Download presentation

Presentation is loading. Please wait.

1

POULTRY SECTOR IN TURKEY AND MARKET CLIMATE PREPARED BY : AYHAN KINDAP / CP TURKEY JUNE 23 2009

4

TURKISH POULTRY SECTOR IN BRIEF The industrialization of Turkish poultry sector goes to 1955 and has grown enormously recently There are app. 12,500 broiler houses and over 500,000 people are employed in the sector including producers, farmers, traders, feed manufacturers, medicine producers, transportation companies Some 2 mln. people rely on the poultry sector to make a living Annual turnover of the sector is about US $ 3 bln. Poultry meat production capacity of Turkey is 4500 mt/day and 1,400,000 mt currently

5

TURKISH POULTRY SECTOR IN BRIEF (continued) Capacity utilization rate at the slaughter houses and breeding poultry houses is approx. 80 % Turkey per capita consumption is around 17 kg while it was 3.8 kg in 1990.This trend shows that there is a big increase potential in the sector. The owners are using their own capital in order to survive. Inspite of all difficulties, the sector continues to grow by a great sacrifice. Sector needs export incentives and per capita income increase for further growth

8

BROILER MEAT PRODUCTION TURKEY IS THE 14TH BIGGEST CHICKEN MEAT PRODUCER WITH 1,150,000 MTS OF CHICKEN MEAT PRODUCED IN 2008 SOURCE :USDA

9

TURKEY WITH 17 KG PER CAPITA CONSUMPTION RANKS 17TH WORLDWIDE

10

TURKEY’S FINANCIAL STANDING Turkish banking sector not affected by the financial crisis as much as the US and European banks because they did not have any toxic instruments. The financial crisis in 2001 lead Turkey to make some financial reforms and to re-structure the banking sector in a sound way. Those structuring now has helped the sector passing this period relatively better than the other countries. Turkey’s position looks better than the average global situation A positive growth is expected after the last quarter in 2009.

