Download presentation

Presentation is loading. Please wait.

1

Treasury bond futures: pricing and applications for hedgers, speculators, and arbitrageurs Galen Burghardt Taifex/Taiwan 7 June 2004

2

Part I: Contract structure and pricing Futures contract specifications Deliverable Treasury issues Pricing Treasury futures relative to deliverable cash bonds Components of the basis The short’s delivery options Fair value of a futures contract

3

Overview of Treasury futures Key contract specifications Supplies of deliverable Treasury bonds and notes Shifts in trading and open interest

4

Key contract specifications

5

Trading days and hours

6

Deliverable Treasury bonds

7

Deliverable Treasury 10-year notes

8

Shifts in trading and open interest

9

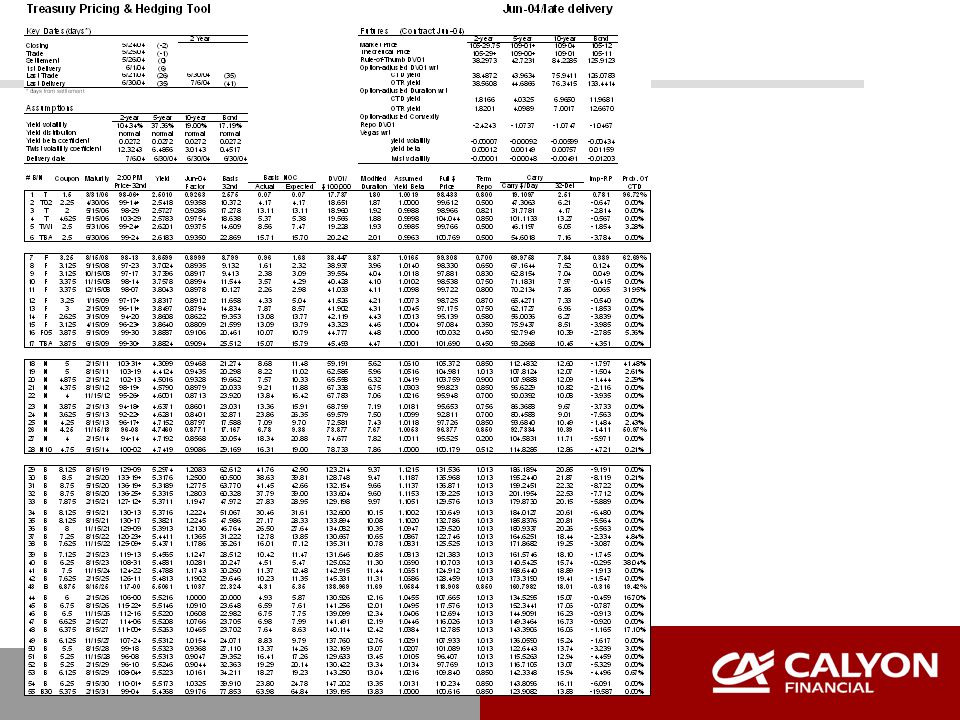

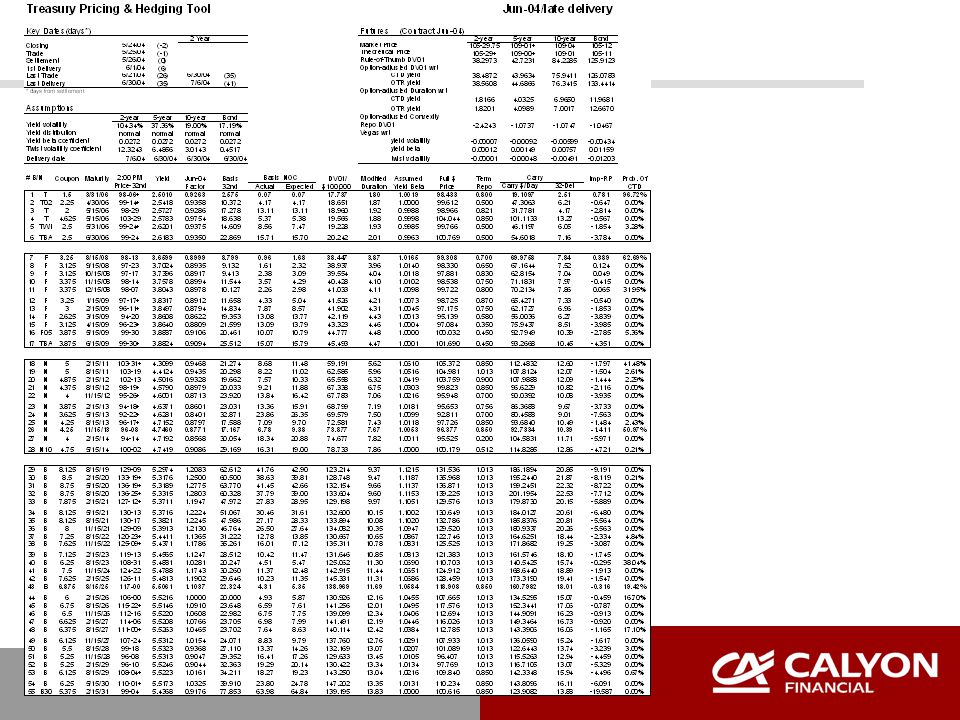

Pricing Treasury futures Identifying the cheapest to deliver The short’s delivery options Pricing and hedging tool

11

Calculating an implied RP (repo) rate (1) Buy the 8.125s of 8/15/19 in the cash market (settle 5/26/04) Spot price = 129-09 ( or 129.2813) Accrued interest at settlement = (8.125/2)x(101/182) = 2.2545 Full price = 131.5357 [ = 129.2813 + 2.2545 ] Deliver the bond on 6/30/04 at today’s futures price Futures price = 105-12 (105.3750) June ‘04 conversion factor = 1.2083 Converted futures price = 127.3246 [ = 1.2083 x 105.3750 ] Accrued interest at futures delivery = (8.125/2)x(136/182) = 3.0357 Futures invoice price = 130.3603 [ = 127.3246 + 3.0357 ]

