Download presentation

Presentation is loading. Please wait.

1

Binary options Giampaolo Gabbi

2

Definition In finance, a binary option is a type of option where the payoff is either some fixed amount of some asset or nothing at all. The two main types of binary options are the cash-or-nothing binary option and the asset-or-nothing binary option. The cash-or-nothing binary option pays some fixed amount of cash if the option expires in-the- money while the asset-or-nothing pays the value of the underlying security. Thus, the options are binary in nature because there are only two possible outcomes. They are also called all-or-nothing options, digital options (more common in forex/interest rate markets), and Fixed Return Options (FROs) (on the American Stock Exchange). Binary options are usually European-style options. For example, a purchase is made of a binary cash-or-nothing call option on XYZ Corp's stock struck at $100 with a binary payoff of $1000. Then, if at the future maturity date, the stock is trading at or above $100, $1000 is received. If its stock is trading below $100, nothing is received.

, and Fixed Return Options (FROs) (on the American Stock Exchange). Binary options are usually European-style options. For example, a purchase is made of a binary cash-or-nothing call option on XYZ Corp s stock struck at $100 with a binary payoff of $1000. Then, if at the future maturity date, the stock is trading at or above $100, $1000 is received. If its stock is trading below $100, nothing is received..")

3

Definition Cash-or-nothing call This pays out one unit of cash if the spot is above the strike at maturity Cash-or-nothing put This pays out one unit of cash if the spot is below the strike at maturity Asset-or-nothing call This pays out one unit of asset if the spot is above the strike at maturity Asset-or-nothing put This pays out one unit of asset if the spot is below the strike at maturity

4

Definition A key difference compared to vanilla options for the option writer is that the maximum possible downside is known in advance. This makes selling binary options a much more risk controlled and less negatively skewed strategy than the typical short volatility position.

5

Definition

6

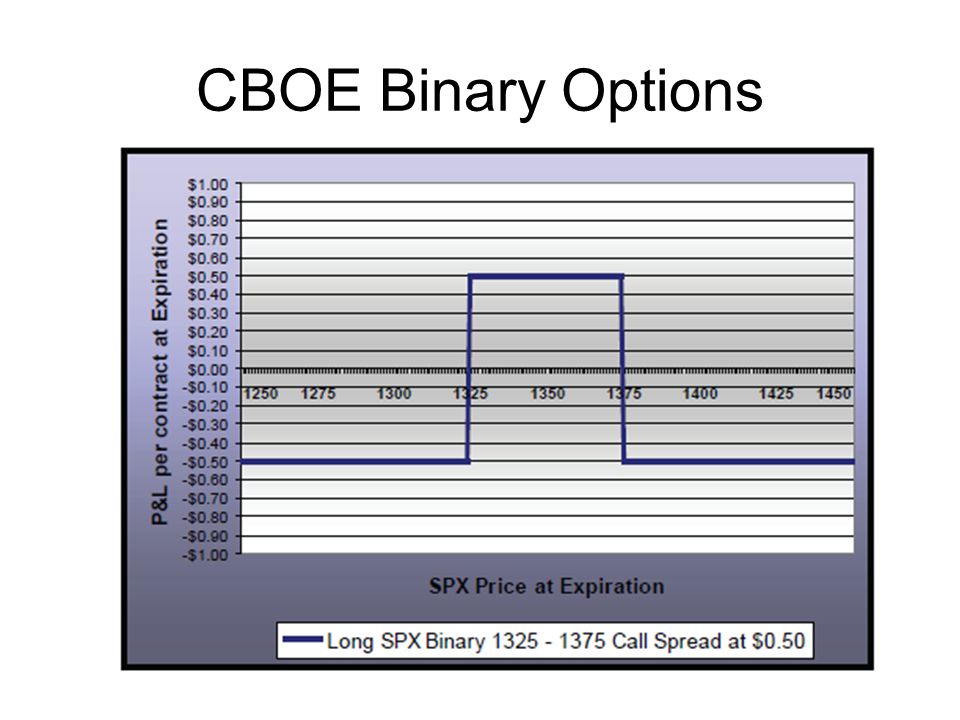

Expressing a Range Trading View A binary option spread, such as one set up by purchasing a binary call at a given strike versus selling a binary call at a higher strike, is the cleanest way of implementing the view that the underlying remains with a defined range. Since a binary option is similar to a call spread, a binary call spread offers a risk reward similar to a condor.

