Download presentation

Presentation is loading. Please wait.

1

CHAPTER 4: INVESTMENT COMPANIES

2

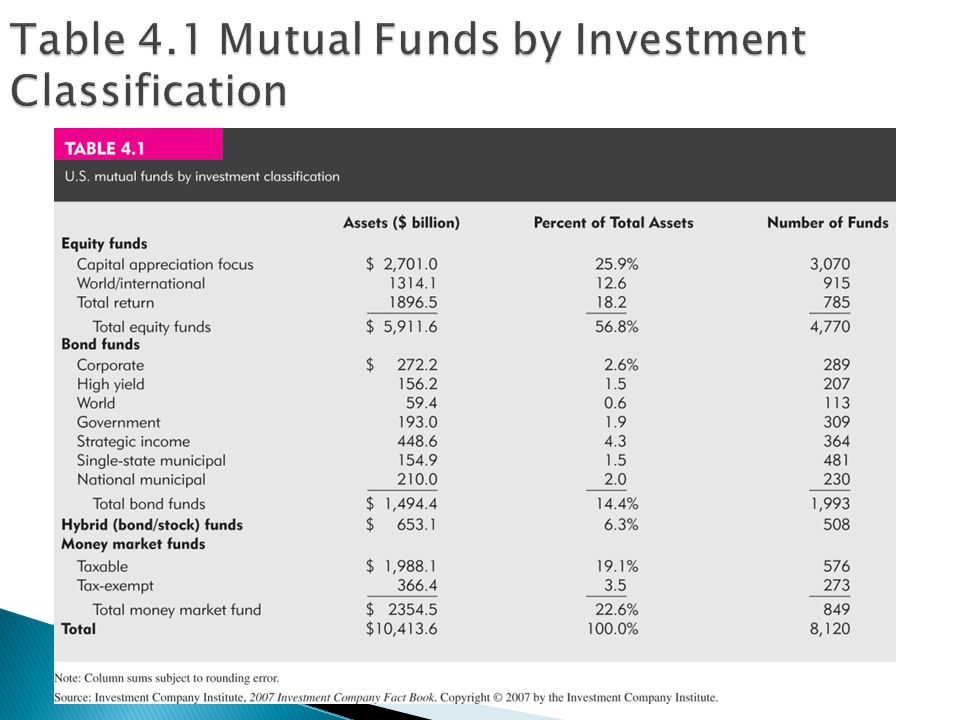

Definition: financial intermediaries that collect funds from individual investors and invest those funds in a potentially wide range of securities Administration & record keeping ◦ issue periodic status reports, keeping track of capital gain distributions, dividends, investments, and redemption Diversification & divisibility: diversify portfolios and investors can buy fractional shares of many different securities Professional management: full-time staffs of security analysts and portfolio managers Reduced transaction costs: can achieve substantial savings on brokerage fees and commissions because of large transactions

3

Net Asset Value ◦ Used as a basis for valuation of investment company shares ◦ Selling new shares ◦ Redeeming existing shares Calculation: Market Value of Assets - Liabilities Shares Outstanding Example: Consider a mutual fund that manages a portfolio of securities worth $120 mil. Suppose the fund owes $4 mil to its investment advisers and owes another $1mil for rent, wages and other expenses. The fund has 5mil shares outstanding. What is NAV of the fund

4

4.2 TYPES OF INVESTMENT COMPANIES

5

Pools of money from many investors that is invested in a portfolio fixed for the life of the fund Little active management Example: invest in municipal bond, corporate bond

6

Hire managers to manage portfolio Open-End ◦ stand ready to redeem or issue shares at their net asset value. If investors in open-end funds want to cash out shares, they sell back to the fund at NAV Closed-End ◦ Funds cannot issue or redeem shares. Investors who want to cash out must sell shares to other investors ◦ Sold at premium or discount to NAV ◦ Shares of close-end fund are traded on organized exchanges just like other common stocks.

8

◦ Commingled funds partnership of investors that pool their funds. Similar to open-end fund. Example: trust or retirement account that have portfolios much larger than those of most individual investors but still too small to warrant managing on a separate basis ◦ REITs: similar to closed-end fund but invest in real estate or loans secured by real estate ◦ Hedge Funds like mutual fund: hedge fund allows private investors to pool assets to be invested by a fund manager Unlike mutual fund: hedge fund are commonly structured as private partnerships and are not subject to many SEC regulations

9

4.3 MUTUAL FUNDS

10

mutual fund is a common name for open- end investment company. Account for >90% of investment company asset. Described in the prospectus Management companies manage a family of mutual funds. Some examples include: ◦ Fidelity ◦ Vanguard ◦ Putnam ◦ Dreyfus

