Download presentation

Presentation is loading. Please wait.

1

WEEK 5 – Review Test Review Test Answers Chapter 7

Need to FOCUS on main points!!!! Chapter 7 Finance Instruments Chapter 8 Overview Loan Process Loan Origination Loan Processing…………possibly next wk!!

2

TEST REVIEW HAND OUT TESTS W/SCORES HAND OUT TEST QUESTIONS

ONE STUDENT TAKING MAKEUP TEST

3

Chapter 7 Finance Instruments

4

I. Promissory Notes

5

Promissory Notes MAKER TQ PAYEE TQ

Before a lender will finance the purchase of a house, the borrower must promise to repay the funds. A PROMISSORY NOTE is a written promise to pay money. TQ MAKER TQ PAYEE TQ The promissory note is the basic evidence of debt: it shows who owes how much money to whom.

6

Figure 7-1 PAGE 122 TEXT

7

Chapter 7 Finance Instruments

8

I. Promissory Notes

9

Promissory Notes Before a lender will finance the purchase of a house, the borrower must promise to repay the funds. VERY LIKELY TQS ABOUND ON THIS PAGE!!! TQ A PROMISSORY NOTE is a written promise to pay money. MAKER PAYEE The promissory note is the basic evidence of debt: it shows who owes how much money to whom.

10

Figure 7-1 PAGE 122

11

A. NEGOTIABLE INSTRUMENTS

NEGOTIABLE INSTRUMENTS are promissory notes that are freely transferable. The promissory note is almost always accompanied by a security instrument. DEED OF TRUST, MORTGAGE, ARE 2 GREAT EXAMPLES A SECURITY INSTRUMENT gives the creditor the right to have the security property sold to satisfy the debt if the debtor fails to pay the debt according to the terms of the agreement. The security instrument may be either a deed of trust or a mortgage

12

LOOK BELOW II. The Deed of Trust

13

The Deed of Trust The DEED OF TRUST (or TRUST DEED) is a commonly used security device. ESPECIALLY IN CALIFORNIA TQ GRANTOR or TRUSTOR TQ BENEFICIARY TQ TRUSTEE TQ

14

DEED OF TRUST – CONTINUED

(PAGE 126 TEXT) DEED OF TRUST – CONTINUED The deed of trust (lien) gives the creditor the right to force the sale of the property if the debtor defaults on the obligations under the promissory note or the trust deed.

DEED OF TRUST – CONTINUED. The deed of trust (lien) gives the creditor the right to force the sale of the property if the debtor defaults on the obligations under the promissory note or the trust deed.")

15

A. REQUIREMENTS FOR A VALID TRUST DEED

To be valid, a deed of trust must contain certain provisions. These include: 1. A statement pledging the property as collateral for a debt (a granting clause). 2. A complete and unambiguous property description. 3. The amount of the debt. 4. The maturity date of the debt. 5. A defeasance clause (stating that the trust deed will be cancelled when the debt is paid). 6. A power-of-sale clause. When the debt is paid in full, the beneficiary directs the trustee to reconvey the title to the trustor. TQ A DEED OF RECONVEYANCE returns full title to the maker of the debt. TQ

. 2. A complete and unambiguous property description. 3. The amount of the debt. 4. The maturity date of the debt. 5. A defeasance clause (stating that the trust deed will be cancelled when the debt is paid). 6. A power-of-sale clause. When the debt is paid in full, the beneficiary directs the trustee to reconvey the title to the trustor. TQ. A DEED OF RECONVEYANCE returns full title to the maker of the debt. TQ.")

16

Figure 7-2 DEED OF TRUST PAGE PG 126

BE AWARE A “USUAL” DOT IS APPX 15 PGS. TQ

18

B. FORECLOSURE A deed of trust allows the beneficiary to foreclose the lien without the burden of bringing a legal action. TQ This is called a NONJUDICIAL FORECLOSURE, which is foreclosure without having to go to court. THE USUAL COURSE OF ACTION IN CALIFORNIA. TQ TQ TQ!!!

19

C. POWER OF SALE The deed of trust contains a power-of-sale clause that authorizes the trustee to sell the property without court supervision if the debtor defaults. TQ A typical power-of-sale clause might read as follows: If the default is not cured on or before the date specified in the notice, lender, at its option, may require immediate payment in full of all sums secured by this security instrument without further demand and may invoke the power of sale. If lender invokes the power of sale, lender shall execute or cause trustee to execute a written notice of the occurrence of an event of default and of lenders election to cause the property to be sold.

