Download presentation

Presentation is loading. Please wait.

1

How Can We Get Medications for the Underinsured and How Should We Deal with Denials From Insurance Companies? Mark T. Osterman, MD MSCE Assistant Professor of Medicine University of Pennsylvania

2

Disclosures Advisory board for Janssen, Abbvie, UCB Research grant support from UCB

3

Outline Definitions / statistics –Uninsured, underinsured, cost sharing Affordable Care Act Medicare / Medicaid Special considerations –Age 26, end of year, insurance / job loss Non-government patient assistance –CCFA, letters / data, hospitals, pharma, charitable organizations, clinical trials Persistence

4

Thanks to My Friends Peter Higgins Corey Siegel Jim Lewis Laura Wingate Dorothy Williams & Michelle Grainger

5

Definitions Uninsured: no insurance of any kind Underinsured: insured all year but not enough, or more specifically –Medical expenses > 10% of annual income –Annual income 5% of annual income –Deductibles > 5% of annual income Cost sharing: payment of health care by both patient and insurance company Schoen C et al, Health Aff 2005

6

Cost Sharing Deductible –Amount you pay before insurance starts to pay –Still have to pay the copay Coinsurance –Your share of costs of health care services (%) –You pay this after deductible met Copay –Fixed amount you pay for a health care service –Varies with type of service

–You pay this after deductible met Copay –Fixed amount you pay for a health care service –Varies with type of service")

9

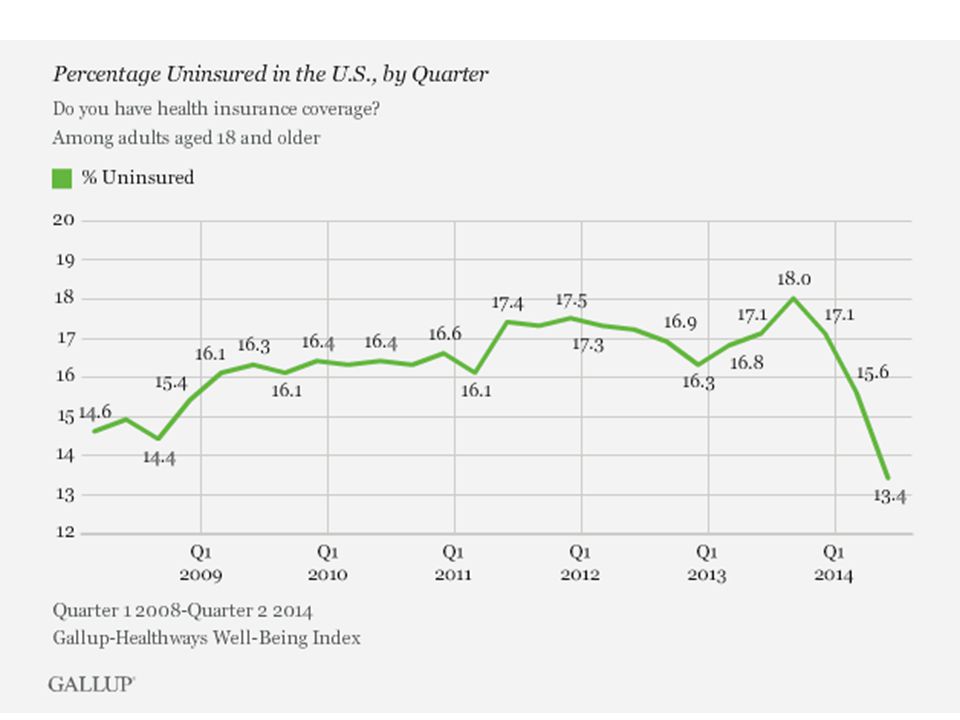

Statistics In 2012, 32 million < 65 underinsured –47 million uninsured, so total 79 million By state –Uninsured (2012) <10%: MA, HI, MN, DE, VT, DC, CT, NY, RI, IA, ND, WI >15%: TX, NV, FL, AZ, WY, NM, NC, GA, AL, AK –Uninsured + underinsured (2012): Low: MA – 14% High: ID, FL, NV, NM, TX – 36-38% www.commonwealthfund.org Henry J. Kaiser Family Foundation

10

Why the Lack of Insurance Limited income Demographics –Hispanic, remote rural, low education, religion Unemployment / underemployment Employers do not provide health benefits High premium / deductible / coinsurance –Cost sharing: move burden to patient Restricted benefits Youth: feel invincible, limited income www.Medicare.gov

