Download presentation

Presentation is loading. Please wait.

1

Pavement Planning from a Life Cycle Perspective Life Cycle Assessment and Life-Cycle Cost Analysis

2

This presentation has been prepared solely for information purposes. It is intended solely for the use of professional personnel, competent to evaluate the significance and limitations of its content, and who will accept full responsibility for the application of the material it contains. The National Ready Mixed Concrete Association and any other organizations cooperating in the preparation of this presentation strive for accuracy but disclaim any and all responsibility for application of the stated principles or for the accuracy of the content or sources and shall not be liable for any loss or damage arising from reliance on or use of any content or principles contained in this presentation. Unless otherwise indicated, all materials in this presentation are copyrighted to the National Ready Mixed Concrete Association. All rights reserved. Reproduction, modification or retransmission in any form is prohibited without the prior written permission of the National Ready Mixed Concrete Association. © 2009 National Ready Mixed Concrete Association.

3

Antitrust Policy Statement The National Ready Mixed Concrete Association assigns the highest priority to full compliance with both the letter and the spirit of the antitrust laws. Agreements among competitors that unreasonably limit competition are unlawful under federal and state antitrust laws, and violators are subject to criminal fines and incarceration, civil fines and private treble-damage actions. Even the successful defense of antitrust litigation or an investigation can be very costly and disruptive. It is thus vital that all meetings and activities of the Association be conducted in a manner consistent with the Association’s antitrust policy. Examples of illegal competitor agreements are those that attempt to fix or stabilize prices, to allocate territories or customers, to limit production or sales, or to limit product quality and service competition. Accordingly, it is inherently risky and potentially illegal for competitors to discuss under Association auspices, or elsewhere, the subjects of prices, pricing policies, other terms and conditions of sale, individual company costs (including planned employee compensation), the commercial suitability of individual suppliers or customers, or other factors that might adversely affect competition. It is important to bear in mind that those in attendance at Association meetings and activities may include competitors, as well as potential competitors. Any discussion of sensitive antitrust subjects with one’s competitors should be avoided at all times before, during, and after any Association meeting or other activity. This is particularly important because a future adversary may assert that such discussions were circumstantial evidence of an illegal agreement, when viewed in light of subsequent marketplace developments, even though there was, in fact, no agreement at all. If at any time during the course of a meeting or other activity, Association staff believes that a sensitive topic under the antitrust laws is being discussed, or is about to be discussed, they will so advise and halt further discussion for the protection of all participants. Member attendees at any meeting or activity should likewise not hesitate to voice any concerns or questions that they may have in this regard. Adopted by the NRMCA Board of Directors September 18, 2006.

, the commercial suitability of individual suppliers or customers, or other factors that might adversely affect competition. It is important to bear in mind that those in attendance at Association meetings and activities may include competitors, as well as potential competitors. Any discussion of sensitive antitrust subjects with one’s competitors should be avoided at all times before, during, and after any Association meeting or other activity. This is particularly important because a future adversary may assert that such discussions were circumstantial evidence of an illegal agreement, when viewed in light of subsequent marketplace developments, even though there was, in fact, no agreement at all. If at any time during the course of a meeting or other activity, Association staff believes that a sensitive topic under the antitrust laws is being discussed, or is about to be discussed, they will so advise and halt further discussion for the protection of all participants. Member attendees at any meeting or activity should likewise not hesitate to voice any concerns or questions that they may have in this regard. Adopted by the NRMCA Board of Directors September 18,")

8

Life Cycle Assessment

18

Life-Cycle Cost Analysis

24

Goal: Make pavements more sustainable Find the largest opportunities to reduce emissions in the pavement life cycle?

25

High volume road: Route 101 in Oxnard, CA (at Route 232 junction) 65 mph highway 3 lanes each direction + 4 shoulders Daily traffic: 139,000 (Of which trucks: 6,672) Moderate volume road: Route 67 in Ramona, CA (at Route 78 junction) 35 mph urban road 2 lanes in each direction + 4 shoulders Daily traffic: 23,400 (Of which trucks: 1,357) Low volume road: Route 178 in Sequoia National Forest 35 mph rural road 1 lane in each direction Daily traffic: 5,200 (Of which trucks: 468) Model Scenarios

65 mph highway 3 lanes each direction + 4 shoulders Daily traffic: 139,000 (Of which trucks: 6,672) Moderate volume road: Route 67 in Ramona, CA (at Route 78 junction) 35 mph urban road 2 lanes in each direction + 4 shoulders Daily traffic: 23,400 (Of which trucks: 1,357) Low volume road: Route 178 in Sequoia National Forest 35 mph rural road 1 lane in each direction Daily traffic: 5,200 (Of which trucks: 468) Model Scenarios")

