Download presentation

Presentation is loading. Please wait.

1

Health Insurance – Part 1 Eric Jacobson

2

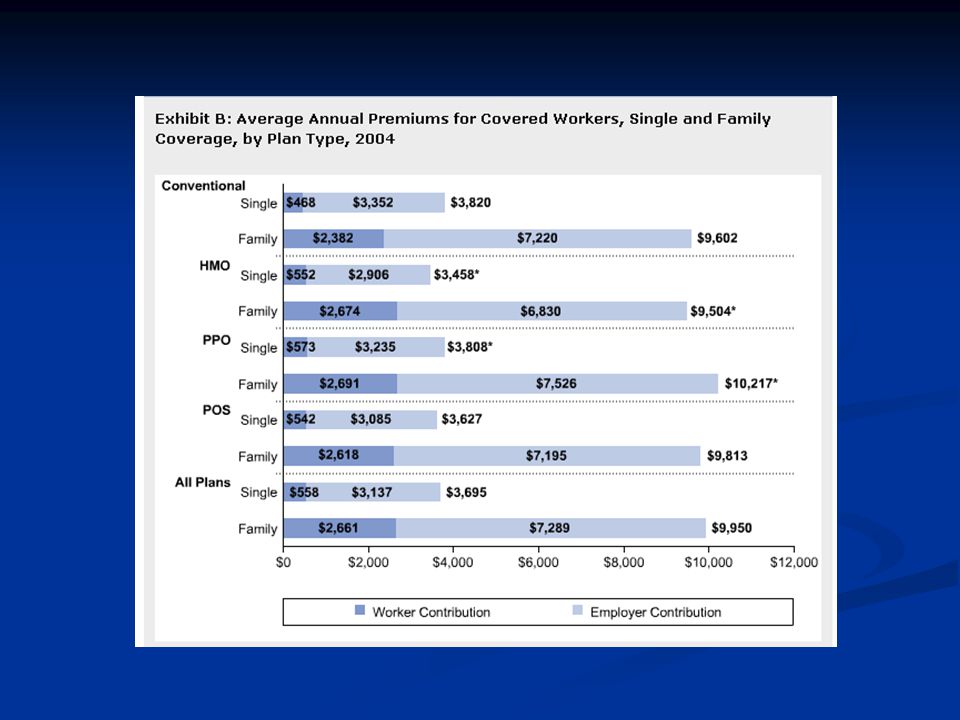

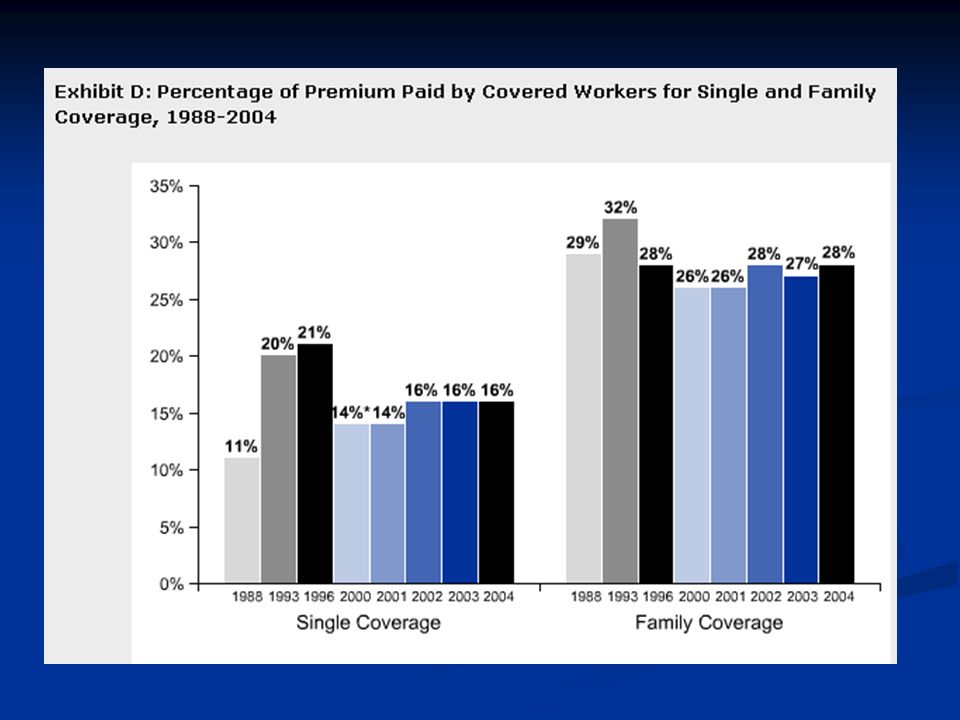

Employer Health Benefits 2004 Annual Survey Kaiser Family Foundation www.kff.org

9

Health Insurance Premiums Claims Experience 90% Loading Charge 10% The Determinants of Health Insurance Premiums

