Download presentation

Presentation is loading. Please wait.

2

preparing foraudits

3

PhonesLunch Workbook Restrooms

4

agenda Audit Preparation ■Types of Audits ■Institutional Responsibility Top 10 Audit Findings ■Examples ■Resolutions Program Reviews ■ Program review findings Workbook page 2

6

Preparing for an Audit

7

■Types of Audits ♦Compliance audit ♦Financial statement audit ■Schools ♦For-profit schools (and servicers) Compliance audit conducted under ED’s FSA Audit Guide ♦Public & nonprofit Audit conducted in accordance with Office Management and Budgets A-133 audits 2009-2010 FSA Handbook, Vol 2, Chapter 11 and Chapter 12 34 CFR 668.23(a)(1), 34 CFR 668.23(a)(5) Workbook page 3

Compliance audit conducted under ED’s FSA Audit Guide ♦Public & nonprofit Audit conducted in accordance with Office Management and Budgets A-133 audits FSA Handbook, Vol 2, Chapter 11 and Chapter CFR (a)(1), 34 CFR (a)(5) Workbook page 3")

8

■Think like an auditor ♦Audit date ♦Auditors are looking at samples to extrapolate into trends Focus on your basic processes before the audit Policy and Procedures Manual –Up-to-date audit preparation Workbook page 4

9

■Who ♦Schools must hire a qualified independent auditor ♦State schools may use state auditors ■When ♦Compliance and financial audits must be conducted annually on the basis of the school's fiscal year audit preparation Workbook page 4

10

■Policy and procedures manual ♦Focus on functionality, not appearance ■Emphasis on content ■Policy and procedures manual should be the “road map” for all of your internal processing audit preparation Workbook page 4

11

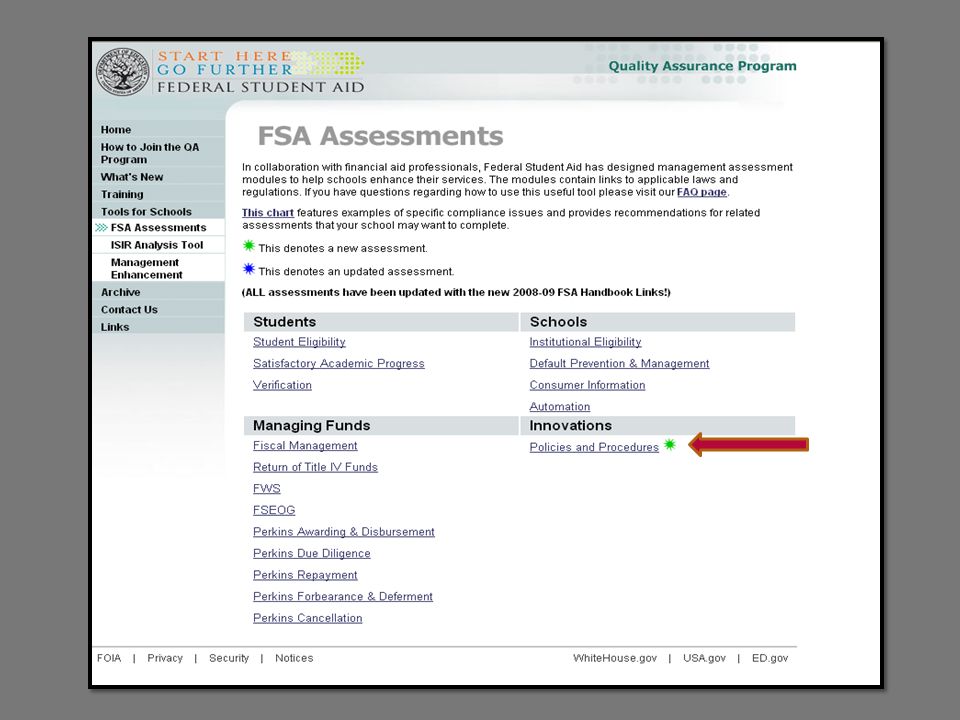

■FSA assessments tool http://ifap.ed.gov/IFAPWebApp/qualitya ssurance/SFAAssessment.jspFF http://ifap.ed.gov/IFAPWebApp/qualitya ssurance/SFAAssessment.jspFF ■The assessments assist ♦evaluating processes ♦providing citations ♦self-test activities and summaries to ensure completeness auditing tools Workbook page 5

