Download presentation

Presentation is loading. Please wait.

1

Public Sector Economics Tax Incidence

2

Private Sector Response to Public Redistribution price changes –partial equilibrium –general equilibrium migration altruism insurance markets

3

Outline of Topics partial equilibrium –excise tax theory elastic agents bear less principle of comprehensive cost –cigarette tax incidence general equilibrium theory capital tax incidence incidence of taxes and spending by –income group –cohort social security paternalism

4

industry cost curve industry demand B/C = depends only on dp/dt Tax on Demanders pre-tax price after-tax price no-tax price A B D B+D = borne by demanders F C E C+E = borne by suppliers D+E = dwc B+C = government revenue

5

industry cost curve industry demand B/C = depends only on dp/dt Tax on Demanders pre-tax price after-tax price no-tax price A B D B+D = borne by demanders F C E C+E = borne by suppliers D+E = dwc B+C = government revenue

6

Partial Equilibrium Model general results –“elastic agents bear less” –doesn’t matter whether the tax is levied on the buyer or seller special results –only supply and demand elasticities matter –only suppliers and demanders in the taxed market are affected –both suppliers and demanders are harmed by the tax

7

Incidence in the “Long Run” “long run” = capital can adjust if capital is elastically supplied in the long run, than capital will not bear the burden of taxes theories of the supply of capital –international trade –economic growth theories

8

Descriptions of Policy Incidence dimensions of government redistribution –income classes –age/year of birth –factor ownership –occupation instruments of redistribution –taxes –spending –regulation

9

Pechman’s Study of Tax Incidence people distinguished only by their annual income statutory incidence only –savings and work are fixed –consumption patterns are fixed, and do not vary by income class –variety of assumptions regarding incidence of corporate income, property, and payroll taxes IIT: 100% on payer sales and excise: 100% on consumers payroll tax: 75-100% on workers property tax: 100% on landholders and/or capital owners corporate income: variety MERGE files –start with CPS –for filing population, use Form 1040 income information for “similar” families in the IRS database –CPS necessary because it is a random sample benchmark: proportional income tax

10

Pechman’s Study of Tax Incidence: Results no significant difference from flat tax, except at very top and bottom results for top and bottom are mild, and vary across incidence models transfers –appear very progressive in Pechman –but Social Security is a big part of transfers, and is not so progressive w.r.t. lifetime income

11

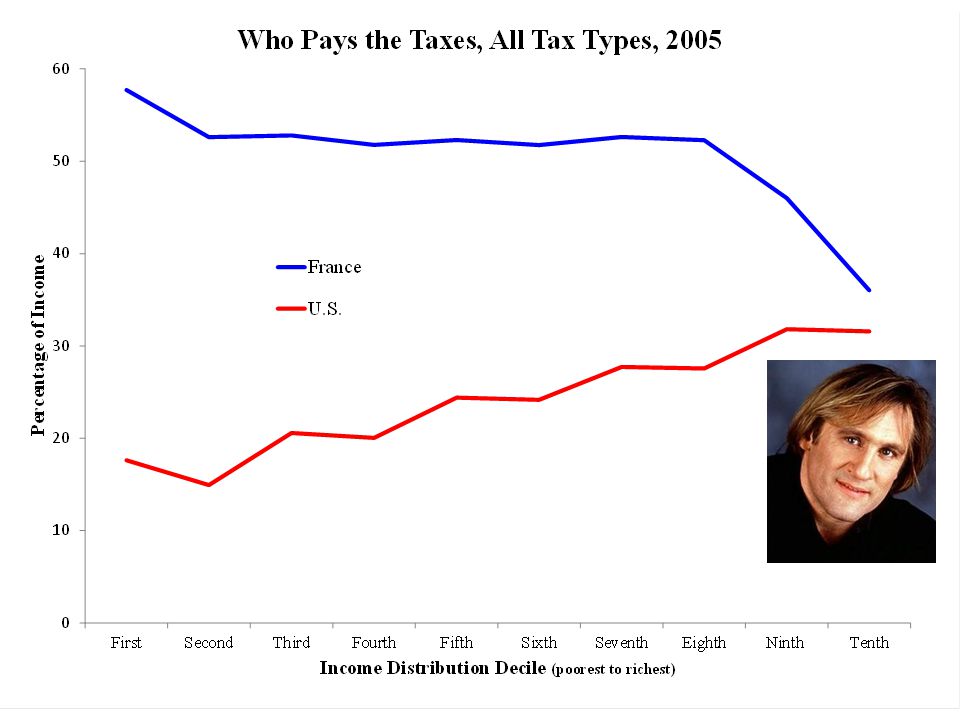

Regressive Taxes in Western Europe Western European countries –known for their generous welfare states –Sometimes known for progressive income taxes However, income tax is not the only tax especially in Western Europe Other taxes –payroll taxes, sales taxes, excise taxes, property taxes –often are regressive Western European taxes are more regressive because they are less income-tax intensive

