Download presentation

Presentation is loading. Please wait.

1

PPACA February 2015

2

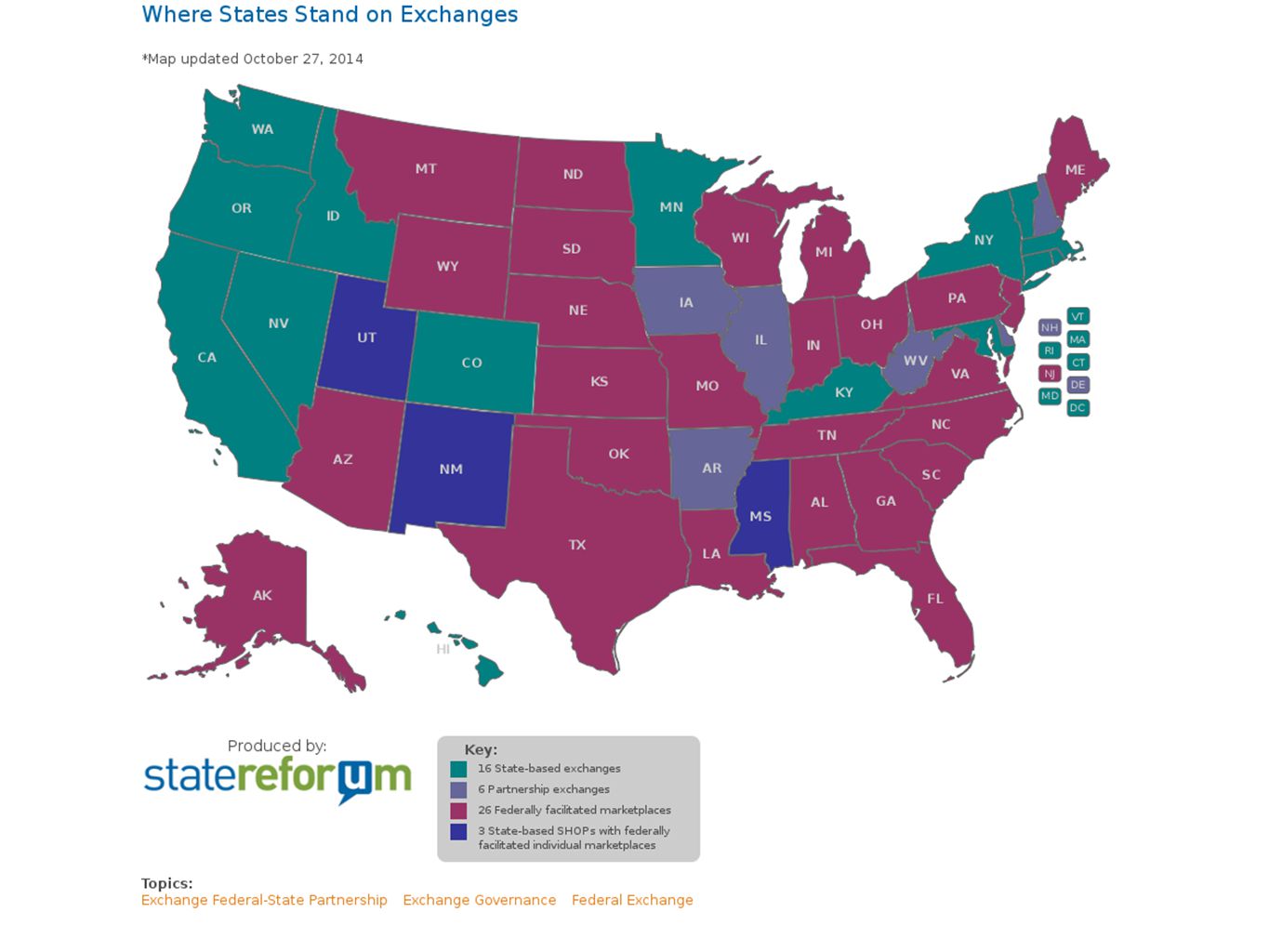

SSA.gov The cost of adequate private health insurance, if paid for in old age, is more than most older persons can afford. Prior to Medicare, only a little over one-half of those aged 65 and over had some type of hospital insurance ; few among the insured group had insurance covering any part of their surgical and out-of-hospital physicians' costs. Also, there were numerous instances where private insurance companies were terminating health policies for aged persons in the high risk category. Many thousands of carefully arrived at decisions were made and incorporated in the more than 50 pages of enacted legislation crammed full with detailed provisions for putting the ideas behind health insurance into effect. Medicare Established 1965 SenateYeaNayNot Voting D5774 R13172 HouseYeaNayNot Voting D237488 R70682 Medicare Vote

3

PPACA Established 2010 SenateYeaNayNot Voting D & I6000 R0391 HouseYeaNayNot Voting D219340 R01782 PPACA Vote

4

PPACA Individual Mandate Employer Shared Responsibility COVER MORE PEOPLE

6

June 2012 PPACA - Constitutional? It is a tax!

7

June 2012 Medicaid expansion

8

March 2015 Premium Subsidies for Federal Exchanges?

11

To Repeal PPACA February 2015

12

Religious objections held by certain For-Profit, "closely held" employers were legally legitimate. 2014 SCOTUS ruling

13

Changes to PPACA? Full Time Employee Definition From 30 hours to 40 hours? Cadillac Tax Change to regional threshold amounts? Increase amounts?

15

$10,200 $27,500 $10,200 $27,500 $10,200 $27,500 $10,200 $27,500 $10,200 $27,500 $10,200 $27,500 $10,200 $27,500 $10,200 $27,500 $10,200 $27,500 $10,200 $27,500 $10,200 $27,500 $10,200 $27,500

16

