Download presentation

Presentation is loading. Please wait.

1

Analysis of Demand Charge and Other Natural Gas Pricing Issues

2

Valerie Wood 2386 Dahlk Circle Verona, WI 53593 Tel: (608) 848-6255 E-mail: vkwood@energysolutionsinc.com

")

3

Demand Charge Proposed Structure –Daily fixed facilities charge –Daily demand rate (NEW) –Volumetric rate Impacts –Class 6 (Fg-6, Ig-6, Tf-6)100,000 dth to 799,999 dth annually –Class 7 (Fg-7, Ig-7, Tf-7)800,000 dth to 999,999 dth annually –Class 8 (Fg-8, Ig-8, Tf-8)1,000,000 dth or more annually Class Types –Fg - System supply firm gas supplies –Ig – System supply interruptible gas supplies –Tf - Transportation

–Volumetric rate Impacts –Class 6 (Fg-6, Ig-6, Tf-6)100,000 dth to 799,999 dth annually –Class 7 (Fg-7, Ig-7, Tf-7)800,000 dth to 999,999 dth annually –Class 8 (Fg-8, Ig-8, Tf-8)1,000,000 dth or more annually Class Types –Fg - System supply firm gas supplies –Ig – System supply interruptible gas supplies –Tf - Transportation")

4

Demand Charge Implementation Maximum demand quantity (MDQ) Phase in starting 1/1/2008 –Month 1: MDQ based on peak day in Jan –Month 2: MDQ based on peak day for Jan-Feb –Month 3: MDQ based on peak day for Jan-Mar –….. –Month 12: MDQ based on peak day for Jan-Dec 2008 New rates effective 1/1/2009 –MDQ based on peak day for Jan-Dec 2008 MDQ established annually thereafter based on the last 12 months of usage.

5

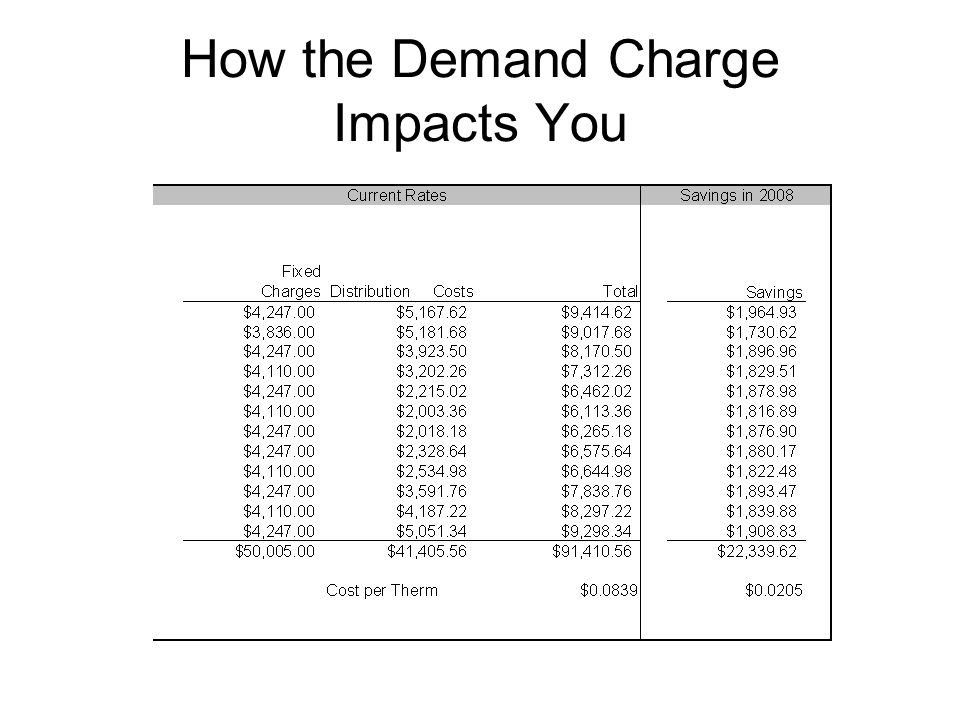

How the Demand Charge Impacts You

8

Demand Quantity Forgiveness Waiver Ability to waive the calculation of the demand quantity for a period of as long as 10 consecutive days effective annually starting on November 1. –Designed for infrequent, unusual, and short duration load increases. –Customer must file request for waiver at least 10 days prior to the requested waiver date. –Granting a waiver is at the utility’s discretion.

9

Elimination of Meter Aggregation Multiple meters are aggregated for billing. –Currently grand-fathered Potential impacts to customer if eliminated –The sum of the meter volumes can put a customer into a higher rate class. By separating the usage by individual meter, each meter will fall into its own rate class. –Smaller usage meters may no longer find it beneficial to transport. –The additional meter charge of $.12 per day will be eliminated and the customer will have to pay the applicable facilities charge for the rate class.

