Download presentation

Presentation is loading. Please wait.

1

Wage Withholding Tax Re-introduction May 2004 Speaker : Mr Ihsan Shamran Dir. of Corporations Dept.

2

All income taxes (personal and corporate) were suspended from January 1st of year 2003 to April 30th of year 2004. (Reference : Policy Orders issued by the CPA #37, #45 and #84)

.")

3

Employers Private sector Mixed sector State-owned enterprises

4

Employee definition Any person who has performed or is performing work for a wage and works under the administration and direction of the party employing him. Reference : Instructions No. 3 of 1983

5

Income subject to withholding tax Salaries, wages Allowances (subject to 30% rule for specific allowances) Bonuses

Bonuses")

6

Principal exemptions Allowances for –Clothing –food –lodging –transportation Not taxable if < 30% of the total wage of the employee Other Allowances fully taxable

7

Principal Exemptions (con’t) Are exempted from tax : All income earned by foreign employees of foreign contractors and subcontractors of the CPA, Coalition Forces, forces of countries acting in coordination with the Coalition Forces’ governments that are providing assistance to Iraq.

Are exempted from tax : All income earned by foreign employees of foreign contractors and subcontractors of the CPA, Coalition Forces, forces of countries acting in coordination with the Coalition Forces’ governments that are providing assistance to Iraq.")

8

Principal Exemptions (con’t) Are exempted from tax : All income earned by foreign employees of foreign contractors and subcontractors of foreign governments, international organizations and non governmental organizations registered pursuant to CPA Order #45, that are providing assistance to Iraq.

Are exempted from tax : All income earned by foreign employees of foreign contractors and subcontractors of foreign governments, international organizations and non governmental organizations registered pursuant to CPA Order #45, that are providing assistance to Iraq.")

9

Principal Exemptions (con’t) Are exempted from tax : Salaries and allowances paid by United Nations from its own budget to its officials and employees.

Are exempted from tax : Salaries and allowances paid by United Nations from its own budget to its officials and employees.")

10

Preparation of Reports, Forms and Schedules A: Employees Report B: Forms Dhad.D\4A C: Income Tax Deductions Schedule Must be filed and submitted to the Direct Deduction Section in the main office of the General Commission for Taxes (Baghdad) or to the branches of the General Commission for Taxes (hereinafter “GTC”). All forms, reports, schedules and correspondence sent to the GTC should be in the Arabic Language.

11

Preparation of Reports, Forms and Schedules (con’t) A: Employees Report List of name and job title of all employees Salary or monthly wage for each of the employees Hiring date Serially numbered starting with #1 Limit date for submission : July 1, 2004 Report should be prepared for new hires, every three months.

A: Employees Report List of name and job title of all employees Salary or monthly wage for each of the employees Hiring date Serially numbered starting with #1 Limit date for submission : July 1, 2004 Report should be prepared for new hires, every three months.")

12

Preparation of Reports, Forms and Schedules (con’t) A: Employees Report (con’t) For confidentiality and security reasons : Foreign companies may remit the employees report at the same time than Forms Dhad.D/4A (no later than March 31 st 2005) to the head officer of Direct Deduction Section in Baghdad.

A: Employees Report (con’t) For confidentiality and security reasons : Foreign companies may remit the employees report at the same time than Forms Dhad.D/4A (no later than March 31 st 2005) to the head officer of Direct Deduction Section in Baghdad.")

13

Preparation of Reports, Forms and Schedules (con’t) B: Form Dhad.D\4A Page 1 : 1) To be distributed among the employees. 2) Employees complete page 1 and sign. 3) Remit quickly to the employer 4) Employer verify employees’ information If employer does not receive completed Form Dhad.D\4A from the employee, employee shall be entitled to only bachelor’s allowance for the year.

Employees complete page 1 and sign. 3) Remit quickly to the employer 4) Employer verify employees’ information If employer does not receive completed Form Dhad.D\4A from the employee, employee shall be entitled to only bachelor’s allowance for the year..")

15

Preparation of Reports, Forms and Schedules (con’t) B: Form Dhad.D\4A Page 2 To be completed by employer and submitted to the GTC before March 31 st of the following year. (Foreign companies may submit to the head officer of Direct Deduction Section in Baghdad)

.")

17

Preparation of Reports, Forms and Schedules (con’t) C: Income Tax Deductions Schedule To be completed by the employer at the end of every year in duplicate showing all the income, allowances and deductions, which are brought from page #2 of Form Dhad.D\4A To be completed by employer and submitted to the GTC before March 31 st of the following year.

C: Income Tax Deductions Schedule To be completed by the employer at the end of every year in duplicate showing all the income, allowances and deductions, which are brought from page #2 of Form Dhad.D\4A To be completed by employer and submitted to the GTC before March 31 st of the following year.")

20

Method of deducting income tax and its payment dates A special register should be kept wherein shall be entered salaries, allowances and wages of their employees who are subject to income tax. Tax withheld shall be remitted to either the Direct Deduction Section at the GTC or the unit of Wage Withholding Assessment at the branches of the GTC.

