Download presentation

Presentation is loading. Please wait.

1

Global Economics Eco 6367 Dr. Vera Adamchik

Intl Factor Movements and MNEs: Part 1

2

FDI and Multinational Enterprise

3

The U.S. company IBM pays cash to acquire 15% of all outstanding equity shares of a Taiwanese company that makes computer components. A U.S. investor John Smith pays cash to buy 10,000 shares (0.1% of all outstanding equity shares) of the same Taiwanese company. Both of these share purchases are international flows of financial capital from the U.S. to Taiwan. But only one is foreign direct investment.

of the same Taiwanese company. Both of these share purchases are international flows of financial capital from the U.S. to Taiwan. But only one is foreign direct investment.")

4

The key difference between the two investments is the degree to which each investor can control or influence the management of the company.

5

In foreign direct investment the investor has, or could have, an effective voice in the management of the foreign company. But how much ownership is enough to give the investor the ability to affect the management of the foreign firm? The agreed international standard is 10% ownership. (This standard is used by the U.S. and many other countries, but not by all countries.)

")

6

FDI typically occurs when the parent company:

(1) obtains sufficient common stock to assume voting control; (2) acquires or constructs new plants; (3) lends money to finance an expansion; (4) reinvests earnings in plant expansion. Hence, FDI serves as a broad measure that captures a country’s ownership of foreign business enterprises.

obtains sufficient common stock to assume voting control; (2) acquires or constructs new plants; (3) lends money to finance an expansion; (4) reinvests earnings in plant expansion. Hence, FDI serves as a broad measure that captures a country’s ownership of foreign business enterprises.")

7

M&A with existing firms greenfield investments

in the foreign country If a U.S. company purchases more than 50% of the shares outstanding, it has a controlling interest and the Taiwanese firm becomes a foreign subsidiary. The building of a plant in Taiwan by a U.S. company is also FDI, because clearly there is ownership and control of the new facility – a branch plant – by the U.S. company. greenfield investments

8

In contrast, John Smith does not expect to have any influence on the day-to-day management of the Taiwanese company. Rather, Smith is seeking financial returns by adding the 10,000 shares to his investment portfolio. Generally, the term international portfolio investment is used for all foreign investments that do not involve management control (that is, all that are not FDI).

.")

9

Examples of FDI and portfolio investments

10

The multinational corporation (MNC), sometimes referred to as

the multinational enterprise (MNE), the transnational corporation (TNC), or the transnational enterprise (TNE), is a firm that owns and controls operations in more than one country.

, the transnational corporation (TNC), or the transnational enterprise (TNE), is a firm that owns and controls operations in more than one country.")

11

The parent firm in the MNE is the headquarters or base firm, located in the home country of the MNE.

The parent firm has one or more foreign affiliates (subsidiaries or branches) located in one or more host countries.

located in one or more host countries.")

12

Vertical FDI – parent company establishes foreign subsidiary for production of intermediate goods or inputs used in the production of final goods. Horizontal FDI – parent company establishes subsidiary for production of good identical to that produced in the host country. Conglomerate FDI – parent company established foreign subsidiary for production of unrelated goods.

13

In-class exercise What is SWFs? (handout – an excerpt from the 2008 World Investment Report). Log on to , then click on “Programmes” (on the top horizontal menu); then click on “Investment and Enterprise” (on the left menu); then click on “Foreign Direct Investment” (on the left); then click on “World Investment Report” (on the left); then click on “WIR series” (on the left menu), click on “WIR 2008,” review Section C of Chapter 1 in this report.

; then click on Investment and Enterprise (on the left menu); then click on Foreign Direct Investment (on the left); then click on World Investment Report (on the left); then click on WIR series (on the left menu), click on WIR 2008, review Section C of Chapter 1 in this report.")

14

FDI: History and current patterns

15

The flow of FDI refers to the amount of FDI undertaken over a given time period. Outflows of FDI are the flows of FDI out of a country. Inflows of FDI are the flows of FDI into a country. The stock of FDI refers to the total accumulated value of foreign-owned assets at a given time.

18

To a large extent, FDI involves firms from industrialized countries investing in other industrialized countries. With one exception, the major home countries are also major host countries. The exception is Japan. It is host to relatively little FDI.

