Download presentation

Presentation is loading. Please wait.

1

Tax Reform in the United States 2009 Art Franczek President of The American Institute of Business and Economics artf@online.ru

2

Introduction, a brief overview of US Taxation on international transactions Obama administration’s proposed Tax Reform: Repeal of Check the Box Repeal of Check the Box Partial repeal of deferral Partial repeal of deferral Repeal of ability of companies Repeal of ability of companies to cross credit Foreign Tax Credits to cross credit Foreign Tax Credits Relevance to International Companies in Russia Observations

3

“The art of Taxation is like plucking feathers from a goose. The idea is to pluck the maximum amount of feathers with the minimum amount of squealing” Bismark

4

The US taxes it’s corporations (incorporated in the US) on worldwide income The US taxes it’s corporations (incorporated in the US) on worldwide income Between 1945 and 1962 income tax on foreign income earned by US companies was deferred until income was distributed to the US. This policy along with the Marshall Plan was designed to rebuild Europe. Between 1945 and 1962 income tax on foreign income earned by US companies was deferred until income was distributed to the US. This policy along with the Marshall Plan was designed to rebuild Europe. In 1962 the Kennedy administration repealed the deferral privilege for certain kinds of passive income like interest, royalties, rents, insurance etc.The Internal Revenue Code section on this repeal was known as Subpart F. Subpart F applied to CFCs( Controlled Foreign Corporations ie those corporations with 50% or more of US ownership) In 1962 the Kennedy administration repealed the deferral privilege for certain kinds of passive income like interest, royalties, rents, insurance etc.The Internal Revenue Code section on this repeal was known as Subpart F. Subpart F applied to CFCs( Controlled Foreign Corporations ie those corporations with 50% or more of US ownership)

In 1962 the Kennedy administration repealed the deferral privilege for certain kinds of passive income like interest, royalties, rents, insurance etc.The Internal Revenue Code section on this repeal was known as Subpart F. Subpart F applied to CFCs( Controlled Foreign Corporations ie those corporations with 50% or more of US ownership).")

5

For the last 47 years the Subpart F anti-deferral provision have remained substantially the same although it has been amended many times For the last 47 years the Subpart F anti-deferral provision have remained substantially the same although it has been amended many times The anti-deferral provisions and the US taxation on Worldwide Income have created an extraordinarily complex system of international system of taxation that includes some of the following issues: The anti-deferral provisions and the US taxation on Worldwide Income have created an extraordinarily complex system of international system of taxation that includes some of the following issues: To compute the Foreign Tax Credit a company must calculate the earnings and profits (ie income in local currency ) applying US tax rules. Allocate such expenses as interest to foreign source income. These rules have resulted in exotic tax planning structures like Tax Inversions and the extensive use of the “check the box rules to avoid Subpart F income inclusion.

6

Some reasons for Tax Reform The US budget deficit for 2010 is projected to be over 2 trillion dollars The US budget deficit for 2010 is projected to be over 2 trillion dollars The Obama administration wants to curb the use of Tax Havens and remove incentives for shifting jobs Overseas The Obama administration wants to curb the use of Tax Havens and remove incentives for shifting jobs Overseas Studies have shown that corporations pay an effective rate of 2.6% on foreign income Studies have shown that corporations pay an effective rate of 2.6% on foreign income

7

Example of Check the Box (allowed since 1996) US CFC’s (in this example the Cayman Islands affiliate) don’t pay tax on income that is not repatriated but passive income( interest, royalties etc. ) from one CFC to another is taxed immediately under Subpart F. In this example the Cayman affiliate lends $10,000,000 to German hybrid ( under check the box German hybrid is considered to be a corporation for German tax purposes and a partnership for US tax purposes). US CFC’s (in this example the Cayman Islands affiliate) don’t pay tax on income that is not repatriated but passive income( interest, royalties etc. ) from one CFC to another is taxed immediately under Subpart F. In this example the Cayman affiliate lends $10,000,000 to German hybrid ( under check the box German hybrid is considered to be a corporation for German tax purposes and a partnership for US tax purposes).

from one CFC to another is taxed immediately under Subpart F. In this example the Cayman affiliate lends $10,000,000 to German hybrid ( under check the box German hybrid is considered to be a corporation for German tax purposes and a partnership for US tax purposes). US CFC’s (in this example the Cayman Islands affiliate) don’t pay tax on income that is not repatriated but passive income( interest, royalties etc. ) from one CFC to another is taxed immediately under Subpart F. In this example the Cayman affiliate lends $10,000,000 to German hybrid ( under check the box German hybrid is considered to be a corporation for German tax purposes and a partnership for US tax purposes)..")