15

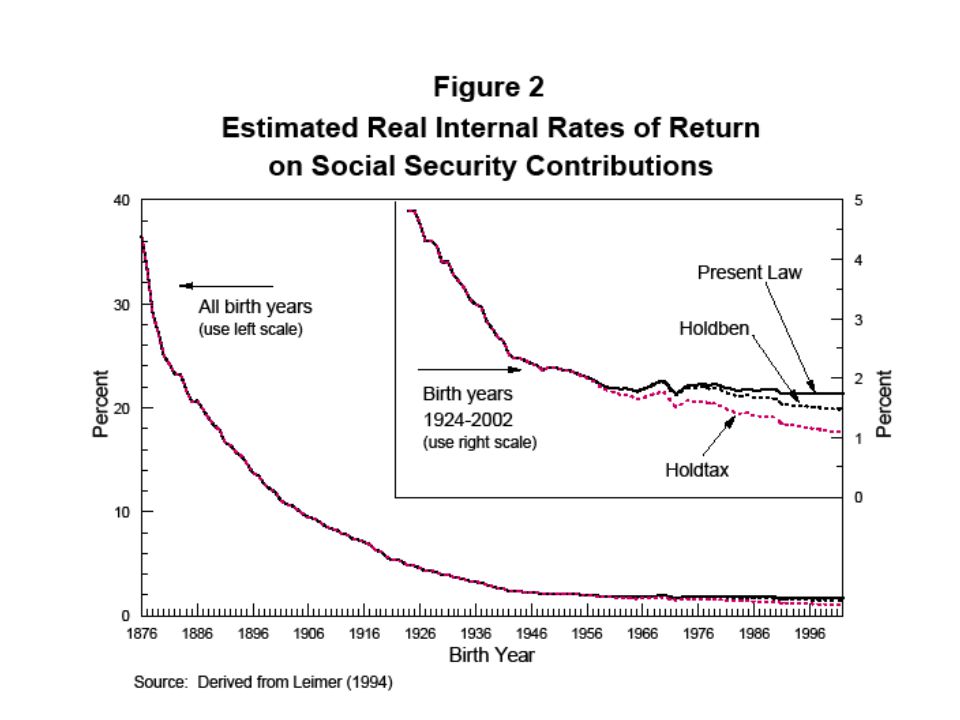

Calculating the Income Incidence of Social Security annual cross-sections show the “poor” receive most of the SS expenditures, but do not pay much of taxes –eg., Musgrave et al (1974, Table 6) –generational accounting = focus on age-dimension rather than income dimension –stratify by both income and year of birth what is the lifetime relation between income and years spent in school? payroll tax caps some portion of benefits may be paid from general revenue. Is the general tax system progressive? payroll tax rates across occupations

16

Calculating the Income Incidence of Social Security (cont’d) special treatment of government employees –do they tend to be rich or poor? –is the supply of government employees competitive? benefit receipt often requires knowledge of eligibility and/or infrastructure –not the same with tax payments –is knowledge correlated with lifetime income? differential valuation of benefits legislative exclusions –minorities. eg., Jamaica, Rhodesia, South Africa –nonunion members –agriculture –trend is toward eliminating exclusions

17

Calculating the Income Incidence of Social Security (cont’d) progressivity of the annual benefit formula SS OASDI paid as a life annuity –more life –> more benefits received –what is the relation between lifetime income and mortality? health benefits paid as reimbursement for medical procedures, etc. –more life –> more benefits received –when alive, more visits to doctor/hospital –> more benefits received –what is the relation between visits and lifetime income? years-of-participation rules for eligibility; SI incidence SS crowds out other (more progressive?) public programs

public programs.")

18

Generational Accounting date of birth accounts –each cohort’s NPV of taxes - transfers, forward from birth –for a self-financed transfer program with negligible admin costs, sum to PV zero across cohorts (including unborn and deceased cohorts in the sum) –more generally cohort sum to PV of (past & present) gov. purchases what is the incidence of these purchases? –can be expressed as: $ per cohort member $ per NPV of taxes (Kotlikoff critique) IRR remaining lifetime accounts (Kotlikoff) –each cohort’s NPV of taxes & benefits, forward from today –sum across cohorts to debt value + PV of future purchases –based entirely on estimates of future tax & transfer rules

IRR remaining lifetime accounts (Kotlikoff) –each cohort’s NPV of taxes & benefits, forward from today –sum across cohorts to debt value + PV of future purchases –based entirely on estimates of future tax & transfer rules.")