19

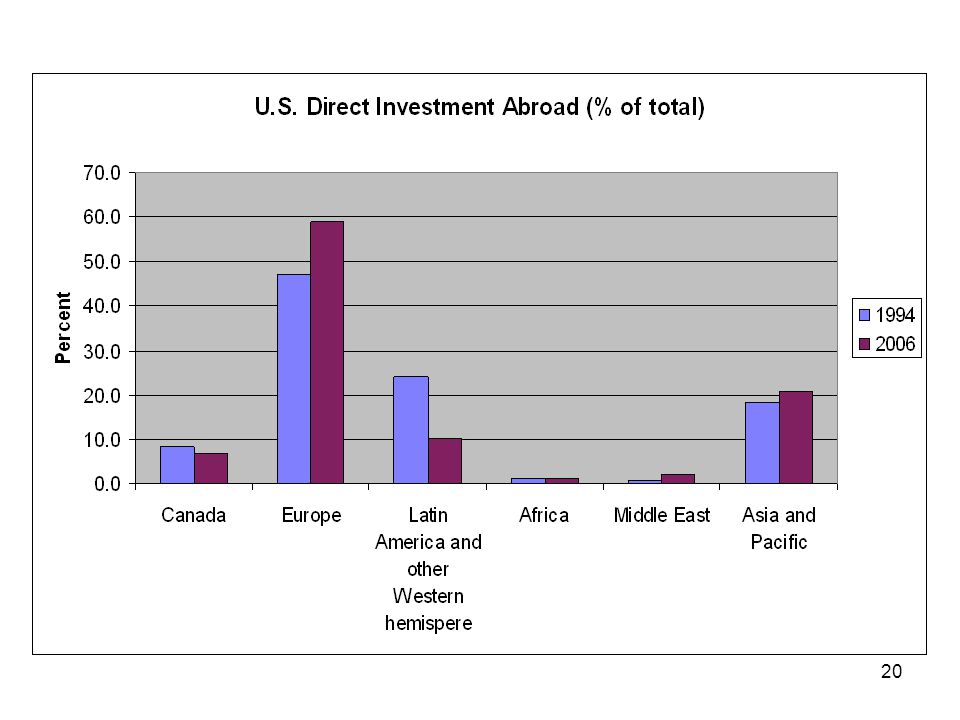

In-class exercise What do you think are the major destinations (countries and geographic regions) for the U.S. direct investment abroad (USDIA)? What do you think are the major sources (countries and geographic regions) of the foreign direct investment in the U.S. (FDIUS)? Name 3-5 countries and 2-3 geographic regions. Then go to the U.S. Bureau of Economic Analysis website to check if your answers are correct. Click on “Balance of Payments” under the “International” title, scroll down to “Operations of Multinational Companies,” click on “Selected Tables” under “Balance of payments and direct investment position data” under the “U.S. direct investment abroad” title, then click on “Capital flows without current-cost adjustment (also shows annual totals) 1994:I-2008:I | HTML | XLS under the “Quarterly Data” title. click on “Selected Tables” under “Balance of payments and direct investment position data” under the “Foreign direct investment in the U.S.” title, then click on “Capital flows without current-cost adjustment (also shows annual totals) 1994:I-2008:I | HTML | XLS under the “Quarterly Data” title.

for the U.S. direct investment abroad (USDIA) What do you think are the major sources (countries and geographic regions) of the foreign direct investment in the U.S. (FDIUS) Name 3-5 countries and 2-3 geographic regions. Then go to the U.S. Bureau of Economic Analysis website to check if your answers are correct. Click on Balance of Payments under the International title, scroll down to Operations of Multinational Companies, click on Selected Tables under Balance of payments and direct investment position data under the U.S. direct investment abroad title, then click on Capital flows without current-cost adjustment (also shows annual totals) 1994:I-2008:I | HTML | XLS under the Quarterly Data title. click on Selected Tables under Balance of payments and direct investment position data under the Foreign direct investment in the U.S. title, then click on Capital flows without current-cost adjustment (also shows annual totals) 1994:I-2008:I | HTML | XLS under the Quarterly Data title.")

22

The top five countries in 2006

USDIA: Netherlands, UK, Luxemburg, Canada, Ireland. FDIUS: UK, Germany, Japan, Canada, France .

23

Components of FDI flows

“In terms of the three main forms of FDI financing, equity investment dominates at the global level. During the past decade, it has accounted for about two-thirds of total FDI flows. The shares of the other two forms of FDI — intra-company loans and reinvested earnings — were on average 23% and 12% respectively. These two forms fluctuate widely, reflecting yearly variations in profit and dividend repatriations or the need for loan repayment.” (The 2005 WIR, Overview, p. 6).

.")