11

Affordable Care Act Enroll 10/1/13 – 3/31/14, 11/15/14 – 2/15/15 –Special enrollment period if miss deadline Require most to have health insurance –Tax penalty unless exempt (>8% of income, no filing, hardship, short gap, religion, Indian, jail) Employers –Require larger business (> 200 employees) to offer coverage to all –Tax credit to small business (< 25 employees) –Exchanges through which smaller business (< 100 employees) can purchase coverage www.hhs.gov

Employers –Require larger business (> 200 employees) to offer coverage to all –Tax credit to small business (< 25 employees) –Exchanges through which smaller business (< 100 employees) can purchase coverage")

12

Special Enrollment Period Signed up but unable to complete enrollment Marriage Having, adopting, or placement of child Permanent move to new area with different health plan options Losing other health coverage Change in eligibility for premium credits / cost- sharing subsidies Newly gaining legal US resident status Government error during enrollment process Health plan violates contract www.hhs.gov

13

Affordable Care Act Expand Medicaid to all non-Medicare-eligible <65 with income < 133% of fed poverty level –States 100% fed funded 2014-16, 90% by 2020 Extend funding for CHIP State-based American Health Benefit Exchanges through which people can buy coverage Premium credits and cost-sharing subsidies with income 100-400% of fed poverty level No pre-existing condition exclusions except for grandfathered plans (purchased before 3/23/10) No lifetime limit on coverage for most benefits www.hhs.gov

No lifetime limit on coverage for most benefits")

14

Affordable Care Act ↓ in uninsured by 10 million in 2014 May not be as dramatic next year (“low- hanging fruit” captured in 2014) Those without insurance the longest may be most difficult to get signed up Other obstacles –Residence in remote areas –Lack of internet access –Less education –Not up to date with news Young J, Huffington Post 2014

Those without insurance the longest may be most difficult to get signed up Other obstacles –Residence in remote areas –Lack of internet access –Less education –Not up to date with news Young J, Huffington Post 2014")

15

Affordable Care Act Plans PlanCoverage / Costs Catastrophic<30 who cannot afford other coverage Must qualify for hardship exemption BronzeCovers ~60% Lowest premium, highest out-of-pocket costs SilverCovers ~70% Lower premium, higher out-of-pocket costs Premium credits / cost-sharing subsidies GoldCovers ~80% Higher premium, lower out-of-pocket costs PlatinumCover ~90% Highest premium, lowest out-of-pocket costs Not offered by all insurers www.hhs.gov

16

Hardship Exemptions Homeless Bankruptcy Insurance cancelled and other plans not affordable Ineligible for Medicaid Unable to pay medical expenses for 2y Unexpected expense ↑ for ill / disabled / aging family member Expect to claim child denied Medicaid / CHIP Eligible for plan but not enrolled due to appeals decision Eviction / foreclosure Fire, flood, disaster Utility shut-off Domestic violence Close family death www.hhs.gov

17

Types of Insurance Gallup-Healthways-Well-Being-Index Type of Insurance% Current / former employer43.5 Self / family member20.7 Medicaid8.4 Medicare6.9 Military / veteran4.7 Union2.5 Other3.8 None16.2 2014 Q2

18

Medicare vs. Medicaid www.Medicare.gov www.medicaid.gov MedicareMedicaid Gov’tFederalFederal-state run by state Eligibility> 65 Disability ALS: immediate ESRD: 3mo post HD/CRT Other chronic diseases (if getting Social Security Disability benefits for 2y) Income Categorical: peds, pregnant, adult in family with dep peds, disability, blind, older Mandate: v low income, peds / pregnant low income, most disabled / older SSI cash assist Homeless: 3 rd party assistance CoverageInpatient / outpatient care Prescription drugs Inpatient / outpatient care Drug coverage optional but provided by all states to most CostDepends on coverageDepends on income and rules of state Can have both (dual eligible)

Income Categorical: peds, pregnant, adult in family with dep peds, disability, blind, older Mandate: v low income, peds / pregnant low income, most disabled / older SSI cash assist Homeless: 3 rd party assistance CoverageInpatient / outpatient care Prescription drugs Inpatient / outpatient care Drug coverage optional but provided by all states to most CostDepends on coverageDepends on income and rules of state Can have both (dual eligible).")

