Download presentation

Presentation is loading. Please wait.

1

1 Governmental Accounting Standards Update Frank Crawford, CPA www.crawfordcpas.comfrank@crawfordcpas.com

2

2 Recently Issued or Effective GASB Pronouncements

3

3 New Pronouncements—2004 Statement No. 43, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans—April Statement No. 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pension Plans—June

4

4 New Pronouncements—2006 Statement No. 49, Accounting and Financial Reporting for Pollution Remediation Obligations—November

5

5 New Pronouncements—2007 Statement No.50, Pension Disclosures-—May Statement No. 51, Accounting and Financial Reporting for Intangible Assets—June Statement No. 52, Land and Other Real Estate Held as Investments by Endowments

6

6 New Pronouncements—2008 Statement No. 53, Accounting and Financial Reporting for Derivative Instruments—June Technical Bulletin No. 2008-1, Determining the Annual Required Contribution Adjustment for Postemployment Benefits

7

New Pronouncements—2009 Statement No. 54, Fund Balance and Governmental Fund Type Definitions— February Statement No. 55, Statement No. 55, The Hierarchy of Generally Accepted Accounting Principles for State and Local Governments - April Statement No. 56, Statement No. 56, Codification of Accounting and Financial Reporting Guidance Contained in the AICPA Statements on Auditing Standards – April 7

8

Effective Dates Immediate ◦ Statement 55 ◦ Statement 56 June 30, 2009 ◦ Statement 45—Phase 2 ◦ Statement 43—Phase 3 ◦ Statement 49 ◦ Statement 52 ◦ TB 2008-1 (Generally) June 30, 2010 ◦ Statement 45—Phase 3 ◦ Statement 51 ◦ Statement 53 June 30, 2011 ◦ Statement 54

June 30, 2010 ◦ Statement 45—Phase 3 ◦ Statement 51 ◦ Statement 53 June 30, 2011 ◦ Statement 54")

9

Statement 45 (for Employers) Subject: accounting and reporting by employers for their OPEB expenses and obligations Applies to all employers that provide OPEB (that is, the employer pays all or part of the cost of the benefits, including implicit rate subsidies) Requires accrual-basis accounting for expense and measurement and disclosure of funded status (UAAL)

Subject: accounting and reporting by employers for their OPEB expenses and obligations Applies to all employers that provide OPEB (that is, the employer pays all or part of the cost of the benefits, including implicit rate subsidies) Requires accrual-basis accounting for expense and measurement and disclosure of funded status (UAAL)")

10

Statement 43 (for Plans) Subject: reporting on stewardship of plan assets by A trustee or plan administrator (stand-alone plan reporting) or An employer or plan sponsor with a fiduciary responsibility for the plan assets that includes the plan as a trust or agency fund in its own financial report

Subject: reporting on stewardship of plan assets by A trustee or plan administrator (stand-alone plan reporting) or An employer or plan sponsor with a fiduciary responsibility for the plan assets that includes the plan as a trust or agency fund in its own financial report")

11

“Postemployment Benefits” As Defined in GASB Statements “Postemployment benefits”—benefits provided after separation from employment as part of the total compensation for services, including: ◦ Pension benefits— Retirement income Other benefits (except postemployment healthcare) if provided through a defined benefit pension plan ◦ Other postemployment benefits (OPEB)— Postemployment healthcare benefits Other forms (for example, life insurance) if provided separately from a defined benefit pension plan

if provided through a defined benefit pension plan ◦ Other postemployment benefits (OPEB)— Postemployment healthcare benefits Other forms (for example, life insurance) if provided separately from a defined benefit pension plan")

12

OPEB “Plan”— Predominant Meanings in Statements 45 and 43 In Statement 45 (employer reporting): ◦ “Plan” usually refers to an employer’s substantive commitment or agreement to provide OPEB—including, for example, provisions or understandings regarding plan membership, eligibility for benefits, types of benefits, points at which benefits will begin and end, and method of financing benefits In Statement 43 (plan reporting): ◦ “Plan” usually refers to a trust or agency fund used to administer the financing of OPEB and the payment of benefits (that is, to assets under the stewardship of an administering entity)—regardless of the financing policy adopted