8

If German hybrid pays Cayman islands Affiliate $1,000,000 in interest that amount is deductible in Germany which has a 40% tax rate the tax savings is $400,000 and the US parent would not recognize any income because the income that Cayman earns from German hybrid is considered to be partnership income therefore is not taxable in the US until Cayman pays the US parent a dividend. If German hybrid pays Cayman islands Affiliate $1,000,000 in interest that amount is deductible in Germany which has a 40% tax rate the tax savings is $400,000 and the US parent would not recognize any income because the income that Cayman earns from German hybrid is considered to be partnership income therefore is not taxable in the US until Cayman pays the US parent a dividend. The Obama tax proposals would repeal the Check the box option so in this case the 1,000,000 of interest paid by the German (now CFC) would be immediately taxable in the US as passive income subject to Subpart F rules. The Obama tax proposals would repeal the Check the box option so in this case the 1,000,000 of interest paid by the German (now CFC) would be immediately taxable in the US as passive income subject to Subpart F rules.

would be immediately taxable in the US as passive income subject to Subpart F rules. The Obama tax proposals would repeal the Check the box option so in this case the 1,000,000 of interest paid by the German (now CFC) would be immediately taxable in the US as passive income subject to Subpart F rules..")

9

The Check the Box structures are very popular among multinationals because it helps to avoid Subpart F income and create cost methods of financing their subsidiaries. The US government doesn’t like them because they allow Multinational corporations an easy way to strip earnings.