High Cost Employer-Sponsored Health Coverage Excise Tax SAMPLE SCHOOL DISTRICT PROJECTED 2018 GROSS PREMIUM = $7,220,260 ADDITIONAL CADILLAC TAX = $550,886 7.6% INCREASE IN ADDITION TO THE RENEWAL ASSUMES ALL EMPLOYEES ARE ON LEVEL 4 OF THE CHAPTER 78 SCHEDULE: $550,886 BOE EMPLOYEES $440,709$110,177

17

Collective Bargaining Timing of C.N.A. and Cadillac Tax What will your position be? Calculate exposure

18

AFFORDABLE? PCORI2012 - 2019 Now at $2.08 per body per year – P.Y. 10/1/14, then adjusted for inflation Trans. Reins.2014 - 2016 2014:$63 per body per year 2015:$44 per body per year 2016: $27 per body per year Health Insurer Fee*2014 – no end date 2014: Approx. 2.5% of premium 2015: Approx. 3.0% of premium 2016: Expected to grow * Only applies to fully insured plans

19

Full Time Employee Tracking

20

Record Keeping & Reporting Report in 2016 for 2015 IRS – use information to enforce mandates: Employer Employee Complex Integration of data from multiple sources: Payroll and other Need to address NOW – vendor? 1094-B 1095-B 1094-C 1095-C

21

We've completed a few returns with dealing with the premium tax credit (Form 8962). My question is how to treat the premium tax credit amount due and refund as to a medical deduction??? We're assuming the amount due (excess advance premium tax repayment) would be a deduction for 2015 and a refund (net premium tax credit) would just lower the deduction for 2015. I did a search online and looked at the instructions for Form 8962 and couldn't find anything in writing. NJSCPA Member Open Forum

would be a deduction for 2015 and a refund (net premium tax credit) would just lower the deduction for I did a search online and looked at the instructions for Form 8962 and couldn t find anything in writing. NJSCPA Member Open Forum.")

22

Min. Value? Affordable? To Substantially All Full Time EEs? MEC? Medium ER? Large ER?