20

D. TRUSTEE’S SALE At the direction of the beneficiary, the trustee conducts an out-of-court sale, or auction, called a TRUSTEE’S SALE. (“WENT TO SALE” on the county courthouse steps) TQ The proceeds from the sale are used to pay off the trustor’s debt. However, before the trustee can sell the property, certain legal requirements must be met. (KNOW THE 3 TQ) A NOTICE OF SALE TRUSTEE’S DEED NOTICE OF DEFAULT The trustee applies the sale proceeds in the following order: 1. To pay the trustee’s costs and sale expenses. 2. To satisfy the beneficiary’s debt. 3. To junior lien holders in order of priority. 4. To the debtor, if any surplus.

TQ. The proceeds from the sale are used to pay off the trustor’s debt. However, before the trustee can sell the property, certain legal requirements must be met. (KNOW THE 3 TQ) A NOTICE OF SALE. TRUSTEE’S DEED. NOTICE OF DEFAULT. The trustee applies the sale proceeds in the following order: 1. To pay the trustee’s costs and sale expenses. 2. To satisfy the beneficiary’s debt. 3. To junior lien holders in order of priority. 4. To the debtor, if any surplus.")

21

E. ADVANTAGES AND DISADVANTAGES OF THE TRUST DEED

For the creditor, the primary advantage of the deed of trust is the quick and inexpensive non-judicial sale process, with no post-sale right of redemption for the borrower. TQ The primary disadvantage (FOR THE ‘BANK’ or noteholder) is that a deficiency judgment is unobtainable after a nonjudicial foreclosure. TQ From the borrower’s point of view, the protection against deficiency judgements is probably the main advantage of the trust deed. TQ TQ!! The speed of the process, the lack of judicial supervision, and the lack of redemption rights following the trustee’s sale are all disadvantages for the borrower.

is that a deficiency judgment is unobtainable after a nonjudicial foreclosure. TQ. From the borrower’s point of view, the protection against deficiency judgements is probably the main advantage of the trust deed. TQ TQ!! The speed of the process, the lack of judicial supervision, and the lack of redemption rights following the trustee’s sale are all disadvantages for the borrower.")

22

REMEMBER – DEED OF TRUST IN

III. Mortgages REMEMBER – DEED OF TRUST IN CALIFORNIA!! TQ

23

Mortgages A MORTGAGE is a two-party instrument in which the borrower mortgages his or her property to the lender. MORTGAGOR MORTGAGEE For the most part, lenders prefer the deed of trust to the mortgage.

24

FORECLOSURE STEPS 3 STEPS TO FORECLOSURE A foreclosure under a mortgage requires a court-ordered sale conducted by the sheriff or other court-appointed official. JUDICIAL FORECLOSURE FORECLOSURE ACTION ORDER OF EXECUTION

25

1. Redemption At any time up until the sheriff’s sale, the debtor may save the property by paying the mortgagee what is due. This right to save or redeem the property before the sale is called the EQUITABLE RIGHT OF REDEMPTION. TQ The debtor may also be obligated to pay delinquent interest, court costs, attorney’s fees, and sheriff’s fees in order to redeem the property.

26

2. Sheriff’s Sale The SHERIFF’S SALE is a public auction, normally held at the courthouse door, and anyone can bid on the property. The property is sold to the highest bidder (BUT, THE NOTEHOLDER NORMALLY HAS A “RESERVE” (minimum) AMOUNT) TQ and the proceeds are used to pay for the costs of the sale and to pay off the mortgage. As with the trust deed, any surplus goes to the debtor. TQ If the property does not bring enough money at the sale to pay off the mortgage, the debtor may be able to obtain a deficiency judgment against the debtor for the remaining debt. NOT CA TQ In some states, such as California, deficiency judgments are prohibited if the mortgage secured a loan to purchase a one-to-four-unit personal residence occupied by the owner. TQ

AMOUNT) TQ and the proceeds are used to pay for the costs of the sale and to pay off the mortgage. As with the trust deed, any surplus goes to the debtor. TQ. If the property does not bring enough money at the sale to pay off the mortgage, the debtor may be able to obtain a deficiency judgment against the debtor for the remaining debt. NOT CA TQ. In some states, such as California, deficiency judgments are prohibited if the mortgage secured a loan to purchase a one-to-four-unit personal residence occupied by the owner. TQ.")

27

3. Post-Sale Redemption After the sale, the debtor has another opportunity to save or redeem the property. TQ The debtor can do this by paying the purchaser the amount paid for the property plus accrued interest from the time of the sale. TQ This right to redeem the property following the sheriff’s sale is called the STATUTORY RIGHT OF REDEMPTION. TQ

28

B. ADVANTAGES AND DISADVANTAGES OF THE MORTGAGE

For the creditor, the main advantage of a mortgage is the right to obtain a personal judgment against the debtor for any deficiency if the property does not bring enough at the sheriff’s sale to satisfy the debt. NOT HERE (CA) IN MOST CASES The main disadvantages to the creditor concern the time and expense involved in executing a judicial foreclosure. ABOUT A YEAR! TQ The advantage of a mortgage for the debtor is slow court proceedings. A mortgagor usually has the time to get the money together to prevent the foreclosure than a trust deed borrower. On the other hand, a disadvantage the mortgagor faces is the possibility of a deficiency judgment and a portion of the debt may have to be repaid. (NOT IF PURCHASE LOAN IN CALIF.) TQ