: ◦ Plan usually refers to an employer’s substantive commitment or agreement to provide OPEB—including, for example, provisions or understandings regarding plan membership, eligibility for benefits, types of benefits, points at which benefits will begin and end, and method of financing benefits In Statement 43 (plan reporting): ◦ Plan usually refers to a trust or agency fund used to administer the financing of OPEB and the payment of benefits (that is, to assets under the stewardship of an administering entity)—regardless of the financing policy adopted")

13

The Substantive Plan Benefits should be projected based on the current substantive plan (the plan as understood by the employer and plan members), including changes made and communicated to plan members, at the time of the actuarial valuation and (or including) the historical pattern of sharing of costs between employer and plan members to that point ◦ Anticipated future changes in plan design should not be included in the projection of benefits A legal or contractual benefit cap (as distinguished from a cap on contributions), should be considered in the projection of benefits if the cap is deemed effective

, including changes made and communicated to plan members, at the time of the actuarial valuation and (or including) the historical pattern of sharing of costs between employer and plan members to that point ◦ Anticipated future changes in plan design should not be included in the projection of benefits A legal or contractual benefit cap (as distinguished from a cap on contributions), should be considered in the projection of benefits if the cap is deemed effective")

14

Postemployment Benefits: Substance of the Transaction Postemployment benefits (pensions and OPEB) are part of the compensation for services rendered by employees; they are part of an exchange transaction between employer and employees Benefits are “earned,” and obligations accrue or accumulate, during employment, but benefits are not taken until after employment (potentially long time lag between incurring and paying the obligation) The (accrual-basis) cost of benefits for a period is part of the total cost of government services for that period, whether or not the employer chooses to fund it concurrently

are part of the compensation for services rendered by employees; they are part of an exchange transaction between employer and employees Benefits are earned, and obligations accrue or accumulate, during employment, but benefits are not taken until after employment (potentially long time lag between incurring and paying the obligation) The (accrual-basis) cost of benefits for a period is part of the total cost of government services for that period, whether or not the employer chooses to fund it concurrently")

15

GASB 25/27 Measurement Approach Harmonizes accounting requirements with funding concepts and methods to the maximum extent appropriate for accrual accounting purposes Although OPEB plans generally are not funded, this approach still is “funding friendly” for OPEB, because an employer that chooses to fund (now or later) need not use different measures for accounting and funding purposes Statement 45 does not include any requirement with respect to an employer’s method of financing or budgeting of OPEB; for example, it does not require that an employer fund the benefits using the actuarial methods required for accounting purposes

need not use different measures for accounting and funding purposes Statement 45 does not include any requirement with respect to an employer’s method of financing or budgeting of OPEB; for example, it does not require that an employer fund the benefits using the actuarial methods required for accounting purposes")

16

Statement 45: measurement and recognition

17

Broad measurement steps Project cash outflows for benefits Discount projected benefits to present value (PV) Allocate the PV of projected benefits to periods using an acceptable actuarial cost method

Allocate the PV of projected benefits to periods using an acceptable actuarial cost method")

18

40 25 62 80 Age when hired Present age Assumed age at retirement Life Expectancy Service Period Measurement approach illustrated Employee Age Timeline

19

40 Measurement approach illustrated 2562 80 1) Project Benefits 2) Discount Actuarial Present Value 3) Actuarial cost method $4,500$15,000 $14,000...

Project Benefits 2) Discount Actuarial Present Value 3) Actuarial cost method $4,500$15,000 $14,000...")

