Download presentation

Presentation is loading. Please wait.

1

The Mexican Crisis of (Tequila Crisis)

")

2

Background In early 1990’s Mexican economy seemed healthy

Recovery from the “lost decade” of 1980’s (1982 debt crisis and 1986 oil crisis) The NAFTA started in early 1994 culminating a series of reforms: Restructuring of foreign debt under the Brady Plan Sharp reductions in budget deficit and inflation rate Cuts in protectionist trade barriers Privatization of various government owned state companies Mexico became member of the OECD in May’ (“The Club of the Wealthy”)

The NAFTA started in early 1994 culminating a series of reforms: Restructuring of foreign debt under the Brady Plan. Sharp reductions in budget deficit and inflation rate. Cuts in protectionist trade barriers. Privatization of various government owned state companies. Mexico became member of the OECD in May’94 ( The Club of the Wealthy )")

3

The 1994 Economic Crisis in Mexico, widely known as the Mexican peso crisis, became an effective crisis with the sudden devaluation of the Mexican peso in December 1994. The impact of the Mexican economic crisis on the Southern Cone and Brazil was labeled the Tequila Effect (Spanish: Efecto Tequila).

.")

4

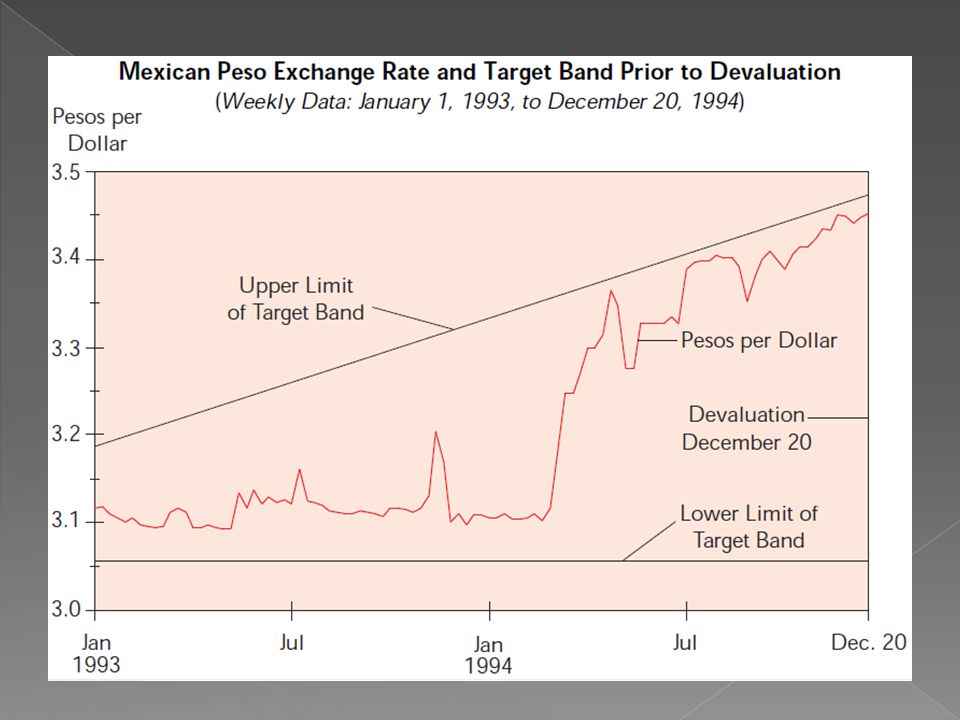

Mexico experienced recurring financial crises in 1976, 1982, 1986 and, with devastating economic and social consequences. The most recent crisis that emerged in December 1994 was the worst with the peso losing 40% of its value. Prior to the crisis, Mexico had a crawling peg exchange rate system. The peso-US dollar exchange rate was kept within a narrow target band, but the upper limit of the band was raised slightly every day by a predetermined amount, allowing for a gradual nominal depreciation of the peso.

5

Exchange rate over-valuation and the current account deficit were the two major problems in the Mexican economy in 1994. Given these problems, several additional factors helped to trigger the crisis: Elections, which are traditionally associated with devaluation, 2) The rise in U.S. interest rates, 3) Loss of investor confidence due to politically linked assassinations, 4) Loose monetary policy in response to the reduction in foreign capital flows, 5) Expansion of quasi-fiscal expenditure via development bank credits, and 6) Shifting fiscal borrowing to short-term, dollar-denominated instruments.

