Download presentation

Presentation is loading. Please wait.

1

Alexander Reisz A Market-Based Framework for Bankruptcy Prediction Alexander S. Reisz Claudia Perlich Thursday, April 12, 2007 Third International Conference on Credit and Operational Risks HEC Montreal

2

Alexander Reisz Motivation According to Black & Scholes (1973)/Merton (1974), the equity of a corporation can be seen as a standard call option written on the assets of the firm with strike equal to face value of debt Put-Call parity: SH can also be seen as holding the firm and owing PV(F), but also having the (put) option to walk away, in effect selling the firm to BH for F, the face value of debt: C=V-PV(F)+P BH are long the assets of the firm, but are short a call option; alternatively, they are long riskless debt, but short a put option: V-C=PV(F)-P

/Merton (1974), the equity of a corporation can be seen as a standard call option written on the assets of the firm with strike equal to face value of debt Put-Call parity: SH can also be seen as holding the firm and owing PV(F), but also having the (put) option to walk away, in effect selling the firm to BH for F, the face value of debt: C=V-PV(F)+P BH are long the assets of the firm, but are short a call option; alternatively, they are long riskless debt, but short a put option: V-C=PV(F)-P")

3

Alexander Reisz The KMV Approach From the pricing equation, and Ito’s lemma,, derive MVA (V t ) and σ A –NB: F=CL+0.5*LTD Compute a distance-to-default (DD), equal to At this point, KMV departs from normality assumption and looks these DDs up in historical default tables For more on the topic, www.moodyskmv.comwww.moodyskmv.com

and σ A –NB: F=CL+0.5*LTD Compute a distance-to-default (DD), equal to At this point, KMV departs from normality assumption and looks these DDs up in historical default tables For more on the topic,")

4

Problems with the BSM Paradigm 1) Shareholder-aligned managers would therefore maximize the volatility of the firm’s assets (new investments) 2) which is positive for small d. Shareholder-aligned managers would therefore maximize the maturity of the firm’s debt 3) Underestimates the probability of bankruptcy overoptimistic credit rating

Underestimates the probability of bankruptcy overoptimistic credit rating.")

5

Alexander Reisz Our framework A (European) down-and-out barrier option is a contract that gives its holder the right, but not the obligation, to purchase an underlying asset at a prespecified price (strike) at a prespecified date (maturity), provided the underlying asset has not crossed a lower bound at any time before maturity V-DOC=PV(F)-P+DIC (the right to pull the plug) Choosing very volatile projects raises the probability to end up in-the-money (and the extent to which you are in- the-money), but also the probability to cross the (exogenous) bankruptcy barrier; C/ 0 leads to an interior solution (you may even end up with a John and Brito (2002) problem)

down-and-out barrier option is a contract that gives its holder the right, but not the obligation, to purchase an underlying asset at a prespecified price (strike) at a prespecified date (maturity), provided the underlying asset has not crossed a lower bound at any time before maturity V-DOC=PV(F)-P+DIC (the right to pull the plug) Choosing very volatile projects raises the probability to end up in-the-money (and the extent to which you are in- the-money), but also the probability to cross the (exogenous) bankruptcy barrier; C/ 0 leads to an interior solution (you may even end up with a John and Brito (2002) problem)")