20

Disclosure of Funded Status and Funding Progress Employers also will be required to disclose the funded status of the benefits as of the most recent valuation and to present as RSI multi-year trend information about funding progress, including the following information: ◦ Actuarial accrued liability (AAL) ◦ Actuarial value of plan assets ◦ Unfunded actuarial accrued liability (UAAL) (AAL minus plan assets) ◦ Funded ratio (actuarial value of plan assets/AAL) ◦ Ratio of UAAL to covered payroll ◦ Notes to RSI regarding changes affecting the interpretation of trends in the amounts reported

◦ Actuarial value of plan assets ◦ Unfunded actuarial accrued liability (UAAL) (AAL minus plan assets) ◦ Funded ratio (actuarial value of plan assets/AAL) ◦ Ratio of UAAL to covered payroll ◦ Notes to RSI regarding changes affecting the interpretation of trends in the amounts reported")

21

Implicit Rate Subsidies An employer’s commitment to permit retirees to participate in the same group as active employees by paying the blended premium involves a real cost to the employer ◦ For example, if claims costs are $6,000 per retiree, and the retiree pays a blended premium of $3,600, the employer generally pays the difference, or $2,400 per retiree The preceding is a function of the significant effect of age on claims costs (that is, claims costs for retirees in a combined group generally will be significantly higher than claims costs for active employees in the group)

")

22

Implicit Rate Subsidies The “implicit” subsidy is no less “real” than an explicit contribution; it is a hard cash outlay (only obscured by the averaging) ◦ For example, if the preceding employer nominally pays the $3,600 blended premium for each active employee, but the cost of coverage (claims costs) for an active employee is only $2,800, the excess of $800 per active employee has nothing to do with providing coverage for active employees; it is a cash contribution by the employer toward the higher cost of coverage for retirees

◦ For example, if the preceding employer nominally pays the $3,600 blended premium for each active employee, but the cost of coverage (claims costs) for an active employee is only $2,800, the excess of $800 per active employee has nothing to do with providing coverage for active employees; it is a cash contribution by the employer toward the higher cost of coverage for retirees")

23

Illustration of Funded Status Information Govt. A Govt. B Unfunded Partially (PAYG) Funded Actuarial accrued liabilities (AAL) (a) $13,500,000 $13,500,000 Actuarial value of plan assets (b) -0-- 9,000,000 Unfunded actuarial accrued liabilities (UAAL) (a-b) 13,500,000 4,500,000 Funded ratio (b/a) 0.0% 66.7% Covered payroll (c) $7,600,000 $7,600,000 UAAL as a % of covered payroll (a-b/c) 177.6% 59.2%

Funded Actuarial accrued liabilities (AAL) (a) $13,500,000 $13,500,000 Actuarial value of plan assets (b) ,000,000 Unfunded actuarial accrued liabilities (UAAL) (a-b) 13,500,000 4,500,000 Funded ratio (b/a) 0.0% 66.7% Covered payroll (c) $7,600,000 $7,600,000 UAAL as a % of covered payroll (a-b/c) 177.6% 59.2%.")

24

Effective Dates Staggered implementation based on a government’s phase for implementing GASB 34 Statement 45 will be effective for the employer’s fiscal year beginning after December 15, 2006 (Phase 1), 2007 (Phase 2), or 2008 (Phase 3) Statement 43 will be effective for the plan’s fiscal year beginning after December 15, 2005 (if largest employer is Phase 1), 2006 (if largest is Phase 2), or 2007 (if largest is Phase 3) Earlier implementation is encouraged

, 2007 (Phase 2), or 2008 (Phase 3) Statement 43 will be effective for the plan’s fiscal year beginning after December 15, 2005 (if largest employer is Phase 1), 2006 (if largest is Phase 2), or 2007 (if largest is Phase 3) Earlier implementation is encouraged")

25

25 Statement 49 — Accounting and Financial Reporting for Pollution Remediation Obligations

26

26 Scope Pollution REMEDIATION Obligations ◦ Excludes prevention or control obligations ◦ Excludes asset retirement obligations—including landfills (Statement 18) ◦ Excludes fines, penalties, toxic torts, product or process safety outlays (NCGA Statement 4)

◦ Excludes fines, penalties, toxic torts, product or process safety outlays (NCGA Statement 4)")

27

27 Obligating Events a. Compelled to take remediation action because of pollution-caused imminent endangerment b. Violate pollution-prevention permit—for example, RCRA permit c. Named, or evidence indicates govt. will be named, as responsible party or PRP for remediation (or cost sharing)

.")