11

Money Market: invest in money market securities. Equity: invest in stocks ◦ Income fund and growth fund Specialized Sector: sector funds Bond: invest in bond

12

Balanced Funds: hold both equities and fixed income securities in relatively stable proportions to meet needs of individual investors Asset Allocation and Flexible: similar to balance funds but the proportion can change according to managers’ forecasts Indexed: match performance of a broad market index. Example: Vanguard 500 Index Fund International

14

4.4 COSTS OF INVESTING IN MUTUAL FUNDS

15

Fee Structure ◦ Front-end load: commission or sale charge paid when purchasing the shares ◦ Back-end load: redemption or exit fee incurred when you sell shares. Operating expenses 12 b-1 charges distribution costs paid by the fund Alternative to a load Fees and performance

18

Initial NAV = $20 Income distributions of $.15 Capital gain distributions of $.05 Ending NAV = $20.10:

19

Example: you purchased 1000 shares of the New Fund at a price of $20 at the beginning of the year. You paid a front-end load of 4%. The securities in which the fund invests increase in value by 12% during the year. The fund’s expense ratio is 1.2%. What is your rate of return on the fund if you sell your shares at the end of the year.

21

4.6 EXCHANGE-TRADED FUNDS

22

ETF allow investors to trade index portfolios like shares of stock Examples – SPDRs, Diamonds, and WEBS Potential advantages ◦ Trade continuously ◦ Lower taxes ◦ Lower costs Potential disadvantages ◦ mispricing ◦ broker fees

23

Table 4.3 EFT Sponsors and Products

24

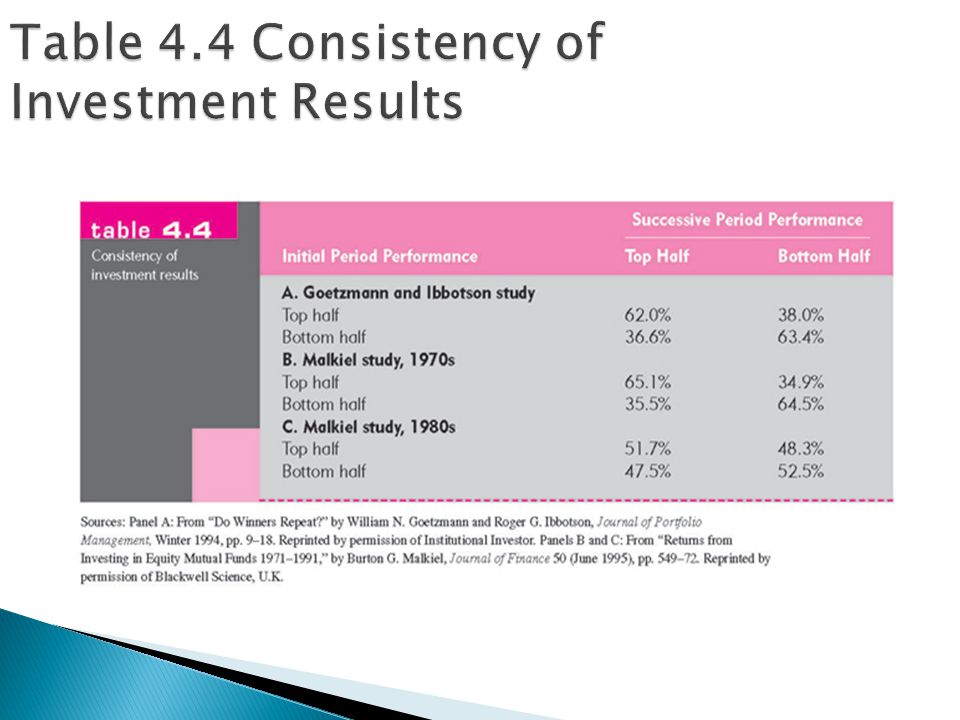

4.7 MUTUAL FUND INVESTMENT PERFORMANCE: A FIRST LOOK

25

Evidence shows that average mutual fund performance is generally less than broad market performance Evidence suggests that over certain horizons some persistence in positive performance ◦ Evidence is not conclusive ◦ Some inconsistencies

27

27

29

4.8 INFORMATION ON MUTUAL FUNDS

30

Wiesenberger’s Investment Companies Morningstar (www.morningstar.com)www.morningstar.com Yahoo (finance.yahoo.com/funds)finance.yahoo.com/funds Investment Company Institute Popular press Investment services

finance.yahoo.com/funds Investment Company Institute Popular press Investment services")

Similar presentations

>")