Download presentation

Presentation is loading. Please wait.

1

Banking and Finance Industry in Hong Kong 09011242 Tsoi Yat Fei 09012680 Cheung Kwok Tung 09010408 Mok Ka Yan

2

Introduction B&F is one of HK’s “pillar” industries Its GDP’s contribution increased from 10% in 1997 to 16% in 2006 Central Govt stated repeatedly supporting HK’s status as an “International Financial Centre”

4

In 2007 68 of World’s top 100 banks operating in HK. A total of 258 foreign owned fin institutions operating in HK. World’s 15th largest banking centre in terms of external assets.

5

6th largest centre for FX trading 7th stock market in terms of market cap 5th in terms of total equity funds raised About US$800b under asset management

8

HK’s core competence and challenges a strong cluster of international firms and services providers strong links with Mainland and SE Asia free capital flows and highly liquid market rule of law

10

Latest developments in banking sector HK’s banking industry underwent some difficulties since Asian Financial Crisis in 1998, with contracting loan portfolio and rising bad debts. But banking structure has remained stable. Average capital adequacy ratio of banks was 28% in 2Q 2004, much higher than minimum requirement of about 10%.

11

HK’s banking industry underwent some difficulties since Asian Financial Crisis in 1998, with contracting loan portfolio and rising bad debts. But banking structure has remained stable. Average capital adequacy ratio of banks was 28% in 2Q 2004, much higher than minimum requirement of about 10%.

12

Banking rebounded significantly in 2004 and 2007 was a very profitable year.Profits for HSBC’s Asia ‐ Pacific operation increased sharply by 53% in 2007 to HK$13.3b. 2008 was the worse year for banking and finance globally, given subprime debacle and meltdown of international investment banking industry. Global investment banking collapsed.

13

For example, HSBC needed to provide US$10b bad ‐ debt provisions in 1 st half of 2008. Total profits declined by 29% and HK’s profit declined by 8%. Losses spread from developed markets to developing markets

15

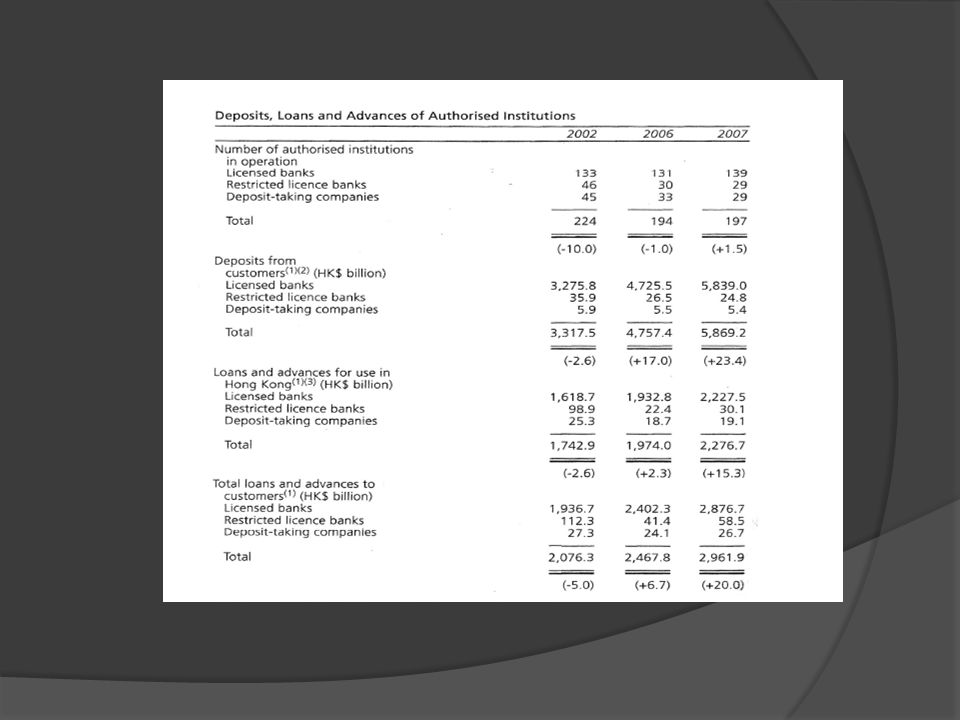

Major structural features of banking industry A 3 tier system: 142 commercial banks, 29 restricted licensed investment banks and 29 DTCs by end ‐ 2007 Govt tightened regulatory requirements: to improve stability of banking sector; # of fin institutions declined sharply after Asian fincrisis; banks from 185 in 1995 to 133 in 2005, DTCs from 132 to 29.