23

70%

24

95%

25

Individual Mandate Employer Mandate Phase-In Employer Mandate Final Record Keeping & Reporting for 2015 Transitional Reinsurance Discontinued Cadillac Tax 20142015201620172018 Timeline

26

Change is INEVITABLE. Progress is OPTIONAL. -Tony Robbins

27

PPACA & The Employer Mandate: 46 Changes and Counting…

28

Employer Mandate is Finally Here! After nearly five years of PPACA, effective Jan 1 st of this year the long-awaited, twice-delayed, Employer Mandate became effective: Employers with 100+ FTE’s must offer health insurance that is both “Affordable” and of “Minimum Value” to at least 70% of their full-time employees, and their children up to age 26, or be subject to penalties. *Employers with plan years starting on a date (7-1) other than January 1 st must begin compliance at the start of their plan year.

other than January 1 st must begin compliance at the start of their plan year..")

29

“Pay or Play” Definitions Applicable Large Employer (ALE): On average at least 50 FT’s/FTE’s during the prior calendar year. Full-Time Employees (FT): Any employee working an average of 30 hours or more a week, or 130 hours or more per month. Full-Time Equivalent (FTE): Total hours worked by Part-Time employees, per month, divided by 120. *FT’s and FTE’s combined are used for purposes of determining if ALE.

: Any employee working an average of 30 hours or more a week, or 130 hours or more per month. Full-Time Equivalent (FTE): Total hours worked by Part-Time employees, per month, divided by 120. *FT’s and FTE’s combined are used for purposes of determining if ALE..")

30

“Pay or Play” Definitions (Cont’d) Affordable: Employee contribution towards single coverage in your least expensive plan must be no greater than 9.5% of their W2 wages. Minimum Value: Plan must cover at least 60% of allowed charges for covered services.

31

Employer Mandate Delays Originally set for 1-1-14 effective date. Finally began in 2015 for Employers with 100+ FTE’s. In 2016, all Employers w/ 50+ FTE’s (“Applicable Large Employers”) must offer coverage to at least 95% of FT employees.

must offer coverage to at least 95% of FT employees..")

32

“Pay or Play” Timeline PPACA Signed Into Law Original Employer Mandate Revised Employer Mandate Revised “Medium Sized” ER Mandate 3-23-101-1-141-1-151-1-16 ALE- Must provide affordable, minimum value coverage to at least 95% of FT EE’s -ER w/ 100+ FTE’s must offer coverage to at least 70% of FT’s (Increases to 95% in 2016) -All ALE’s (50+ FTE’s) must offer coverage to at least 95% FT’s

-All ALE’s (50+ FTE’s) must offer coverage to at least 95% FT’s")

33

Identifying Your Plan Year For School Boards (where Form 5500 filing is not required) the plan year is the policy year, presuming that the plan is administered based on that policy year. However, if the policy renews on July 1st but the plan is administered with open enrollment changes effective on Jan 1 st, HHS might consider your plan year to be calendar year. Additionally, to be considered a non-calendar plan year (Ex: 7-1), you must have maintained that non-calendar plan year since 12-27-12.

, you must have maintained that non-calendar plan year since")

34

“SledgeHammer Penalty” If Board fails to offer Minimum Essential Coverage (MEC) to 95% or more of its Full-Time Employees and their dependent children to age 26 (coverage for spouse not required) To Incur the Penalty: -FTE must a) go to the Exchange, and b) obtain a federal subsidy, and c) actually purchase coverage. Actual Penalty would then be $2,000 per FTE, (minus the first 30) *Estimated Annualized Penalty : 626 FTE – 30 = 596 FTE x $2,000 = $1,192,000 (Penalty assessed monthly every applicable month you are not in compliance.) “SledgeHammer Penalty” If a Board with 100+ FTE’s fails to offer coverage to at least 70% or more of its FT employees and their dependent children to age 26 (coverage for spouse not required), penalty occurs only if: 1)FT employee goes to the Exchange, and… 2)Obtains a federal subsidy, and… 3)Actually purchases coverage. Penalty incurred would then be $2,000 per FT employee, (minus the first 80 employees for 2015, minus the first 30 employees for 2016 and beyond) *Example: 500 FT – 80 = 420 FT x $2,000 = $840,000 (Penalty assessed monthly every applicable month not in compliance.)