10

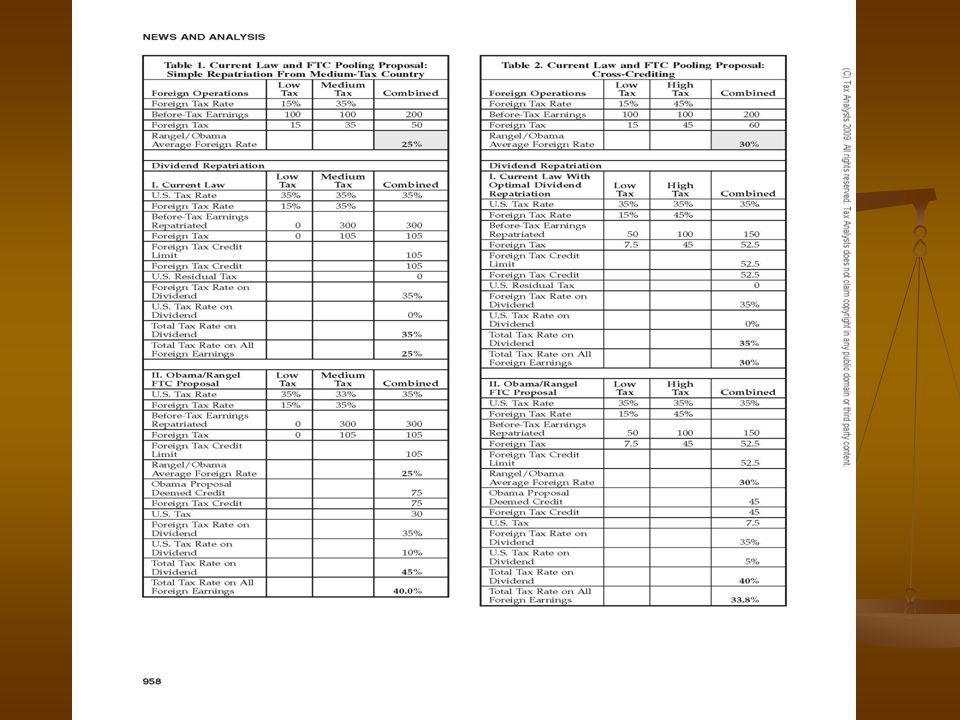

Repeal of Cross Crediting of Foreign Tax credits Currently US corporations can take a Deemed Foreign Tax Credit on dividends from their CFCs the DFTC is calculated Dividend/E &P x Foreign Tax. If tax rate in the CFC is under 35%(US rate) like Russia at 20 % the US parent would pay additional US tax. If the CFC has a higher tax rate than the US like Germany at 40% then the US parent not pay additional US tax on a dividend and would be allowed to the excess (40%-35%) as a credit on their Russian dividend. The Obama Tax proposals disallow this kind of cross crediting and a consolidated rate of all CFCs must be used to compute the FTC. Currently US corporations can take a Deemed Foreign Tax Credit on dividends from their CFCs the DFTC is calculated Dividend/E &P x Foreign Tax. If tax rate in the CFC is under 35%(US rate) like Russia at 20 % the US parent would pay additional US tax. If the CFC has a higher tax rate than the US like Germany at 40% then the US parent not pay additional US tax on a dividend and would be allowed to the excess (40%-35%) as a credit on their Russian dividend. The Obama Tax proposals disallow this kind of cross crediting and a consolidated rate of all CFCs must be used to compute the FTC.

like Russia at 20 % the US parent would pay additional US tax. If the CFC has a higher tax rate than the US like Germany at 40% then the US parent not pay additional US tax on a dividend and would be allowed to the excess (40%-35%) as a credit on their Russian dividend. The Obama Tax proposals disallow this kind of cross crediting and a consolidated rate of all CFCs must be used to compute the FTC. Currently US corporations can take a Deemed Foreign Tax Credit on dividends from their CFCs the DFTC is calculated Dividend/E &P x Foreign Tax. If tax rate in the CFC is under 35%(US rate) like Russia at 20 % the US parent would pay additional US tax. If the CFC has a higher tax rate than the US like Germany at 40% then the US parent not pay additional US tax on a dividend and would be allowed to the excess (40%-35%) as a credit on their Russian dividend. The Obama Tax proposals disallow this kind of cross crediting and a consolidated rate of all CFCs must be used to compute the FTC..")

12

Partial Repeal of Deferral Suppose two US companies decided to borrow $20,000,000 to invest in a new factory. Company A invests that money to build its plant in the U.S. while company B invests in Ireland which has a tax rate of 12%. Suppose two US companies decided to borrow $20,000,000 to invest in a new factory. Company A invests that money to build its plant in the U.S. while company B invests in Ireland which has a tax rate of 12%. If the interest on the loans of companies A and B is $2,000,000 both companies will realize a US tax reduction of $700,000. Company A will pay 35% US tax on its income while company B will pay only 12%. If the interest on the loans of companies A and B is $2,000,000 both companies will realize a US tax reduction of $700,000. Company A will pay 35% US tax on its income while company B will pay only 12%.

13

The current US Tax rules clearly favor the Irish company. The current US Tax rules clearly favor the Irish company. To correct the disadvantage that US investors endure the Obama Tax proposals would not allow a US tax deduction for the interest paid by the Irish company until the earnings of the Irish company are repatriated. To correct the disadvantage that US investors endure the Obama Tax proposals would not allow a US tax deduction for the interest paid by the Irish company until the earnings of the Irish company are repatriated.

14

The Obama administration’s Tax proposals will have little direct effect on US multinational companies doing business in Russia. However some effects on multinational companies as whole might be: The Obama administration’s Tax proposals will have little direct effect on US multinational companies doing business in Russia. However some effects on multinational companies as whole might be: o Changes in the MNC’s repatriation strategies. It is normal for an MNC to repatriate earnings from countries whose tax rate is greater than 35% or where they cross credit so that additional US tax liability is incurred. The new Tax rules will greatly limit a MNC’s repatriation options are likely to result in more foreign earnings offshore. o The WACC ( weighted average cost of capital will increase by about 3% and could reduce the amount an MNC invests in foreign plants.

15

The effective tax rate on MNCs is likely to increase by about 3%. This will reduce profits of MNCs and may affect their stock values and perhaps any stock based compensation plans the MNCs may have for their foreign managers. The effective tax rate on MNCs is likely to increase by about 3%. This will reduce profits of MNCs and may affect their stock values and perhaps any stock based compensation plans the MNCs may have for their foreign managers.

16

The United States along with the G20 are aggressively cracking down abuse of Tax Havens by individuals

17

Art Franczek President of The American Institute of Business and Economics artf@online.ru Thank You

Similar presentations

9.9% (2013) Corporate Tax Rate Switzerland 17.9% USA 35% Amount US MNCs avoid paying in taxes through tax.>")

and Harry Grubert (U.S. Treasury Department)>")