Download presentation

Presentation is loading. Please wait.

2

Introduction A recursive approach A Gerber Shiu function at claim instants Numerical illustrations Conclusions

3

Chan et al. (2003), Dang et al. (2009) - the initial capital of the i-th class of business; - the premium rate of the i-th class of business; - the k-th claim amount in the i-th risk process, with common cdf and pdf ; - the counting process for the i-th risk process. are common shock correlated Poisson processes occurring at rates respectively. where are independent Poisson processes with rates ;

- the initial capital of the i-th class of business; - the premium rate of the i-th class of business; - the k-th claim amount in the i-th risk process, with common cdf and pdf ; - the counting process for the i-th risk process. are common shock correlated Poisson processes occurring at rates respectively. where are independent Poisson processes with rates ;.")

5

Chan et al. (2003) Cai and Li (2005) Yuen et al. (2006) Li et al. (2007) Dang et al. (2009)

Cai and Li (2005) Yuen et al. (2006) Li et al. (2007) Dang et al. (2009)")

6

Chan et al. (2003) for Dang et al. (2009)

for Dang et al. (2009)")

8

Let follow independent PH distributions with parameters (α, T) and (β, Q).

and (β, Q).")

9

is a penalty function that depends on the surplus levels at time T or in both processes. Here are few choices of the penalty functions 1. 2. 3. 4.

10

Where correspond to the cases {τ 1 <τ 2 }, {τ 2 <τ 1 } and {τ 1 =τ 2 } respectively.

11

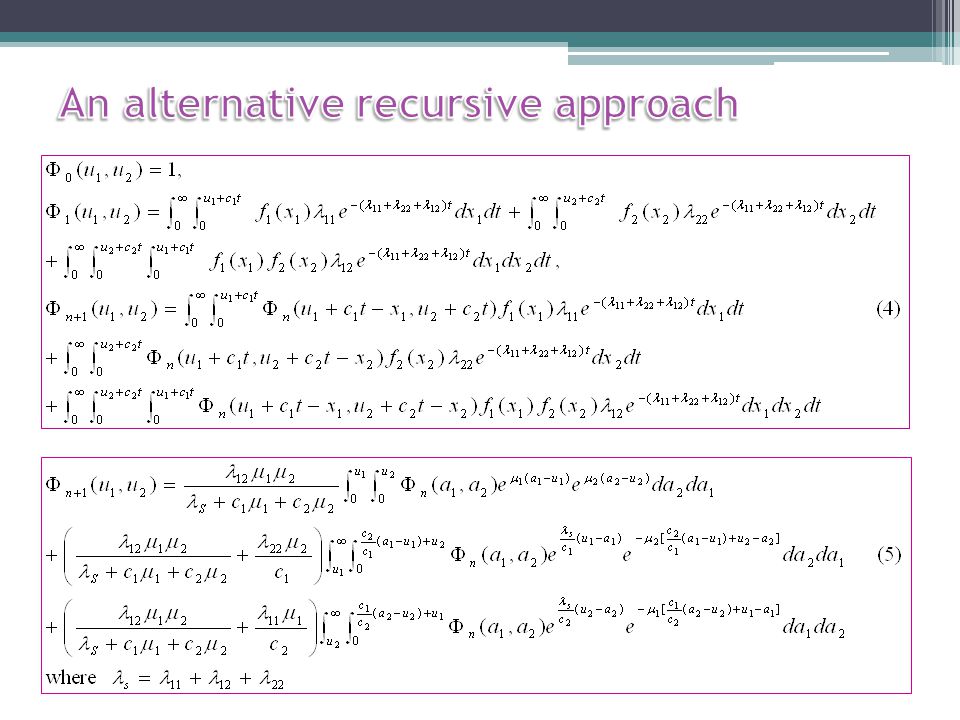

Considering the first case when ruin occurs at the first claim instant in {U 1 (t)} only and using a conditional argument gives By similar method, one immediately has. Hence by adding, we obtain the starting point of recursion. If, and, the three integrals reduce to