7

Expressing a Range Trading View For instance, with the SPX Aug12 1250 binary trading at 0.5 and the Aug12 1300 binary at 0.3, the 1250-1300 binary call spread costs €0.2 and pays out €1 if the index ends between 1250 and 1300 as of the August expiration. In comparison, the condor wins in a similar range but the boundaries are not as clearly defined

8

Definition

9

Market Options are generally traded either OTC or on a national securities exchange registered with the Securities and Exchange Commission ("SEC") or on a contract market designated by the Commodity Futures Trading Commission ("CFTC"). A registered national securities exchange or designated contract market are hereinafter referred to collectively as "organized exchange“. An instrument is described as trading OTC if it trades in some context other than on or through an organized exchange. OTC derivatives are understood to be specifically tailored to the needs and requirements of the end- user, and therefore, lack the standardization and transparency found on organized exchanges. The majority of derivative products are traded OTC. In such a market, large financial institutions serve as derivatives dealers, customizing products for the needs of particular clients. Contract terms are negotiated between the parties, and typically each party has only their contra-party to look to for performance of the contract.

10

Market Binary options have been traded for some time in an OTC environment between institutional traders but not on a national securities exchange. Contract markets have offered "binary options“ based on catastrophic events as well as on certain economic indexes such as the Consumer Price Index (CPI). In France, Germany and Austria, binary options have been traded OTC in a one-sided market between investors and an institution. The institution in these cases is the issuer of the contract and establishes, if applicable, the market for the binary option. OTC binary options have several drawbacks and disadvantages. One disadvantage is that OTC binary options are typically offered by an institution on a non-fungible basis so that a customer can purchase the option only from the institution, and cannot easily resell to a third party because they are not standardized or traded on an exchange. As a result, OTC binary options, as compared to standardized exchange- traded options, lack important attributes of a trading market such as transparency and liquidity.

. In France, Germany and Austria, binary options have been traded OTC in a one-sided market between investors and an institution. The institution in these cases is the issuer of the contract and establishes, if applicable, the market for the binary option. OTC binary options have several drawbacks and disadvantages. One disadvantage is that OTC binary options are typically offered by an institution on a non-fungible basis so that a customer can purchase the option only from the institution, and cannot easily resell to a third party because they are not standardized or traded on an exchange. As a result, OTC binary options, as compared to standardized exchange- traded options, lack important attributes of a trading market such as transparency and liquidity..")

11

Non exchange-traded binary options Binary option contracts have long been available Over- the-counter (OTC), i.e. sold directly by the issuer to the buyer. They were generally considered "exotic" instruments and there was no liquid market for trading these instruments between their issuance and expiration. They were often seen embedded in more complex option contracts. Since mid-2008 binary options web-sites called binary option trading platforms have been offering a simplified version of exchange-traded binary options. It is estimated that around 30 such platforms (including white label products) have been in operation as of January 2011

have been in operation as of January")