28

28 Obligating Events (continued) d. Named, or evidence indicates govt. will be named, in lawsuit to participate in remediation Excludes lawsuits having no merit e. Govt. commences, or legally obligates self to commence Limited to portion legally required to complete

29

29 Recognition Component approach ◦ Recognize components of liability as they become reasonably estimable ◦ Recognition benchmarks Cost accumulation, not fair value Current value, not present value Expected cash flow technique

30

30 Two Contingencies—FAS 5 Recognition Potential Payment Probability (a) x (b) $060%$0 $20040%$80 $80 Potential Payment Probability (a) x (b) $060%$0 $20040%$80 $80

x (b) $060%$0 $20040%$80 $80 Potential Payment Probability (a) x (b) $060%$0 $20040%$80 $80")

31

31 Two Contingencies—FAS 5 Recognition Potential Payment Probability (a) x (b) $060%$0 $20040%$80 $80 Potential Payment Probability (a) x (b) $060%$0 $20040%$80 $80 $1 Now it’s 100% probable. But how much do you record?

32

32 Which Outlays? All direct outlays attributable to remediation ◦ All outlays—not just incremental costs ◦ Consistent with Statement 18 ◦ Includes payroll, pension, and OPEB May include indirect outlays ◦ General overhead ◦ A matter of professional judgment

33

33 Capitalization Criteria: a. Cleanup to prepare property for sale (limited to fair value) b. Polluted property bought and cleaned for use (limited) c. Asset impaired and cleanup restores lost service utility (limited) d. Acquire PP&E that have future alternative use, e.g., land (limited to future service utility) For a. & b.—capitalize only if incurred within reasonable period

c. Asset impaired and cleanup restores lost service utility (limited) d. Acquire PP&E that have future alternative use, e.g., land (limited to future service utility) For a. & b.—capitalize only if incurred within reasonable period.")

34

34 Expected Recoveries from PRPs and Insurance Reduce expense (and expenditure, if available) and... If not realized or realizable— ◦ Net against remediation liabilities When realized or realizable ◦ Accrete liability and report separate recovery assets (cash or receivable)

.")

35

35 Recoveries example Expected outlays $10,000 Expected recoveries 3,000 Net remediation expense $7,000 If recovery not realized or realizable: Pollution remediation liability = $7,000 Pollution remediation liability = $7,000 If recovery realized or realizable: Recovery asset (receivable) = $3,000 Recovery asset (receivable) = $3,000 Pollution remediation liability = $10,000 Pollution remediation liability = $10,000

= $3,000 Recovery asset (receivable) = $3,000 Pollution remediation liability = $10,000 Pollution remediation liability = $10,000")

36

36 Financial Reporting Display Government-wide ◦ Program cost, or ◦ Special item, or ◦ Extraordinary item ◦ No separate display of liability required Governmental funds ◦ Expenditures recognized when liquidated with expendable available resources ◦ No pollution liability, only payables for goods and services used

37

37 Effective Date & Transition Period beginning after December 15, 2007 Measure liabilities at beginning of that period so beginning net assets can be restated Apply retroactively if you have sufficient objective verifiable information to apply to prior periods Early application encouraged

38

38 GASB Statement No. 50 Pension Disclosures An amendment of GASB Statements No. 25 and No. 27

39

39 Pension Disclosures Goal is to conform the pension disclosures with the OPEB disclosures Notes to financial statements would disclose the funded status of the plan as of the most recent actuarial valuation date. ◦ Defined benefit pension plans also would disclose actuarial methods and significant assumptions used in the most recent actuarial valuation in notes to financial statements instead of in notes to RSI.

40

40 Effective Date Generally effective for periods beginning after June 15, 2007

41

41 GASB Statement No. 51 Accounting and Financial Reporting for Intangible Assets

42

42 Background Paragraph 19 of GASB Statement 34 ◦ Capital assets include, “land, improvements to land, easements, buildings, building improvements, vehicles, machinery, equipment, works of art and historical treasures, infrastructure, and all other tangible or intangible assets that are used in operations and that have initial useful lives that extend beyond a single reporting period” (emphasis added).

