Download presentation

Presentation is loading. Please wait.

1

Chapter 5 Energy Derivatives: Structures and Applications (Book Review) Zhao, Lu (Matthew) Dept. of Math & Stats, Univ. of Calgary January 24, 2007 “ Lunch at the Lab ” Seminar

2

Outline Exchange Traded Instruments Swaps Caps, Floors and Collars Swaptions Compound Options – Captions and Floptions Spread and Exchange Options Path Dependent Options

3

1 Introduction Exotic Options More complicated payoff structures than standard derivatives Known as second generation, or sometimes path-dependent options Trade over-the-counter (almost)

")

4

2 Exchange Traded Instruments New York Mercantile Exchange (NYMEX) Futures and American style futures options on oil, gas and electricity; crack spread options Chicago Board Options Exchange (CBOE) Electricity futures and options Sydney Futures Exchange and Nordic Electricity Exchange Electricity futures

Futures and American style futures options on oil, gas and electricity; crack spread options Chicago Board Options Exchange (CBOE) Electricity futures and options Sydney Futures Exchange and Nordic Electricity Exchange Electricity futures")

5

3 Swaps First energy swaps were traded in October 1986 (Chase Manhattan Bank vs. Cathay Pacific Airways and Koch Industries, oil-indexed price swap) Swaps are also known as Contracts-for- Differences or Fixed-for-Floating contracts Used to lock in a fixed price for a certain predetermined but not necessarily constant quantity

Swaps are also known as Contracts-for- Differences or Fixed-for-Floating contracts Used to lock in a fixed price for a certain predetermined but not necessarily constant quantity.")

6

3.1 Vanilla Swap An agreement in which counterparties exchange a floating energy price for a fixed energy price Example Buyer: an oil producer Swap provider: an oil refiner A swap would allow them to buy forward their anticipated oil consumption based on current oil forward prices

7

Vanilla swaps can be priced directly off the forward energy curve since the appropriate portfolio of forward deals is an exact hedge of the swap. Therefore, the payoff at each reset date is the same as for a forward contract A vanilla swap is usually viewed as a weighted average of the forwards underlying the swap with weights being the discount rates to each of the swap settlement dates

8

The value of a vanilla swap

9

3.2 Variable Volume Swap This contract is identical to a vanilla swap except that the underlying quantity or volume is not known in advance The variability of the volume must be modeled in order to price contracts (detailed in Chapter 7)

")

10

3.3 Differential Swap Similar to vanilla swaps except that the counterparties exchange the difference between two different floating prices for a fixed price differential Example A refiner ’ s probability depends on the market price differential of the raw commodity and the refined products and a differential swap allows a refiner to lock in their refining margin at the fixed price

11

A differential swap is a portfolio of forward differential contracts with maturity dates corresponding to the settlement dates underlying the differential swap The value is given by

12

3.4 Margin or Crack Swap A specific form of differential swap in which the fixed price payer receives the difference between the market price differential of the raw commodity and the refined products in appropriate fractions and the fixed price

13

3.5 Participation Swap Similar to a vanilla swap in that the fixed price payer is fully protected when prices rise above the agreed fixed price but they participate in a certain percentage of savings if prices fall. Example A participation swap for gasoil at a fixed price of $150 per ton with a participation of 50% a) If the gasoil price is $160 per ton, the fixed price payer received $10 per ton; b) If the gasoil price is $140 per ton, the fixed price payer only pay the provider $5 per ton

If the gasoil price is $160 per ton, the fixed price payer received $10 per ton; b) If the gasoil price is $140 per ton, the fixed price payer only pay the provider $5 per ton.")

14

3.6 Double-Up Swap The fixed price payer can achieve a better swap price than the market price but in return the swap provider has the option to double the volume before the pricing period starts The fixed price payer is exposed to the risk that if swap prices fall the fixed price receiver will exercise the right to double the swap volume

15

3.7 Extendable Swap Similar to the double-up swap except that the swap provider has the option to extend the period of the swap for a predetermined period

16

4 Caps, Floors and Collars Caps provide price protection for the buyer above a predetermined level for a predetermined period of time Floors guarantee the minimum price that will be paid or received at a predetermined level A collar is a combination of a long position in a cap and a short position in a floor

17

A generic cap can be viewed as a portfolio of standard European call options with strike prices equal to the cap level and maturity dates equal to the settlement dates of the cap Value of a standard cap is given by

18

Similarly, a generic floor is a portfolio of European put options with strike prices equal to the floor level and maturity dates equal to the settlement dates of the floor Value of a floor is given by

19

Collars are typically used by energy buyers who wish to hedge against price increases and wish to use the premium on short floors to pay for the cap protection The strike prices of the cap and floor can be set to yield a collar at zero cost