*Estimated Annualized Penalty : 626 FTE – 30 = 596 FTE x $2,000 = $1,192,000 (Penalty assessed monthly every applicable month you are not in compliance.) SledgeHammer Penalty If a Board with 100+ FTE’s fails to offer coverage to at least 70% or more of its FT employees and their dependent children to age 26 (coverage for spouse not required), penalty occurs only if: 1)FT employee goes to the Exchange, and… 2)Obtains a federal subsidy, and… 3)Actually purchases coverage. Penalty incurred would then be $2,000 per FT employee, (minus the first 80 employees for 2015, minus the first 30 employees for 2016 and beyond) *Example: 500 FT – 80 = 420 FT x $2,000 = $840,000 (Penalty assessed monthly every applicable month not in compliance.).")

35

“Pick-Axe Penalty” Board offers at least 70% of FT employees coverage but may still be subject to $3,000 penalty if any of the following occurs: a)Board does not offer at least one plan that is considered “Affordable” and meets the “Minimum Value” standard, and/or b)FT employee was one of the 30% not offered coverage by the Board. If a or b happens and FT employee obtains subsidized coverage through an Exchange, Board pays $3,000 for each applicable employee. *Penalty only applies for those employees obtaining subsidized coverage through an Exchange.

37

The Road Ahead Supreme Court Case “King vs. Burrell” PPACA has language stating tax credits (subsidies) can only be given to those that enroll in the State-run exchanges (13 states presently). This means that roughly ¾ of the approximate 11.4 million individuals who have signed up for individual coverage through an exchange might be deemed not eligible for a subsidy. 87% of those enrolled thus far have been eligible for subsidies of some sort. If Supreme Court upholds language over 7.4 million will be SOL.

can only be given to those that enroll in the State-run exchanges (13 states presently). This means that roughly ¾ of the approximate 11.4 million individuals who have signed up for individual coverage through an exchange might be deemed not eligible for a subsidy. 87% of those enrolled thus far have been eligible for subsidies of some sort. If Supreme Court upholds language over 7.4 million will be SOL..")

38

The Ripple Effect Both types of ER mandates are triggered only when an EE enrolls for coverage in an exchange plan and receives a premium tax credit or cost-sharing reduction. If no premium tax subsidies are payable in those states, the ER mandate penalties will never be triggered in those states. There would, therefore, be no penalty for violating the employer coverage mandate in those states. *Case is set to begin next week (3/3/15) and a decision is expected by June.

and a decision is expected by June..")

39

Save American Workers Act of 2015 Passed in the House and awaiting Senate vote, would change the definition of “full-time” employee to 40 hours per week vs. 30. Proponents say it will ease employer expense to cover such employees. Exponents say it will result in more employees being forced to work more hours and still not be eligible for insurance. Stay Tuned…

40

Issuing a Combat Order B egin the planning A rrange reconnaissance M ake reconnaissance C omplete the order I ssue the order S upervise

41

AVOIDING the PENALTIES O bey the statutory requirements. H ave your broker/consultant pave a clear path to compliance. S top thinking “It’s not really going to happen.” H ope for the best, but plan for the worst. If all else fails…

43

AVOIDING the PENALTIES O bey the statutory requirements. H ave your broker/consultant pave a clear path to compliance. S top thinking “It’s not really going to happen.” H ope for the best, but plan for the worst. And if all else fails… I nsist to the IRS that you simply “mis-remember” ever hearing about this PPACA thing.

44

AVOIDING the PENALTIES O bey the statutory requirements. H ave your broker/consultant pave a clear path to compliance. S top thinking “It’s not really going to happen.” H ope for the best, but plan for the worst. And if all else fails… I nsist to the IRS that you simply “mis-remember” ever hearing about this PPACA thing. T hank you for joining us today! ;-)

.")