11

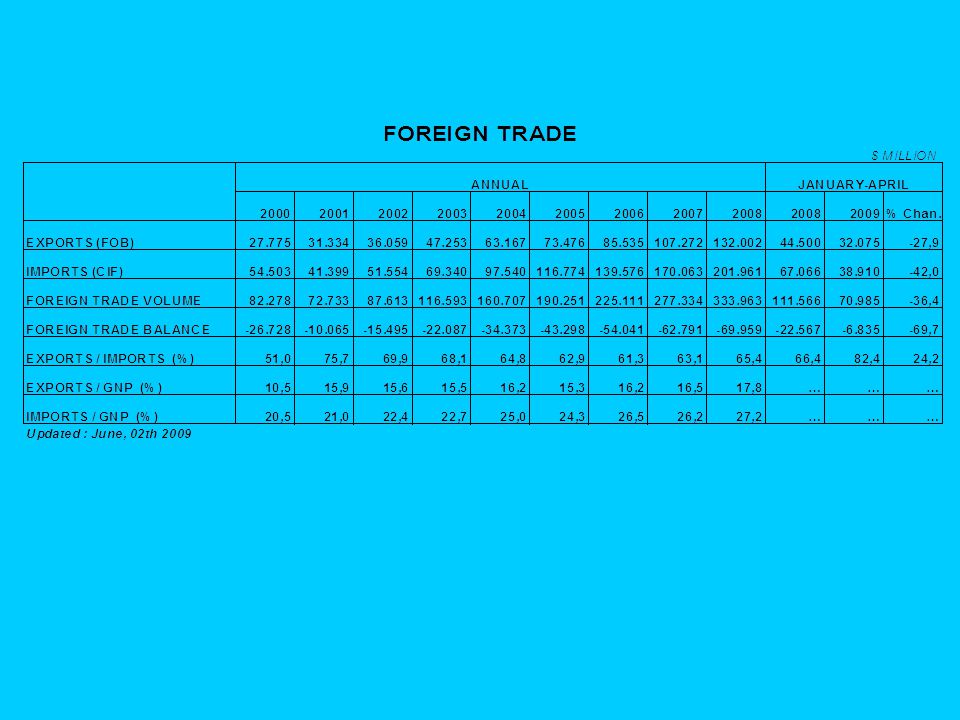

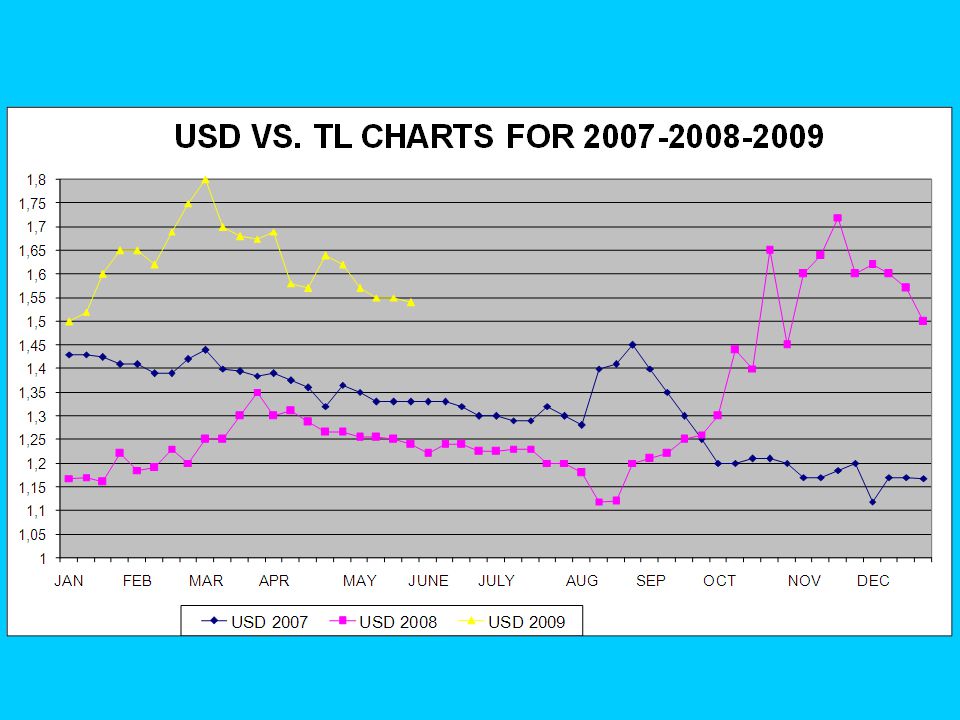

TURKEY’S FINANCIAL STANDING (continued) Amongs the trade volume, credit lines and portfolio investments, Turkey has been affected more by the trade volume drops as can be seen in export and import figures. IMF agreement has not been signed yet. But the government does not see it as a must. Turkey’s interest rates have been recently decreased to more reasonable levels. Credit lines by the banks are still very tight to the real sector.

12

CHRONOLOGY OF CRISIS IN CHICKEN MEAT SECTOR -The sector accused of using hormons in 2004, which caused substanstial sale drops -Bird-flu outbreak in October 2005 and continued in 2006, which caused sale volumes to drop down by 95 %. -Outbreak of tick bite in the fields transfering crimean-congo hemorrhagic fever virus and many incidences of deaths in 2008 -Excess capacity operation in 2008 of the companies hoping to repeat the excellent profitable year in 2007 -Rising commodity and energy prices in 2008 could not be transfered to sale prices

13

-Naturally record losses at the end of 2008 -In addition to huge losses in 2008, the sector members under the examination by the Turkish competition authority for cooperation suspician -Finally global financial crisis in 2008 fall gave a hard hit and caused serious working capital shortages - Devaluation of Turkish TL put additional pressure on the chicken cost because of the cost structure heavily dependent on the imported raw materials CHRONOLOGY OF CRISIS IN CHICKEN MEAT SECTOR (continued )

")

14

ACTIONS AND EFFORTS MADE DURING THE PAST CRISIS Healthy Chicken Platform was established to deal with hormon crisis and then after with bird flu problems. A lot of publications issued and many announcements and programs made to enlighten the public media The poultry meat producer association (BESD-BIR) assumed an important mission to find solutions to the sector’s problems.

assumed an important mission to find solutions to the sector’s problems..")

