Download presentation

Presentation is loading. Please wait.

2

" Don’t be a pig in a highly levered global marketplace.”

3

In days of old when knights were bold and ladies most beholden straw seemed like silk and water, milk and silver almost golden Bill Gross – Pimco Not so sure about that limerick – it was probably a cruel world – those days of old. Yet much of it was fascinating and in some cases surreal. The relationship of “man” and God, for instance. Or better yet … “man,” animals and God. Unlike today, when most believe that animals were put on this Earth Adam, Eve and all of His creatures. Animals were responsible in some strange way for their own actions and therefore should be held accountable for them. for humanity’s pleasure or utility, most people in the Middle Ages believed that God granted free will to Adam, Eve and all of His creatures. Animals were responsible in some strange way for their own actions and therefore should be held accountable for them.

4

it seems. Often, there would be an actual execution with a hog being hanged by the neck until it was dead. The pork chops followed shortly thereafter, I assume. There was no Humane Society in 1500. Somehow I thought those “medieval” times needed a more reality-based ditty than the one cited above, so here’s a modern-day “Chaucer’s” attempt: Accountable? Well yes, animals were actually put on trial for their misdeeds. They might actually be considered “evil.” Beetles that munched on church pews, pigs that dined off of late evening drunkards, locusts that ravaged harvest wheat – all were viewed in a similar fashion much like their human counterparts – thieves, adulterers and murderers alike. Sometimes the animal would be brought before an actual court, sometimes (as with insects) tried in absentia. In the case of ravaging pigs, for instance, there might be a full judicial hearing with a prosecutor, defense and a robed judge who could order a range of punishments, including probation or even excommunication. No bad little piggies went to heaven,trial

tried in absentia. In the case of ravaging pigs, for instance, there might be a full judicial hearing with a prosecutor, defense and a robed judge who could order a range of punishments, including probation or even excommunication. No bad little piggies went to heaven,trial.")

5

In days of old when pigs were bold and people very prayerful a locust might be canonized and drunkards had to be careful. Now on to the world of investing, me Lords and Ladies, which by the way is full of little piggies feeding at the trough, scaredy “cats” afraid of their own shadow, and ostriches sticking their heads in the sand. And too, history will record that capitalism and its markets are a dog-eat-dog world. If so, we’ve currently got a menagerie to rival anything in those “days of old.” But let’s stick with the piggies for the following Investment Outlook. Hopefully the prose will be better than the previous poetry. I find it fascinating the number of ways that investors approach the “value” of securities and other investments such as commercial real estate or homes. Many of them are legitimate and form a solid foundation in academic research or even common sense. “Natural” interest rates, P/E ratios, cap rates,

6

risk and liquidity premiums, and even real estate’s “location, location, location” are ways to fundamentally price an asset. Add to that the emotional influence of human nature and you have a pretty good idea as to why prices go up and down; not necessarily a pretty good idea as to when they will go up and down, but at least the why part is partially visible. But lost in this rather complex maze of why is the function of credit and credit expansion in a modern, financial-based economy that it dominates. Asset prices are dependent on credit expansion or in some cases credit contraction, and as credit goes, so go the markets, one might legitimately say, and I do most emphatically say that! What exactly do I mean by “credit?” Well, money in all its multiple forms. Cash is a form of credit in my definition because you can use it to buy things. Bonds are credit. Stocks are credit. Houses and real estate can be considered credit when they are securitized and sold to investors in mortgage pools. In our modern financial economy, credit is anything that can be transferred on a wire or a computer from one account to another and ultimately be used as the basis for spending money on things such as groceries or airplane tickets.