27

Deflection

28

Roughness

32

Concrete’s LCCA

34

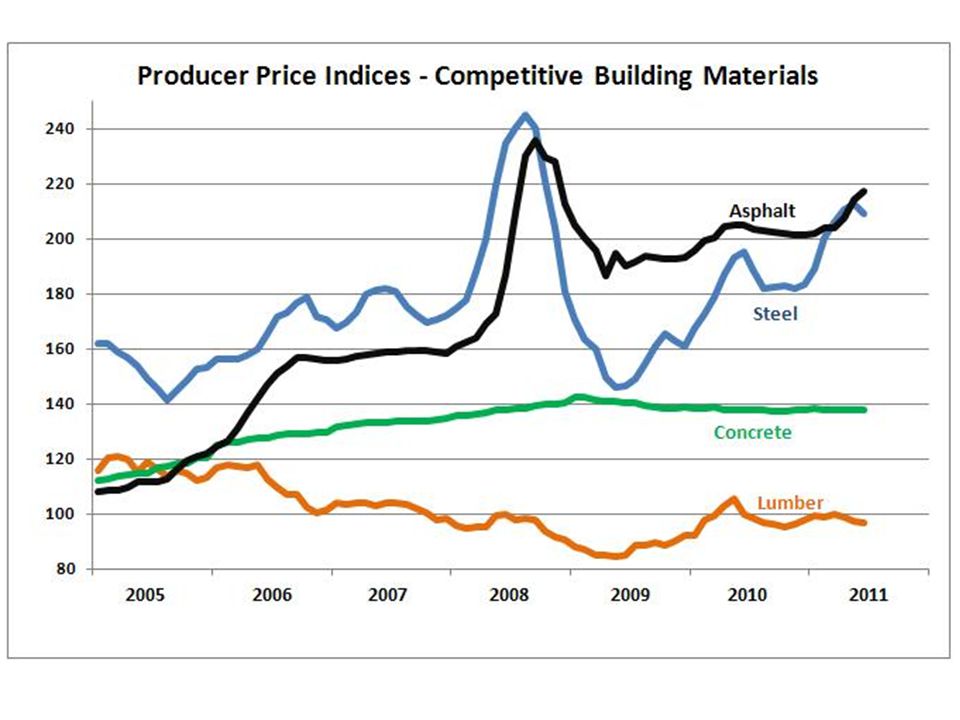

Return on Investment – Historically

35

Return on Investment – Today

36

Initial Cost Comparison FDOT Asphalt Design Subgrade 5.5” Asphalt Ty-SP 12” Limerock Base Course (LBR = 100) 0.75-1.5” Frict. Course 12” Type-B Stabilized Subgrade (LBR=40) FDOT Concrete Design MEDPG Optimized Concrete 23% 3% 1” Asph. Structural Layer 12.0” PCC Jointed w/ Dowels 4” ATPB non-structural 12” Type-B Stabilized Subgrade (LBR=40) Subgrade 1.5” Asph. Structural Layer 10.0” PCC Jointed w/ Dowels 12” Limerock Stabilized Base (LBR=70) Subgrade Initial costs for 10 miles, 2 lanes & Shoulders. Costs include Pavement, base, and subgrade stabilization materials and labor Asphalt = $85.00 / ton, Concrete CY Price = $104.62 ($94.62/CY + $10/CY for delivery) M $ The Florida DOT Example Mechanistic Empirical Design Pavement Guide (MEDPG) provides optimized pavement design Slide Courtesy of Cemex, Inc.

FDOT Concrete Design MEDPG Optimized Concrete 23% 3% 1 Asph. Structural Layer 12.0 PCC Jointed w/ Dowels 4 ATPB non-structural 12 Type-B Stabilized Subgrade (LBR=40) Subgrade 1.5 Asph. Structural Layer 10.0 PCC Jointed w/ Dowels 12 Limerock Stabilized Base (LBR=70) Subgrade Initial costs for 10 miles, 2 lanes & Shoulders. Costs include Pavement, base, and subgrade stabilization materials and labor Asphalt = $85.00 / ton, Concrete CY Price = $ ($94.62/CY + $10/CY for delivery) M $ The Florida DOT Example Mechanistic Empirical Design Pavement Guide (MEDPG) provides optimized pavement design Slide Courtesy of Cemex, Inc..")