15

ACTIONS AND EFFORTS MADE DURING THE PAST CRISIS (continued) BESD-BIR analysed the market and made reasonable production projections for the coming years to regulate the market The sector improved their production facilities and invested in bio-security to attain EU standards. Chicken meat used to be sold at 85 % bulk before the bird flu crisis. Now all the chicken meat are packed and branded.

16

PRECAUTIONS TAKEN IN THE COMPANY LEVEL DURING THE FINANCIAL CRISIS PROCUREMENT SIDE - Increased the payment terms to suppliers -Decreased inventory to min. Level -Avoided purchases by hard currency -Decreased imports of raw materials SALE - Reduced collection days -No new buyers accepted -Tight collection policy implied GENERAL - Savings in all expenses -Over head expenses reduced -Traveling expenses reduced

17

SECTOR’S STRONG POINTS The food sector is supposed to be the less affected sector in a financial crisis. Chicken meat is always preferred in Turkey because of relatively cheaper price compared to red and fish meat prices which are 3-4 times higher Majority of the population in Turkey is muslim. They don’t eat porc meat. Poultry meat has a great consumption potential Exports to Irak have reached a substantial level. That alleviates the local domestic market supply pressure. Expect more exports in 2009 Financial crisis did not reduce the chicken meat consumption in Turkey Turkish poultry sector have modern and technologically renewed facilities. 60 % of the sector has export licence for EU

18

SECTOR’S STRONG POINTS (continued) Turkey is ranked the 4th largest chicken producer in EU countries after Spain, UK, and France. Existingly, chicken meat produced in Turkey is free from bird flu Almost all sector facilities have air-chillers as opposed to the existingly leading exporting countries. Fresh chilled chicken meat can be exported to nearby countries because of proximity Bio-security conditions comply with EU norms Turkey is increasingly attracting more tourists reaching 26 mln people yearly

19

SECTOR’S WEAK POINTS Turkey upto now could not be a major player in chicken meat market worldwide because it is competing with USA and BRASIL producers which they can procure corn and soybean at much cheaper prices. After the crisis oil prices and commodity prices reduced. But producers could not enjoy enough the cheap energy prices nor cheap corn prices Although 90 % of the corn need can be produced locally. Cost is double. Export is not enough to regulate surplus suply Turkey ranks 14 th in the world chicken meat production. But only 3 % can be exported existingly

20

SECTOR’S WEAK POINTS (continued) Although Turkey geographically is located at the center of main consumption areas which are Europe, Middle East and Russia. Turkey can not be competitive in these markets since the sector can not enjoy export incentives like US producers with 600 usd/mt and European producers with 525 usd/mt. Turkey’s support is as low as 26 USD/mt Turkey’s poultry sector has always been in a perfect competition described in economics books. Ambitious Poultry companies trying to be the number 1 in the market disregarding the analytical studies showing the size of the market. Unfortunately, all sector members became the victim of over-competition. The global financial crisis cought the sector in their weakest period until when they had been already making loss for 14 months.

21

INPUT MATERIALS AND EFFECTS ON THE SECTOR

22

TURKEY GRAIN PRODUCTION (1000 TONS ) AND 2009 ESTIMATES

AND 2009 ESTIMATES")