15

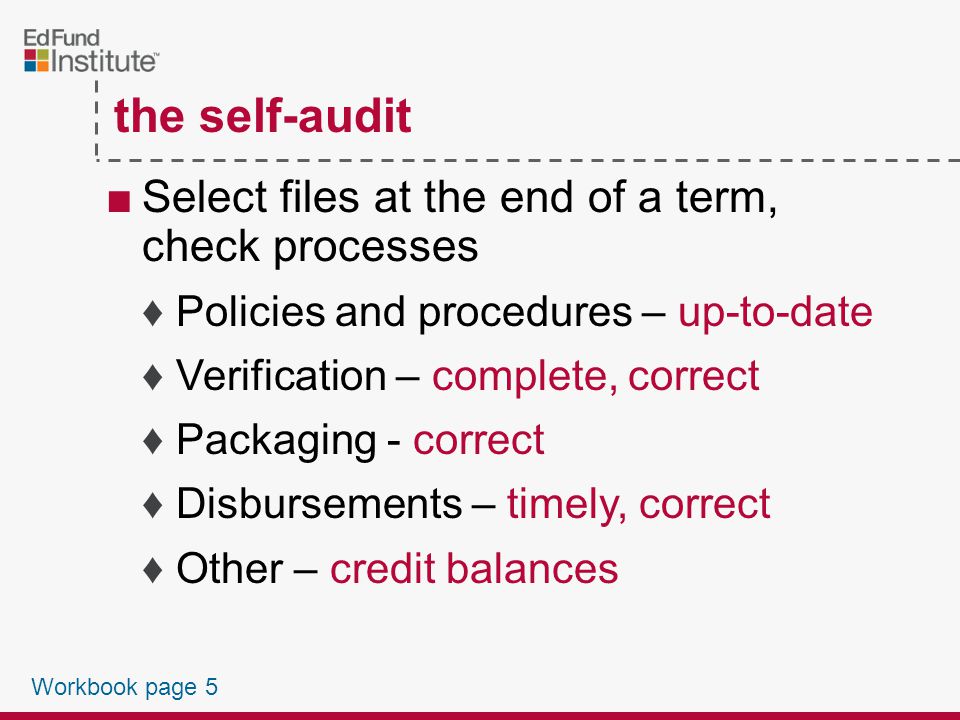

■Select files at the end of a term, check processes ♦Policies and procedures – up-to-date ♦Verification – complete, correct ♦Packaging - correct ♦Disbursements – timely, correct ♦Other – credit balances the self-audit Workbook page 5

16

■Organize documents within files before the audit ■Documents need to be in a consistent order ■Auditors searching files for documents may encourage a more methodical review the audit

17

■Be prepared to respond to findings ■Auditors are not always correct — findings can be an area for discussion ■It is possible to discuss a potential finding before it is included in a report the audit

18

■Documents examined ♦School catalog ♦Accreditation letter ♦Licenses, if applicable ♦Program Participation Agreement ♦Enrollment records the audit - documents Workbook page 5

19

■Loan applications and counseling documents ■Award calculations ■Title IV funds received and disbursed ■R2T4 calculations ■NSLDS reports ■G5 records the audit - documents Workbook page 5

20

■How ♦Schools must now use ED's eZ-Audit Web site to submit their financial statements and compliance auditseZ-Audit Web site ♦Effective June 16, 2003 FSA AUDIT GUIDE http://www.ed.gov/about/offices/list/oig/nonfed/sfa.html the audit Workbook page 6