21

Method of deducting income tax and its payment dates (con’t) Tax withheld may be paid in either cash or by certified checks, together with a list showing the names of the employees from whose income the tax was deducted, and the amount deducted from each of them, and the related period of the year. Address in Baghdad: Jamal Abdlnasar Street, second building after Iraqi Museum.

23

Method of deducting income tax and its payment dates (con’t) About the form shown on the previous slide, for confidentiality and security reasons, foreign companies may do the following: Keep the names of employees secret and use only the ID nationality number or the employee ID number.

About the form shown on the previous slide, for confidentiality and security reasons, foreign companies may do the following: Keep the names of employees secret and use only the ID nationality number or the employee ID number.")

24

The withheld tax is to be paid in 4 installments as follows : The amounts due for January, February and March = 1 st day of April The amounts due for April, May and June = 1 st day of July The amounts due for July, August and September = 1 st day of October The amounts due for October, November and December = 2nd day of January.

25

Penalties and Interests If the tax is not settled as indicated before on the fixed dates, an additional percentage of 5% shall be imposed after the lapse of 21 days from the fixed date. An additional percentage of 10% shall be imposed if the amount is not paid within 21 days after the expiration of the first period. Interest to be charged according to Resolution #307 of 1984.

26

Penalties (con’t) Other penalties may apply when the employer fails to carry out the duties imposed on him under the Income Tax Law #113 or the regulations issued there under, or refusing or delaying to submit to the Financial Authority any statement or information he was obliged or called upon to submit under the provisions of the Income Tax Law.

Other penalties may apply when the employer fails to carry out the duties imposed on him under the Income Tax Law #113 or the regulations issued there under, or refusing or delaying to submit to the Financial Authority any statement or information he was obliged or called upon to submit under the provisions of the Income Tax Law.")

27

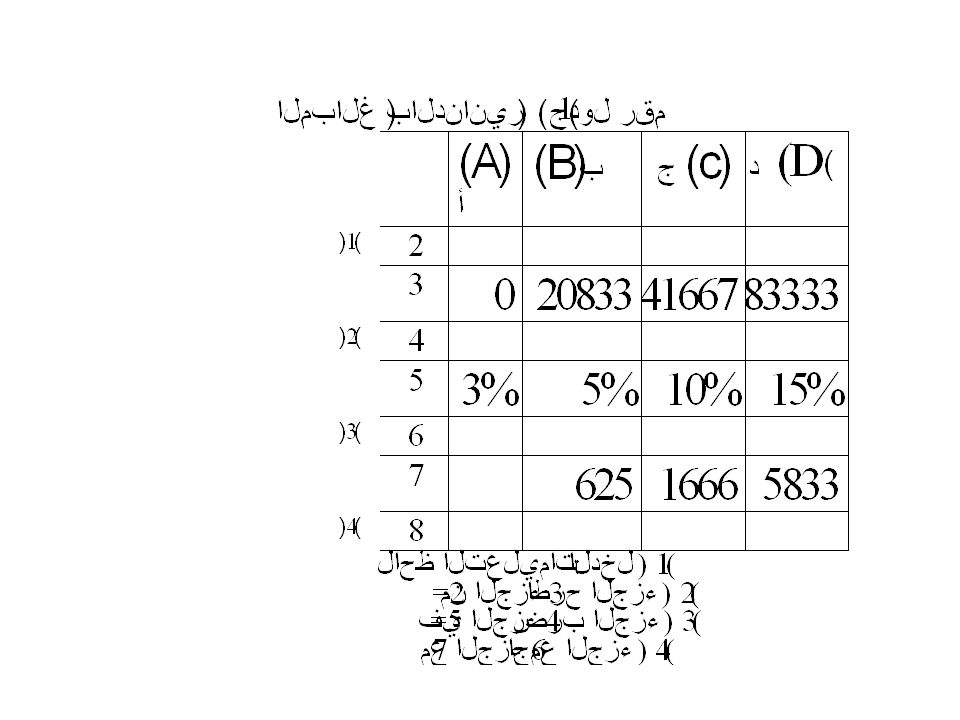

Legal allowances The income subject to income tax by direct deduction is reduced by the legal allowances granted to the resident individuals Bachelor personID 208,333 / month Married employeeID 375,000 / month Widow or divorceeID 266,667 / month State-Owned Enterprise employee (for 2004 only)ID 441,667 / month

ID 441,667 / month")

28

Legal allowances (con’t) Additional allowances : For every child ID 16,667 / month If > 63 years oldID 25,000 / month No additional allowances for State-Owned Enterprises employees (ID 441,667 / month even if they have more than 4 children) So, no tax to withhold on income of a single employee working in the private sector if he earns less than ID 208,333 for a particular month.

Additional allowances : For every child ID 16,667 / month If > 63 years oldID 25,000 / month No additional allowances for State-Owned Enterprises employees (ID 441,667 / month even if they have more than 4 children) So, no tax to withhold on income of a single employee working in the private sector if he earns less than ID 208,333 for a particular month.")

