Download presentation

Presentation is loading. Please wait.

1

January and February 2015 Insurance and Benefits Management

2

Insurance provided to employees is determined by Collective Bargaining with the Unions ◦ TALC Article 14, SPACL Article 13 ◦ Board Contribution (a.k.a. “Board Flex”) $6372 per year ◦ Board Paid Life Insurance - $20,000 Insurance Task Force (TALC 14.09, SPALC 13.09) ◦ Representation 8 Union Representatives (4 TALC, 4 SPALC) 8 Management Representatives ◦ Purpose: to review current insurance programs and to explore alternatives, improvements, changes, and specifications to the existing insurance programs. ◦ Meets monthly

$6372 per year ◦ Board Paid Life Insurance - $20,000 Insurance Task Force (TALC 14.09, SPALC 13.09) ◦ Representation 8 Union Representatives (4 TALC, 4 SPALC) 8 Management Representatives ◦ Purpose: to review current insurance programs and to explore alternatives, improvements, changes, and specifications to the existing insurance programs. ◦ Meets monthly.")

3

RFPs (Request for Proposals) ◦ Draft RFP with specifications for the insurance being sought. ◦ Release RFP to vendors. ◦ Vendors provide responses. ◦ Responses are evaluated by ITF Subcommittee. ◦ Recommendation is taken to the full ITF Committee. ◦ ITF recommendation is taken to the Board. ◦ Board takes final action to award the contract. ◦ I&B implements plans selected.

7

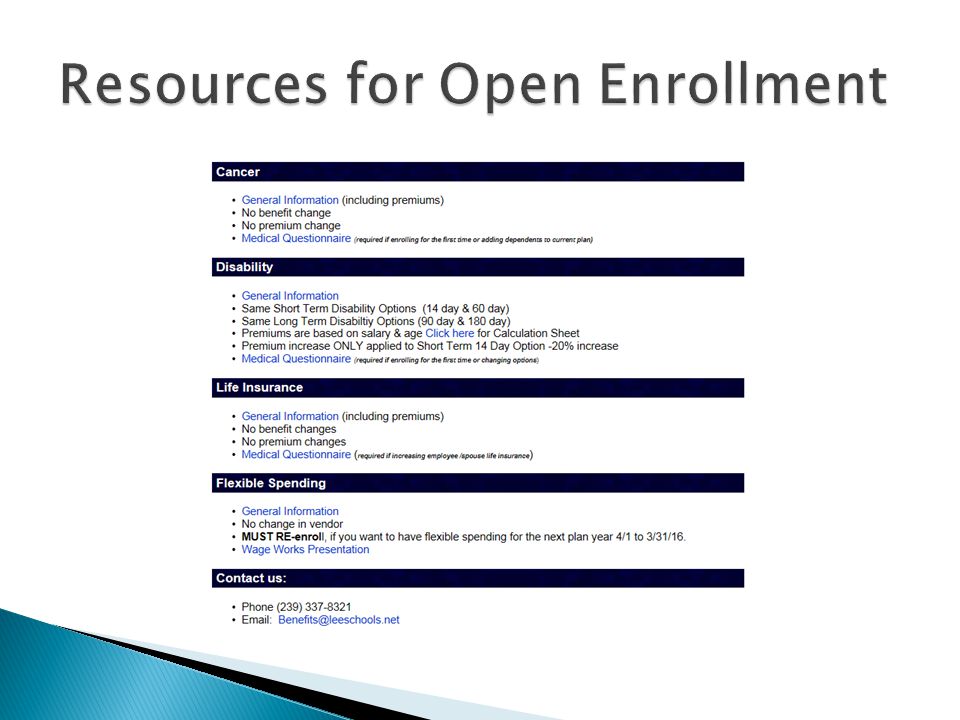

Dental: Humana ◦ Same plans, HMO: same rates, PPO: 3% rate increase Vision: Avesis ◦ Same Plan, 1.3% rate decrease Cancer and Other Specified Disease: AllState ◦ Same plan options, same rates ◦ Evidence of Insurability (EOI) form REQUIRED if making any changes. Life Insurance: Minnesota Life ◦ Same plan options, same rates ◦ Evidence of Insurability (EOI) form REQUIRED if making any changes.

form REQUIRED if making any changes..")