12

Exchange-traded binary options In 2007, the Options Clearing Corporation proposed a rule change to allow binary options, and the Securities and Exchange Commission approved listing cash-or- nothing binary options in 2008. In May 2008, the American Stock Exchange (Amex) launched exchange-traded European cash-or-nothing binary options, and the Chicago Board Options Exchange (CBOE) followed in June 2008. The standardization of binary options allows them to be exchange-traded with continuous quotations. Amex offers binary options on some ETFs and a few highly liquid equities such as Citigroup and Google. Amex calls binary options "Fixed Return Options"; calls are named "Finish High" and puts are named "Finish Low". To reduce the threat of market manipulation of single stocks, Amex FROs use a "settlement index" defined as a volume-weighted average of trades on the expiration day. CBOE offers binary options on the S&P 500 (SPX) and the CBOE Volatility Index (VIX). The tickers for these are BSZ and BVZ, respectively. CBOE only offers calls, as binary put options are trivial to create synthetically from binary call options. BSZ strikes are at 5-point intervals and BVZ strikes are at 1-point intervals. The actual underlying to BSZ and BVZ are based on the opening prices of index basket members. Both Amex and CBOE listed options have values between $0 and $1, with a multiplier of 100, and tick size of $0.01, and are cash settled

launched exchange-traded European cash-or-nothing binary options, and the Chicago Board Options Exchange (CBOE) followed in June The standardization of binary options allows them to be exchange-traded with continuous quotations. Amex offers binary options on some ETFs and a few highly liquid equities such as Citigroup and Google. Amex calls binary options Fixed Return Options ; calls are named Finish High and puts are named Finish Low . To reduce the threat of market manipulation of single stocks, Amex FROs use a settlement index defined as a volume-weighted average of trades on the expiration day. CBOE offers binary options on the S&P 500 (SPX) and the CBOE Volatility Index (VIX). The tickers for these are BSZ and BVZ, respectively. CBOE only offers calls, as binary put options are trivial to create synthetically from binary call options. BSZ strikes are at 5-point intervals and BVZ strikes are at 1-point intervals. The actual underlying to BSZ and BVZ are based on the opening prices of index basket members. Both Amex and CBOE listed options have values between $0 and $1, with a multiplier of 100, and tick size of $0.01, and are cash settled.")

13

Example of a Binary Options Trade A trader who thinks that the EUR/USD strike price will close at or above 1.2500 at 3:00 p.m. can buy a call option on that outcome. A trader who thinks that the EUR/USD strike price will close at or below 1.2500 at 3:00 p.m. can buy a put option or sell the contract. At 2:00 p.m. the EUR/USD spot price is 1.2490. the trader believes this will increase, so he buys 10 call options for EUR/USD at or above 1.2500 at 3:00 p.m. at a cost of $40 each.

14

Example of a Binary Options Trade The risk involved in this trade is known. The trader’s gross profit/loss follows the ‘all or nothing’ principle. He can lose all the money he invested, which in this case is $40 x 10 = $400, or make a gross profit of $100 x 10 = $1000. If the EUR/USD strike price will close at or above 1.2500 at 3:00 p.m. the trader's net profit will be the payoff at expiry minus the cost of the option: $1000 - $400 = $600. The trader can also choose to liquidate (buy or sell to close) his position prior to expiration, at which point the option value is not guaranteed to be $100. The larger the gap between the spot price and the strike price, the value of the option decreases, as the option is less likely to expire in the money. In this example, at 3:00 p.m. the spot has risen to 1.2505. The option has expired in the money and the gross payoff is $1000. The trader's net profit is $600

his position prior to expiration, at which point the option value is not guaranteed to be $100. The larger the gap between the spot price and the strike price, the value of the option decreases, as the option is less likely to expire in the money. In this example, at 3:00 p.m. the spot has risen to The option has expired in the money and the gross payoff is $1000. The trader s net profit is $600.")

15

CBOE to list binary options on S&P 500, VIX

16

CBOE Binary Options CBOE Binary Options are contracts that have an "all-or- nothing" payout depending on the settlement price of the underlying broad-based index relative to the strike price of the binary option. Binary Call Options pay either 1) a fixed cash settlement amount, if the underlying index settles at or above the strike price at expiration; or 2) nothing at all, if the underlying index settles below the strike price at expiration. Binary Put Options pay either 1) a fixed cash settlement amount, if the underlying index settles below the strike price at expiration; or 2) nothing at all, if the underlying index settles at or above the strike price at expiration.

a fixed cash settlement amount, if the underlying index settles at or above the strike price at expiration; or 2) nothing at all, if the underlying index settles below the strike price at expiration. Binary Put Options pay either 1) a fixed cash settlement amount, if the underlying index settles below the strike price at expiration; or 2) nothing at all, if the underlying index settles at or above the strike price at expiration..")