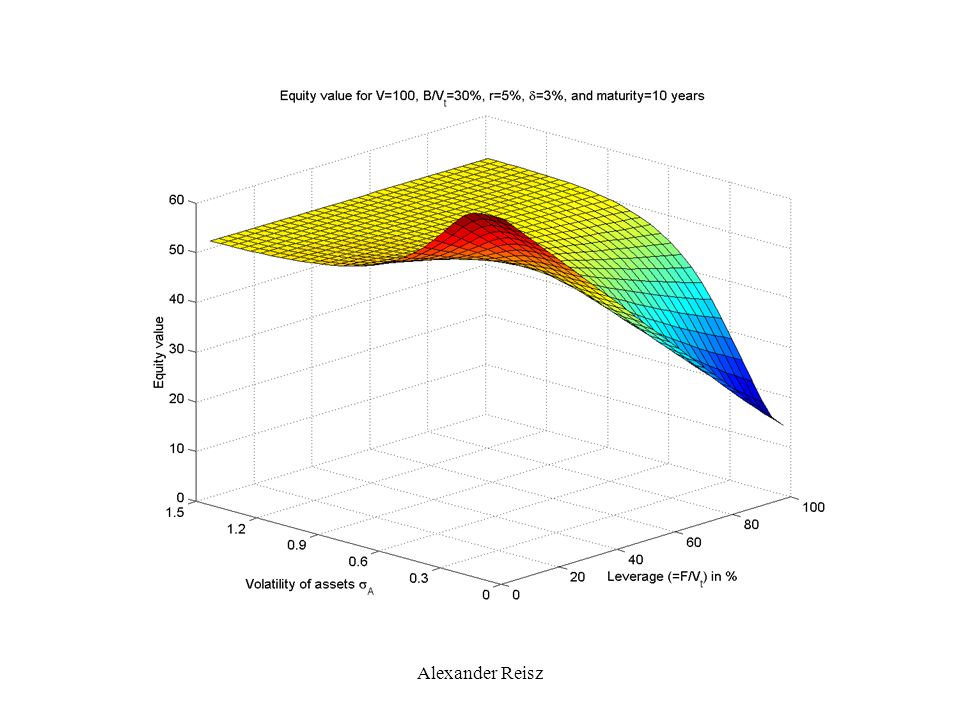

6

Alexander Reisz

9

Results Equity prices do reflect embedded barriers (on average, 30% of MVA) Better performance of predicted default probabilities than in the BSM or KMV frameworks, both in terms of discriminatory power (ranking) and in terms of calibration However, even in the barrier model, probabilities have to be recalibrated (no big deal); explains KMV’s modified strike price and departure from normality But our power (ranking accuracy) is achieved without departing from the model’s assumptions!

Better performance of predicted default probabilities than in the BSM or KMV frameworks, both in terms of discriminatory power (ranking) and in terms of calibration However, even in the barrier model, probabilities have to be recalibrated (no big deal); explains KMV’s modified strike price and departure from normality But our power (ranking accuracy) is achieved without departing from the model’s assumptions!")

10

Alexander Reisz Results (contd.) The Old Man ain’t dead yet: in one-year-ahead predictions, Altman (1968, 1993) scores outperform structural models! Combine accounting-based scores and PD’s from structural models in a logistic regression to achieve highest power.

11

Alexander Reisz Assumptions galore Exogenous bankruptcy bound B Markets are dynamically complete (existence of an MMA may not even be necessary) No bankruptcy costs, APR holds (no rebate) Constant interest rate

No bankruptcy costs, APR holds (no rebate) Constant interest rate")

12

Alexander Reisz Stock value (when F>B) with and See it as a standard BS option minus the ex-ante costs of the covenant Not increasing in for all other parameters

with and See it as a standard BS option minus the ex-ante costs of the covenant Not increasing in for all other parameters")

13

Alexander Reisz Brockman and Turtle (2003): a critique When you assume that MVA=BVD+MVE, you force B>F. Indeed, the barriers backed out by BT can be fairly well replicated by just solving DOC(V,F,B)=V-F for reasonable parameters (Wong and Choi, 2005) Although it is possible, it is suspicious when it holds for almost all firms (uniformly riskless corporate debt) Good luck in front of a court of law (maybe it works in Germany…) Contradicts KMV’s use of a strike price of CL+0.5*LTD<F; visitation and excursion times structural models; and Leland and Toft’s (1996) gamble for resurrection

=V-F for reasonable parameters (Wong and Choi, 2005) Although it is possible, it is suspicious when it holds for almost all firms (uniformly riskless corporate debt) Good luck in front of a court of law (maybe it works in Germany…) Contradicts KMV’s use of a strike price of CL+0.5*LTD<F; visitation and excursion times structural models; and Leland and Toft’s (1996) gamble for resurrection.")

14

Alexander Reisz Backing out V t, A, and B: a generalized market-based approach Start with 60,110 firm-years (1988-2002) Theory: A and B are constant for the life of the firm Empirically: Allow A and B to vary from year to year for a given firm (amount of liabilities varies anyway from year to year; trivially allows for variation in leverage ratios) However, force in a first step A and B to be constant over two consecutive years; the price and Ito equations for t-1 and t are solved for V t-1, V t, A and B Keep V t, A and B. V t-1, A and B for time t-1 will be estimated from equations for t-1 and t-2 (so as to avoid a hindsight bias) Left with 33,037 firm-years (5,784 unique firms)

Left with 33,037 firm-years (5,784 unique firms).")