24

TNCs Today, an estimated 79,000 TNCs control some 790,000 foreign affiliates around the world (The 2008 WIR, p. 9).

.")

25

In-class exercise What are the top TNCs in terms of their foreign assets, number of foreign affiliates, etc.? What countries have the greatest number of TNCs? Can you think about any reasons why? Log on to , then click on “Programmes” (on the top horizontal menu); then click on “Investment and Enterprise” (on the left menu); then click on “Foreign Direct Investment” (on the left); then click on “World Investment Report” (on the left); then do the following: (a) on the left menu, click on “Largest TNCs” and review the lists for the top non-financial and financial TNCs; (b) click on “WIR series” (on the left menu), click on “WIR 2008,” review Section D of Chapter 1 in this report.

; then click on Investment and Enterprise (on the left menu); then click on Foreign Direct Investment (on the left); then click on World Investment Report (on the left); then do the following: (a) on the left menu, click on Largest TNCs and review the lists for the top non-financial and financial TNCs; (b) click on WIR series (on the left menu), click on WIR 2008, review Section D of Chapter 1 in this report.")

27

foreign direct investment

Theories of foreign direct investment

28

Why do multinational enterprises exist?

The answer seems simple – because they are profitable. That is, multinationals are simply a way of shifting financial capital between countries based on national differences in returns and risks. But the issue is more complicated than it sounds.

29

Although return and risk may play a role in the decisions by firms about whether to make direct investments, this financial theory of direct investment is not adequate. It does not explain why these international investments would be large enough to establish managerial control over the foreign companies. If the challenge is to transfer capital from one country to another, international portfolio investment can accomplish this task better than direct investment by firms whose major preoccupation lies in production and marketing.

30

The eclectic approach There is some agreement that several different pieces together provide a good explanation of why multinational firms exist (and why they are as large as they are). The combination of these pieces into a framework for understanding the multinational enterprise is often called the eclectic approach, with credit for the synthesis going to John Dunning (“Toward an Eclectic Theory of International Production: Some Empirical Tests”, Journal of International Business Studies, Vol. 11, 9-31, 1980). 30

. The combination of these pieces into a framework for understanding the multinational enterprise is often called the eclectic approach, with credit for the synthesis going to John Dunning ( Toward an Eclectic Theory of International Production: Some Empirical Tests , Journal of International Business Studies, Vol. 11, 9-31, 1980). 30.")

31

The eclectic approach considers: 1

The eclectic approach considers: 1. Firm-specific advantages (to overcome inherent disadvantages of being foreign). 2. Location factors (that favor foreign production over exporting). 3. Internalization advantages (that favor direct investment over contracting with independent firms). 31

. 2. Location factors (that favor foreign production over exporting). 3. Internalization advantages (that favor direct investment over contracting with independent firms). 31.")

32

1. Firm-specific advantages

What makes it possible for a multinational to overcome the inherent disadvantages of being foreign? To be successful, the multinational must have one or more firm-specific advantages, that is, one or more assets of the multinational enterprise that are not assets held by its local competitors in the host country (or, perhaps, by any other firm in the world). 32

. 32.")

33

A firm’s secret technology, patents,

access to very large amounts of financial capital, amounts far larger than the ordinary national firm can command, marketing advantages, truly superior management techniques. 33

34

Alternatives to FDI However, even if the firm has firm-specific advantages, still there are at least two alternatives to direct investment. First, the firm could export from its own country. Second, instead of using FDI to set up an affiliate, the firm could sell or rent its firm-specific advantages (superior technology, a strong brand name, better management practices, marketing techniques, etc.) to foreign firms using licenses.

to foreign firms using licenses.")

35

2. Location factors Location factors are key to answering the question “Export or FDI?” Location factors often favor foreign production over exporting (low costs of producing in foreign countries, low transportation costs, economies of scale, no need to pay tariffs or comply with other non-tariff barriers on imports, etc.). Hence, FDI is more attractive when transportation costs or trade barriers make exporting unattractive.

. Hence, FDI is more attractive when transportation costs or trade barriers make exporting unattractive.")

36

3. Internalization advantages

Further, in making the decision between FDI and licensing of foreign firms, the firm with the asset must weigh the advantages and disadvantages of each alternative.

37

An important advantage of licensing foreign firms is that the firm avoids (most of) the inherent disadvantages of establishing and managing its own foreign operations. On the other side, there are advantages of keeping the use of the firm-specific advantages within (internal to) the enterprise.

the enterprise.")