16

Capital adequacy ratio remained high by international standard Japan encountered severe recession in 1990s: greatly reduced business operation in HK, # of banks in HK declined from 46 to 11,DTCs from 37 to 3. US, Mainland and local banks also declined, while Taiwan banks increased from 5 in 1999 to 17 in 2007.

18

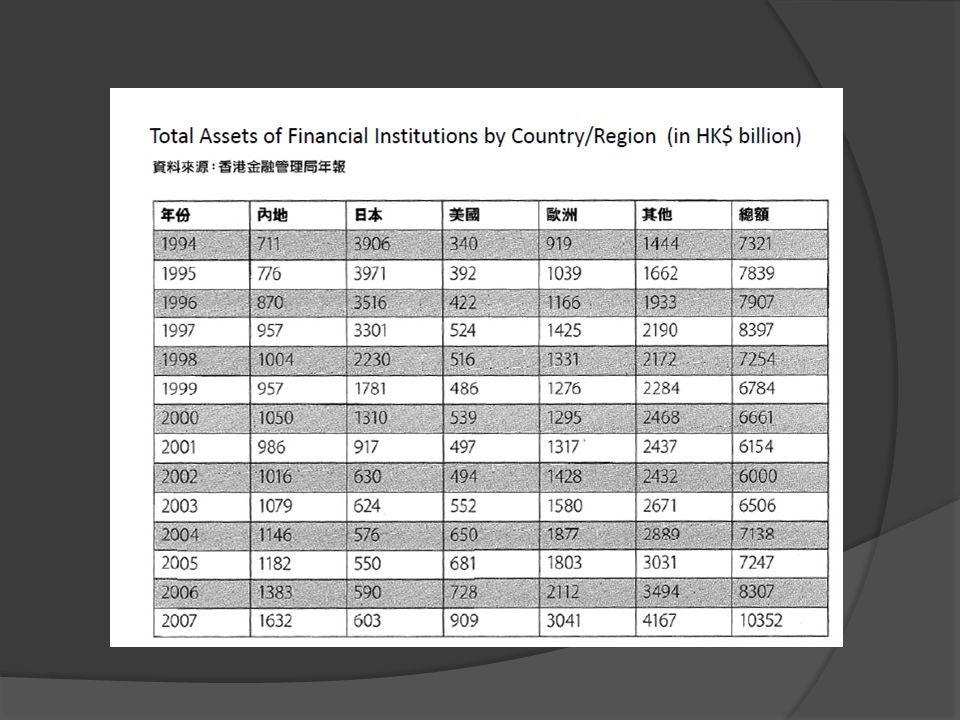

Total banking assets were HK$10,400b, 16 % by Mainland banks, 9% US, 6% Japan, 30% European Total banking assets declined from HK$8,400b in 1997 to HK$6,000b in 2002, down by 29%; mainly due to contraction of Japanese banks and weak economic activities.