45

Measuring Employees Hours 45

46

WHY do we have to measure? The Employer Mandate requires that you offer coverage to substantially ALL employees working an average of 30+ hours The law is complicated. You most likely have employees that would be considered FT under the Employer Mandate... That you don’t know about! The government needs to collect this information in order to know whether or not you are compliant 46

47

WHAT do we have to measure? An employees hours of service include: Each hour the EE is paid or entitled to payment when no work is performed Each hour during which no duties are performed due to vacation, holiday, illness, incapacity, layoff, jury duty or leave of absence There is no limit on the number of hours counted for a paid leave of absence 47

48

What about Summer? 48 1. What did the employee’s hours average during the school year? 2. Use that. Example. Teacher works 36 hours/week on average. Each summer week credit them as though they worked 36 hours

49

WHEN do we have to measure? You should be measuring a YEAR OR MORE in advance of when you need to be compliant with the law. 49 Example. BOE with 100+ FTEs and effective date of 7/1/15. Should ALREADY be measuring!!!

50

Who do I measure? 50 Full Time 30+ Hours Variable ???? Part Time < 30 Hours TEACHERS FT AIDES SECRETARIES SUBSTITUTES? CUSTODIANS? COACHES? PARAS? TEMPS? PT AIDES CUSTODIANS PARAS

51

Measuring Hours 3 Ways to Measure Employees Hourly Employees – Count actual hours worked Aide, Para Salaried Employees – 8 hour day or 40 hour work week Teachers, Principals Reasonable Method Per Diem, Substitutes, Coaches 51

52

How to Measure (safe harbor) MEASUREMENT PERIOD – Record the hours worked A period of 3-12 months ADMINISTRATIVE PERIOD – Get employees to sign up or sign waivers A Period of up to 90 days STABILITY PERIOD – Employee is locked into benefits Minimum of 6 months Matches the Measurement (i.e. MP =12 months, SP = 12 months) 52

52.")

53

AP Standard Measurement Period Measurement Example 12/31/15 1/1/16 1/1/15 12/31/16 1/1/14 Stability Period Standard Measurement Period: 12 Months 5/1/14 Administrative Period: 60 Days Stability Period: 12 Months 53 7/1/15 Stability Period 12/31/14 7/1/16

54

New Hire Example “Initial Measurement Period” ABC Employer hires a new employee On September 1, 2014 Position where it’s unknown whether or not employee will end up being “Full Time” Measured Against 2 Measurement Periods: 1.Standard Measurement Period 2.Initial Measurement Period 54

55

New Hire Example “Initial Measurement Period” Initial Measurement Period & Admin Period may not extend beyond the last day of the first calendar month beginning on or after the 1 year anniversary of the employees start date 13 months and a fraction of a month 55

56

AP Standard Measurement Period Initial Measurement Example 56 12/31/15 1/1/16 1/1/15 12/31/16 1/1/14 SMP Standard Stability Period Standard Measurement Period: 12 Months Initial Measurement Period: 12 Months Administrative Period: 1 Month Stability Period: 12 Months Initial Stability Period: 12 Months 9/1/14 11/30/15 12/1/14 IMP Initial Measurement Period 8/31/15 AP 9/30/15 12/31/14 ISP Initial Stability Period 9/30/16

57

Coach Example - Offer ABC Employer has an employee that: Works as a SUB 4 days/wk (26 hours/wk) Works as a track COACH during the winter 2 hours/day and 8 hours on Saturday (18 hours) Coaches for 13 weeks 57 40 weeks in a school year 27 weeks at 26 hours 13 weeks at 44 hours (26 + 18) Average Hours worked: 27wks * 26hrs + 13wks * 44hrs = 1,274 total hours 1,274hrs / 40 weeks AVERAGE HOURS: 31.85