IN MOST CASES. The main disadvantages to the creditor concern the time and expense involved in executing a judicial foreclosure. ABOUT A YEAR! TQ. The advantage of a mortgage for the debtor is slow court proceedings. A mortgagor usually has the time to get the money together to prevent the foreclosure than a trust deed borrower. On the other hand, a disadvantage the mortgagor faces is the possibility of a deficiency judgment and a portion of the debt may have to be repaid. (NOT IF PURCHASE LOAN IN CALIF.) TQ.")

29

IV. Real Estate Contracts

JUMP TO WINFORMS ON W. W. W…. SEE EXAMPLES BESIDES THE BOOK….

30

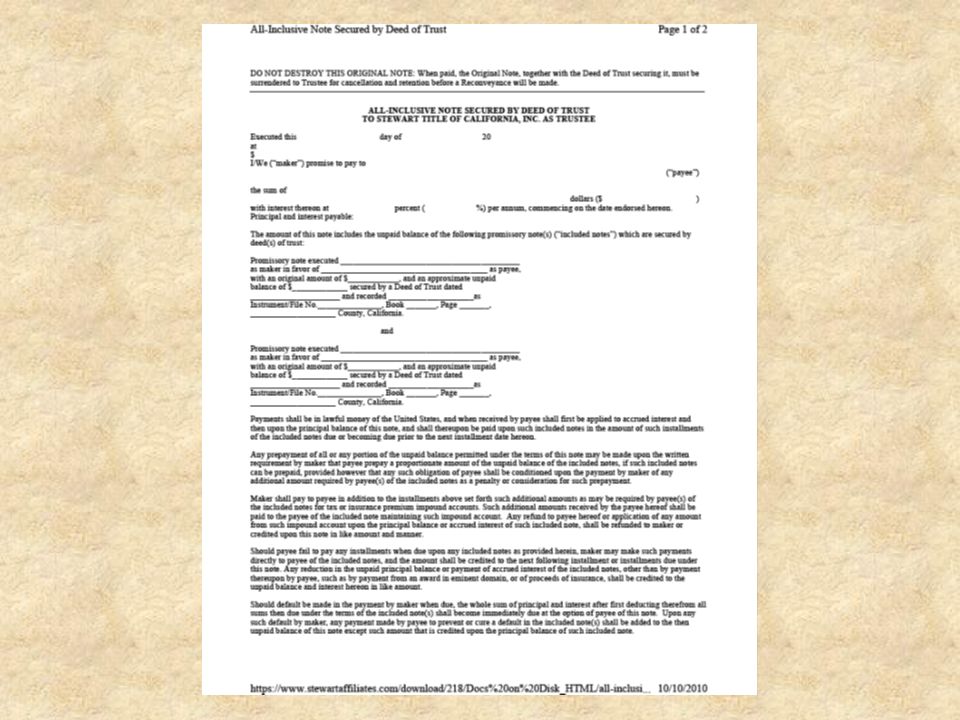

Real Estate Contracts Real estate contracts are also called contracts for deed, installment sales contracts, conditional sales contracts, and land contracts. TQ Real estate contracts differ significantly from mortgages and deeds of trust. Under a REAL ESTATE CONTRACT, the seller (VENDOR) retains legal title until the buyer (VENDEE) pays off the entire contract. AKA “ALL INCLUSIVE TRUST DEED” or AITD (or “wraparound”) TQ During the period the purchaser is paying on the contract, which may be many years, the purchaser has the right to possess and enjoy the property, but is not the legal owner, DOESN’T HAVE TITLE. TQ A lot of contreversey around this type of title….it’s fine if seller has it “free & clear” but if no…POSSIBLE ISSUES TQ

retains legal title until the buyer (VENDEE) pays off the entire contract. AKA ALL INCLUSIVE TRUST DEED or AITD (or wraparound ) TQ. During the period the purchaser is paying on the contract, which may be many years, the purchaser has the right to possess and enjoy the property, but is not the legal owner, DOESN’T HAVE TITLE. TQ. A lot of contreversey around this type of title….it’s fine if seller has it free & clear but if no…POSSIBLE ISSUES TQ.")

33

A. ADVANTAGES AND DISADVANTAGES OF REAL ESTATE CONTRACTS

For the seller, one advantage of contract sales is the personal satisfaction or security that the seller may feel by remaining the title owner. A QUIET TITLE The main disadvantage for the vendor is the expense and time required for terminating the contract and retaking possession of the property. A serious disadvantage for the vendee under the contract is the fact that the vendor remains the legal owner, unlike mortgages or deeds of trust.