![Calculating an implied RP (repo) rate (1) Buy the 8.125s of 8/15/19 in the cash market (settle 5/26/04) Spot price = ( or ) Accrued interest at settlement = (8.125/2)x(101/182) = Full price = [ = ] Deliver the bond on 6/30/04 at today’s futures price Futures price = ( ) June ‘04 conversion factor = Converted futures price = [ = x ] Accrued interest at futures delivery = (8.125/2)x(136/182) = Futures invoice price = [ = ]](http://images.slideplayer.com/14/4185112/slides/slide_11.jpg "Calculating an implied RP (repo) rate (1) Buy the 8.125s of 8/15/19 in the cash market (settle 5/26/04) Spot price = ( or ) Accrued interest at settlement = (8.125/2)x(101/182) = Full price = [ = ] Deliver the bond on 6/30/04 at today’s futures price Futures price = ( ) June ‘04 conversion factor = Converted futures price = [ = x ] Accrued interest at futures delivery = (8.125/2)x(136/182) = Futures invoice price = [ = ]")

12

Calculating an implied RP (repo) rate (2) Calculate the rate of return Implied repo rate = ((130.3603/131.5357)-1)x(360/35) = 0.09191 (or -9.191%) Note: This implied return is expressed as a money market rate using an actual/360 money market day-count convention.

rate (2) Calculate the rate of return Implied repo rate = (( / )-1)x(360/35) = (or %) Note: This implied return is expressed as a money market rate using an actual/360 money market day-count convention.")