Works as a track COACH during the winter 2 hours/day and 8 hours on Saturday (18 hours) Coaches for 13 weeks weeks in a school year 27 weeks at 26 hours 13 weeks at 44 hours ( ) Average Hours worked: 27wks * 26hrs + 13wks * 44hrs = 1,274 total hours 1,274hrs / 40 weeks AVERAGE HOURS: 31.85")

58

Coach Example – No Offer ABC Employer has an employee that: Works as a SUB 3 days/wk (19.5 hours/wk) Works as a track COACH during the winter 2 hours/day and 8 hours on Saturday (18 hours) Coaches for 13 weeks 58 40 weeks in a school year 27 weeks at 19.5 hours 13 weeks at 37.5 hours (19.5 + 18) Average Hours worked: 27wks * 19.5hrs + 13wks * 37.5hrs = 1,014 total hours 1,014hrs / 40 weeks AVERAGE HOURS: 25.35

Works as a track COACH during the winter 2 hours/day and 8 hours on Saturday (18 hours) Coaches for 13 weeks weeks in a school year 27 weeks at 19.5 hours 13 weeks at 37.5 hours ( ) Average Hours worked: 27wks * 19.5hrs + 13wks * 37.5hrs = 1,014 total hours 1,014hrs / 40 weeks AVERAGE HOURS: 25.35")

59

Affordable Care Act Today’s Discussion Employer Reporting Cadillac Tax 59

60

ACA Reporting Why is Employer Reporting Required? 60 The ACA reporting requirements help the IRS assess and collect the employer- shared responsibility penalty

61

Employer Reporting When Must Reporting Start? The first reporting year is 2016 (for calendar year 2015): IRS: 2015 data due via paper filing March 1, 2016; online filing due March 31, 2016 Employees: statement for 2015 year of coverage due January 31, 2016 61

: IRS: 2015 data due via paper filing March 1, 2016; online filing due March 31, 2016 Employees: statement for 2015 year of coverage due January 31,")

62

Employer Reporting When is Reporting Due in Subsequent Years? IRS: reporting for prior year of coverage due each February 28 online filing date is March 31 Employees: statement for prior year of coverage due each January 31 Reporting is due each and every year: it is imperative that data is collected each month for easy and accurate year-end reporting 62

63

Employer Reporting IRS Code §6055 What is Required? Proof of compliance with Code §6055 Employers offering health insurance must offer minimum essential coverage *individuals must have minimum essential coverage each month or pay a penalty Report consists of a return filed with the IRS and a statement for each employee 63

64

Employer Reporting What is minimum essential coverage? Minimum essential coverage is the type of health coverage an individual must have to meet the individual responsibility requirements under the ACA. This includes marketplace plans, job-based coverage, Medicare, Medicaid, TRICARE, or CHIP. If the individual does not have this coverage, he/she is subject to a tax penalty by the IRS. 64

65

Employer Reporting IRS Code §6055 Who Must Report? Health insurers and self-insured plan sponsors are required to report Plans provided by an insurer: employer must satisfy the reporting requirements, but the insurer will complete the report to the IRS Self-insured plans: the employer must satisfy all aspects of reporting requirements, including filing with the IRS 65

66

Employer Reporting IRS Code §6055 What Data Is Required? The reports require information about the employer and dependents, such as Employee name, address, Taxpayer ID Months enrolled in coverage under employer plan o Note the specific months that each employee is enrolled must be reported o Employer must be certain to track this data monthly for accurate reporting at year-end 66

67

Employer Reporting IRS Code §6055 What Forms are Required? 67 Self-insured employers with <50 full-time employees must file: To IRS: Form 1094-B / Transmittal of Health Coverage Information Returns To employees: Form 1095-B / Health Coverage

68

Employer Reporting IRS Code §6055 IRS Form 1094-B…Page 1 68

69

Employer Reporting IRS Code §6055 IRS Form 1095B…Page 1 69

70

70 Employer Reporting IRS Code §6055 IRS Form 1095-B…Page 2

71

Employer Reporting IRS Code §6056 What is Required? Proof of compliance with Code §6056 Employers offering health insurance must confirm to IRS and employees that plan offers minimum value coverage Employers must offer minimum value coverage each month or pay a penalty if any full-time employee enrolls in coverage through the Marketplace Exchange with a tax subsidy Report consists of a return filed with the IRS and a statement for each employee 71