20

IRR as a measure of Generational Incidence

21

Magic Trick 1: Combine SS with Profitable Government Enterprise SSA (NPV = 0) Profitable Enterprise (NPV > 0)

Profitable Enterprise (NPV > 0)")

22

Magic Trick 1: Combine SS with Profitable Government Enterprise SSA (NPV = 0) Profitable Enterprise (NPV > 0)

Profitable Enterprise (NPV > 0)")

23

“REFORMED” SSA that can spend more than it taxes Magic Trick 1: Combine SS with Profitable Government Enterprise

24

Generational Accounts Feature Present Values

25

Generational Accounting – Some Results large redistribution in the age dimension –from postwar generations to prewar generations (eg., Leimer) –from unborn generations to current generations (Kotlikoff) –old age public pensions are the main mechanism –education spending hardly reverses this –current laws in most, but not all, countries (among those studied) imply redistribution from unborn generations other (obvious) results –cutting OASDI benefits hurts older generations –raising the sales tax to finance constant OASDI benefits hurts younger generations less than raising the payroll tax –unavoidable legacy

–from unborn generations to current generations (Kotlikoff) –old age public pensions are the main mechanism –education spending hardly reverses this –current laws in most, but not all, countries (among those studied) imply redistribution from unborn generations other (obvious) results –cutting OASDI benefits hurts older generations –raising the sales tax to finance constant OASDI benefits hurts younger generations less than raising the payroll tax –unavoidable legacy")

26

Social Security Reforms unavoidable legacy: since older cohorts, younger cohorts must do poorly unless –NPV’s do not sum to zero –ie, combine Social Security with a profitable government enterprise viable government enterprises? –buying stocks and selling bonds –reducing tax distortions has positive NPV –charging for immigration what is the connection between the government enterprise and SS? Would the enterprise be profitable without SS? example: letting SS earn the pretax return = reducing capital taxes

27

Distortions and Redistribution are distortions a necessary but unintended byproduct of redistribution? –standard public finance view –but why are “strings attached” to the transfers? –can this apply to “universal” participation programs? is redistribution a necessary but unintended byproduct of distortion? –paternalism –correcting market failures –producer interests –tax incidence is very different distinguishing these models –compare magnitude of distortions with magnitude of redistribution –look at take-up rates –are distortions in the direction of luxury or inferior goods? –is the statutory incidence against the poor? –what determines the markets for intervention?

28

Three Versions of Paternalism consumption-based paternalism –literal consumption externality/merit good/impure altruism information-based paternalism –arises from pure altruism –disagreement about the probability of various contingencies –but is force necessary? Why not communicate the information? strategically-induced paternalism –arises from pure altruism, and the timing of decisions –e.g., Samaritan’s Dilemma, parents relying on their children for elderly support –unfunded mandate enhances efficiency, while helping the Samaritan at the expense of the beneficiary

29

Three Versions of Paternalism consumption-based paternalism –literal consumption externality/merit good/impure altruism information-based paternalism –arises from pure altruism –disagreement about the probability of various contingencies –but is force necessary? Why not communicate the information? strategically-induced paternalism –arises from pure altruism, and the timing of decisions –e.g., Samaritan’s Dilemma, parents relying on their children for elderly support –unfunded mandate enhances efficiency, while helping the Samaritan at the expense of the beneficiary

30

Strategically-Induced Paternalism consumption over time: c 1 and c 2 –superscripts r, p still indicate rich poor second stage –rich make voluntary transfer to the poor –poor consume the sum of their savings and this transfer –no government at this stage –savings from previous period denoted m r and m p –second stage decision rules are: –assume: the rich are altruistic enough, and/or poor are poor enough –> positive and equal partial derivatives of c 2 p (m p,m r ) in the interval (0,1)

in the interval (0,1)")

31

Strategically-Induced Paternalism consumption over time: c 1 and c 2 –superscripts r, p still indicate rich poor second stage –rich make voluntary transfer to the poor –poor consume the sum of their savings and this transfer –no government at this stage –savings from previous period denoted m r and m p –second stage decision rules are: –assume: the rich are altruistic enough, and/or poor are poor enough –> positive and equal partial derivatives of c 2 p (m p,m r ) in the interval (0,1)

in the interval (0,1)")

32

Strategically-Induced Paternalism (cont’d) first stage –rich and poor separately choose their savings, looking ahead to the effect of their savings on future consumption –government may be regulating, or taxing, at this stage –without government, rich have objective –compare with

first stage –rich and poor separately choose their savings, looking ahead to the effect of their savings on future consumption –government may be regulating, or taxing, at this stage –without government, rich have objective –compare with")

33

Strategically-Induced Paternalism (cont’d) first stage –rich and poor separately choose their savings, looking ahead to the effect of their savings on future consumption –government may be regulating, or taxing, at this stage –without government, rich have objective –compare with

first stage –rich and poor separately choose their savings, looking ahead to the effect of their savings on future consumption –government may be regulating, or taxing, at this stage –without government, rich have objective –compare with")

34

Differential Valuation if paternalism is operative, differential valuation is necessarily an exercise in extrapolation “structural” approach –build a numerical model of demand –choose utility parameters (or demand elasticities) –calculate compensating variation or consumer surplus prices from secondary markets –resale of in-kind transfers. but is the existence of a resale market consistent with paternalism? –hedonics. also applicable when differential valuation derives from the public production function (eg., public housing) –contingent valuation

–contingent valuation.")

Similar presentations