20

5 Swaptions A swaption is a European option on an energy swap A call option on the swap, also called a payer swaption, with strike price K and time to maturity T, provides the holder of the option the right to enter into a swap, paying the fixed price K and receiving the floating energy spot price A put option on a swap, or receiver swaption, gives the purchaser of the option the right to sell a swap or receive the fixed price K and pay the floating price

21

The payoff to the payer swaption as The value of the payer swaption is

22

If physical settlement considered Payoff Value

23

6 Compound Options-Captions and Floptions An option which allows its holder to purchase or sell another option for a fixed price is called a compound option A caption is an option on a cap and a floption is an option on a floor These instruments are options on portfolios of options and no simple analytical formulae exist

24

7 Spread and Exchange Options 7.1 Calendar Spreads If the futures contracts are written on the same underlying energy, but with different maturity dates, then the option is often referred to as a calendar spread option Payoff to a European call spread option with strike K and maturity T as

25

Value of the calendar spread option

26

7.2 Crack Spreads If the futures contracts underlying the option are written on two separate energies, then the option is often referred to as a crack spread option. The maturity of the futures contracts can be on the same date or different dates Options of this type are often used by companies who are exposed to the difference in price between two different energies

27

Payoff Value

28

7.3 Exchange Options Provide a payout which is based on the relative performance of two energy prices Two types: a) out-performance options ’ payoff b)

out-performance options ’ payoff b)")

29

8 Path Dependent Options 8.1 Asian Options-Average Price and Average Strike Asian options are options whose final payoff is based in some way on the average level of an energy price during some or all of the life of the option In general, the main use of Asian options is hedging an exposure to the average price over a period of time

31

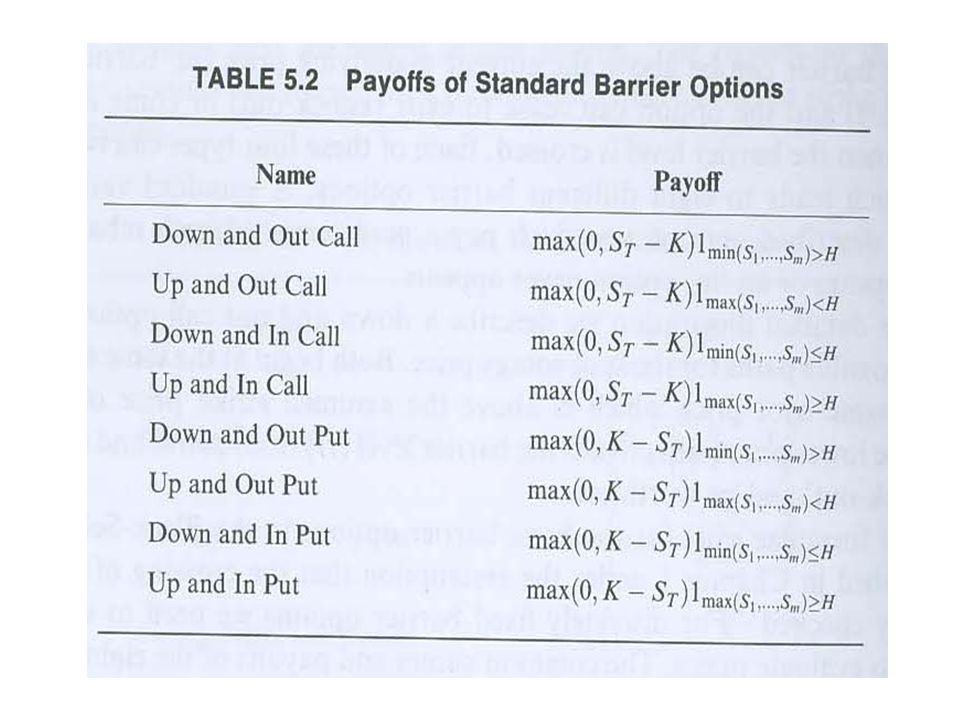

8.2 Barrier Options Barrier options are standard options that either cease to exist or only come into existence if the underlying price crosses a predetermined level – the barrier Analytical formulae exist for the basic barrier options in the Black-Scholes-Merton world under the assumption that the crossing of the barrier is continuously checked. For discretely fixed barrier options we need to use numerical techniques to evaluate prices