21

20 ■Provides Instant Audit Info ■Identifies Overdue Audits ■Streamlined FSA Review Process ■Non-editable PDF file (official record) Retained & Used to Validate Data ■Add’l Changes to Reduce Reporting Burden Ez-Audit System https://ezaudit.ed.gov/EZWebApp/common /login.jsp Workbook page 6

Retained & Used to Validate Data ■Add’l Changes to Reduce Reporting Burden Ez-Audit System /login.jsp Workbook page 6")

22

up next: review of top 10 audit findings BREAK TIME

23

Top 10 Audit Findings Workbook page 7

24

#10 Credit Balance Deficiencies Workbook page 8

25

#10 credit balance deficiencies ■Must pay A.Date balance, if balance occurred after first day of class of a B.First day of classes of payment period if occurred on or before first day of class occurred payment period credit balance Workbook page 8

26

■Authorizations ♦Disburse FSA funds ♦Pay allowable charges ♦Hold an FSA credit balance ♦Apply FSA funds to minor prior-year charges #10 credit balance deficiencies 2008-09 FSA Handbook Vol. 4, Chapter 2, Page 25 - 26 Workbook page 9

27

■Authorizations ♦Must clearly explain How to cancel or modify –must pay credit balance within 14 days Not retroactive How school will issue credit balances 2008-09 FSA Handbook Volume 4, Chapter 2 #10 credit balance deficiencies Workbook page 9

28

■Authorizations ♦Schools cannot Require or coerce Fail to explain how to cancel or modify Fail to explain changes are not retroactive Fail to detail funds the authorization covers #10 credit balance deficiencies 2008-09 FSA Handbook Volume 4, Chapter 2 Workbook page 9

29

■Examples ♦Unable to determine when a credit balance occurred ♦Credit balances not released within 14 days ♦Credit balances held without student authorization #10 credit balance deficiencies Workbook page 10

30

#9 Student Status Confirmation Reporting (SSCR) Errors Workbook page 10

Errors Workbook page 10")

31

#9 SSCR reporting errors ■Report filed late ♦After 30 days of receipt of roster ■Report not filed ♦Not less than twice a year ■Report not retained for 3 years Workbook page 10

32

SSCR reporting errors ■Examples ♦File not submitted within 30 days ♦Using incorrect enrollment status code ♦Incorrect graduation effective date ♦Student(s) reported withdrawn incorrectly Workbook page 10

reported withdrawn incorrectly Workbook page 10")

33

#8 Incorrect Pell Payments Workbook page 11

34

■Overpayment or underpayment ♦Always use Pell Grant payment schedule ♦Ensure correct student status: full- time, three-quarter time, half-time ♦Monitor total award - cannot exceed maximum allowable #8 incorrect Pell payments Workbook page 11

35

■Recalculation not performed ♦Changes in EFC due to Corrections Updating Adjustments ♦Overpayments can be repaid by Adjusting future disbursements Repayment #8 incorrect Pell payments Workbook page 11

36

■Change in enrollment status between terms ♦Term-based, credit-hour programs must calculate a student’s payment for each term ♦Enrollment status may be different in each term ♦Must recalculate if different #8 incorrect Pell payments Workbook page 12

37

TRUE or FALSE A student is considered to have begun attendance in all classes if student attends at least one day of class for each course? #8 incorrect Pell payments T

38

TRUE or FALSE A school must have a procedure in place to know whether a student has begun attendance in all classes? #8 incorrect Pell payments T

39

■Annual award calculated incorrectly ♦Examples Incorrect EFC used Incorrect Pell formula Inaccurate proration calculation Adjustments not made when enrollment status changed/courses not counted in enrollment status Workbook page12

40

■Interim disbursement not recovered ♦An interim disbursement allowed before verification is complete First payment period ♦School is liable for interim disbursement if student Received an overpayment Fails to complete verification #8 incorrect Pell payments Workbook page 12