19

Medicare Coverage Federal and state laws National coverage decisions made by Medicare about what should be covered Local coverage decisions made by companies in each state that process claims for Medicare and decide what is medically necessary and therefore should be covered in that area www.Medicare.gov

20

Medicare Parts www.Medicare.gov PartWhat’s Covered A (Inpatient) Hospital, skilled nursing, nursing home, hospice, home health care (including visits / tests / procedures) B (Outpatient) Services: clinical research studies, ambulance, mental health, 2 nd opinion before surg, certain drugs (infused / injected by MD, EN / TPN, oral chemo / anti-emetics) Supplies: EN / TPN, ostomy, neb, wheelchair / walker Preventative: certain vaccines (flu, Pneumovax, HBV) C (Advantage) Run by private insurance company (HMO / PPO) Often lower deductibles / copays Includes all Part A / B coverage, often prescription drug May not cover non-medically necessary services D (Prescription) Each Part D plan has its own list of covered drugs, premiums, deductibles, copays, coinsurance Drugs not covered by Part B (self-injectable, Zostavax) Pay extra $145-832 / year if income > $85,000 Max deductible $320 in 2015

Hospital, skilled nursing, nursing home, hospice, home health care (including visits / tests / procedures) B (Outpatient) Services: clinical research studies, ambulance, mental health, 2 nd opinion before surg, certain drugs (infused / injected by MD, EN / TPN, oral chemo / anti-emetics) Supplies: EN / TPN, ostomy, neb, wheelchair / walker Preventative: certain vaccines (flu, Pneumovax, HBV) C (Advantage) Run by private insurance company (HMO / PPO) Often lower deductibles / copays Includes all Part A / B coverage, often prescription drug May not cover non-medically necessary services D (Prescription) Each Part D plan has its own list of covered drugs, premiums, deductibles, copays, coinsurance Drugs not covered by Part B (self-injectable, Zostavax) Pay extra $ / year if income > $85,000 Max deductible $320 in 2015")

21

The Dreaded Donut Hole Most Medicare prescription drug programs have coverage gap: temporary limit on drug coverage Begins when spend $2,850 out-of-pocket Ends 1/1 of next year or $4,550 out-of-pocket –“Catastrophic coverage” for rest of year: small copay or coinsurance Includes deductible, copay, coinsurance, and 50% manufacturer discount payment on brand- name drugs Excludes premium, pharmacy dispensing fee Once in donut hole, you pay 47.5% for brand- name, 72% for generic drugs www.Medicare.gov

22

Medicare with Other Insurance Coordination of benefits rules: >1 payer –1º payer pays up to limit of its coverage –2º payer pays only if there are uncovered costs, but may not pay all of these Conditional payment –Payment Medicare makes for services other payer is responsible for –Medicare makes payment so you are not stuck with bill –Your responsibility to make sure Medicare gets repaid (call Benefits Coordination and Recovery Center) www.Medicare.gov

")

23

Medigap Medicare supplement insurance Sold by private company: pay premium Covers costs not covered by Medicare: copay, coinsurance, deductible Must have Part A / B Cannot have Part D and Medigap for drugs –Most Medigap drug coverage not creditable (do not pay as much as standard Part D) –May pay more if join Part D later No long-term care, vision / hearing / dental www.Medicare.gov

–May pay more if join Part D later No long-term care, vision / hearing / dental")

24

Age 26 Before ACA, insurance companies could remove children at age 19 With ACA, most must cover up to age 26 –Married, living / financially independent of parents, school, eligible for employer’s plan Qualify for special enrollment period Get patients thinking about age 26 early –Avoid missing doses / tests / office visits Other options if < 26 –Student, private, Medicaid, catastrophic www.hhs.gov

25

Other Special Considerations End of year: plan renewal / change –Starts October –Patients who consumed much of your time with authorization / denial issues need to consider better plan (costs more) Loss of insurance / job –Patients often know this is coming –Advanced planning to get assistance –Avoid missing meds and flaring

Loss of insurance / job –Patients often know this is coming –Advanced planning to get assistance –Avoid missing meds and flaring")

26

CCFA ccfa.org/science-and-professionals/programs- materials/appeal-letters Bathroom accommodations (school / dorm, job) Social Security disability Patient financial assistance programs –Meds –Out-of-pocket expenses –Ostomy supplies: Ostomy Group, Friends of Ostomates Worldwide, United Ostomy Assoc of America, Convatec, Hollister