17

CBOE Binary Options

21

Creating Contingent Premium Options Contingent premium options are those in which the buyer pays a premium only if the option finishes in the money, and are commonly used as a cheapening mechanism. A plain vanilla option in combination with a binary option whose payoff at expiration would equal the premium of the vanilla creates a structure similar to a contingent premium option. Such a structure loses close to the strike in compensation for the lower premium but does not involve a premium payment if one’s directional view happens to be incorrect.

22

Creating Contingent Premium Options

23

Binary Option value For binary options with European exercise, pricing is relatively straightforward as an analytical expression is available in the Black Scholes world. For the European binary call that pays off 1 at expiration T if the underlying S is over the strike K, the expiration payoff can be summarized as

24

Relationship to vanilla options' Greeks Since a binary call is a mathematical derivative of a vanilla call with respect to strike, the price of a binary call has the same shape as the delta of a vanilla call, The delta of a binary call has the same shape as the gamma of a vanilla call.

25

Interpretation of prices In a prediction market, binary options are used to find out a population's best estimate of an event occurring - for example, a price of 0.65 on a binary option triggered by the Democratic candidate winning the next US Presidential election can be interpreted as an estimate of 65% likelihood of him winning. In financial markets, expected returns on a stock or other instrument are already priced into the stock. However, a binary options market provides other information. Just as the regular options market reveals the market's estimate of variance (volatility), i.e. the second moment, a binary options market reveals the market's estimate of skew, i.e. the third moment. A portfolio of binary options can also be used to synthetically recreate (or valuate) any other option (analogous to integration).

, i.e. the second moment, a binary options market reveals the market s estimate of skew, i.e. the third moment. A portfolio of binary options can also be used to synthetically recreate (or valuate) any other option (analogous to integration)..")

26

Interpretation of prices (Intrade)

")

27

Interpretation of prices

28

Replication with Option Spreads The simplest listed instrument available that reasonably mimics the payoff of a binary call option is a call spread. The ideal hedge would be a spread of infinitesimal width, but even with the strike intervals available in listed options, replication of a binary is reasonably accurate except very close to expiration. The imperfectness of such a hedge is a consequence of the non-zero probability of the underlying finishing between the two strikes. Since the 5-point interval between strikes for near term SPX options is much tighter than the 1-point interval between VIX option strikes, this theoretical hedge implies a narrower range for the bid-offer spread on SPX binaries.

29

Replication with Option Spreads To illustrate the construction of a replicating call spread, we consider the 1300 strike binary call option on the SPX expiring in Aug11. A potential hedge for this is the 1295-1300 call spread on SPX with the same expiration. Since the binary pays off $1 (corresponding to a payoff of $100 per contract) if SPX closes at or above 1300 at expiration, compared to a $5 payoff for the spread, we need 0.2 units of the call spread for each binary option.

if SPX closes at or above 1300 at expiration, compared to a $5 payoff for the spread, we need 0.2 units of the call spread for each binary option..")

30

Replication with Option Spreads Next figure illustrates how the price of a binary option varies as a function of the underlying as expiration approaches. With several months to go in the life of the option, the mark to market of the option is not unlike that of the underlying itself. With about a week to expiration, it resembles a call spread with a similar time to expiration. However, very close to expiration, the binary becomes very convex just below the strike and is highly negatively convex at levels slightly above the strike.

31

Replication with Option Spreads

Similar presentations

>")

Course : Security Analysis and Portfolio Management Unit III: Financial Derivatives.>")

to purchase or sell an asset at a fixed price as some future date.>")

>")