The rise in U.S. interest rates, 3) Loss of investor confidence due to politically linked assassinations, 4) Loose monetary policy in response to the reduction in foreign capital flows, 5) Expansion of quasi-fiscal expenditure via development bank credits, and. 6) Shifting fiscal borrowing to short-term, dollar-denominated instruments.")

6

The Mexican economic crisis was the result of policy mistakes that led to an investor panic. The assassination of presidential candidate Donaldo Colosio caused foreign investors to demand a higher return on investments to compensate for increased perceived risk. The Mexican central bank fought the increase in interest rates through an expansion of domestic credit. This credit was converted to dollars and led to a drain on Central Bank foreign exchange reserves. Meanwhile the exchange rate remained moderately over-valued. Moreover, the Mexican government rolled over its short-term peso-denominated debt into short-term dollar denominated debt in an attempt to decrease the cost of government borrowing.

7

“a speculative attack can topple an exchange rate peg even when economic fundamentals are sound, if investors display herding behavior and the country is financially vulnerable with large amounts of ST debt”

8

The result of Mexican economic policy in 1994 was to place the economy in a vulnerable position with respect to its external debt: the government held a large amount of short-term dollar donominated debt, reserves had dwindled, and expectations of a devaluation had developed. Once the first devaluation was announced on December 20, investors panicked and ran from the peso. The peso value of dollar-denominated government debt rose sharply, as did interest rates for new government debt. The result was a government liquidity crisis. This crisis in turn contaminated the private sector's credit-worthiness and created the threat of a collapse of the banking system.

9

Fixed Exchange Rate Mexico maintained a crawling peg exchange rate system Government intervention kept the exchange rate vis-à-vis the USD within a narrow target band, upper limit was raised slightly daily to up to ~2.3% p.a. In real terms the Peso was appreciating: Mexico inflation > US inflation + peso depreciation This encourage imports and discourage exports increasing the current account deficit, which rose from 2.8% of GDP in 1989 to +7% of GDP from The Mexican government seemed unconcerned due to increasing levels of international reserves (USD 30Bn in Feb’94) Current Account deficit rose from 2.8% in 1989 to an average of more than 7% of GDP from

Current Account deficit rose from 2.8% in 1989 to an average of more than 7% of GDP from")

10

The band floor was fixed at 3. 051 Mexican pesos per US dollar

The band floor was fixed at Mexican pesos per US dollar. The band ceiling had been allowed to increase pesos a day and any increase of the peso – US dollar exchange rate beyond this threshold would force the Mexican central bank to intervene and defend the parity. In December 1994, the Mexican government decided to devalue the peso by 15 percent, to about four pesos per dollar and within a few days the peso plummeted, sinking the country into a financial crisis which led to a 9.2% fall in real GNP per capita and a loss of 2 million jobs

12

Mexico’s Wild Year of 1994 Mexico’s Central Bank blamed a series of political shocks in 1994 for the devaluation of Dec’94 that resulted in the financial crisis of 1995 Jan’04 - Rebellion in the state of Chiapas by local Indians Mar’04 - Assassination of the official party’s presidential candidate (L.D. Colossio) Jun’04 – Kidnapping of prominent businessman (A. Harp) Sep’04 – Assassination of highest official of the ruling party Sharp drop in Mexico’s international reserves (USD 11Bn in 4 weeks in Mar’94) Interest rate rose sharply and the peso depreciated (8% in Mar’94 up to 15% in early Dec’94).

Jun’04 – Kidnapping of prominent businessman (A. Harp) Sep’04 – Assassination of highest official of the ruling party. Sharp drop in Mexico’s international reserves. (USD 11Bn in 4 weeks in Mar’94) Interest rate rose sharply and the peso depreciated. (8% in Mar’94 up to 15% in early Dec’94).")

14

As in prior election cycles, a pre-election disposition to stimulate the economy, temporarily and unsustainably, led to post-election economic instability. There were concerns about the level and quality of credit extended by banks during the preceding low-interest rate period, as well as the standards for extending credit. The country's risk premium was also affected by an armed rebellion in Chiapas, causing investors to be wary of investing their money in an unstable region. The Mexican government's finances and cash availability were further hampered by two decades of increasing spending, debt loads, and low oil prices. Its ability to absorb shocks was hampered by its commitments to finance past spending.