19

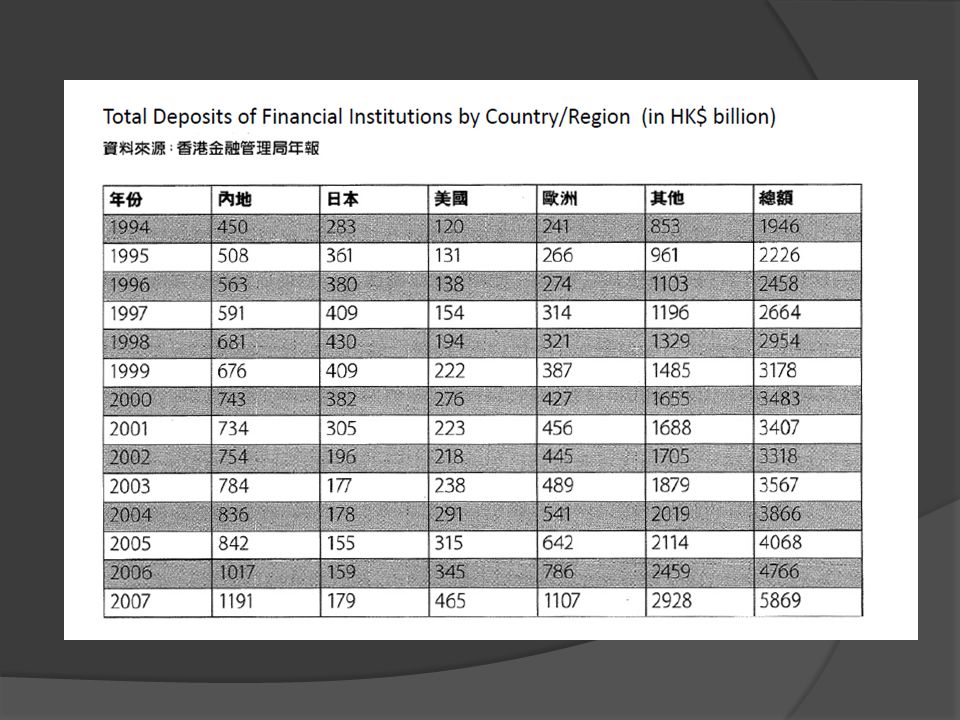

Between 1994 & 1997, Japanese banks loans accounted for more than 50% of total loans; HK was used as a “Booking Centre” for their regional loans; Japan’s 80% loans were overseas loans. As for other banks, about 80% loans were used in HK.

20

Trends for merger and acquisition intensified in 2000s: e.g. Bank of East Asia purchased First Pacific Bank (2000), DBS purchased Dao Heng Bank (2001), BA (Asia) acquired by a Mainland Bank; because more severe competition, economies of scale, required larger asset size to enter Mainland market

, DBS purchased Dao Heng Bank (2001), BA (Asia) acquired by a Mainland Bank; because more severe competition, economies of scale, required larger asset size to enter Mainland market.")

28

With declining traditional businesses, banks expanded aggressively into non ‐ interest earning businesses, e.g. wealth management, fund management, insurance, investing in other fin assets. Banks’ new strategy was very successful until collapse of Lehman Minibond & Accumulator in 2nd half of 2008.

29

Banking is under restructuring now: (i) more conservative & returning to basics, (ii) declining non interest income, (iii) deteriorating risk profile of borrowers, (iv) restrictive lending and de ‐ leveraging, (v) increasing interest & other fees, (vi) more provisions, (vii) declining returns.

more conservative & returning to basics, (ii) declining non interest income, (iii) deteriorating risk profile of borrowers, (iv) restrictive lending and de ‐ leveraging, (v) increasing interest & other fees, (vi) more provisions, (vii) declining returns.")

31

Latest developments of securities industry Market capitalization increased rapidly from HK$6,700b at end ‐ 2004 to HK$20,700b at end ‐ 2007, mainly due to listing of many large Mainland companies in HK. HK ranked 7th internationally Total banking assets declined from HK$8,400b in 1997 to HK$6,000b in 2002, down by 29%; mainly due to contraction of Japanese banks and weak economic activities.

32

In 2008, HSI and share prices of many major listed companies once declined by more than 60%. Share prices of HKEx (0388) dropped from a high of HK$265.6 to HK$49.7. IPO activities contracted sharply in 2008 Derivative warrants became very active in recent years, with largest trading volume globally and a lot of retail interest.

dropped from a high of HK$265.6 to HK$49.7. IPO activities contracted sharply in 2008 Derivative warrants became very active in recent years, with largest trading volume globally and a lot of retail interest..")

33

Major structural features of securities industry There were 1,248 listed companies with 444 Mainland ‐ related (5/2008).Mainland companies accounted for about 57% of market cap, up from 27% in 2000 & about 70% of average daily transactions.

.Mainland companies accounted for about 57% of market cap, up from 27% in 2000 & about 70% of average daily transactions.")

37

Between 2003 and 2007, HK ranked within top 5 internationally in terms of fund ‐ raised Top 10 largest IPOs in the last few years were all Mainland ‐ related companies and 9 of them were financial institutions

38

Businesses of large IPOs were concentrated with large investment banks, e.g. BOC Finance, Morgan Stanley, Goldman, Deutsche Bank, Merrill Lynch, HSBC, Citi, etc. Other smaller sponsors involved in smaller IPOs.

