Download presentation

Presentation is loading. Please wait.

1

The Future of New Venture Finance: Transformation from Art to Science Richard Smith May 2002 Peter F. Drucker Graduate School of Management Claremont Graduate University Venture Finance Institute http://www.cgu.edu/drucker/vfi/

2

New Venture Opportunity Cost of Capital and Financial Contracting Frank Kerins Washington State University Janet Kiholm Smith Claremont McKenna College Richard Smith Claremont Graduate University

3

“Good ideas and good products are a dime a dozen. Good execution and good management - in a word, good people - are rare.” --Arthur Rock

5

©2000, Entrepreneurial Finance, Smith and Kiholm Smith Chapter 14 Organizational Structure of Venture Capital Investment Portfolio Companies –Value creation – Generate deal flow – Screen opportunities – Harvest investments – Negotiate deals – Monitor and advise General Partners Venture Capital Fund – Pension plan – Endowments – Life insurance companies – Corporations – Individuals Limited Partners Effort and 1% of capital Annual Management Fee 2-3% Carried Interest 20- 30% of Gain 99% of Investment Capital Capital Appreciation 70-80% of Gain Investment Capital and Effort Financial Claims

10

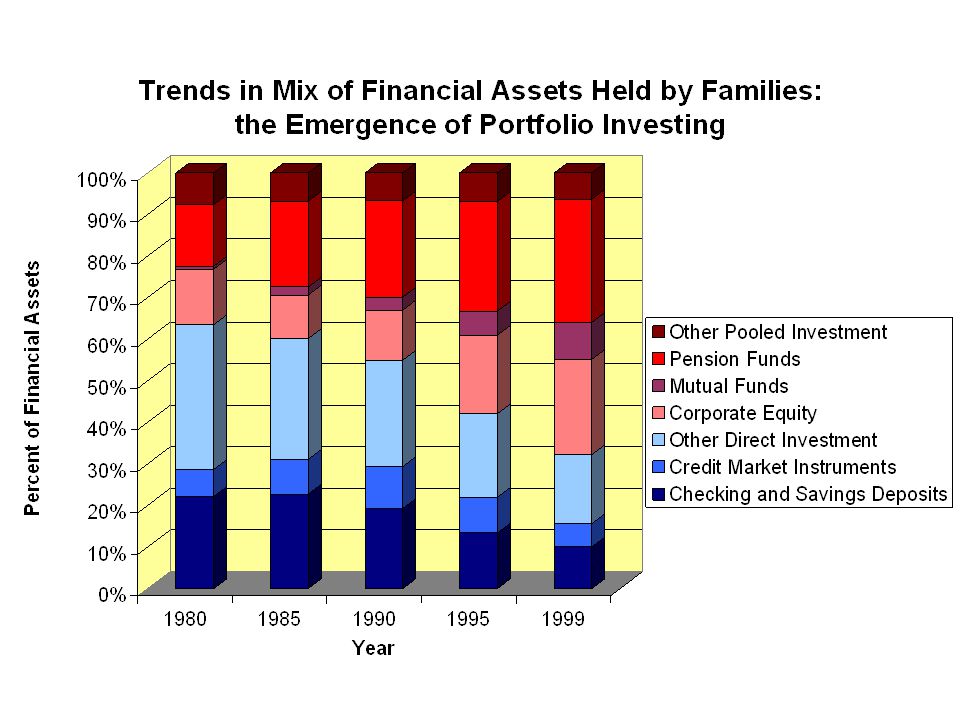

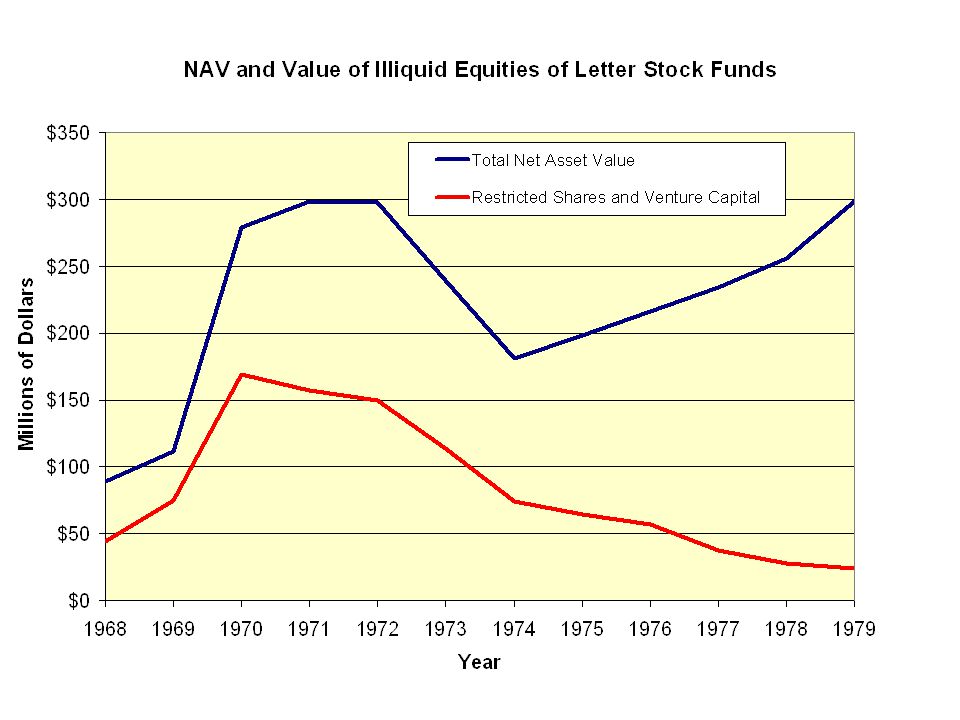

Implications of VC History Capital starvation before 1979 due to ICA/SEC regulation.

11

Implications of VC History Capital starvation before 1979 due to ICA/SEC regulation. Expected returns higher than needed after 1979.

12

Implications of VC History Capital starvation before 1979 due to ICA/SEC regulation. Expected returns higher than needed after 1979. Rapid growth in demand from institutional investors.

13

Implications of VC History Capital starvation before 1979 due to ICA/SEC regulation. Expected returns higher than needed after 1979. Rapid growth in demand from institutional investors. Inability of established VCs to respond.

14

Implications of VC History Capital starvation before 1979 due to ICA/SEC regulation. Expected returns higher than needed after 1979. Rapid growth in demand from institutional investors. Inability of established VCs to respond. Compounding effects of the Internet boom.