12

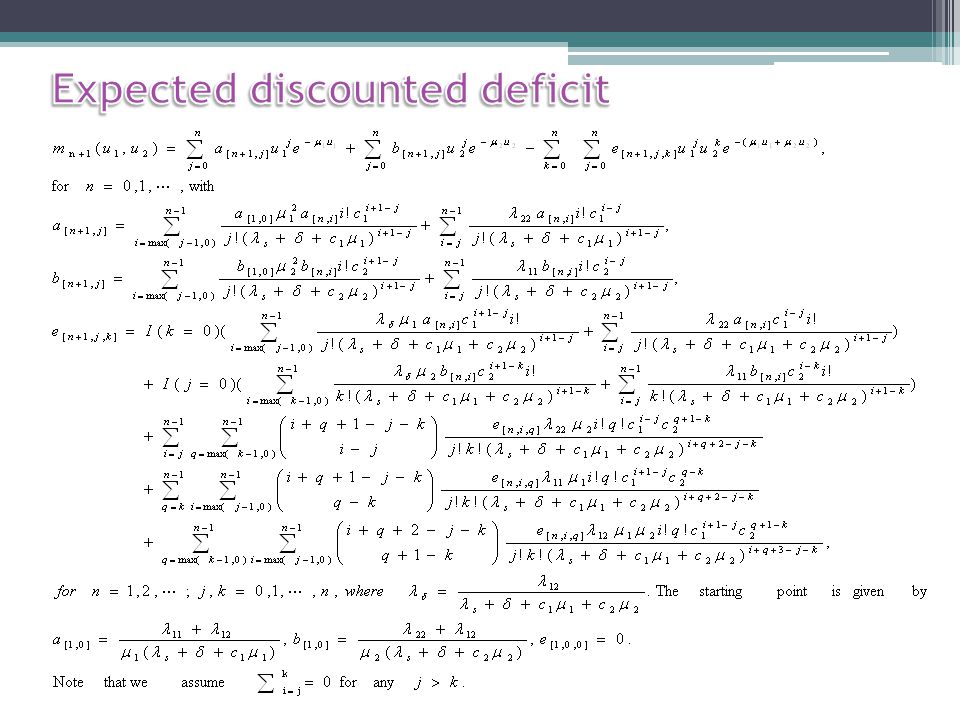

The idea that we use to find a computational tractable solution of (16) is based on mathematical induction. Therefore, the expected discounted deficit when ruin happens at the instant of the first claim is given by

14

Using equation (4) for n=0 and λ 11 =λ 22 =0 along with the trivial condition, we obtain

for n=0 and λ 11 =λ 22 =0 along with the trivial condition, we obtain")

16

We denote the survival probability associated to the time of ruin T and, by.

17

u 1 =2,u 2 =10, c 1 =3.2, c 2 =30, 1/µ 1 =1 and 1/µ 2 =10. Case 1: Independent model — λ 11 =λ 22 =2; λ 12 =0. Case 2: Three-states common shock model — λ 11 =λ 22 =1.5; λ 12 =0.5. Case 3: Three-states common shock model — λ 11 =λ 22 =0.5; λ 12 =1.5. Case 4: One-state common shock model — λ 11 = λ 22 = 0; λ 12 = 2. Note that λ 1 = λ 2 = 2, and θ 1 = 0.6 and θ 2 = 0.5.

18

In Case 1, after 100 iterations we obtain a ruin probability of 0.6306428 that is very close to the exact value of 0.6318894.

19

Cai and Li (2005, 2007) provided simple bounds for Ψ and (u 1, u 2 ) given by

provided simple bounds for Ψ and (u 1, u 2 ) given by")

20

δ = 0.05

21

This quantity is achieved by letting w 1 (y, z) = y+z and w 2 (.,. ) = w 12 (.,.) =0

= y+z and w 2 (.,. ) = w 12 (.,.) =0")

22

This quantity is achieved by letting w 2 (y, z) = y+z and w 1 (.,. ) = w 12 (.,.) =0

= y+z and w 1 (.,. ) = w 12 (.,.) =0")

23

Several extensions: 1.Correlated claims 2.Correlated inter-arrival times and the resulting claims 3.Renewal type risk models

Similar presentations

![Exponential and Poisson Chapter 5 Material. 2 Poisson Distribution [Discrete] Poisson distribution describes many random processes quite well and is mathematically.](/11/3232279/big_thumb.jpg "Exponential and Poisson Chapter 5 Material. 2 Poisson Distribution [Discrete] Poisson distribution describes many random processes quite well and is mathematically.>")

EM Theorem.>")