10

Elimination of Meter Aggregation Same as the utility proposed in Docket 05- UR-102. –PSC indicated that they will consider eliminating this practice in a future proceeding when there are fewer changes at work. Customer impact –If you currently have meter aggregation Impact: Increased costs (?) –If you don’t have meter aggregation Impact: Benefit is built into rates as this subsidy is eliminated.

–If you don’t have meter aggregation Impact: Benefit is built into rates as this subsidy is eliminated..")

11

Pulse Signal Device Tariff Allows customers and/or marketers to monitor natural gas usage real-time using the existing telemeter. –Installation fee for pulse equipment Existing telemeter: One-time fee of $400 New telemeter: One-time fee of $1,650 –Ongoing maintenance fee $.10 per day No charges for service calls in the first 180 days of installation After 180 days, customer is charged for all service calls (diagnostic and corrective) Cannot use data to dispute bill Optional service

Cannot use data to dispute bill Optional service.")

12

Annual Rate Audit Each year, customer’s usage is evaluated to determine which rate class it falls within. –New language: We Energies reserves the right to assign that meter to a rate class that it would have been assigned to had the customer actually consumed the gas in the annual rate audit period for which the company built sufficient facilities to serve. Reclassification from Class 5 to Class 6 –If no prior communication from utility of this change, the reclassification to Class 6 is waived for 6 months.

13

Natural Gas Price Update Why are prices so much higher this year than in 2006?

14

Natural Gas Price Update: CSU Hurricane Forecasts 05/31/05 5/31/06 5/31/07 Avg. Named Tropical Storms 15 17 17 9.6 Hurricanes 8 9 9 5.9 Intense Hurricanes 4 5 5 2.3 NOTE: 2006 & 2007 aren’t typos. The forecasts were identical. 2007 NOTES: Subtropical storm Andrea was not classified as a tropical storm by the National Hurricane Center, so it won’t be counted as a “named” tropical storm. Tropical Storm Barry will count as the first storm of the 2007 season.

15

Natural Gas Price Update CSU Hurricane Forecasts Probabilities for at least one major (category 3- 4-5) hurricane landfall on each of the coastal areas: Entire U.S. Coastline –5/31/06 (82%) vs. 5/31/07 (74%) U.S. East Coast incl. Peninsula Florida –5/31/06 (69%) vs. 5/31/07 (50%) Gulf Coast from the Florida Panhandle westward to Brownsville –5/31/06 (38%) vs. 5/31/07 (30%)

vs. 5/31/07 (74%) U.S. East Coast incl. Peninsula Florida –5/31/06 (69%) vs. 5/31/07 (50%) Gulf Coast from the Florida Panhandle westward to Brownsville –5/31/06 (38%) vs. 5/31/07 (30%).")

16

Natural Gas Price Drivers: Storage Inventories First week of June 20051,890 Bcf First week of June 20062,320 Bcf First week of June 20072,163 Bcf First week of June 5-year avg. 1,890 Bcf 10/31/07 Projections 3,400-3,500 Bcf

17

June: 90-Day Weather Forecasts Jul 06 – Sep 06 Jul 07 – Aug 07

18

June: Winter Forecasts Dec 06 – Feb 07

21

One Change from Last Year: Water Temperatures El Niño Conditions: Above-normal sea surface temperatures in the eastern Atlantic. These conditions tend to decrease Atlantic hurricane activity by increasing vertical wind shear across the area where Atlantic tropical cyclones develop. –CSU forecast indicated that they did not expect El Niño conditions to develop in 2006. La Niña Conditions: Below-normal sea surface temperatures in the eastern Atlantic. These conditions tend to facilitate tropical storm formation because of reduced vertical wind shear and weaker trade winds. –CSU forecasts indicate a gradual cooling and they expect La Niña conditions to form by summer/fall.

22

What the Future Holds Hedge funds (speculators) are protecting the $7.50 level. The question is whether or not they will able to continue to do that without support from Mother Nature. If weather is moderate, expect a gradual decline into July that will come to an end with the first hurricane activity. Hurricane-related rallies aren’t expected to be sustainable given the current supply situation. –Record level LNG imports –Gulf facilities have been reinforced –Exception – several hits like 2005 Winter premiums are likely to remain in tact until closer to November 2007. One Suggestion. Evaluate basis for winter (when commodity prices are the highest, it tends to be a good time to lock in basis).

..")

23

Thank You !! If you would like a copy of our Excel spreadsheet to compare your costs under the proposed demand charge, we’ll be happy to e-mail you a copy of the spreadsheet. Just give us a call or send us an e-mail with your request. Once you receive the spreadsheet, just input your usage data and the benefit or loss will automatically calculate for both 2008 and 2009. vkwood@energysolutionsinc.com (608) 848-6255

")

Similar presentations

Most LDCs served by 3 or fewer.>")