13

Identifying the cheapest to deliver As a rule, the issue with the highest implied RP (repo) rate is identified as the cheapest to deliver As a better rule, the issue with the smallest difference between its own term repo rate and its implied repo is the cheapest to deliver

rate is identified as the cheapest to deliver As a better rule, the issue with the smallest difference between its own term repo rate and its implied repo is the cheapest to deliver")

14

Basis concepts Definition What drives the basis Changes in the cheapest to deliver Fair value of a futures contract

15

Basis defined Basis = Spot price - (Conversion factor x Futures price) Example of 6.875s of 8/15/25 Spot price = 117-00 (or 117.0000) June ‘04 Factor = 1.1037 June ‘04 futures price = 105-12 (or 105.3750) Basis = 117.0000 - 1.1037 x 105.3750 = 117.0000 - 116.3024 = 0.6976 or 23.32/32nds [ = 0.6976 x 32 ]

![Basis defined Basis = Spot price - (Conversion factor x Futures price) Example of 6.875s of 8/15/25 Spot price = (or ) June ‘04 Factor = June ‘04 futures price = (or ) Basis = x = = or 23.32/32nds [ = x 32 ]](http://images.slideplayer.com/14/4185112/slides/slide_15.jpg "Basis defined Basis = Spot price - (Conversion factor x Futures price) Example of 6.875s of 8/15/25 Spot price = (or ) June ‘04 Factor = June ‘04 futures price = (or ) Basis = x = = or 23.32/32nds [ = x 32 ]")

16

What drives the basis?

17

How carry is calculated Example of 6.875s of 8/15/25 on 5/25/04 (to settle 5/26/04) Spot price = 117-00 (117.000) Accrued interest = (6.875/2) x (101/182) = 1.9076 where 101 is actual days from 2/15/04 to 5/26/04) and 182 is actual days from 2/15/04 to 8/15/04 Full price = 118.9076 [ = 117.0000 + 1.9076 ] Coupon income = (6.875/2) x ( 35/182) = 0.6611 Financing expense = 118.9076 x.00850 x (35/360) = 0.0983 Carry = Coupon income - Financing expense = 0.6611 - 0.0983 = 0.5628 Carry = 18.01/32nds [ = 0.5628 x 32 ]

![How carry is calculated Example of 6.875s of 8/15/25 on 5/25/04 (to settle 5/26/04) Spot price = ( ) Accrued interest = (6.875/2) x (101/182) = where 101 is actual days from 2/15/04 to 5/26/04) and 182 is actual days from 2/15/04 to 8/15/04 Full price = [ = ] Coupon income = (6.875/2) x ( 35/182) = Financing expense = x x (35/360) = Carry = Coupon income - Financing expense = = Carry = 18.01/32nds [ = x 32 ]](http://images.slideplayer.com/14/4185112/slides/slide_17.jpg "How carry is calculated Example of 6.875s of 8/15/25 on 5/25/04 (to settle 5/26/04) Spot price = ( ) Accrued interest = (6.875/2) x (101/182) = where 101 is actual days from 2/15/04 to 5/26/04) and 182 is actual days from 2/15/04 to 8/15/04 Full price = [ = ] Coupon income = (6.875/2) x ( 35/182) = Financing expense = x x (35/360) = Carry = Coupon income - Financing expense = = Carry = 18.01/32nds [ = x 32 ]")

18

Shifts in the cheapest to deliver

24

Futures are fairly priced if expected basis net of carry equals actual basis net of carry Futures are rich if expected basis net of carry exceeds actual basis net of carry (that is, if the basis is cheap) Futures are cheap if expected basis net of carry is less than actual basis net of carry (and the basis is rich)

Futures are cheap if expected basis net of carry is less than actual basis net of carry (and the basis is rich)")

25

Part II: Applications Hedging Basis trading Speculation (duration management) Curve trading Synthetic asset construction Volatility arbitrage

Curve trading Synthetic asset construction Volatility arbitrage")

26

Hedging Finding the option-adjusted value of a basis point Measuring “stub” risk (repo exposure) Yield betas

Yield betas")

28

Option-adjusted DV01s

29

Hedging example Hedge $100 million of the 5.375s of 2/15/31 (on-the-run) DV01/$100,000 = $139.195 Position DV01 = $100,000,000 x ($139.195/$100,000) = $139,195 Option-adjusted futures DV01 = $126.078 For parallel shifts in the yield curve, Hedge ratio = $139,195 / $126.078 = 1,104 contracts

DV01/$100,000 = $ Position DV01 = $100,000,000 x ($ /$100,000) = $139,195 Option-adjusted futures DV01 = $ For parallel shifts in the yield curve, Hedge ratio = $139,195 / $ = 1,104 contracts")