15

Alexander Reisz Summary statistics

16

Alexander Reisz (Physical) probabilities of bankruptcy Early bankruptcy: Bankruptcy at maturity:

probabilities of bankruptcy Early bankruptcy: Bankruptcy at maturity:")

17

Alexander Reisz Total probability of bankruptcy First line: BS probability of assets ending up short of F, the promised repayment Second line denotes the increase in the probability of bankruptcy due to the possibility of early passage (well…almost) Allows one to stay within the model’s framework and fit B to a training sample

Allows one to stay within the model’s framework and fit B to a training sample")

18

Alexander Reisz

20

Evaluating the performance of probability estimates Accuracy does not reflect quality of probabilities: –No discrimination for extreme priors (a dumb model can achieve very high accuracy) –Equal penalty for prediction of 0.01 or 0.499 in case of default (although the latter is very large in credit risk): accuracy is not designed to judge continuous probabilities, but 0/1 predictions –But in credit risk, we are not interested in 0/1 predictions, but in a continuous variable (at what rate should we lend?) ; even more so the case because of asymmetry of costs (lending to Enron vs. denying credit to small businesses that would have deserved it)

.")

21

Alexander Reisz What we want An evaluation metric that reflects how well a model ranks firms (discriminatory power) –Did our model predict a larger PD for firms that actually defaulted? In particular, we want to know how many of the true defaults we catch for an arbitrary Type I error rate we are willing to tolerate A metric that reflects whether the predicted PD’s correspond to ex-post frequencies of default (calibration) –Pb: you need many “similar” firms to judge ex-post whether your average PD over a given group corresponds to the ex post true frequency of default for that group In general: recalibration is easy, more power is hard to achieve: favor the more powerful model

–Pb: you need many similar firms to judge ex-post whether your average PD over a given group corresponds to the ex post true frequency of default for that group In general: recalibration is easy, more power is hard to achieve: favor the more powerful model.")

22

Alexander Reisz Panel A: 1 Year ModelBSMKMVDOCAltman Z- score Altman Z’’- score Number of Observations 25,582 22,462 Prior Survival Rate 0.9930 0.9944 Area Under ROC 0.71700.74780.7636 †‡ 0.7794 * 0.7769 Accuracy (Concordance) 0.97380.92440.9903NA Log-likelihood -9,819.17-5,483.97-4,486.29NA Panel B: 3 Year Number of Observations 18,216 15,892 Prior Survival Rate 0.9515 0.9555 Area Under ROC0.73690.75970.7625 †* 0.68900.7279 Accuracy (Concordance) 0.90630.85420.9092NA Log-likelihood-11,804.74-10,090.4-9,200.75NA Significant differences in AUC between DOC and BSM are identified by †, between DOC and KMV by ‡, and between DOC and the better of the two Altman scores by * (the symbol is entered next to the AUC of the dominating model).

NA Log-likelihood -9, , ,486.29NA Panel B: 3 Year Number of Observations 18,216 15,892 Prior Survival Rate Area Under ROC †* Accuracy (Concordance) NA Log-likelihood-11, , ,200.75NA Significant differences in AUC between DOC and BSM are identified by †, between DOC and KMV by ‡, and between DOC and the better of the two Altman scores by * (the symbol is entered next to the AUC of the dominating model).")

23

Alexander Reisz

24

Need to recalibrate!