72

Employer Reporting IRS Code §6056 What is Required? What is a minimum value coverage plan? Minimum value coverage is a requirement that ensures a health plan covers, on average, at least 60% of the cost of benefits. Coverage is affordable if the employee’s annual contribution for individual coverage does not exceed 9.56% of the employee’s yearly household income. 72

73

Employer Reporting IRS Code §6056 Who Must Report? Applicable Large Employers (ALEs) with an average of 50+ full-time employees (FTEs) must report annually ALE / Applicable Large Employers: An employer with an average of at least 50 full-time employees on business days during the preceding calendar year FTE / Full-time Employee: Full-time equals 30 hours of work/week or 130 hours of work/month; includes full-time equivalents 73

with an average of 50+ full-time employees (FTEs) must report annually ALE / Applicable Large Employers: An employer with an average of at least 50 full-time employees on business days during the preceding calendar year FTE / Full-time Employee: Full-time equals 30 hours of work/week or 130 hours of work/month; includes full-time equivalents 73.")

74

Employer Reporting IRS Code §6056 Are You an ALE? Employers might need help determining if they are an Applicable Large Employer (ALE): The employer will need to carefully track employee hours Part-time hours must be converted to full-time hours Employers must begin gathering required information beginning January 2015 in order to complete accurate reporting in 2016 74

: The employer will need to carefully track employee hours Part-time hours must be converted to full-time hours Employers must begin gathering required information beginning January 2015 in order to complete accurate reporting in")

75

Employer Reporting IRS Code §6056 What Data is Required? The reports require information about the employer, full-time employees, and coverage, such as: Employer name, address, EIN Employee name, address, Tax Identification Number Months employee enrolled in coverage under employer plan Number of full-time employees enrolled each month If coverage offers minimum value Employee share of (individual) lowest-cost monthly premium 75

lowest-cost monthly premium 75.")

76

Employer Reporting IRS Code §6056 What Data is Required? A wide range of information is required: o Note the specific months that each employee is enrolled must be reported o Employer must be certain to track this data monthly for accurate reporting at year-end o Employer must determine who will collect and store the data 76

77

Employer Reporting IRS Code §6056 What Forms are Required? 77 Insured and self-insured employers with 50+ full- time employees must file: To IRS: Form 1094-C / Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Returns To employees: Form 1095-C / Employer-Provided Health Insurance Offer and Coverage

78

Employer Reporting IRS Code §6056 IRS Form 1094-C… Page 1 78

79

Employer Reporting IRS Code §6056 IRS Form 1094-C…Page 2 79

80

Employer Reporting IRS Code §6056 IRS Form 1094-C…Page 3 80

81

81 Employer Reporting IRS Code §6056 IRS Form 1095-C…Page 1

82

82 Employer Reporting IRS Code §6056 IRS Form 1095-C…Page 2

83

Employer Reporting IRS Code §6055 and §6056 How Are Forms Filed? IRS: employers who are filing 250+ W2 forms must file online with the IRS; <250 can mail to assigned IRS center or file online Employees: paper statements must be delivered via first-class mail to the employee’s last known address o Statements can be transmitted electronically if employee agrees and can retrieve the statement o Statements can be included within the W2 mailing 83

84

Employer Reporting IRS Code §6055 and §6056 Do Penalties Apply? Penalties may be waived if failure to report is allowed as reasonable cause Some relief may be given if mistakes are made in reporting for coverages, penalties for incorrect or incomplete filing if employer made a ‘good faith’ effort to comply with requirements Employers that do not submit an annual report to the IRS or fail to provide statements to full-time employees may be penalized up to $100 per return (annual maximum of $1.5 million) 84

84.")