Social Security disability Patient financial assistance programs –Meds –Out-of-pocket expenses –Ostomy supplies: Ostomy Group, Friends of Ostomates Worldwide, United Ostomy Assoc of America, Convatec, Hollister")

27

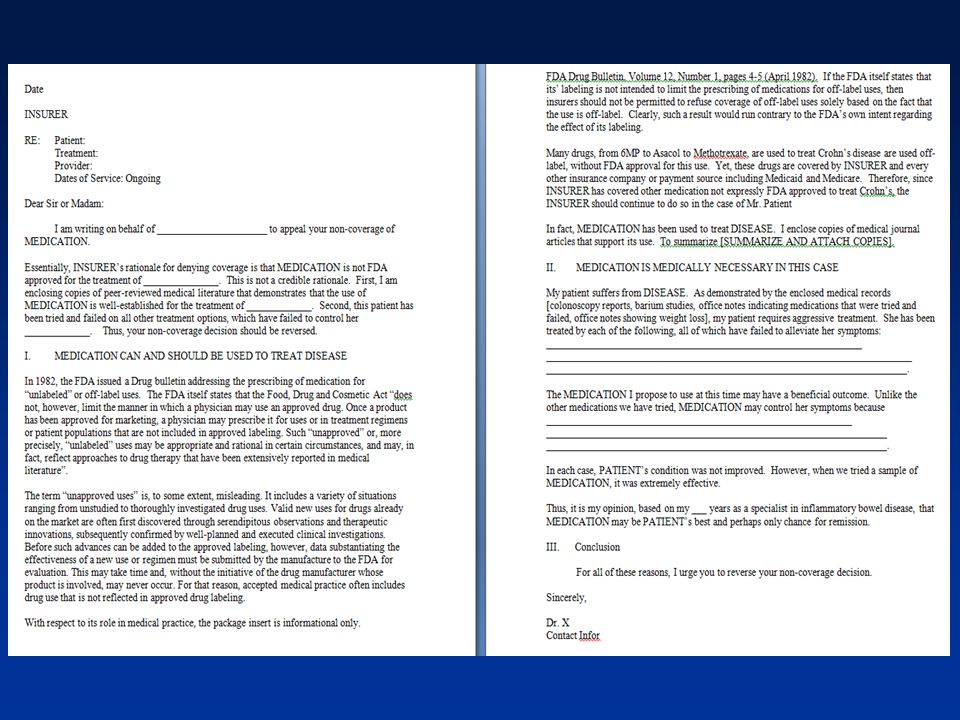

CCFA ccfa.org/science-and-professionals/programs- materials/appeal-letters Meds –Dose escalation of anti-TNF –Off label use Tests –Fecal calprotectin –TPMT, thiopurine metabolites –IFX / HACA –Capsule endoscopy

30

CCFA ccfa.org/living-with-crohns-colitis/talk-to-a-specialist –Help center staff expert at answering questions and finding resources ccfa.org/science-and-professionals/programs- materials/patient-brochures –Healthcare reform: fact sheet / update –IBD insurance checklist: MDs, tests, meds, supplies, services, expense sheet –Employment and IBD: laws, accommodations, FMLA, employment resources ccfa.org/assets/pdfs/resources –Webinar (CCFA / CMS) on insurance marketplace –Webinar on managing costs of IBD

on insurance marketplace –Webinar on managing costs of IBD")

31

Defeat Them With Data Anti-TNF dose escalation –IFX: ACCENT I, IHIS, UPMC / Leuven, St. Clair –ADA: CHARM, Billioud meta-analysis, BIRD –CZP: PRECiSE 4 Off-label use / dosing –UST: CERTIFI, demand CD dosing, dose escalation (cite anti-TNF data) –GOL for CD: demonstrate prior response and then LOR to all other anti-TNFs –Tofacitinib: Sandborn

–GOL for CD: demonstrate prior response and then LOR to all other anti-TNFs –Tofacitinib: Sandborn.")