23

TURKEY’S RAW MATERIAL IMPORTS

29

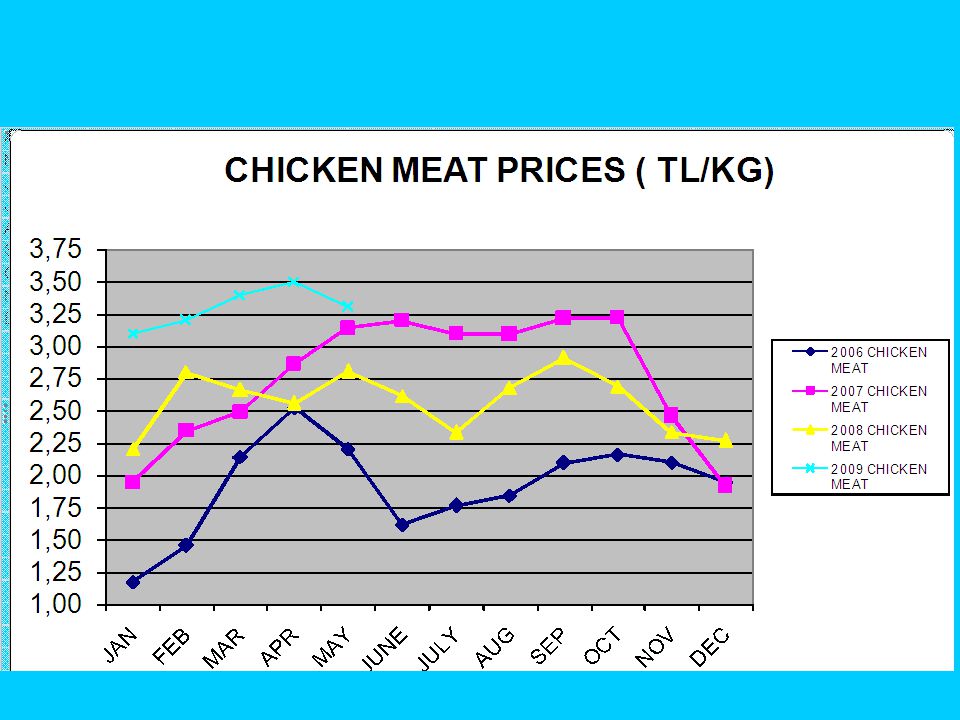

CHICKEN MEAT CHICKEN MEAT SALE PRICE vs COST –2004 – 2009(2) ( TL/Kg) ( TL/Kg) T

( TL/Kg) ( TL/Kg) T")

30

DAMAGES OF GLOBAL FINANCIAL CRISIS ON TURKISH POULTRY SECTOR 3 middle sized poultry producers had to stop operation because of lack of working capital. Many people lost their jobs because of lay-offs Number of raw material suppliers are reduced. Supply and competitive raw material prices are gone. Increasing liabilities to banking sector presenting further financial risks

31

WHAT TURKISH POULTRY SECTOR SHOULD DO 35 % of the world chicken meat exports are made to the countries nearby Turkey. Turkey need to concentrate on these countries and find ways to be competitive in these markets. Companies should study market size and produce accordingly. Chicken meat producers and raw material suppliers should cooperate more. Both of the sectors are dependent on each other. Strategical alliances and partnerships need to be established to create synergies amongs those in the food chain Cost consiousness and savings have been never be needed so badly

32

WHAT SHOULD BE DONE GLOBALLY Commodity prices are subject to great speculations. Entry of Speculators must be limited and regulated in these markets. Purchasing power of consumers should be increased Crop Planted areas need to be increased Crop and yield improvements Cost improvements More information sharing amongs the related parties More performance-oriented and target-oriented management understanding need to be praised in the companies to raise new management teams

33

CONCLUSIONS Chicken business is a very risky business already in itself Capacity up and downs in the sector take long time Many health issues affecting the consumption substantially. Input raw materials are heavily dependent on wheather conditions and continously fluctuating. Commodity price movements after the involvement of hedge funds became out of control. They need to be regulated Rising demand for meat worldwhite increases the demand for grain and oil seeds, which causes them to be more expensive On the other hand,chicken meat prices are almost constant.

34

CONCLUSIONS No demand rationing seen yet in spite of increasing commodity prices Majority of the people has either constant income or reducing income. There is not much hope for chicken meat price increase The business used to be cycling. Profitable years was following the loss years. But now, lost years are more dominating. New risk management systems should be utilized to maintain the sector’s future Collective efforts now are more needed for everyone in the food chain to have a sustainable growth in the future.

35

THANK YOU Ayhan Kindap / CP GROUP Turkey Head of Purchasing and Foreign Trade ayhank@superonline.com

Similar presentations

2.UNEMPLOYMENT 3.INFLATION 4.INCOME PER CAPITA 5.BALANCE OF PAYMENTS: EXPORTS.>")

Muthanna Investment Company (MIC)>")

World Bank Currency: Renminbi Gross domestic product:>")