40

Report on Econ Submit on “China’s 11 Five ‐ year Plan & Development of HK”, 2007. Major recommendations for promoting HK’s Banking & Financial Sector: (i) Explaining to Central Govt ways to better utilize HK’s financial system & position to benefits Mainland’s development

Explaining to Central Govt ways to better utilize HK’s financial system & position to benefits Mainland’s development.")

41

(ii) HK’s regulatory organizations and fin industry should be actively seeking opportunities to set up regular mechanisms to work closely with relevant departments in Mainland to formulate relevant fin policies & strategies.

HK’s regulatory organizations and fin industry should be actively seeking opportunities to set up regular mechanisms to work closely with relevant departments in Mainland to formulate relevant fin policies & strategies.")

42

(iii) HK’s regulatory organizations should cooperate closely together with relevant departments in Mainland to explore technical implementation details of various financial policies.

HK’s regulatory organizations should cooperate closely together with relevant departments in Mainland to explore technical implementation details of various financial policies.")

43

(iv) HK’s regulatory organizations should cooperate closely together with relevant departments in Mainland to explore technical implementation details of various financial policies.

HK’s regulatory organizations should cooperate closely together with relevant departments in Mainland to explore technical implementation details of various financial policies.")

44

(v) Liberalizing restrictions to permit more HK financial companies to operate freely in Mainland. (vi) Liberalizing Mainland’s investors, companies & fin institutions to “go out”, using HK as a platform.

Liberalizing Mainland’s investors, companies & fin institutions to go out , using HK as a platform..")

45

(vii) Permitting HK’s fin instruments to be traded in Mainland, particularly those issued by Mainland institutions in HK (viii) Strengthening HK’s position to manage RMB transactions. (ix) Enhancing connections of HK & Mainland’s financial infrastructure development

Enhancing connections of HK & Mainland’s financial infrastructure development.")

46

(x) Encouraging more Mainland institutions using HK’s finmarket for international asset management. (xi) Enhancing HK’s position as insurance and reinsurance centre.

Enhancing HK’s position as insurance and reinsurance centre..")

47

Regarding securities market: (i) Inviting more Mainland companies to be listed in HK, on a sustainable basis. (ii) Reducing transaction cost in securities market. (iii) Reviewing securities market’s regulatory framework.

Reducing transaction cost in securities market. (iii) Reviewing securities market’s regulatory framework..")

48

(iv) Encouraging financial innovations. (v) Promoting activities of fin intermediaries. (vi) Providing legal backing to listing rules.

Providing legal backing to listing rules..")

49

Regarding FX & Futures Markets: (i) Developing RMB’s futures and options market. (ii) Attracting Mainland users to participate in HK market. (iii) Strengthening regulatory system & mechanism for FX, Futures & Commodities markets.

Attracting Mainland users to participate in HK market. (iii) Strengthening regulatory system & mechanism for FX, Futures & Commodities markets..")

50

(iv) Developing more commodity trading products for HK’s market. (v) Developing HK’s asset management business.

Developing HK’s asset management business..")

51

(iv) Developing more commodity trading products for HK’s market. (v) Developing HK’s asset management business.

Developing HK’s asset management business..")

52

Collapse of Lehman Brothers in US resulted in a financial & political crisis in HK. “Lehman Minibond” & Re ‐ regulation for HK: Over 40,000 investors involved, with more than HK$20b. Some people lost all their savings.

53

What are the issues: (i) structural weakness of the current regulatory system (HKMA, SFC, HKAB) (ii) unethical business practices of management/individual banking employees (iii) insufficient investors’ education.

structural weakness of the current regulatory system (HKMA, SFC, HKAB) (ii) unethical business practices of management/individual banking employees (iii) insufficient investors’ education.")

54

What are the issues: (i) structural weakness of the current regulatory system (HKMA, SFC, HKAB) (ii) unethical business practices of management/individual banking employees (iii) insufficient investors’ education.

structural weakness of the current regulatory system (HKMA, SFC, HKAB) (ii) unethical business practices of management/individual banking employees (iii) insufficient investors’ education.")

55

Inquiry question What are the positions of HK Govt, HKMA, SFC, major political parties? Why are they different?

Similar presentations

Households Firms Government Foreigners Financial Markets.>")

>")