34

V. Typical Clauses in Security Instruments

35

A. ACCELERATION CLAUSE Almost all promissory notes, mortgages, deeds of trust, and many real estate contracts contain an acceleration clause. An ACCELERATION CLAUSE allows the creditor or seller to accelerate the debt, that is, to declare the entire outstanding balance immediately due and payable in the event of default. Most lenders will wait until payments are at least 90 days delinquent before they enforce an acceleration clause. Under California law, if the loan is secured by owner-occupied residential property, the borrower must be allowed to prepay up to 20% of the original loan amount in one year without penalty.

36

B. PREPAYMENT CLAUSE Many conventional “SUBPRIME” loans HAVE prepayment provisions. Not a likely scenario for current or future financing now The basic effect of a prepayment provision is to charge the debtor for paying off the loan too early and depriving the lender of receiving the anticipated interest. TQ !!

37

C. ALIENATION CLAUSE’S DUE ON SALE CLAUSE

Alienation refers to transfer of ownership of a property under contract by a third party. *** see next slide for clarification ALIENATION CLAUSES in loan documents limit the debtor’s right to transfer the property without the creditor’s permission. TQ DUE ON SALE CLAUSE In California, a lender may not enforce the alienation clause and also the prepayment penalty on one-to-four-unit dwellings. TQ

38

CLARIFICATION of “ALIENATION”*

Party 1 own’s a single family residence, with a mortgage on it, owed to Party 2 Party 2, is the lender, and entered into a contract with Party 1 after qualification etc, and with an “alienation” clause in the loan contract Party 3 buys the property from Party 1, who then enters into a “land contract” or “AITD” with Party 1, while Party 1 still owes Party 2. The alienation clause stipulates then, that Party 2 needs to be paid in full….hmmmmm

39

D. SUBORDINATION CLAUSE

Generally, the priority among mortgages, trust deeds, and real estate contracts is determined by the date of recording, the first recorded instrument being the first in priority. In some situations, however, the parties may desire that a later recorded instrument have priority over an earlier recorded instrument. This is particularly common (or at least has been) in construction financing. A SUBORDINATION CLAUSE states that the instrument in which it is contained will be subordinate (junior) to a construction loan lien (mortgage or deed of trust) to be recorded later.

in construction financing. A SUBORDINATION CLAUSE states that the instrument in which it is contained will be subordinate (junior) to a construction loan lien (mortgage or deed of trust) to be recorded later.")

40

E. PARTIAL RELEASE, SATISFACTION, OR RECONVEYANCE CLAUSE This exists, we’ll talk but not test…!

A PARTIAL RELEASE, SATISFACTION, OR RECONVEYANCE CLAUSE obligates the creditor to release part of the property from the lien when part of the debt has been paid. Example: A real estate contract for the purchase of five acres of land may contain a clause stating that when the vendee has paid 20% of the purchase price, the vendor will execute a deed to the vendee for one acre of the land. This would allow the vendee to acquire clear title to one acre, which may then be used to build upon. Such clauses are also frequently found in blanket mortgages or trust deeds covering subdivisions in the process of being developed and sold. PARTIAL RELEASE (for real estate contracts) PARTIAL SATISFACTION (for mortgages) PARTIAL RECONVEYANCE (for trust deeds)

PARTIAL SATISFACTION (for mortgages) PARTIAL RECONVEYANCE (for trust deeds)")

41

VI. CHAPTER SUMMARY Instruments of real estate finance are documents that provide evidence of debt and give the lender the right to proceed against the collateral property if the borrower defaults on the loan. The promissory note is the basic instrument of debt, signed by the borrower and showing the amount of the loan, interest rate, method and manner of repayment, and the borrower’s promise to repay the debt. TQ Mortgages, deeds of trust, and real estate contracts give the lender or seller the right to foreclose against or repossess the property if the buyer defaults. TQ (so they can regain the use of their capital hopefully) Some particular clauses found in many mortgages, trust deeds, and installment contracts include acceleration clauses, prepayment provisions, and alienation (due- on-sale) clauses. Subordination agreements and partial release or satisfaction clauses are less common in residential loans, but are frequently found in construction or development loans.

Some particular clauses found in many mortgages, trust deeds, and installment contracts include acceleration clauses, prepayment provisions, and alienation (due- on-sale) clauses. Subordination agreements and partial release or satisfaction clauses are less common in residential loans, but are frequently found in construction or development loans.")

42

DONE FOR TONIGHT LET’S ALL STUDY CHAPTERS 8 & 9

CHAPTER TEN IS NOT REQUIRED NEXT WEEK WE WILL COVER THE LOAN PROCESS ALSO WE WILL DISCUSS “ORIGINATION” VS. PROCESSING

Similar presentations

>")

–Commercial Larger apartments & non-residential.>")