38

“Perpetual Pavement” “Perpetual Payment”

44

Concrete Rehab: Patch & diamond grind at years 30 and 45 Asphalt Rehab: 4” AC Overlay in years 14 & 28 2” Mill / 4” AC Overlay in year 42 Design – Asphalt: 6.5” AC (inc 1.5” PFC) / 12” Limerock (LBR=100) / 12” Limerock (LBR=40); Concrete: 10” JPCP / 1.5” AC / 12” Limerock (LBR=70) Initial costs - Pavement, base, and subgrade stabilization materials and labor (Asphalt = $85.00 / ton, Concrete = $94.62 / CY) Rehabilitation - Concrete activities based on MEPDG, Asphalt Activities based on standard FDOT Standards Current year costs for asphalt are inflated at 5.9% and concrete at 4% Rehab costs also include other Incidental Costs (striping, mob, etc) - Assumed to be 40% of Material Costs and Traffic Control - 5% of material cost, Engineering & Inspection - 5% of material cost Nominal Expenditures by Pavement Type for 10 MilesTotal Cost Net Present Value Concrete Asphalt ASPHALT’S HISTORICAL 5.9% INFLATION GREATLY INCREASES THE ASPHALT COST OF OWNERSHIP M $ Asphalt is 84% more expensive when using historical inflation rates year 84%

/ 12 Limerock (LBR=100) / 12 Limerock (LBR=40); Concrete: 10 JPCP / 1.5 AC / 12 Limerock (LBR=70) Initial costs - Pavement, base, and subgrade stabilization materials and labor (Asphalt = $85.00 / ton, Concrete = $94.62 / CY) Rehabilitation - Concrete activities based on MEPDG, Asphalt Activities based on standard FDOT Standards Current year costs for asphalt are inflated at 5.9% and concrete at 4% Rehab costs also include other Incidental Costs (striping, mob, etc) - Assumed to be 40% of Material Costs and Traffic Control - 5% of material cost, Engineering & Inspection - 5% of material cost Nominal Expenditures by Pavement Type for 10 MilesTotal Cost Net Present Value Concrete Asphalt ASPHALT’S HISTORICAL 5.9% INFLATION GREATLY INCREASES THE ASPHALT COST OF OWNERSHIP M $ Asphalt is 84% more expensive when using historical inflation rates year 84%")

45

Concrete Rehab: Patch &diamond grind at years 30 and 45 Asphalt Rehab: 4” AC Overlay in years 10 & 20 2” Mill / 4” AC Overlay in years 30, 40, and 50 Design – Asphalt: 6.5” AC (inc 1.5” PFC) / 12” Limerock (LBR=100) / 12” Limerock (LBR=40); Concrete: 10” JPCP / 1.5” AC / 12” Limerock (LBR=70) Initial costs - Pavement, base, and subgrade stabilization materials and labor (Asphalt = $85.00 / ton, Concrete = $94.62 / CY) Rehabilitation - Concrete activities based on MEPDG, Asphalt Activities based on 2003 FDOT Pavement management records for interstates. Current year costs are inflated at 4% Rehab costs also include other Incidental Costs (striping, mob, etc) - Assumed to be 40% of Material Costs and Traffic Control - 5% of material cost, Engineering & Inspection - 5% of material cost Nominal Expenditures by Pavement Type for 10 MilesTotal Cost Net Present Value Concrete Asphalt ACTUAL 10 YEAR ASPHALT REHABILITATION SCHEDULES AND HISTORICAL 5.9% INFLATION ARE COMBINED M $ Using FDOT history and historical inflation, asphalt’s is 152% more than concrete year 152%

- Assumed to be 40% of Material Costs and Traffic Control - 5% of material cost, Engineering & Inspection - 5% of material cost Nominal Expenditures by Pavement Type for 10 MilesTotal Cost Net Present Value Concrete Asphalt ACTUAL 10 YEAR ASPHALT REHABILITATION SCHEDULES AND HISTORICAL 5.9% INFLATION ARE COMBINED M $ Using FDOT history and historical inflation, asphalt’s is 152% more than concrete year 152%.")

46

Miles of Roadway End Lane Miles = 8,316Trad. Concrete = 5,849 Asphalt = 9,425MEPDG Concrete Lane Miles

47

Miles of Roadway Lane Miles End Lane Miles = 8,316Trad. Concrete = 5,849 Asphalt = 9,425MEPDG Concrete

49

web.mit.edu/cshub

Similar presentations

Confidentiality & Conflict of Interest Palm Beach, Florida January 16, 2013 R. Darrell Taylor.>")