8

Disability: Reliance Standard ◦ Same plan options Short Term Disability (14-day or 60-day elimination) Long Term Disability (90-day or 180-day elimination) ◦ Rates for Long Term and 60-day Short Term remain the same. ◦ Rates for 14-day Short Term increase 20% ◦ Disability is calculated based on age and current salary. ◦ Evidence of Insurability (EOI) form REQUIRED if making any changes.

form REQUIRED if making any changes..")

9

Flexible Spending: WageWorks ◦ Adjudication of claims is industry standard and will continue. This protects both the employee and the District. ◦ No cost to the employee to participate ◦ Employee elects amount to be set aside for qualified expenses. ◦ IRS increased the annual maximum contribution to $2,550. ◦ Requires Annual Election

10

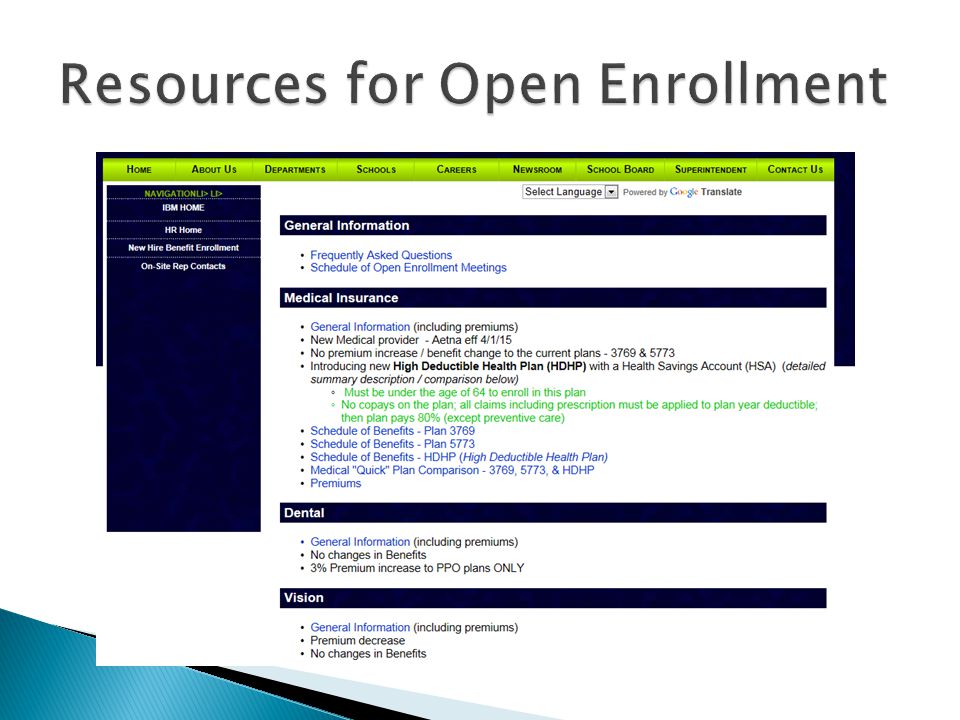

New Vendor: Aetna effective April 1, 2015 New Onsite Representative – Kim Murphy Two current plans (Plan 5773 and Plan 3769) ◦ Same coverage ◦ Same rates New Plan Option: High Deductible Health Plan with a Health Savings Account.

◦ Same coverage ◦ Same rates New Plan Option: High Deductible Health Plan with a Health Savings Account.")