25

Alexander Reisz Panel A: 1 Year; estimation period: 1988-1999; evaluation period: 2000-2001 ModelBSMKMVDOCAltman Z-scoreAltman Z’’-score In-sample recalibration Number of Observations 25,582 22,462 Prior Survival Rate 0.9930 0.9944 Area Under ROC 0.71700.74780.7636 †‡ 0.7794 * 0.7769 Accuracy (Concordance) 0.9930 0.99420.9943 Log-likelihood-2,033.54-2,006.28-1,992.04-1,431.87-1,461.10 Average Log-likelihood -0.0795-0.0784-0.0779-0.0637-0.0650 Out-of-sample recalibration Number of Observations 2,761 2,456 Prior Survival Rate 0.9931 0.9939 Area Under ROC 0.73080.76530.7865 †‡ 0.8063 * 0.7268 Accuracy (Concordance) 0.9931 0.99270.9935 Log-likelihood-215.88-211.03-208.77-174.51-177.81 Average Log-likelihood -0.0782-0.0764-0.0756-0.0711-0.0724 Significant differences in AUC between DOC and BSM are identified by †, between DOC and KMV by ‡, and between DOC and the better of the two Altman scores by * (the symbol is entered next to the AUC of the dominating model).

Log-likelihood-2, , , , , Average Log-likelihood Out-of-sample recalibration Number of Observations 2,761 2,456 Prior Survival Rate Area Under ROC †‡ * Accuracy (Concordance) Log-likelihood Average Log-likelihood Significant differences in AUC between DOC and BSM are identified by †, between DOC and KMV by ‡, and between DOC and the better of the two Altman scores by * (the symbol is entered next to the AUC of the dominating model).")

26

Alexander Reisz The picture KMV does not want you to see From Saunders and Allen (2002)

")

27

Alexander Reisz Panel B: 3 Year; estimation period: 1988-1997; evaluation period: 1998-1999 In-sample recalibration Number of Observations 18,216 15,892 Prior Survival Rate 0.9515 0.9555 Area Under ROC 0.73690.75970.7625 †* 0.68900.7279 Accuracy (Concordance) 0.9515 0.95540.9550 Log-likelihood-6,513.08-6,437.45-6,421.25-5,617.30-5,493.12 Average Log-likelihood -0.3575-0.3534-0.3525-0.3534-0.3457 Out-of-sample recalibration Number of Observations 2,592 2,267 Prior Survival Rate 0.9117 0.9153 Area Under ROC 0.73800.76640.7795 †* 0.70550.6997 Accuracy (Concordance) 0.9117 0.91620.9127 Log-likelihood-1491.61-1,468.16-1,444.00-1,361.07-1,385.83 Average Log-likelihood -0.5755-0.5664-0.5571-0.6004-0.6113 Significant differences in AUC between DOC and BSM are identified by †, between DOC and KMV by ‡, and between DOC and the better of the two Altman scores by * (the symbol is entered next to the AUC of the dominating model).

Log-likelihood-6, , , , , Average Log-likelihood Out-of-sample recalibration Number of Observations 2,592 2,267 Prior Survival Rate Area Under ROC †* Accuracy (Concordance) Log-likelihood , , , , Average Log-likelihood Significant differences in AUC between DOC and BSM are identified by †, between DOC and KMV by ‡, and between DOC and the better of the two Altman scores by * (the symbol is entered next to the AUC of the dominating model).")

28

Alexander Reisz Future research I: Fitting better models Debt structures form a PF of American (outside; compound) barrier options Debt covenants may specify that a certain time has to be spent consecutively (cumulatively) below the bankruptcy barrier (excursion (visitation) time): Parisian (Parasian) options Allow for severity of excursion to play a role as well: Galai, Wiener, and Raviv (2005) General problem: backing out a parameter when only numerical pricing is available

barrier options Debt covenants may specify that a certain time has to be spent consecutively (cumulatively) below the bankruptcy barrier (excursion (visitation) time): Parisian (Parasian) options Allow for severity of excursion to play a role as well: Galai, Wiener, and Raviv (2005) General problem: backing out a parameter when only numerical pricing is available")

29

Alexander Reisz Future research II: let’s be realistic Force in a first step A and B to be constant over three consecutive years; the price and Ito equations for t-2, t-1 and t are solved for V t-2, V t-1, V t, A, B and R, the option rebate Provides a new estimate of violations of the APR rule on the shareholders’ side Estimate bond prices using both early bankruptcy and bankruptcy at maturity; in both cases, LGD is given endogenously by the model Alternatively, use the recalibrated total PD’s to estimate equilibrium bond yields on new issues.

30

Alexander Reisz

Similar presentations

: Pays a premium upfront Gets to “call.>")

?>")