32

Defeat Them With Data Fecal calprotectin: Mao meta-analysis Thiopurines –TPMT: Weinshilboum, Black –Metabolites: Osterman, Dubinsky x2 IFX / HACA –Proactive (Cheifetz), reactive (Afif) –Other: ACCENT I / II, SONIC, Baert, Maser, Van Assche, Bortlik, Imaeda, ACT I / II, Seow ADA / AAA –Karmiris (Leuven), Roblin, ULTRA 2

, reactive (Afif) –Other: ACCENT I / II, SONIC, Baert, Maser, Van Assche, Bortlik, Imaeda, ACT I / II, Seow ADA / AAA –Karmiris (Leuven), Roblin, ULTRA 2")

33

Hospital Assistance Social worker / financial counselor –Help with access to insurance / medications Business administrator / pharmacy head –Payment plans –Copay assistance / coverage –Can lower price of office visit to Medicare rate –Bridge funding until have insurance –Cost forgiveness for inpatient services

34

Pharma Most have patient assistance for underinsured Most have ties to charitable organizations for uninsured (contribute money each year) IFX –AccessOne: verification of benefits –Remistart Only commercial insurance covering IFX Patient pays $50 per infusion Max $8-10K / year then Remistart Extended –Medicare: Medigap, foundation assistance –No insurance: J&J Patient Assistance Foundation (income < 47K), other foundations

IFX –AccessOne: verification of benefits –Remistart Only commercial insurance covering IFX Patient pays $50 per infusion Max $8-10K / year then Remistart Extended –Medicare: Medigap, foundation assistance –No insurance: J&J Patient Assistance Foundation (income < 47K), other foundations")

35

Pharma ADA –Commercial insurance covering ADA Get $2,750-6,500 toward deductible After that, copay cards as low as $5 ($700- 800 / mo out-of-pocket expenses covered) Max $9,000 / year then Abbvie Patient Assistance Foundation –Medicare: Medigap, foundation assistance Unless Part D with retiree drug subsidy –No insurance: Abbvie Patient Assistance Foundation (income < 46K), other foundations

Max $9,000 / year then Abbvie Patient Assistance Foundation –Medicare: Medigap, foundation assistance Unless Part D with retiree drug subsidy –No insurance: Abbvie Patient Assistance Foundation (income < 46K), other foundations")

36

Charitable Organizations The early bird gets the worm Needy Meds –Gateway to foundations Patient Advocate Foundation (CD, CRC) –Copay / coinsurance / deductible –Need insurance (commercial, Medicare) –Income < 400% of federal poverty line Chronic Disease Fund (CD, CRC) –Copay, transportation, lodging –Need insurance (commercial, Medicare) –Income requirements vary by state

–Copay / coinsurance / deductible –Need insurance (commercial, Medicare) –Income < 400% of federal poverty line Chronic Disease Fund (CD, CRC) –Copay, transportation, lodging –Need insurance (commercial, Medicare) –Income requirements vary by state")

37

Charitable Organizations Patient Access Network Foundation (IBD) –Copay: max award for IBD $3,800 –Need Medicare –Income < 400% of federal poverty line HealthWell Foundation (IBD) –Copay / coinsurance / deductible / premium –Need insurance (commercial, Medicare) –Income < 400-500% of federal poverty line Nat’l Org for Rare Disorders (NORD) (IBD) –Uninsured or underinsured –Copay / coinsurance / deductible / premium, travel, testing, consultation

–Copay: max award for IBD $3,800 –Need Medicare –Income < 400% of federal poverty line HealthWell Foundation (IBD) –Copay / coinsurance / deductible / premium –Need insurance (commercial, Medicare) –Income < % of federal poverty line Nat’l Org for Rare Disorders (NORD) (IBD) –Uninsured or underinsured –Copay / coinsurance / deductible / premium, travel, testing, consultation")

38

Clinical Trials www.clinicaltrials.gov Trials with various therapies –Old drugs –Novel drugs –Nutritional –FMT –Stem cell transplant –Other (hyperbaric O2, yoga) Methotrexate for UC (MERIT-UC)

Methotrexate for UC (MERIT-UC)")

39

Persistence Persistence beats resistance Payers often obstructive and time drain –RNs / MAs ready to provide documentation –MD’s time is often weakest link Don’t give up: you can beat them Peer-to-peer review: call medical director –Defeat them with data / expertise –Consequences: hospitalization, surgery –Make them squirm: put them in your place (if patient were their child / parent / themselves)

")

Similar presentations

2012 Medicare 101.>")

>")

Plans Eligibility and Enrollment periods 2.>")

>")

and limitations Medicare.>")