11

Fill current prescriptions NOW with Florida Blue! ◦ Filled at the 54 day mark ◦ Receive 90 days of medication ◦ 130+ days (4+ months) of medication on hand New prescription drug provider: Aetna Rx File Transfer of current prescription from Prime to Aetna Rx Ineligible transfers ◦ Certain medications legally prohibited from transfer ◦ Expired prescriptions ◦ Prescriptions with no more refills Mandatory Generics, mandatory mail, etc. still applicable Maintenance Options ◦ Aetna Rx Mail Order ◦ CVS Option Mandatory mail prescriptions available for pick up at CVS 90 day (3X) supply 2X copay

of medication on hand New prescription drug provider: Aetna Rx File Transfer of current prescription from Prime to Aetna Rx Ineligible transfers ◦ Certain medications legally prohibited from transfer ◦ Expired prescriptions ◦ Prescriptions with no more refills Mandatory Generics, mandatory mail, etc. still applicable Maintenance Options ◦ Aetna Rx Mail Order ◦ CVS Option Mandatory mail prescriptions available for pick up at CVS 90 day (3X) supply 2X copay.")

13

Different “plan type” than what has been offered by SDLC in the past. It is like a 401K for medical needs ◦ Money is put aside pre-tax. ◦ Employer (District) money is added to the account each pay period. ◦ Money is withdrawn tax-free for qualified expenses. IRS determines which expenses are “qualified”. Same list as the Flexible Spending Accounts. Eligible dependents are defined by IRS, NOT the health plan.

money is added to the account each pay period. ◦ Money is withdrawn tax-free for qualified expenses. IRS determines which expenses are qualified . Same list as the Flexible Spending Accounts. Eligible dependents are defined by IRS, NOT the health plan..")

14

Must meet deductible for all services, including Rx, except in-network preventative care, before benefits apply. You pay Deductible/Coinsurance for all services (including Rx) except preventative care. NO COPAYs APPLY for any services, including drug copays. Members are responsible for the full cost of the Aetna contracted (discounted) rate. Employees with Family coverage (covering at least one other person on the plan) must meet the FAMILY deductible before any benefits are payable for non-preventative services.

except preventative care. NO COPAYs APPLY for any services, including drug copays. Members are responsible for the full cost of the Aetna contracted (discounted) rate. Employees with Family coverage (covering at least one other person on the plan) must meet the FAMILY deductible before any benefits are payable for non-preventative services..")

15

To be eligible for an HSA, you: Must be covered under a high deductible health plan. Must have no other health coverage. Must be 63 or younger to enroll. Must not be enrolled in Medicare (EE or dependents). Must not be claimed as a dependent on some else’s tax return. Must not have a standard (or full purpose) Flexible Spending Account (FSA) or HRA. AND Your spouse must not have a full purpose FSA.

. Must not be claimed as a dependent on some else’s tax return. Must not have a standard (or full purpose) Flexible Spending Account (FSA) or HRA. AND Your spouse must not have a full purpose FSA..")

16

Plan 3769 and 5773 are the same plan at the same rates for the next plan year. ◦ District Contributes $6372 per year ($265.50 per pay) toward employee medical premiums. If HDHP/HSA is elected, employee still receives the $6372 per year, but split between premium and the HSA. $4,887.60 toward premium ($203.65 per pay) $1484.40 into the HSA ($61.85 per pay)

toward employee medical premiums. If HDHP/HSA is elected, employee still receives the $6372 per year, but split between premium and the HSA. $4, toward premium ($ per pay) $ into the HSA ($61.85 per pay).")

17

In-Network Deductibles (Employee/Family) ◦ 3769 Plan: $500/$1,500 ◦ 5773 Plan: $1000/$3,000 ◦ HDHP Plan: $2,500/$5,000 Out of Pocket Maximums (Employee/Family) ◦ 3769 Plan: $3,000/$6,000 ◦ 5773 Plan: $4,000/$8,000 ◦ HDHP Plan: $6,250/$12,500 Maximum HSA Contribution (2015) ◦ $3,350 Individual (employee only) ◦ $6,650 Family (employee + anyone)

◦ 3769 Plan: $500/$1,500 ◦ 5773 Plan: $1000/$3,000 ◦ HDHP Plan: $2,500/$5,000 Out of Pocket Maximums (Employee/Family) ◦ 3769 Plan: $3,000/$6,000 ◦ 5773 Plan: $4,000/$8,000 ◦ HDHP Plan: $6,250/$12,500 Maximum HSA Contribution (2015) ◦ $3,350 Individual (employee only) ◦ $6,650 Family (employee + anyone)")