41

#7 Verification Violations Workbook page 13

42

■Required policies ♦School must Deadlines and consequences Method of notifying of students Correction procedures Procedures for overpayment cases #7 verification violations Workbook page 13

43

■A school must provide ♦Documents required for verification ♦Student’s responsibility throughout the process ♦Student notification of award changes #7 verification violations Workbook page 13

44

■Selected after disbursement ♦Verify application ♦Must repay all aid Except Stafford loan funds and FWS wages earned Cancel any further disbursements #7 verification violations Workbook page 13

45

■Examples ♦Verification worksheet ♦Untaxed income ♦Conflicting information ♦Required corrections ♦Verification ♦Dependency overrides *finding on both audits & program reviews #7 verification violations not signed not verified not resolved not processed incomplete improperly/undocumented* Workbook page 14

46

#6 Auditor’s Opinion Cited in Audit Workbook page 14

47

#6 auditor’s opinion cited in audit ■Independent auditor’s opinion cited ♦Refers to anything other than an unqualified opinion ♦Indicates serious deficiencies/areas of concern in the audit Workbook page 14

48

Examples ■Failure to reconcile program accounts ■High Perkins default rates ■Continuing problems with R2T4 ■Inadequate accounting systems and/or procedures ■Lack of internal controls #6 auditor’s opinion cited in audit Workbook page 14

49

■Lack of Administrative Capability ■Incorrect R2T4 calculations ■Improper academic progress standards ■Inadequate accounting system #6 auditor’s opinion cited in audit Workbook page 14

50

#5 Student Status vs. Common Mistakes Workbook page 15

51

Examples ■“W” for graduated students ■ Incorrect graduation date ■ Students reported as withdrawn for summer break #5 student status vs. common mistakes Workbook page 15

52

#4 Entrance and Exit Counseling Deficiencies

53

■Must include ♦Use of MPN ♦Importance of repayment ♦Consequences of default ♦Repayment schedules ♦Borrowers rights and responsibilities ♦Loan terms and conditions #4 entrance counseling Workbook page 15

54

must complete loan counseling before first disbursement is made A. First-time borrowers B. May be conducted #4 entrance counseling ■Entrance counseling individually, in groups or online Workbook page 16 C. Materials not received online must be mailed to borrower

56

#4 exit counseling ■Required for exit counseling ♦Review of entrance counseling ♦Consequences of default Adverse credit Collection and litigation ♦Repayment required ♦Average monthly repayment schedules ♦Repayment options Workbook page 17

57

#4 exit counseling ■Required for exit counseling ♦Debt management strategies ♦Forbearance, deferment and cancellation options ♦NSLDS and FSA Ombudsman ♦Rights and Responsibilities ♦Personal contact information Workbook page 17

59

#4 exit counseling ■You must ensure students ■May be conducted ■Must document graduating or withdrawing receive loan counseling individually, in groups or online that student participated in and completed counseling Workbook page 18

60

#4 entrance & exit deficiencies ■What can you do ♦Without notification Online Mail sent to last known address ♦Materials must be mailed Within 30 days ♦Not required to use certified mail with a return receipt requested ♦Must document student’s file 2009-10 FSA Handbook Volume 2, Chapter 6, Pages 78-84

61

#3 R2T4 Calculation Errors Workbook page 19

62

■When to calculate R2T4 ♦Title IV recipient ♦Did not return from LOA ♦Withdraws from program #3 R2T4 – calculation errors Workbook page 19

63

■What and how much to consider ♦Pell Grant ♦Campus-based aid (except FWS) ♦FFEL or DL ♦ACG/SMART ♦TEACH Grant #3 R2T4 – calculation errors Workbook page 19

♦FFEL or DL ♦ACG/SMART ♦TEACH Grant #3 R2T4 – calculation errors Workbook page 19")

64

■Up through the 60% point ♦Pro rata schedule is used ■After the 60% point ♦Student has earned 100% ♦School must still complete a return calculation to determine eligibility for post-withdrawal disbursement #3 R2T4 – calculation errors Workbook page 19