7

And so when an investor tries to think about “prices” for these various forms of credit, it is necessary to get behind the winds of credit itself, to see what causes credit to behave like a mild South Seas breeze or a destructive typhoon in the China Sea. Credit creation or credit destruction is really the fundamental force that changes P/Es, risk premiums, natural interest rates, etc. For most investors that may be hard to understand, but that is where the little piggies come in. Imagine you are on that South Sea island with only two people. Each of you owns half of the island, grows your own food and has four little piggies for bacon and chops and all of the good stuff that people like to eat. Things are copasetic; the local “economy” is doing fine, but one day your other buddy figures out a way to make a new crop that you don’t have. She’s the island’s entrepreneur, so to speak. Well, being jealous and perhaps a tad greedy, your previous buddy refuses to share the secret. But she will offer you a future share of her harvest for one of your little pigs – there being no money, credit or anything of the sort on the island. You love that bacon, but the lady is living higher on the hog, so to speak, with that new “crop,” so you agree on a deal – one pig for one year’s harvest of her future “crop.” Despite the lack of a “stock market,” “crops” are now trading at a P/E of 1 X pigs. One pig equals one future year’s worth of your ex-buddy’s bountiful harvest. Well the months roll by and one thing leads to another, and for some

8

reason you want some more of your neighbor’s “crop.” Maybe it’s marijuana and the island has just legalized it for medicinal purposes. Let’s just say. And let’s say you’re willing to part with another pig for another share of medicinal “weed.” Neighbor, sensing enthusiasm, says, “No, it’ll cost you three pigs,” which is all you have, but you’re feeling high and certainly very hungry so you say OK. This funny smelling “grass” now sells at 3 X pigs, or a pigs-to-“grass” P/E ratio of 3/1 and everybody’s happy. Until … well … to get back to the real world, those piggies have really been credit or cash substitutes all along, and now in order to keep this system going you need more pigs or more credit in order to continue. But you’re out of pigs. A funny thing now happens in this capitalistic South Sea island and mainly to the price of marijuana. It traded last year at 3 pigs to 1, but since you’re out of pigs and credit, the price collapses. Grass goes to zero because there is no more credit; you have no more pigs to pay for it. So for those of you who don’t live in Washington State or Colorado or others who are a little miffed at this example, let’s just put it this way.

9

P/Es of 3 or P/Es of 15 or P/Es of 0 are intimately connected to the amount of available credit. So are interest rates. If there was only one dollar to lend and someone was desperate to have it, the interest rate would be usurious. If there was one trillion dollars of credit and no one was eager to borrow for some reason or another, then the rate would be.01% like it is today and for the past five years in my personal money market account. The amount of credit and its growth rate are critical to asset prices, and of course asset prices in our modern economy are critical to growth and job creation and future prospects for investment. We have a fiat/credit/debt-based economy that depends on the continuous creation of more and more credit in order to thrive and some would say – even survive. We need those pigs and more of them. And they need to circulate and be traded – what some would call “velocity” – in order to keep the economy growing. Our South Sea island economy never did change until the new crop was discovered, but concurrently, not until the pigs started to be traded for it.

10

And so? Well, to use the U.S. as an example, we officially have 57 trillion dollars’ worth of credit (stocks not being part of the Fed’s official definition) and probably 20 trillion more in what has come to be known as the “shadow” system. But call it 57 trillion because the Fed and Chart 1 do. the Fed

and probably 20 trillion more in what has come to be known as the shadow system. But call it 57 trillion because the Fed and Chart 1 do. the Fed.")

11

It used to grow pre-Lehman at 8–10% a year, but now it only grows at 3– 4%. Part of that growth is due to the government itself with recent deficit spending. A deficit of one trillion dollars in 2009–2010 equaled a 2% growth rate of credit by itself. But despite that, other borrowers such as households/businesses/local and foreign governments/financial institutions have been less than eager to pick up the slack. With the deficit now down to $600 billion or so, the Treasury is fading as a source of credit growth. Many consider that as a good thing but short term, the ability of the economy to expand and P/Es to grow is actually negatively impacted, unless the private sector steps up to the plate to borrow/invest/buy new houses, etc. Credit over the past 12 months has grown at a snail’s 3.5% pace, barely enough to sustain nominal GDP growth of the same amount.GDP growth Is there a one-for-one relationship between credit growth and GDP? Certainly not. That is where velocity complicates the picture and velocity is influenced by interest rates and the price of credit. But with QE beginning its taper, and interest/mortgage rates 150 basis points higher than they were in July of 2012, velocity may now negatively impact the equation. MV=PT or money X velocity = GDP is how economists explain it in old model textbooks. Actually the new model should read CV=PT or credit X velocity = GDP but most economists are classically trained to the Friedman model, which viewed money in a much narrower sense.