15

April 2000 to Today

17

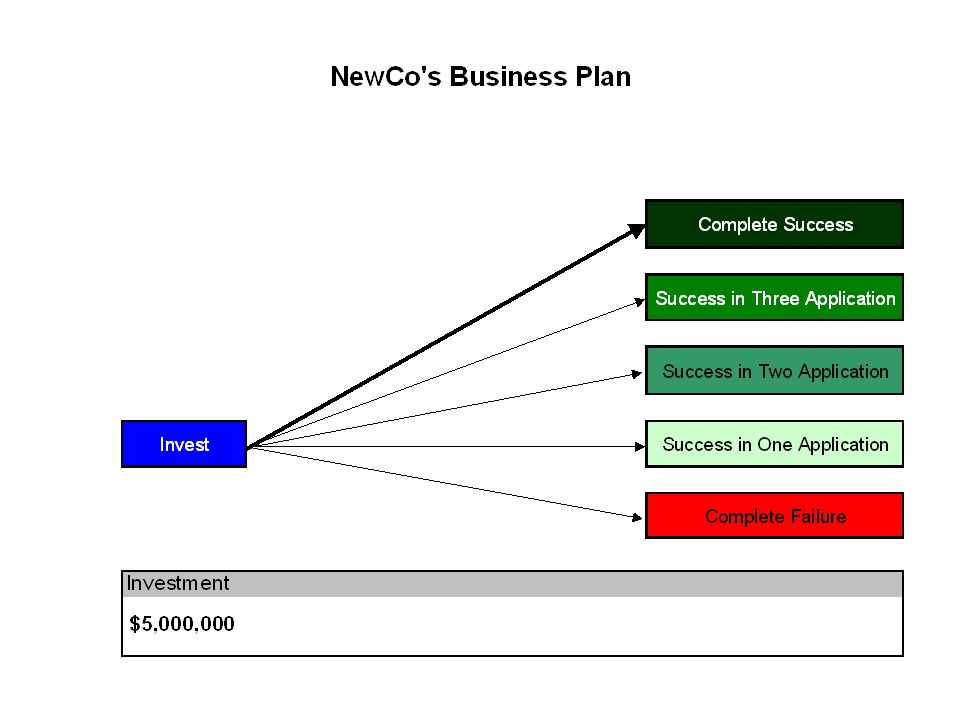

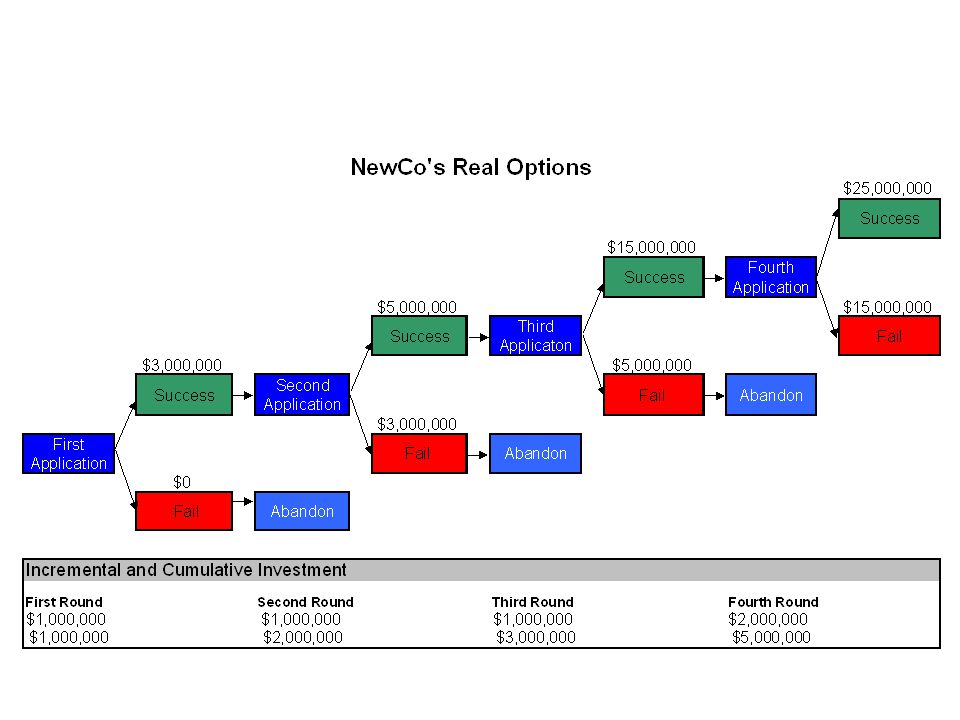

Four principles of value-maximizing deal structure

18

Limit risk and enhance expected return by structuring financing around objective milestones that are related to risk.

19

Four principles of value-maximizing deal structure Limit risk and enhance expected return by structuring financing around objective milestones that are related to risk. If the entrepreneur and the investor have similar expectations, allocate most of the risk to the investor.

20

Four principles of value-maximizing deal structure Limit risk and enhance expected return by structuring financing around objective milestones that are related to risk. If the entrepreneur and the investor have similar expectations, allocate most of the risk to the investor. Shift risk to the better informed or more optimistic party.

21

Four principles of value-maximizing deal structure Limit risk and enhance expected return by structuring financing around objective milestones that are related to risk. If the entrepreneur and the investor have similar expectations, allocate most of the risk to the investor. Shift risk to the better informed or more optimistic party. Use risk allocation to align the interests and incentives of the parties

25

Valuing the Real Options Model the venture cash flows based on the agreed deal structure. Use risky discount rates to value the real options. Work back recursively through the decision tree to determine current value and required ownership. Use the model to evaluate alternative structures for the purpose of aligning interests and maximizing value.

26

Valuation: Corporate Setting Discount expected cash flows at a rate determined by market opportunity cost (CAPM) Infer discount rate from betas of comparable market assets Implicit assumptions: – Same standard deviation of holding period returns – Same correlation with market – (Ultimate) Investor is (can be) well-diversified

Infer discount rate from betas of comparable market assets Implicit assumptions: – Same standard deviation of holding period returns – Same correlation with market – (Ultimate) Investor is (can be) well-diversified")

27