38

Internalization advantages are the advantages of using an asset within the firm rather than finding other firms that will buy, rent, or license the asset. In other words, the advantages of keeping the use of the assets under the control of the enterprise itself, and avoiding the transaction costs and risks of licensing an independent firm. FDI keeps the use of the assets under the control of the enterprise itself.

39

Internalization theory suggests that licensing has three major drawbacks:

licensing may result in a firm’s giving away valuable technological know-how to a potential foreign competitor; licensing does not give a firm the tight control over manufacturing, marketing, and strategy in a foreign country that may be required to maximize its profitability; a problem arises with licensing when the firm’s competitive advantage is based not so much on its products as on the management, marketing, and manufacturing capabilities that produce those products.

40

Hence, a firm will favor FDI over licensing when it wishes to maintain control over its technological know-how, or over its operations and business strategy, or when the firm’s capabilities are simply not amenable to licensing.

41

Theories of FDI: Summary

The “ownership-location-internalization” (O-L-I) framework has become the centerpiece of the literature on multinational corporations. This framework suggests that it is optimal for a firm to be a MNC, and thereby locate some of its production centers outside its home country, if three different conditions are satisfied.

framework has become the centerpiece of the literature on multinational corporations. This framework suggests that it is optimal for a firm to be a MNC, and thereby locate some of its production centers outside its home country, if three different conditions are satisfied.")

42

The “O-L-I” paradigm The firm has to own knowledge (technology) about products and processes that endow it with an advantage over competitors within its industry. Location in the host country should provide the firm some advantage like elimination of tariff and transportation costs that induces the firm to locate (part of) its operations in the host country. Internalization will benefit the firm when it is more profitable to conduct transactions and production within a single organization than in separate organizations.

about products and processes that endow it with an advantage over competitors within its industry. Location in the host country should provide the firm some advantage like elimination of tariff and transportation costs that induces the firm to locate (part of) its operations in the host country. Internalization will benefit the firm when it is more profitable to conduct transactions and production within a single organization than in separate organizations.")

43

The O-L-I paradigm A firm undertakes FDI when ownership, location, and internalization advantages combined make a location appealing Location advantage (optimal location) Location advantage (optimal location) Ownership advantage (special asset) Internalization advantage (using the assets within the firm) 43

Location. advantage. (optimal location) Ownership. advantage. (special asset) Internalization. advantage. (using the assets. within the firm) 43.")

44

The mode of entry The “ownership-location-internalization” paradigm, however, does not provide any obvious rationale as to HOW a MNC should enter a new market: as a wholly owned subsidiary, by way of acquisition of a local firm, or in partnership (joint-venture) with a local firm. The choice of an entry mode is critical in a firm’s globalization strategy because each entry mode differs on the degree of control allowed to the parent company, the degree of risk incorporated in its implementation and the demands it places on the firm’s resources. It is amongst the most significant decisions that a firm will make as it embarks upon a global strategy to penetrate foreign markets.

with a local firm. The choice of an entry mode is critical in a firm’s globalization strategy because each entry mode differs on the degree of control allowed to the parent company, the degree of risk incorporated in its implementation and the demands it places on the firm’s resources. It is amongst the most significant decisions that a firm will make as it embarks upon a global strategy to penetrate foreign markets.")

45

Recently, the choice of the mode of entry in a foreign country by a firm has become one of the most widely researched areas in the international business arena. Several theoretical perspectives have been advanced to explain the choice of entry mode by global companies. Over the past decades, more than 25 different variables (for example, firm size, multinational experience, industry growth, global industry concentration, technical intensity, etc.) have been empirically tested for their influence on the entry mode decision. However, research findings on the significance of variables in terms of their impact on choice of entry mode have been conflicting: some studies identify some factors as being significant, and others negate such conclusions.

have been empirically tested for their influence on the entry mode decision. However, research findings on the significance of variables in terms of their impact on choice of entry mode have been conflicting: some studies identify some factors as being significant, and others negate such conclusions.")

46

Benefits and costs of FDI

47

Government policy is often shaped by a consideration of the costs and benefits of FDI.

48

Host-country benefits

There are four main benefits of inward FDI for a host country: 1. resource transfer effects - FDI can make a positive contribution to a host economy by supplying capital, technology, and management resources that would otherwise not be available; 2. employment effects - FDI can bring jobs to a host country that would otherwise not be created there;

49

3. balance of payments effects - a country’s balance-of-payments account is a record of a country’s payments to and receipts from other countries. Governments typically prefer to see a current account surplus (exports > imports) than a deficit. FDI can help a country to achieve a current account surplus if the FDI is a substitute for imports of goods and services, and if the MNE uses a foreign subsidiary to export goods and services to other countries.

than a deficit. FDI can help a country to achieve a current account surplus if the FDI is a substitute for imports of goods and services, and if the MNE uses a foreign subsidiary to export goods and services to other countries.")