15

In order to finance the deficit (current account deficit 7% of GDP), Salinas issued the Tesobonos, a type of debt instrument denominated in pesos but indexed to dollars. Mexico experienced lax banking or corrupt practices; moreover, some members of the Salinas family collected enormous illicit payoffs. The EZLN, an insurgent rebellion, officially declared war on the government on January 1; even though the armed conflict ended two weeks later, the grievances and petitions remained a cause of concern, especially amongst some investors

16

The EZLN's violent uprising in Chiapas in 1994 along with the assassination of Presidential candidate Luis Donaldo Colosio made the nation's political future look less certain to investors, who then started placing a larger risk premium on Mexican assets. Mexico had a fixed exchange rate system that accepted pesos during the reaction of investors to a higher perceived country risk premium and paid out dollars. However, Mexico lacked sufficient foreign reserves to maintain the fixed exchange rate and was running out of dollars at the end of 1994. The peso then had to be allowed to devalue despite the government's previous assurances to the contrary, thereby scaring investors away and further raising its risk profile.

17

When the government tried to roll over some of its debt that was coming due, investors were unwilling to buy the debt and default became one of few options. A crisis of confidence damaged the banking system which in turn fed a vicious cycle further affecting investor confidence.

18

All of the above concerns, along with increasing current account deficit fostered by consumer binding and government spending, caused alarm among those who bought the tesobonos. The investors sold the tesobonos rapidly, depleting the already low central bank reserves. Given the fact that it was an election year, whose outcome might have changed as a result of a pre-election-day economic downturn, Banco de México decided to buy Mexican Treasury Securities to maintain the monetary base, thus keeping the interest rates from rising. This caused an even bigger decline in the dollar reserves.

19

The peso crashed under a floating regime from four pesos to the dollar to 7.2 to the dollar in the space of a week. The United States intervened rapidly, first by buying pesos in the open market, and then by granting assistance in the form of $50 billion in loan guarantees. The dollar stabilized at the rate of 6 pesos per dollar. By 1996, the economy was growing (peaked at 7% growth in 1999). In 1997, Mexico repaid, ahead of schedule, all US Treasury loans.

. In 1997, Mexico repaid, ahead of schedule, all US Treasury loans.")

20

Was Devaluation Inevitable?

Mexico’s private capital inflow totaled USD 95Bn from Capital inflow did not financed long-term investment spending (i.e. factories, equipment) that would have helped built future export potential required to reduced the current account deficit without slashing imports. Instead, capital inflow went into short-term financial investments (i.e. bank deposits and government bonds) that could flow out very fast in case of crisis.

that would have helped built future export potential required to reduced the current account deficit without slashing imports. Instead, capital inflow went into short-term financial investments (i.e. bank deposits and government bonds) that could flow out very fast in case of crisis.")

21

5 yrs. Total USD 95Bn (100%) USD 43Bn (45%) USD 28Bn (30%) USD 24Bn (25%)

USD 43Bn (45%) USD 28Bn (30%) USD 24Bn (25%)")

22

Foreign Capital Inflows

Mainly in government bonds, mainly short-term Mexican interests rates remained far above US rates 3 months CETE averaged 13% in 1992, with exchange rate depreciation of no more than 2.3% p.a., the rate of return in USD was ~11% vs. 3.73% of T-Bills In Feb’94, the US FED increase interests rates for the 1st time since before last recession (250 bps) Mexican Government issued short term debt in USD (Tesobonos)

Mexican Government issued short term debt in USD. (Tesobonos)")

23

The Bailout The crisis was handled relatively quickly due to the prompt response of the United States and the IMF in providing a $50 billion line of credit. Mexico, in return, put up its oil revenues as collateral. After a tough recession in 1995, Mexico began to recover strongly from the crisis. The rescue package restored investor confidence and stopped the massive capital outflows.

24

The Bailout Alan Greenspan believed that the immediate problems arising if Mexico defaulted out-weighted the moral hazard problem. The US and Mexico negotiated terms of the loan agreement (Mexico to limit money and credit and a collateral of oil export revenues to be deposited at Fed) The Peso continued to depreciate (up to $7.45) until Mexico announced a stringent austerity package.

The Peso continued to depreciate (up to $7.45) until Mexico announced a stringent austerity package.")

25

Conclusions Banking Crisis

More frequent in periods of high international capital mobility More likely with fixed exchange rates The Mexican crisis may have had elements of a self-fulfilling speculative attack: Calvo and Mendoza (1995) argue that “a speculative attack can topple an exchange rate peg even when economic fundamentals are sound, if investors display herding behavior and the country is financially vulnerable with large amounts of ST debt”

argue that a speculative attack can topple an exchange rate peg even when economic fundamentals are sound, if investors display herding behavior and the country is financially vulnerable with large amounts of ST debt")

Similar presentations

Walid Metwaly Wei Zhang (Richard)>")

Cash. The Beginnings of the Crisis The Mexican Peso Crisis began in 1994. The Mexican Peso Crisis began in 1994. In happened,>")