Download presentation

Presentation is loading. Please wait.

1

The Long-Term Effects of Cross-Listing, Investor Recognition, and Ownership Structure on Valuation Michael R. King, Bank of Canada Dan Segal, Univ. of Toronto November 2006

2

“[C]ompanies listed in the U.S. … have found that a U.S. listing pays off in a higher profile, greater access to new capital, a wider shareholder base and more liquidity for their stock.” Financial Post April 6,1996 Karolyi (2004) ‘conventional wisdom’

![[C]ompanies listed in the U.S. … have found that a U.S.](http://images.slideplayer.com/13/4144712/slides/slide_2.jpg "listing pays off in a higher profile, greater access to new capital, a wider shareholder base and more liquidity for their stock. Financial Post April 6,1996 Karolyi (2004) ‘conventional wisdom’.")

4

Motivation How permanent are valuation gains? How do they vary across time? How do effects vary cross-sectionally? Firm characteristics (growth, ROA, leverage) Ownership (widely-held, control 20%+,dual-class) Endogeneity issue Matching methods (size, industry) 2SLS: 1 st – investor holdings, 2 nd – Tobin’s q Before & after using only cross-listed firms

Ownership (widely-held, control 20%+,dual-class) Endogeneity issue Matching methods (size, industry) 2SLS: 1 st – investor holdings, 2 nd – Tobin’s q Before & after using only cross-listed firms.")

5

Findings Only transitory increase in valuation from cross- listing; disappears in 3 years Not explained by changing U.S. shareholder base Outperform initially if attract larger number or % holdings of U.S. investors No variation by ownership structure at high levels Widening of investor base & improved info environment are distinct effects Dual-class benefit at low levels when others do not Reduced info asymmetry (Jensen & Meckling 1976)

.")

6

Overview Hypothesis development Data and methodology Univariate tests Importance of U.S. investors Cross-sectional variation by owner type Cross-listing – before and after

7

Merton (1987) investor recognition Investors only buy stocks they know about Shadow cost of incomplete information … …leads to higher expected excess returns Studies focus on change in investor base (q i ) or change in visibility (1) (2)

investor recognition Investors only buy stocks they know about Shadow cost of incomplete information … …leads to higher expected excess returns Studies focus on change in investor base (q i ) or change in visibility (1) (2)")

8

First hypothesis (H1) Foerster & Karolyi (1999) event studies (ARs) Change in investor base primary; liquidity secondary Baker et al (2002), Lang et al (2003) Increased analyst following & media following Improved information environment Cross-country studies with industry controls Few firm controls (size, capital raising, earnings growth) Focus on point in time H1: Higher number or percentage hldgs by U.S. investors higher Tobin’s q

9

Second hypothesis (H2) Permanent or transitory? Foerster & Karolyi (1999) find pre-listing run-up & post- listing decline [-1,1] in ARs ; could be investor recognition or liquidity Mittoo (2003) same pattern for Cdn firms [-1,3]; reject liquidity as longer horizon explanation Sarkissian & Schill (2004) study ARs of firms listed in 1998 over [-10,10]; permanent gains are due to investor familiarity Gozzi et al (2005) study Tobin’s q [-2,2]; focus on changing components, not investor base H2: Permanent gains if maintain wider investor base over time

find pre-listing run-up & post- listing decline [-1,1] in ARs ; could be investor recognition or liquidity Mittoo (2003) same pattern for Cdn firms [-1,3]; reject liquidity as longer horizon explanation Sarkissian & Schill (2004) study ARs of firms listed in 1998 over [-10,10]; permanent gains are due to investor familiarity Gozzi et al (2005) study Tobin’s q [-2,2]; focus on changing components, not investor base H2: Permanent gains if maintain wider investor base over time.")

10

Third hypothesis (H3) U.S. investors avoid closely-held foreign firms Edison & Warnock (2004), Leuz, Lins & Warnock (2005), Ferreira & Matos (2006) Improvement in info environment is key Lang et al (2004), Ammer et al (2005) Impact of concentrated ownership; separation of cash-flow vs. control Morck et al (1988), Claessens et al (2002), Lins (2003), Lemmon & Lins (2003), Doidge et al (2006) H3: Firms with control 20%+ or dual-class have lower investor recognition than widely-held firms

, Leuz, Lins & Warnock (2005), Ferreira & Matos (2006) Improvement in info environment is key Lang et al (2004), Ammer et al (2005) Impact of concentrated ownership; separation of cash-flow vs. control Morck et al (1988), Claessens et al (2002), Lins (2003), Lemmon & Lins (2003), Doidge et al (2006) H3: Firms with control 20%+ or dual-class have lower investor recognition than widely-held firms.")

11

Fourth hypothesis (H4) Increased valuations due to reduced info asymmetry; greater monitoring (bonding) Coffee (1998, 2002), Stulz (1998), Reese & Weisbach (2002), Firm-level effect vs. country-level effect (LLSV) Doidge et al (2004) controlling shareholders weigh costs vs. private benefits Doidge (2004) benefits should be larger when agency problems greatest e.g. firms with dual-class shares H4: Firms with control 20%+ or dual-class benefit more at low levels of investor holdings

Doidge et al (2004) controlling shareholders weigh costs vs. private benefits Doidge (2004) benefits should be larger when agency problems greatest e.g. firms with dual-class shares H4: Firms with control 20%+ or dual-class benefit more at low levels of investor holdings.")