50

4. effects on competition and economic growth - FDI in the form of greenfield investment increases the level of competition in a market, driving down prices and improving the welfare of consumers. Increased competition can lead to increased productivity growth, product and process innovation, and greater economic growth.

51

Host-country costs Inward FDI has three main costs:

1. the possible adverse effects of FDI on competition within the host nation --subsidiaries of foreign MNEs may have greater economic power than indigenous competitors because they may be part of a larger international organization;

52

2. adverse effects on the balance of payments:

with the initial capital inflows that come with FDI must be the subsequent outflow of capital as the foreign subsidiary repatriates earnings to its parent country, when a foreign subsidiary imports a substantial number of its inputs from abroad, there is a debit on the current account of the host country’s balance of payments;

53

3. the perceived loss of national sovereignty and autonomy -- key decisions that can affect the host country’s economy will be made by a foreign parent that has no real commitment to the host country, and over which the host country’s government has no real control. Management Focus: DP World and the United States Summary This feature explores the reaction to the bid by DP World, a Dubai-based ports operator, to acquire P&O, a British firm that runs a network of global marine terminals. An acquisition of P&O would give DP World management of six U.S. ports. While the Bush administration claimed the acquisition posed no threat to national security, several prominent U.S. Senators raised concerns about the acquisition. Ultimately, DP World pulled out of the deal, but stated that it would look for alternative ways to enter the U.S. market. The following questions can be used in a discussion. Suggested Discussion Questions 1. Do you agree with the senators who raised concerns about the DP World deal? Why or why not? Would your response be different if DP World were a British firm? Discussion Points: This issue will probably generate significant debate among students. At the heart of the issue is whether a company, because of its country of origin, should be denied ownership of something that could be important to a nation’s national security. Some students will probably argue that the U.S. was unjustified in its reaction to the deal, that DP World has a long history of American associations. Students taking this perspective will probably suggest that the U.S. is being prejudiced against the company simply because of its nationality. Other students however, will probably claim that DP World’s role in with American companies to date, has not involved ownership of ports that could be important to the country’s national security. Students in this camp will probably argue that the ports should be owned by American companies, or at least companies from countries that are allies of the United States in order to preserve national security, but definitely not a state-owned company from the Middle East. The implication here is that ownership of the ports would effectively transfer to a foreign government. 2. DP World has vowed to enter the U.S. market in some other way. Why is the U.S. market so important to DP World? What do you think the response of the government might be to another attempt by DP World? Discussion Points: The U.S. market is important to DP World because it is an epicenter of capitalism. Goods from all over the world flow to the United States, and DP World wants to be in a position to capitalize on this. Students will probably agree that should the company make another attempt to gain a foothold in the market, the United States will be reluctant to allow DP World a significant role in the country, especially in major ports.

54

In-class exercise Review the book “Does Foreign Direct Investment Promote Development?” edited by Theodore H. Moran , Edward M. Graham and Magnus Blomström published in May 2005 ( ). As the authors state, “This book confirms that FDI can have DRAMATICALLY DIFFERENT IMPACTS, BOTH POSITIVE AND NEGATIVE.” If interested, you may want to read Chapter 2 of the book “The Impact of Inward FDI on Host Countries: Why Such Different Answers?” (click on the link provided above, then click on “Chapter 2”).

. As the authors state, This book confirms that FDI can have DRAMATICALLY DIFFERENT IMPACTS, BOTH POSITIVE AND NEGATIVE. If interested, you may want to read Chapter 2 of the book The Impact of Inward FDI on Host Countries: Why Such Different Answers (click on the link provided above, then click on Chapter 2 ).")

55

Home-country benefits

The benefits of FDI for the home country include: the effect on the capital account of the home country’s balance of payments from the inward flow of foreign earnings; the employment effects that arise from outward FDI; the gains from learning valuable skills from foreign markets that can subsequently be transferred back to the home country.

56

Home-country costs The home country’s balance of payments can suffer:

from the initial capital outflow required to finance the FDI; if the purpose of the FDI is to serve the home market from a low cost labor location; if the FDI is a substitute for direct exports; employment may also be negatively affected if the FDI is a substitute for domestic production.

Similar presentations

>")