65

■Examples ♦Institutional charges incorrect ♦Scheduled breaks not included ♦Incorrect withdrawal dates ♦Use of out-of-date R2T4 forms ♦Mathematical errors #3 R2T4 – calculation errors Workbook page 19

66

■Tools to assist in R2T4 ♦Worksheets can be found at http://www.ifap.ed.gov/ifap/titleiv.jsp ♦Software can be accessed at http://www/fafsa.ed.gov/FOTWWebApp/fa a/faa.jsp ♦Worksheets and software is optional #3 R2T4 – calculation errors 2008-09 FSA Handbook Volume 5, Chapter 2, Page 119-125

67

#2 R2T4 Returns Made Late Workbook page 20

68

■An institution does not satisfy the requirements if ♦Institution’s records show check was issued more than 45 days ♦Date on cancelled check shows bank endorsed check more than 60 days or later #2 R2T4 returns made late Interim Final Regulations Federal Register, Vol 71, No 152, Page 45672 Workbook page 20

69

■Examples ♦Returns not made within 45 days ♦Inadequate system in place to identify/track withdrawals ♦No process in place to track number of days remaining to return funds ♦Lack of coordination between offices #2 R2T4 returns made late Workbook page 20

70

#1 Repeat Findings Failure to Take Corrective Action Workbook page 20

71

■School failed to adequately develop, implement and/or monitor procedures to ensure corrective action plan was followed ■Same finding(s) indentified in subsequent audit(s) #1 repeat findings Workbook page 20

indentified in subsequent audit(s) #1 repeat findings Workbook page 20")

72

Program Review Findings Workbook page 21

73

audit & program review findings ■R2T4 Calculation errors ■Return of Title IV funds made late ■Pell Overpayment/Underpayment ■Verification Violations ■Entrance/Exit counseling deficiencies ■Credit Balance deficiencies Workbook page 21

74

■Consumer information requirements not met ■Lack of administrative capability ■Policies and procedures not developed ■Crime statistics not reported or reported incorrectly * ■Inadequate SAP policy program review findings Workbook page 21

75

consumer information ■Campus Security ■Crime statistics ■Fire Safety Report for On-campus Housing ■Missing Persons Policies and Procedures ■Drug Violation Notification and Penalties ■Drug and Alcohol Prevention Program Workbook page 22 & 23 DCL 08.12

76

Audit – Finding Incorrect ■Require auditor to provide specific regulation/law violated & discuss a reasonable resolution ■Indicate in CAP reasons why the finding is erroneous ♦Necessary for Audit Resolution Process ♦Provide Details to Support Position & Cite Regulation or Law in Support of Assertion 75