12

So our PIMCO word of the month is to be “careful.” Bull markets are either caused by or accompanied by credit expansion. With credit growth slowing due in part to lower government deficits, and QE now tapering which will slow velocity, the U.S. and other similarly credit-based economies may find that future growth is not as robust as the IMF and other model-driven forecasters might assume. Perhaps the whisper word of “deflation” at Davos these past few weeks was a reflection of that. If so, high quality bonds will continue to be well bid and risk assets may lose some luster. In any case, don’t be a pig in today’s or any day’s future asset markets. The days of getting rich quickly are over, and the days of getting rich slowly may be as well. Most medieval, perhaps. Davos And too, stick with PIMCO. Believe me when I say, we are a better team at this moment than we were before. I/we take the future challenge faced by all asset managers with close to a sacred trust. Not the one that the ancients granted to animals, but a more modern one embraced by the relationship of client/fiduciary and the need to be held accountable, sort of like the pigs and locusts in days of old when knights were bold.

13

Most ‘Medieval’ Speed Read 1)Asset prices depend on credit creation and expansion. 2) The U.S. and other countries create less credit from the public standpoint as their deficits decline. 3) 3–4% credit expansion in the U.S. may not be enough to maintain 3% growth, especially if asset prices go down and velocity is affected. 4) Don’t be a pig in a highly levered global marketplace. There is risk out there. William H. Gross

The U.S. and other countries create less credit from the public standpoint as their deficits decline. 3) 3–4% credit expansion in the U.S. may not be enough to maintain 3% growth, especially if asset prices go down and velocity is affected. 4) Don’t be a pig in a highly levered global marketplace. There is risk out there. William H. Gross.")

14

Tom McClellan BOTTOM LINE February’s bounce is stronger than we expected, and stronger than called for by our leading indicators. It arrives with very strong breadth, meaning that liquidity is no problem. The market might encounter other problems, but when liquidity is strong the other problems do not amount to much. The current view is that the market is overbought, and while breadth is strong, there are still other divergences. We look for a decline into a May bottom, but then a really strong rest of the year. T-Bond prices should benefit from that presumptive stock market correction, at least until May. Gold prices are still trending upward, and are set to do so into April. But gold futures need to get up above $1420 before the summer cycle dip, or else that means the Dec. 2013 price low gets taken out.

15

What To Expect Stocks show bottoms ahead on March 5/6, 13, and 17. That March 17 bottom signal gains some confirmation from an implied bottom signal on the BC Indicator due March 19, but those can invert. And the situation is made all the more confusing by a conflicting Timing Model top signal March 17. Sometimes the conflicting signals fight to a draw, and sometimes their collision sparks greater volatility. The March 4-5 top signals for T-Bonds may already be in, with the crisis in Ukraine now showing signs of abating. But more tops are ahead, and the trend is still clearly upward at the moment. Gold shows very little in the way of immediate guidance, but an important looking top is due April 9. That fits well with the comparison to the 2011 pattern as shown on page 4.

16

A Long Term Look At Gold The top chart on page 8 takes a really long term view of the history of gold prices, dating back to the founding of the U.S. when the price of gold was fixed in U.S. law. We sometimes need to pause to remember that for most of our history, gold has been fixed at a stationary price, with a couple of adjustments to that along the way. Pres. Nixon abandoned that fix in 1971, unilaterally terminating the convertibility of dollars to gold. Americans have only been allowed to trade gold legally since January 1975.

