies the loan

222

Credit Analysis Evaluation Procedures: Judgmental and Credit Scoring

In both cases, judgmental and quantitative, a lending officer collects information regarding the borrower’s character, capacity, and collateral

223

Credit Analysis An Application: Credit Scoring a Consumer Loan

You receive an application for a customer to purchase a 2007 Jeep Cherokee Do you make the loan?

224

Credit Analysis An Application: Credit Scoring a Consumer Loan

The Credit Score At this bank, the loan is automatically approved if the total score equals at least 200 The loan is automatically denied if the total score is below 150 Accept/Reject is indeterminate for scores between 150 & 200

226

Credit Analysis An Application: Credit Scoring a Consumer Loan

The Credit Decision The credit decision rests on the loan officer’s evaluation of the applicant’s character and capacity to repay the debt

227

Credit Analysis An Application: Credit Scoring a Consumer Loan

The Credit Decision The loan officer has numerous grounds for denying credit Limited credit history Local residence was established too recently Employed too recently

228

Credit Analysis An Application: Credit Scoring a Consumer Loan

The Credit Decision The loan officer sees some positive things Applicant appears to be a hard worker who is the victim of circumstances resulting from her husband’s death It is unlikely that anyone who puts almost 30 percent down on a new model is going to walk away from a debt

229

Credit Analysis An Application: Credit Scoring a Consumer Loan

The Credit Decision The loan officer sees some positive things The bank will likely lose Groome as a depositor if it denies the application What would you recommend?

230

Credit Analysis Your FICO Credit Score

Summarizes in one number an individual’s credit history Lenders often use this number when evaluating whether to approve a consumer loan or mortgage Many insurance companies consider the score when determining whether to offer insurance coverage and how to price the insurance

231

Credit Analysis Your FICO Credit Score

Summarizes in one number an individual’s credit history The scores range from 300 to 850 with a higher figure indicating a better credit history The national average is 670 The higher the score is, the more likely it is a lender will see the individual as making the promised payments in a timely manner

232

Credit Analysis Your FICO Credit Score

An individual’s credit score is based on five broad factors: Payment history 35% Amounts owed 30% Length of credit history 15% New credit 10% Type of credit in use 10%

234

Credit Analysis An Application: Indirect Lending

A retailer sells merchandise and takes the credit application Because many firms do not have the resources to carry their receivables, they sell the loans to banks or other financial institutions

235

Credit Analysis An Application: Indirect Lending

These loans are collectively referred to as dealer paper Banks aggressively compete for paper originated by well-established automobile, mobile home, and furniture dealers

236

Credit Analysis An Application: Indirect Lending

Dealers negotiate finance charges directly with their customers A bank, in turn, agrees to purchase the paper at predetermined rates that vary with the default risk assumed by the bank, the quality of the assets sold, and the maturity of the consumer loan

237

Credit Analysis An Application: Indirect Lending

A dealer normally negotiates a higher rate with the car buyer than the determined rate charged by the bank This differential varies with competitive conditions but potentially represents a significant source of dealer profit

238

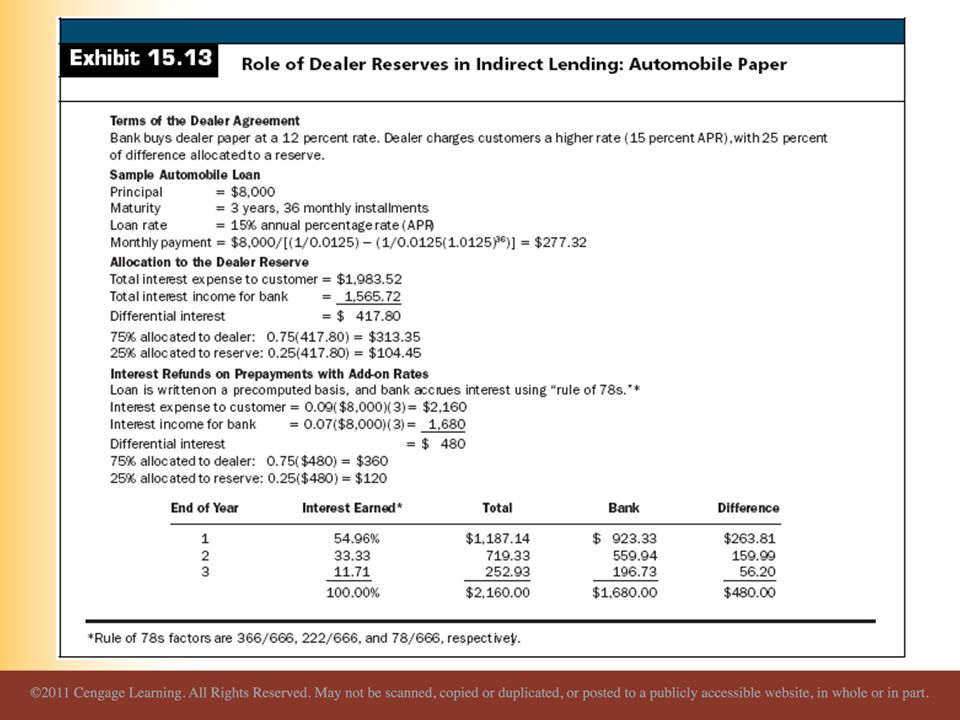

Credit Analysis An Application: Indirect Lending

Most indirect loan arrangements provide for dealer reserves that reduce the risk in indirect lending The reserves are derived from the differential between the normal, or contract loan rate and the bank rate, and help protect the bank against customer defaults and refunds

240

Recent Risk and Return Characteristics of Consumer Loans

Revenues from Consumer Loans The attraction is two-fold: Competition for commercial customers narrowed commercial loan yields so that returns fell relative to potential risks Developing loan and deposit relationships with individuals presumably represents a strategic response to deregulation

241

Recent Risk and Return Characteristics of Consumer Loans

Revenues from Consumer Loans Consumer loan rates have been among the highest rates quoted at banks in recent years In addition to interest income, banks generate substantial non-interest revenues from consumer loans

242

Recent Risk and Return Characteristics of Consumer Loans

Revenues from Consumer Loans With traditional installment credit, banks often encourage borrowers to purchase credit life insurance on which the bank may earn a premium

243

Recent Risk and Return Characteristics of Consumer Loans

Consumer Loan Losses Losses on consumer loans are normally the highest among all categories of bank credit Losses are anticipated because of mass marketing efforts pursued by many lenders, particularly with credit cards Credit card losses and fraud amounted to more than $12 billion in 2005

244

Recent Risk and Return Characteristics of Consumer Loans

Interest Rate and Liquidity Risk with Consumer Credit The majority of consumer loans are priced at fixed rates New auto loans typically carry 4-year maturities, and credit card loans exhibit an average 15- to 18-month maturity

245

Recent Risk and Return Characteristics of Consumer Loans

Interest Rate and Liquidity Risk with Consumer Credit Bankers have responded in two ways to deal with the interest rate risk: Price more consumer loans on a floating-rate basis Commercial and investment banks have created a secondary market in consumer loans, allowing loan originators to sell a package of loans

246

Evaluating Consumer Loans

Similar presentations