31

Hedging example using yield betas Hedge $100 million of the 5.375s of 2/15/31 (on-the-run) DV01/$100,000 = $139.195 Position DV01 = $100,000,000 x ($139.195/$100,000) = $139,195 Option-adjusted futures DV01 = $126.078 Yield betas 1.0000 (for 5.375s) 1.0584 (for the cheapest to deliver) Hedge ratio = ($139,195 / $126.078) x (1.0000/1.0584) = 1,043 contracts

DV01/$100,000 = $ Position DV01 = $100,000,000 x ($ /$100,000) = $139,195 Option-adjusted futures DV01 = $ Yield betas (for 5.375s) (for the cheapest to deliver) Hedge ratio = ($139,195 / $ ) x (1.0000/1.0584) = 1,043 contracts")

32

Other ways to think about hedging Duration adjustment Interest rate immunization Asset allocation

33

Duration adjustment Hedging, as usually described, is simply a way to reduce net duration to zero Speculating, on the other hand, is a matter of choosing a target duration to take advantage of a view on the level of interest rates.

34

Option-adjusted DV01s

35

Duration adjustment (example) Problem: You have a $200 million portfolio of 10-year notes with a duration of 7 and want to reduce the portfolio’s duration to 5. Solution: Find the number of futures, N, that sets ($200,000,000 x.07 + N x $109,031.25 x.07)/$200,000,000 equal to.05. Solving, we find N = -524 (rounded). Shorting 524 futures, each with a portfolio equivalent value of $109,031.25 and an option-adjusted duration of.07 would be like shorting, fully leveraged, a note portfolio of $57,132,375 with a duration of.07.

/$200,000,000 equal to.05. Solving, we find N = -524 (rounded). Shorting 524 futures, each with a portfolio equivalent value of $109, and an option-adjusted duration of.07 would be like shorting, fully leveraged, a note portfolio of $57,132,375 with a duration of.07..")

36

Immunization Duration is a concept that is defined for parallel shifts in the yield curve. Immunization is an approach to hedging that provides protection against non-parallel shifts in the yield curve

38

Immunization with futures On 5/26/04, CTD Treasury issues had maturities of 3/31/06(2-year) 8/15/08(5-year) 11/15/13(10-year) 8/15/25(bond) To “immunize” the portfolio from a complex change in yields, determine the partial sensitivity of your portfolio to changes in each of these yields and hedge accordingly. (Other terms are buckets, key rates, and factors.)

.")

39

Asset allocation Futures are excellent tools for changing your macro asset mix without disturbing the real underlying portfolio. For example, one could buy bond futures and sell equity futures as a way of increasing a portfolio’s exposure to bonds and decreasing its net exposure to equity prices. Advantages? –Lower transactions costs –Preserving or transporting alpha

40

Futures hedges are imperfect Futures hedges will make or lose money because of unexpected changes : the short’s delivery option value (due to changes in cheapest to deliver or changes in yield volatility) term repo rates the slope of the deliverable yield curve

term repo rates the slope of the deliverable yield curve")

41

Basis trades Definition of a long basis trade You are long the basis if, for every $100,000 par amount of a bond (or note) that you are long you are short a number of futures equal to the bond’s conversion factor Example of $100 million of the 6.875s of 8/15/25 June ‘04 factor = 1.1037 Buy $100 million of the 6.875s at 117-00 Sell 1,104 [ = $100,000,000 x (1.1037/$100,000) ] June ‘04 futures You are long the basis at 22.32/32nds

![Basis trades Definition of a long basis trade You are long the basis if, for every $100,000 par amount of a bond (or note) that you are long you are short a number of futures equal to the bond’s conversion factor Example of $100 million of the 6.875s of 8/15/25 June ‘04 factor = Buy $100 million of the 6.875s at Sell 1,104 [ = $100,000,000 x (1.1037/$100,000) ] June ‘04 futures You are long the basis at 22.32/32nds](http://images.slideplayer.com/14/4185112/slides/slide_41.jpg "Basis trades Definition of a long basis trade You are long the basis if, for every $100,000 par amount of a bond (or note) that you are long you are short a number of futures equal to the bond’s conversion factor Example of $100 million of the 6.875s of 8/15/25 June ‘04 factor = Buy $100 million of the 6.875s at Sell 1,104 [ = $100,000,000 x (1.1037/$100,000) ] June ‘04 futures You are long the basis at 22.32/32nds")

42

P/L of a basis trade A basis trade has four components Change in the price of the cash bond Change in the futures price Coupon income Financing (repo) expense By construction, the combined effect of price changes will equal the change in the basis (times the value of a 32nd). For example, each 32nd on a $100 million basis position is worth $31,250.