18

Employees can use only the amount in their account at the time of service. Owned and controlled by employee, portable, not forfeited, at termination, or if you change medical plans. Employee decides how to invest and spend the money. ◦ Pay for current qualified medical, dental and vision expenses. ◦ Save for future medical and retirement health care expenses that won’t be subject to federal tax. Accumulated HSA funds rollover Triple tax advantage ◦ Contributions (individuals/employers) are tax exempt ◦ No taxes on qualified withdrawals ◦ No taxes on account interest and earnings

are tax exempt ◦ No taxes on qualified withdrawals ◦ No taxes on account interest and earnings.")

19

Currently,$265.50 per check is added to your check under the “Board Flex” code. Medical, Dental, Vision, and Cancer Insurance are deducted pre-tax. Life Insurance and Disability Insurance are deducted post-tax. If you elect the HDHP/HSA, your paycheck will look different. ◦ Board Flex will be $203.65 (instead of $265.50) ◦ The balance of the Board Contribution ($61.85) will be a new row titled “HSA” under “Employer Paid Benefits” box

◦ The balance of the Board Contribution ($61.85) will be a new row titled HSA under Employer Paid Benefits box.")

20

TiersPlan 3769Plan 5773 High Deductible Health Plan (HDHP)** Employee Only$272.70$255.96$203.65 Employee / Spouse $660.33$618.21$552.35 Employee / Child $409.70$384.00$326.89 Employee / Children $574.56$538.06$475.20 Employee/ Family $832.43$779.04$707.17

** Employee Only$272.70$255.96$ Employee / Spouse $660.33$618.21$ Employee / Child $409.70$384.00$ Employee / Children $574.56$538.06$ Employee/ Family $832.43$779.04$707.17")

21

Employee Only - Low Cost Scenario Service # of Services Covered Amount Total Cost 2015 Employee Cost 37695773HSA HSA Fund $0 $1,484 Preventive Visit (Well Adult)1$220 $0 PCP OV (sick visit)1$100 $25$35$100 Specialist OV1$160 $60$85$160 Generic - Retail1$25 $0 $25 Brand Formulary - Retail2$110$220$50 $220 Employee Subtotal $725$135$170$505 HSA Used $505 Total Employee OOP Expense $725$135$170$0 Annual Premium $173$0 HSA Balance $979 True Employee OOP Cost with Premium $308$170$0 Assumes services are in-network, occur sequentially, and all ER HSA contributions are available at the time of service.

1$220 $0 PCP OV (sick visit)1$100 $25$35$100 Specialist OV1$160 $60$85$160 Generic - Retail1$25 $0 $25 Brand Formulary - Retail2$110$220$50 $220 Employee Subtotal $725$135$170$505 HSA Used $505 Total Employee OOP Expense $725$135$170$0 Annual Premium $173$0 HSA Balance $979 True Employee OOP Cost with Premium $308$170$0 Assumes services are in-network, occur sequentially, and all ER HSA contributions are available at the time of service.")

22

Employee Only - High Cost Scenario Service # of Services Covered Amount Total Cost 2015 Employee Cost 37695773HSA HSA Fund $0 $1,484 Preventive Visit (Well Adult)1$220 $0 PCP OV (sick visits)3$100$300$75$105$300 Specialist OV (Orthopedic Surgeon)3$160$480$180$255$480 IP Hospital (3 days); Musculoskeletal1$25,000 $2,745$3,640$4,048 Physical Therapy20$95$1,900$0 $172 Generic - Retail10$25$250$0 $50 Brand Formulary - Retail2$110$220$0 $44 Employee Subtotal $28,370$3,000$4,000$5,094 HSA Used $1,484 Total Employee OOP Expense $28,370$3,000$4,000$3,610 Annual Premium $173$0 HSA Balance $0 True Employee OOP Cost with Premium $3,173$4,000$3,610 Assumes services are in-network, occur sequentially, and all ER HSA contributions are available at the time of service.