12

Data and methodology 16 year panel 1989-2004: match Xlist with non-Xlist (size, industry); 2,802 obs; 683 firms Control for: time-zone, form of XLIST, legal effects Univariate tests; panel regressions with fixed effects; time variation in all dummies e.g. Xlist, owner type, control % Endogeneity: matching methods, before-after

13

Cross-listing & ownership structure Non-XLISTXLIST Blue = Widely Yellow = Dual Red = Control20%+

14

Table 2: Importance of U.S. investors

15

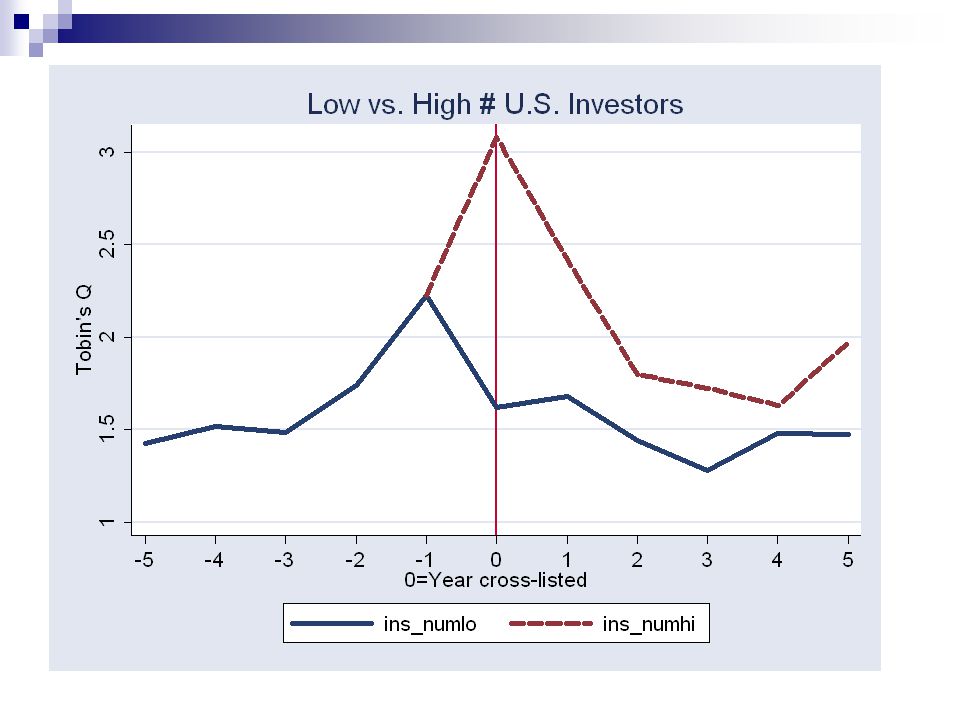

Table 2: Importance of U.S. investors (2) Split XLIST dummy into low vs. high based on median number of investors (INUM) or % investors (IHOL) Only firms in upper halves increase in valuation Firms that fail to widen investor base same as non-XLIST

or % investors (IHOL) Only firms in upper halves increase in valuation Firms that fail to widen investor base same as non-XLIST.")

16

Table 3: Time-series effects Interact INUM with year dummies relative to XLIST Only INUM year 0 & 1 significant; monotonic decline Similar but weaker for IHOL

17

Table 4: Ownership effects Control 20%+ valued similarly to widely-held firms Dual-class have lower valuations on average XLIST have higher valuations on average No significance from interaction terms

18

Table 5: Ownership & U.S. investors Only firms in INUMHI / IHOLHI increase in valuation Control 20%+ do worse at higher # or % Dual-class same at higher; do better at lower # or %

19

Cross-listing – before and after Address endogeneity using only cross-listed firms 120 firms cross-listed 1990-2003 Exclude IPOs/spin-offs or less than [-1,1] 69 firms, median 7 yrs (min 3 yrs, max 11 yrs) Repeat analysis in Tables 2-5

![Cross-listing – before and after Address endogeneity using only cross-listed firms 120 firms cross-listed Exclude IPOs/spin-offs or less than [-1,1] 69 firms, median 7 yrs (min 3 yrs, max 11 yrs) Repeat analysis in Tables 2-5](http://images.slideplayer.com/13/4144712/slides/slide_19.jpg "Cross-listing – before and after Address endogeneity using only cross-listed firms 120 firms cross-listed Exclude IPOs/spin-offs or less than [-1,1] 69 firms, median 7 yrs (min 3 yrs, max 11 yrs) Repeat analysis in Tables 2-5")

20

Table 6: XLIST before - after Dual-class benefit more from cross-listing Clear time-series pattern; benefit mis-specified

22

Summary Widening of U.S. investor base & improved info environment are distinct effects Valuations peak in year 0 then fall monotonically at all levels of U.S. investor holdings and across all ownership structures U.S. investors less willing to invest in dual-class Dual-class benefit more even when they fail to widen their U.S. investor base Reduction in info asymmetry has separate impact on valuation for firms with greatest agency problems

Similar presentations

>")

. Lecture Overview u Review u Two broad types of capital markets research u Information content of earnings.>")

Qiao Liu, HKU Corporate Governance.>")

“ The Mechanics of Raising.>")