43

Why trade the basis Convergence (sale of delivery options) Yield volatility Changes in the slope of the yield curve Superior financing position Mispriced basis Changes in term repo rates

Yield volatility Changes in the slope of the yield curve Superior financing position Mispriced basis Changes in term repo rates")

44

Changes in yield levels and spreads

45

Changes in the cheapest to deliver

46

Net basis of the 5s of 2/11

47

Speculating with Treasury futures The P/L of a cash bond trade has three components Change in the price of the bond Coupon income Financing (repo) expense The P/L of a futures trade has only one component Change in the futures price Note of caution: An appropriate comparison of the two strategies requires a complete accounting for all sources of gain or loss

expense The P/L of a futures trade has only one component Change in the futures price Note of caution: An appropriate comparison of the two strategies requires a complete accounting for all sources of gain or loss")

48

Curve trading You can trade the slope of the curve using the basis as your trading vehicle You can trade the slope of the curve using combinations of 2s, 5s, 10s, and bonds

49

Unweighted and weighted NOB spreads An unweighted long NOB spread (10-year notes versus Bonds) would be long one 10-year note contract and short one bond contract Chief advantage is a simple P/L structure. As the price spread widens, you make money. As the price spread narrows, you lose money. Chief drawback is its exposure to a change in the slope of the yield curve. With a long unweighted NOB spread, you would profit from a parallel downward shift in the yield curve, but lose from a parallel upward shift in yields.

50

Option-adjusted DV01s

51

Constructing a weighted NOB spread Futures DV01s 10-year note futures -- $75.94 Bond futures -- $126.08 Trade ratio Buy 1.66 [ = $126.08 / $75.94 ] 10-year futures for each bond contract you sell. The resulting trade is duration or DV01 neutral

![Constructing a weighted NOB spread Futures DV01s 10-year note futures -- $75.94 Bond futures -- $ Trade ratio Buy 1.66 [ = $ / $75.94 ] 10-year futures for each bond contract you sell.](http://images.slideplayer.com/14/4185112/slides/slide_51.jpg "The resulting trade is duration or DV01 neutral.")

52

5 and 10-year yields and yield spreads

53

10-year less 5-year yield spread

54

Cumulative P/Ls

55

Characteristics of real bonds Wealth Yield exposure Credit spread exposure Other (covenants, taxes, safekeeping, etc.)

")

56

Constructing synthetic bonds To create a synthetic Treasury, combine: –Term cash –Duration equivalent futures position To create a synthetic corporate, add: –Credit derivative

57

Experience with selling the 10-year basis

58

Most profitable example

59

Least profitable example

60

Yield enhancement trades come and go Mispricings in futures can last several years Opportunities to do yield enhancement migrate from market to market –Bond futures in the late 80s –Treasury note (both 5s and 10s) and bund futures in the early 90s –10-year futures in the early 00s

and bund futures in the early 90s –10-year futures in the early 00s")

61

Volatility arbitrage If implied yield volatility in the basis market is low relative to implied volatility in the outright options market, buy the basis and sell a collection of real options

62

Sell a straddle against this position choosing a strike price that corresponds to a forward yield approximately 6.7 basis points higher than the current level of forward yields

63

Roll of money market futures Term repo rates play a large role in the success of hedges and basis trades Short-term money market futures can be very useful in reducing term financing risk In the U.S., Fed funds futures traded at the CBOT provide an excellent hedge for term repo risk

Similar presentations

slope increases (long term R increases more than short term or short term even decreases) buy notes sell bonds.>")