29

Tax Rates Rate Annual income (after allowances) 3%Up to ID 250,000 5%Over ID 250,000 and up to ID 500,000 10%Over ID 500,000 and up to 1,000,000 15%Over ID 1,000,000

3%Up to ID 250,000 5%Over ID 250,000 and up to ID 500,000 10%Over ID 500,000 and up to 1,000,000 15%Over ID 1,000,000")

30

Tax rates (con’t) The amount delineating the tax-bracket amounts above are divided by 12 months in order to determine the amount of tax to withhold for every month.

The amount delineating the tax-bracket amounts above are divided by 12 months in order to determine the amount of tax to withhold for every month.")

31

Tax rates (con’t) Rate Monthly income (after montly allowances) 3%Up to ID 20,833 5%Over ID 20,833 and up to ID 41,667 10%Over ID 41,667 and up to ID 83,333 15%Over ID 83,333

Rate Monthly income (after montly allowances) 3%Up to ID 20,833 5%Over ID 20,833 and up to ID 41,667 10%Over ID 41,667 and up to ID 83,333 15%Over ID 83,333")

32

How to calculate the monthly tax amount to withhold : Use of a work chart provided in the brochure Use of withholding tables available at the office of the GTC

33

Use of the work chart (brochure) First step : –Calculate the monthly salary, monthly wages and monthly taxable allowances –Minus monthly deductions provided in Article 8 of the Income Tax Law #113 paid by the employee such as : Pension and contributions as determined by Pension and Social Security Laws (Private sector : 5% on gross wage)

First step : –Calculate the monthly salary, monthly wages and monthly taxable allowances –Minus monthly deductions provided in Article 8 of the Income Tax Law #113 paid by the employee such as : Pension and contributions as determined by Pension and Social Security Laws (Private sector : 5% on gross wage)")

34

Use of the work chart (brochure) Second step: Subtract from the amount of the last slide the monthly legal allowance to which the employee is entitled: Bachelor personID 208,333 / month Married employeeID 375,000 / month Widow or divorceeID 266,667 / month State-Owned Enterprise employee (for 2004 only)ID 441,667 / month

Second step: Subtract from the amount of the last slide the monthly legal allowance to which the employee is entitled: Bachelor personID 208,333 / month Married employeeID 375,000 / month Widow or divorceeID 266,667 / month State-Owned Enterprise employee (for 2004 only)ID 441,667 / month")

35

Use of the work chart (brochure) Second step (con’t) Additional monthly legal allowances : For every child ID 16,667 / month If > 63 years oldID 25,000 / month

Second step (con’t) Additional monthly legal allowances : For every child ID 16,667 / month If > 63 years oldID 25,000 / month")

36

Use of the work chart (brochure) If after the deduction of the monthly legal allowance which the employee is entitled, there is still a positive amount, that means there is income tax to withhold. This monthly income tax to withhold can be determined by using the workchart provided in the last page of the brochure.

38

Use of Withholding tables A second method is provided for the employers in order to determine the monthly income tax to withhold for each of their employees: The employer can use Tax Tables called: –Tax Withholding Table – Single and Married –Tax Withholding Table – Widow or Divorcee

39

Use of Withholding tables (con’t) First step –Calculate the monthly salary, monthly wages and monthly taxable allowances –Minus monthly deductions provided in Article 8 of the Income Tax Law #113 paid by the employee such as : Pension and contributions as determined by Pension and Social Security Laws Example = monthly salary of ID 703,000

First step –Calculate the monthly salary, monthly wages and monthly taxable allowances –Minus monthly deductions provided in Article 8 of the Income Tax Law #113 paid by the employee such as : Pension and contributions as determined by Pension and Social Security Laws Example = monthly salary of ID 703,000")

40

Use of Withholding tables (con’t) First step (con’t) Example : Single employee Monthly salary =ID 703,000 –Social security and pension contributions (private sector : 5%) = ID 35,150 Taxable income before Legal Allowance= ID 667,850

First step (con’t) Example : Single employee Monthly salary =ID 703,000 –Social security and pension contributions (private sector : 5%) = ID 35,150 Taxable income before Legal Allowance= ID 667,850")

41

Use of Withholding tables (con’t) Second step: Depending on the particular status of the employee, select one of the two tax tables which is applicable to the employee. Determine the code allowance which the employee is entitled for the month For example, single employee = O

42

Use of Withholding tables (con’t) Third step: Under the column “Taxable income per month (before any applicable legal allowance)” of the selected Tax Table, you determine the taxable income per month bracket attributable to the employee. For this example ID 660,000 to ID 669,999

43

Use of Withholding tables (con’t) Fourth step: The number in ID that corresponds in the applicable code allowance column is the amount of monthly income tax to withhold. For this example : ID 61,833

44

For More Information See the “User’s guide for the wage withholding tax” and all other related documents at : http://www.iraqcoalition.org/arabic/taxes/ http://www.iraqcoalition.org/taxes/

Similar presentations