18

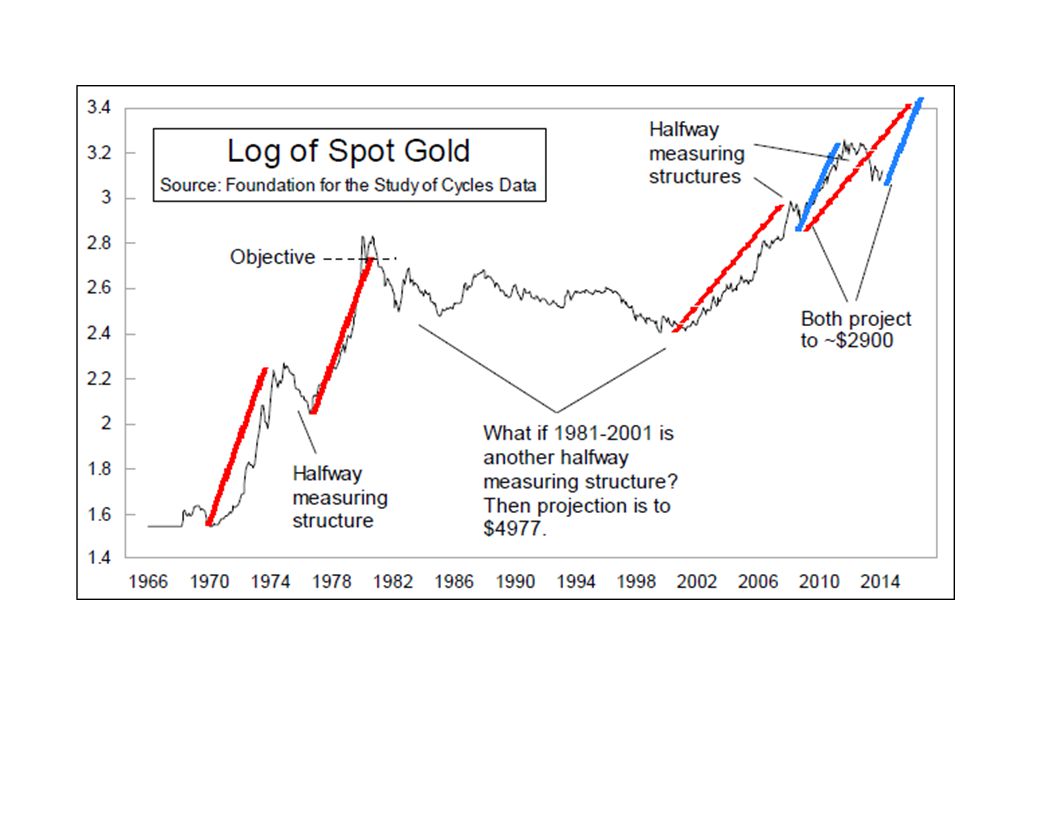

The history of gold’s price moves since the early 1970s dwarfs all of the previous deviations from the fixed price throughout history, and shows us just how much the dollar has been devalued (according to this measure). One notable point about the initial up move in the 1970s was that there was a significant pause just about halfway up, as measured on this logarithmic scaling. In classic bar chart analysis, that pause could be thought of as a halfway measuring “flag” structure. Gartley fans might just explain that it is a case of “AB=CD”. Whatever is the case, we don’t have a lot of history to look at to validate this idea of using such an interpretation.

19

But there was one notable spike up in the 1860s that we can perhaps consult. President Lincoln needed to fund the Civil War, and so the federal government printed “greenback” notes not backed by gold or silver, but rather by only the full faith and credit of the U.S. That sent gold prices up, and it was not until 1879 that the U.S. was able to return to a standard gold price of $20.67/oz. What is interesting about this is that the surge from 1861-65 also had a halfway pause, and the upside objective suggested by it was met and even exceeded. So based on this one case, and that of the 1970s, it may be a reasonable measuring technique.

20

That takes us to the final chart, where we contemplate the implications of the current structure. There was a significant pullback in 2008, related to the financial crisis then. If gold equals the logarithmic magnitude of the 2001-08 rise, then measuring from the late 2008 gives us an upside objective of around $2900/oz. A similar upside objective comes from applying this technique to the 2011- 2013 pullback. When gold might get there is not determined with this technique, but think years, not months. Perhaps even more interesting is to apply this same technique to the “pause” represented by the entire 1981- 2001 pullback. Using that as our “flag” structure projects to $4977!!

22

It is painful to contemplate the political and economic conditions which would be associated with that much of a rise in gold prices. And the whole application of this long term technique is based on a very small sample size. But it seems reasonable at this point. Let’s get to $2900 first, and then see what it looks like.

Similar presentations

we first.>")