85

Employer Reporting IRS Code §6055 and §6056 Gather the Data… It is imperative that employers collect employment data each and every month in order to provide year-end reports to the IRS and employees easily and accurately. The employer must have a fool- proof system in place to track employee hours. 85

86

Employer Reporting IRS Code §6055 and §6056 Report the Data… 86

87

Cadillac Tax IRS Code § 49801 [eff. 2018] What Is It? 87 Purchase Price = $70,000 7% Sales Tax = $4,900

![Cadillac Tax IRS Code § [eff. 2018] What Is It.](http://images.slideplayer.com/13/4162603/slides/slide_87.jpg "87 Purchase Price = $70,000 7% Sales Tax = $4,900.")

88

Cadillac Tax IRS Code § 49801 What Is Taxed? A tax is assessed on any amount by which the monthly cost of an employer-sponsored health plan exceeds the annual limitation set by the IRS (excess benefit) Applies to the cost of “applicable employer- sponsored coverage” excluded from employee’s gross income Intended to “encourage” companies to choose lower-cost plans for employees 88

Applies to the cost of applicable employer- sponsored coverage excluded from employee’s gross income Intended to encourage companies to choose lower-cost plans for employees 88.")

89

Cadillac Tax IRS Code § 49801 What Is Not Taxed? The tax does not apply to coverage for long-term care or “excepted benefits”, such as: Accident-only or disability income insurance Workers’ compensation or similar insurance Automobile medical payment insurance Separate, non-excepted benefit dental / vision plans Some independent coverages for specific disease/ illness or hospital indemnity insurances 89

90

Cadillac Tax IRS Code §49801 How Is the Tax Calculated? Imposes a 40% excise tax on health coverage monthly costs exceeding annual limit Currently, 2018 annual dollar limit is $10,200/individual and $27,500/ other o Qualified retirees and those in high-risk professions have higher limitations of $11,850/individual and $30,950/other Future annual limits may be adjusted for cost of living and emerging age/gender data 90

91

Cadillac Tax IRS Code §49801 For Example…Individual Coverage 91 Mary is enrolled in a plan with an annual premium of $11,000 The ACA annual limit for an individual plan is $10,200 Her plan premium is $800 above the annual limit ($800 excess benefit) $800 x 40% = $320

$800 x 40% = $320")

92

Cadillac Tax IRS Code §49801 For Example…Family Coverage 92 Tom’s family is enrolled in a health plan with an annual premium of $28,000 The ACA annual limit for an family plan is $27,500 His plan premium is $500 above the annual limit ($500 excess benefit) $500 x 40% = $200

$500 x 40% = $200")

93

Cadillac Tax Knowns IRS Code §49801 Who pays the tax? o Fully insured plans: the insurer o Self-insured plans: the employer/administrator Are there penalties for incorrect tax payments? o The employer will be subject to a tax penalty o Penalties do not apply if employer can provide it did not know of a mistake if corrected within 30 days and the IRS agrees to waive the penalty o The insurer must pay the amount of any unpaid tax 93

94

Cadillac Tax IRS Code §49801 The Unknowns How will the tax be billed/collected? o No regulations published to date o Can the tax be passed onto employees? The tax is coming in 2018 but what further updates are to come? 94

95

Cadillac Tax IRS Code §49801 High-Cost vs. Low-Cost Plans 95

96

Introduce lower-cost alternative plans as soon as and whenever possible High Deductible plans could save up to 30% versus current plan rates Defined Contribution benefits with employer contribution below the tax 96 Cadillac Tax IRS Code §49801 High-Cost vs. Low-Cost Plans

97

The Wrap-Up Capture 2015 data now for 2016 reporting Watch for updates about 2018 Cadillac tax Boards and employees must be willing to adopt a benefit package that costs less Rely on your professionals now more than ever 97

Similar presentations

Shared Responsibility Mandate 1.>")

>")

Presented by the Asian American Hotel Owners Association (AAHOA)>")