1$220 $0 PCP OV (sick visits)3$100$300$75$105$300 Specialist OV (Orthopedic Surgeon)3$160$480$180$255$480 IP Hospital (3 days); Musculoskeletal1$25,000 $2,745$3,640$4,048 Physical Therapy20$95$1,900$0 $172 Generic - Retail10$25$250$0 $50 Brand Formulary - Retail2$110$220$0 $44 Employee Subtotal $28,370$3,000$4,000$5,094 HSA Used $1,484 Total Employee OOP Expense $28,370$3,000$4,000$3,610 Annual Premium $173$0 HSA Balance $0 True Employee OOP Cost with Premium $3,173$4,000$3,610 Assumes services are in-network, occur sequentially, and all ER HSA contributions are available at the time of service.")

23

Employee + Family - Low Claims Scenario Service # of Services Covered Amount Total Cost 2015 Employee Cost 37695773HSA HSA Fund $0 $1,484 Preventive Visit (2 Well Adult; 2 well child) 4$220$880$0 PCP OV (sick visits)2$100$200$50$70$200 Specialist OV2$160$320$120$170$320 Generic - Retail12$25$300$0 $300 Employee Subtotal $1,700$170$240$820 HSA Used $820 Total Employee OOP Expense $1,700$170$240$0 Annual Premium $13,606$12,324$12,085 HSA Balance $664 True Employee OOP Cost with Premium $13,776$12,564$12,085 Assumes services are in-network, occur sequentially, and all ER HSA contributions are available at the time of service.

4$220$880$0 PCP OV (sick visits)2$100$200$50$70$200 Specialist OV2$160$320$120$170$320 Generic - Retail12$25$300$0 $300 Employee Subtotal $1,700$170$240$820 HSA Used $820 Total Employee OOP Expense $1,700$170$240$0 Annual Premium $13,606$12,324$12,085 HSA Balance $664 True Employee OOP Cost with Premium $13,776$12,564$12,085 Assumes services are in-network, occur sequentially, and all ER HSA contributions are available at the time of service.")

24

Employee + Family - High Cost Scenario Service # of Services Covered Amount Total Cost 2015 Employee Cost 37695773HSA HSA Fund $0 $1,484 (4) Preventive Visits (2 Well Adult; 2 well child) 4$220$880$0 PCP OV (sick visits)3$100$300$75$105$300 Specialist OV (Cardiologist, Endorinologist) 11$160$1,760$660$935$1,760 Inpatient Hospital (4 days) - heart attack1$185,000 $2,340$3,065$7,940 Generic - Retail24$25$600$0 $120 Brand Rx Retail *24$145$3,480$600 $696 Employee Subtotal $192,020$3,075$4,705$10,816 HSA Used $1,484 Total Employee OOP Expense $192,020$3,075$4,705$9,332 Annual Premium $13,606$12,324$12,085 HSA Balance $0 True Employee OOP Cost with Premium $16,681$17,029$21,416 Assumes services are in-network, occur sequentially, and all ER HSA contributions are available at the time of service.

Preventive Visits (2 Well Adult; 2 well child) 4$220$880$0 PCP OV (sick visits)3$100$300$75$105$300 Specialist OV (Cardiologist, Endorinologist) 11$160$1,760$660$935$1,760 Inpatient Hospital (4 days) - heart attack1$185,000 $2,340$3,065$7,940 Generic - Retail24$25$600$0 $120 Brand Rx Retail *24$145$3,480$600 $696 Employee Subtotal $192,020$3,075$4,705$10,816 HSA Used $1,484 Total Employee OOP Expense $192,020$3,075$4,705$9,332 Annual Premium $13,606$12,324$12,085 HSA Balance $0 True Employee OOP Cost with Premium $16,681$17,029$21,416 Assumes services are in-network, occur sequentially, and all ER HSA contributions are available at the time of service.")

Similar presentations

Presented by: Cafro Agency, LLC David L. Cafro, CIC (860) 779-DAVE.>")

Everything You Need to Know.>")

with HSA Effective July 1, 2009.>")

Everything You Need to Know.>")

with a Health Savings Account (H S A)>")

Health Savings Account (HSA)>")