77

76 Program Compliance School Eligibility Victoria Edwards, Chief Compliance Officer– DC (202) 377-4275 Robin Minor, General Manager – Wash DC (202) 377-3173 Call the appropriate School Participation Team for information and guidance on audit resolution, financial analysis, program reviews, school and program eligibility/recertification and school closure information. School Participation Teams – Northeast Geneva Leon, Director – Wash DC (202) 377-3173 geneva.leon@ed.gov New York/Boston (Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, Vermont, New Jersey, New York, Puerto Rico, Virgin Islands) William Swift – New York (646) 428-3750 Rosemary Torpey - Boston (617) 289-0133 Elizabeth Coughlin-New York (646) 428-3737 Patrice Fleming - Wash DC (202) 377-4209 Philadelphia (DC, Delaware, Maryland, Pennsylvania, Virginia, West Virginia) Nancy Gifford - Philadelphia (215) 656-6442 John Loreng – Philadelphia (215) 656-6437 Michael Frola - Wash DC (202) 377-3364 Foreign Schools Barbara Hemelt - Wash DC (202) 377-3168 School Participation Teams-South Central Carolyn White, Director – Wash DC (202) 377-3173 carolyn.white@ed.gov Atlanta (Alabama, Florida, Georgia, Mississippi, North Carolina, South Carolina) Charles Engstrom - Atlanta (404) 562-6315 Christopher Miller – Atlanta (404) 562-6304 Patricia Dickerson-Wash DC (202) 377-4218 Dallas (Arkansas, Louisiana, New Mexico, Oklahoma, Texas) Patrick Kennedy - Dallas (214) 661-9490 Janet Dragoo - Dallas (214) 661-9481 Clifton Knight - Wash DC (202) 377-4244 Kansas City (Iowa, Kansas, Kentucky, Missouri, Nebraska, Tennessee) Ralph LoBosco-Kansas City (816) 268-0410 Dvak Corwin – Kansas City (816) 268-0420 Phillip Brumback-Wash DC (202) 377-3464 School Participation Teams - Northwest Douglas Laine, Director – Wash DC (202) 377-3173 douglas.laine@ed.gov Chicago (Illinois, MN, Ohio, Wisconsin, IN) Douglas Parrott - Chicago (312) 730-1532 David Heath – Chicago (312) 730-1522 Earl Flurkey – Chicago (312) 730-1521 Denver (Colorado, Michigan, Montana, North Dakota, South Dakota, Utah, Wyoming) Harry Shriver - Denver (303) 844-3677 x116 Dan Whiting - Denver (303) 844-3677 x120 San Francisco/Seattle (American Samoa, Arizona, California, Guam, Hawaii, Nevada, Palau, Marshall Islands, N. Marianas State of Micronesia, Alaska, Idaho, Oregon, Wash.) Linda Henderson- San Fran (415)-486-5609 Martina Fernandez-Rosario (415)-486-5605 Dyon Toney - Wash DC (202) 377-3639

New York/Boston (Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, Vermont, New Jersey, New York, Puerto Rico, Virgin Islands) William Swift – New York (646) Rosemary Torpey - Boston (617) Elizabeth Coughlin-New York (646) Patrice Fleming - Wash DC (202) Philadelphia (DC, Delaware, Maryland, Pennsylvania, Virginia, West Virginia) Nancy Gifford - Philadelphia (215) John Loreng – Philadelphia (215) Michael Frola - Wash DC (202) Foreign Schools Barbara Hemelt - Wash DC (202) School Participation Teams-South Central Carolyn White, Director – Wash DC (202) Atlanta (Alabama, Florida, Georgia, Mississippi, North Carolina, South Carolina) Charles Engstrom - Atlanta (404) Christopher Miller – Atlanta (404) Patricia Dickerson-Wash DC (202) Dallas (Arkansas, Louisiana, New Mexico, Oklahoma, Texas) Patrick Kennedy - Dallas (214) Janet Dragoo - Dallas (214) Clifton Knight - Wash DC (202) Kansas City (Iowa, Kansas, Kentucky, Missouri, Nebraska, Tennessee) Ralph LoBosco-Kansas City (816) Dvak Corwin – Kansas City (816) Phillip Brumback-Wash DC (202) School Participation Teams - Northwest Douglas Laine, Director – Wash DC (202) Chicago (Illinois, MN, Ohio, Wisconsin, IN) Douglas Parrott - Chicago (312) David Heath – Chicago (312) Earl Flurkey – Chicago (312) Denver (Colorado, Michigan, Montana, North Dakota, South Dakota, Utah, Wyoming) Harry Shriver - Denver (303) x116 Dan Whiting - Denver (303) x120 San Francisco/Seattle (American Samoa, Arizona, California, Guam, Hawaii, Nevada, Palau, Marshall Islands, N. Marianas State of Micronesia, Alaska, Idaho, Oregon, Wash.) Linda Henderson- San Fran (415) Martina Fernandez-Rosario (415) Dyon Toney - Wash DC (202)")

78

knowledge practice application closing thoughts…

79

Thank you for joining me today!

Similar presentations

Swift Session 7 – San Diego.>")