Problems of New Venture Valuation VCs represent well-diversified investors, entrepreneurs cannot be well-diversified. The entrepreneur’s required rate of return depends on total risk and achievable diversification. Little data is available on risk attributes of comparable investments. Equilibrium holding period returns and standard deviations are endogenous.

28

Ability to Diversify and Opportunity Cost of Capital Well-diversified investor Undiversified entrepreneur

29

Estimation of Undiversified Entrepreneur’s Opportunity Cost of Capital Direct use of market transactions not possible. CEQ avoids endogeneity problem – Estimating from market returns data (per unit of value to diversified investor).

..")

30

Estimation of Undiversified Entrepreneur’s Opportunity Cost of Capital Expected cash flow (capital market equilibrium). Entrepreneur’s opportunity cost of capital

31

Estimation of Undiversified Entrepreneur’s Opportunity Cost of Capital CEQ of Underdiversified entrepreneur – Underdiversified investment – Estimating from market returns data

32

Data US IPOs from 1995 through 2000 Measurement

33

Descriptive Evidence Parameter Estimates: Mean – Standard deviation of returns (annualized) 120% – Ratio of firm standard deviation to S&P 500 4.88 – Correlation with S&P 500 0.20 – Equity beta with S&P 500 0.99 Aggregations: – Calendar year – Industry – Age (years after IPO) – Financial Condition (revenue and income status) – Size (Employees)

120% – Ratio of firm standard deviation to S&P – Correlation with S&P – Equity beta with S&P Aggregations: – Calendar year – Industry – Age (years after IPO) – Financial Condition (revenue and income status) – Size (Employees)")

34

Descriptive Evidence Total risk (standard deviation of returns): – Decreases with firm age, size, and financial condition – Differs across industries and over calendar years Total risk to market risk: – Decreases with firm age, size, and financial condition Beta – Increases with firm age and size – High in year of IPO and transition to profitability Correlation – Increases with firm age, financial condition, and size

: – Decreases with firm age, size, and financial condition – Differs across industries and over calendar years Total risk to market risk: – Decreases with firm age, size, and financial condition Beta – Increases with firm age and size – High in year of IPO and transition to profitability Correlation – Increases with firm age, financial condition, and size")

35

Results

Similar presentations