34

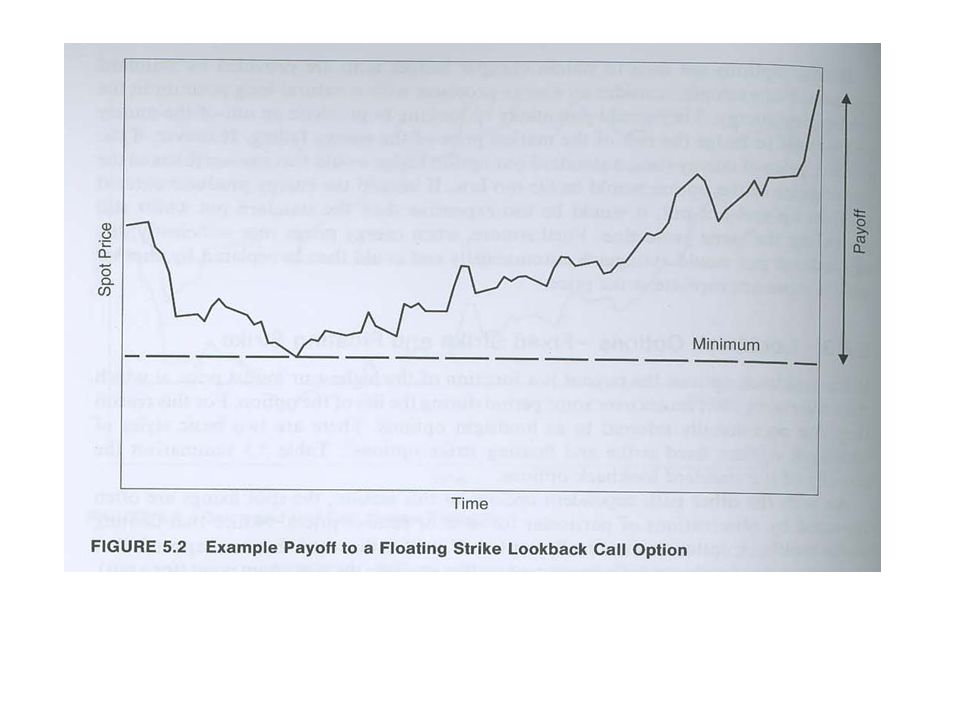

8.3 Lookback Options-Fixed Strike and Floating Strike The payout of lookback options is a function of the highest or lowest price at which the underlying asset trades over some period during the life of the option. For this reason, they are occasionally referred to as hindsight options Analytical formulae exist for the standard lookback options in a Black-Scholes-Merton world when the maximum or minimum is checked continuously, but numerical techniques must be used for discretely fixed examples

37

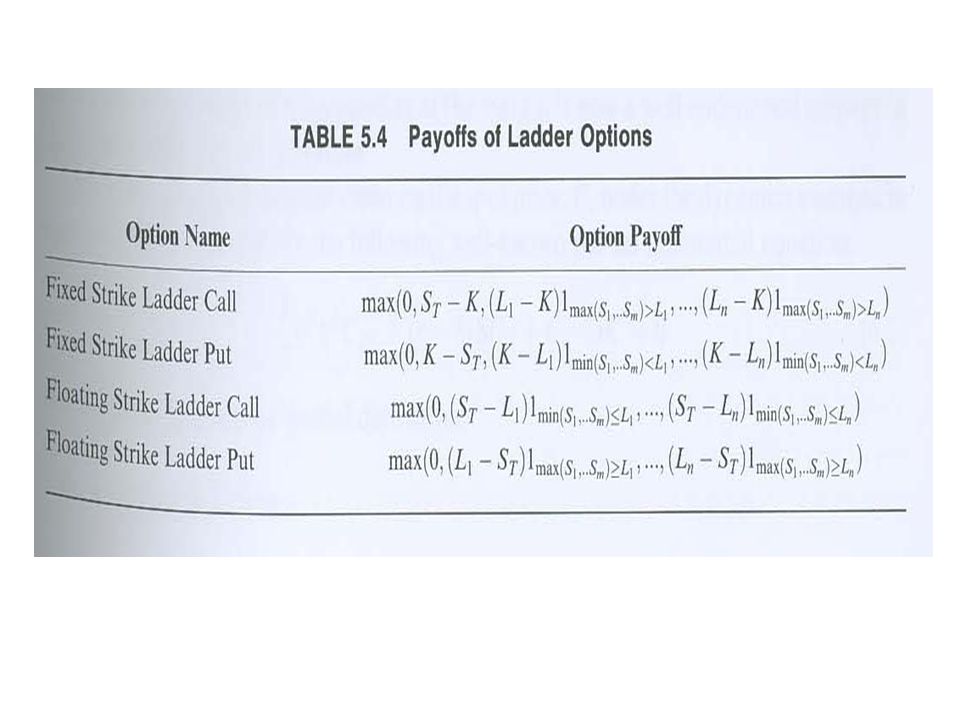

8.4 Ladder and Cliquet Options Ladder options have a predefined set of levels such that if the underlying price crosses a particular level it locks in a minimum payoff equal to the difference between the level crossed and the strike price

40

Cliquet options have a predefined set of dates at which the underlying price is observed and they payoff the maximum of the differences between these fixings and the predefined strike price for a call or the maximum of the differences between the predefined strike price and the fixings for a put

41

9 Summary Exotic options are almost common place in the energy markets compared with other markets The high volatility exhibited by many energy commodities and the fact that they have been embedded in many energy contracts for a long time has led to a ready acceptance for these kinds of derivatives

42

THE END THANK YOU!

Similar presentations

Eurodollar futures options.>")