10

Health Insurance Premiums Claims Experience 90% Loading Charge 10% The Determinants of Health Insurance Premiums Determinants of Claims Experience Benefit Coverage Government Mandates Demographic characteristics of the insured Industry Region Medical inflation rate Cost-containment policies Co-payments Deductibles Utilization review Etc…

11

Health Insurance Premiums Claims Experience 90% Loading Charge 10% The Determinants of Health Insurance Premiums Determinants of Loading Charge Administrative costs Marketing costs Risk premium Reserves Profits

12

Risk Premiums: Primary vs. Secondary Risks Group insurance reduces “secondary risk.” Group insurance reduces “secondary risk.” Two kinds of risk... Two kinds of risk... Primary risk: calculated odds that a bad event will occur ($6000 expected value of health costs for an adult.) Primary risk: calculated odds that a bad event will occur ($6000 expected value of health costs for an adult.) Secondary risk: chance that the actual payout doesn’t equal the calculated expected value. (The calculation proves to be wrong.) Larger numbers reduce secondary risk. Secondary risk: chance that the actual payout doesn’t equal the calculated expected value. (The calculation proves to be wrong.) Larger numbers reduce secondary risk.

Primary risk: calculated odds that a bad event will occur ($6000 expected value of health costs for an adult.) Secondary risk: chance that the actual payout doesn’t equal the calculated expected value. (The calculation proves to be wrong.) Larger numbers reduce secondary risk. Secondary risk: chance that the actual payout doesn’t equal the calculated expected value. (The calculation proves to be wrong.) Larger numbers reduce secondary risk..")

14

Typical Loading Fees by Group Size As a Percent of Benefits (Phelps, p. 343)

")

15

“Small-business profits are getting pinched because of price increases for employee health insurance. Among small companies that posted lower earnings in August vs. a year ago, 18% blamed higher insurance costs, says a survey of 544 firms by the National Federation of Independent Business trade group. In a similar survey a year ago, 11% blamed health insurance costs for their earnings dip.” Rising health costs take bite out of small biz – USA Today 10/5/03

16

Why is Small Group Health Insurance So Expensive? Per capita loading costs decrease as firm group size increases – econ of scale. Per capita loading costs decrease as firm group size increases – econ of scale. Loading costs = (risk premium + administrative costs + marketing costs + profits) Small group purchasers have less bargaining power. Small group purchasers have less bargaining power. Adverse selection. Adverse selection.

Small group purchasers have less bargaining power. Small group purchasers have less bargaining power. Adverse selection. Adverse selection..")

17

Key Definitions Adverse selection – Enrollees may seek to join a health plan at a premium that reflects a lower level of risk than their own. Adverse selection – Enrollees may seek to join a health plan at a premium that reflects a lower level of risk than their own. Risk selection (cream skimming) – Occurs when insurers attempt to attract more favorable risk group. Risk selection (cream skimming) – Occurs when insurers attempt to attract more favorable risk group. Moral hazard – Any change in individual behavior due to insurance that increases expected losses, such as higher utilization of covered services. (Seat belts, Lipitor, low copayments) Moral hazard – Any change in individual behavior due to insurance that increases expected losses, such as higher utilization of covered services. (Seat belts, Lipitor, low copayments)

– Occurs when insurers attempt to attract more favorable risk group. Risk selection (cream skimming) – Occurs when insurers attempt to attract more favorable risk group. Moral hazard – Any change in individual behavior due to insurance that increases expected losses, such as higher utilization of covered services. (Seat belts, Lipitor, low copayments) Moral hazard – Any change in individual behavior due to insurance that increases expected losses, such as higher utilization of covered services. (Seat belts, Lipitor, low copayments).")

18

Adverse Selection Sicker individuals more likely to: Sicker individuals more likely to: Demand insurance Demand insurance Demand more generous insurance, given a choice of plans Demand more generous insurance, given a choice of plans Largely due to “asymmetric info” (individuals vs insurers). Largely due to “asymmetric info” (individuals vs insurers). This process, called adverse selection (or self- selection), complicates the issue of how much choice to offer consumers in the health care market. This process, called adverse selection (or self- selection), complicates the issue of how much choice to offer consumers in the health care market.

. This process, called adverse selection (or self- selection), complicates the issue of how much choice to offer consumers in the health care market. This process, called adverse selection (or self- selection), complicates the issue of how much choice to offer consumers in the health care market..")

19

Consequence of Adverse Selection and Community Rating: Persons with poorer-than-average health status apply for, or continue, insurance coverage to a greater extent than do persons with average or better health expectations. Persons with poorer-than-average health status apply for, or continue, insurance coverage to a greater extent than do persons with average or better health expectations. Experience Rating? Experience Rating?

20

An Example of Adverse Selection 100 People 1% chance of needing $100k treatment Pure Premium = 1 Person 30% chance of needing $100k treatment Pure Premium = ? (asymmetric info) $1,000

$1,000.")

Similar presentations

>")