.")

43

43 Overarching Question What are the “intangible assets that are used in operations” that are mentioned in Statement 34, paragraph 19? ◦ APB Opinion 17, Intangible Assets Issued in 1970 and had been authoritative guidance for governments prior to Statement 34 Did not define intangible assets, but listed them Patents Trademarks Copyrights

44

44 Description An intangible asset is an asset that possesses all of the following characteristics: ◦ Lack of physical substance ◦ Lack of physical substance ◦ Nonfinancial nature ◦ Initial useful life extending beyond a single reporting period

45

45 Lack of Physical Substance Intangible assets usually result from legal or contractual rights and clearly have no physical substance. ◦ Trademarks, copyrights, royalty interests What about intangible assets closely related to tangible assets? ◦ Right-of-way easement for a road ◦ Water rights

46

46 Right-of-Way Easement A right-of-way easement for a road depends on a tangible asset—land—to enable a government to provide transportation services. What is the asset? ◦ The asset is not the land or the road. ◦ The asset is the right-of-way easement (a right to use the land for a specific purpose). It is a contractual right that does not have physical substance.

. It is a contractual right that does not have physical substance..")

47

47 Lack of Physical Substance Accounts receivables and investment securities do not have physical substance. Are they intangible assets?

48

48 Nonfinancial in Nature Second characteristic of intangible assets is that they are nonfinancial in nature. ◦ Must not be in monetary form Like cash and investment securities ◦ Must be neither a claim nor a right to assets in monetary form Like receivables

49

49 Initial Useful Life Extending Beyond a Single Reporting Period All capital assets, not just intangible assets, must have an useful life that extends beyond one reporting period. IF NOT, expense when incurred.

50

50 Common Types of Intangible Assets Right-of-way easements Other types of easements Patents, copyrights, trademarks Land use rights Water rights Licenses and permits Computer software ◦ Purchased or licensed ◦ Internally generated

51

51 Scope Exceptions Intangible assets acquired or created primarily for directly obtaining income or profit ◦ Copyrights on books or recordings given to a university so they can earn royalties Capital leases Goodwill from a combination transaction

52

52 Basic Reporting Guidance All existing authoritative guidance related to capital assets should be applied to these intangible assets ◦ Purchased intangible assets recognized at historical purchase price ◦ Donated intangible assets recognized at fair value when acquired

53

53 Basic Reporting Guidance All intangible assets subject to Statement should be classified as part of capital assets in government-wide, proprietary fund, and fiduciary fund statement of net assets. ◦ Because intangible assets are considered capital assets, they are reported as expenditures (not assets) in governmental fund financial statements.

in governmental fund financial statements..")

54

54 Basic Reporting Guidance Capital assets (including intangibles) that are being depreciated or amortized are reported separately from capital assets that are not being depreciated or amortized.

that are being depreciated or amortized are reported separately from capital assets that are not being depreciated or amortized.")

55

55 Amortization Allocation of the cost of intangible assets over their estimated useful lives. Existing guidance for depreciation of capital assets generally applies to amortizing intangible assets. ◦ Amortization expense reported for intangible assets with finite useful lives. Amortization period for contractual or legal rights limited to period of expected service capacity.

56

56 Amortization Example Town has a right to use water from a lake for 20 years. What is the amortization period? Same scenario, but town for a nominal amount has the right to renew the water rights for an additional 10 years. Amortization period?

57

57 Amortization Example Town has a right to use water from a lake for 20 years. What is the amortization period? ◦ 20 years Same scenario, but town for a nominal amount has the right to renew the water rights for an additional 10 years. Amortization period? ◦ 30 years—assuming evidence exists town would seek renewal

58

58 Amortization No amortization for intangible assets with indefinite useful lives ◦ No factors (legal, contractual, technological, or otherwise) currently exist that limit the useful life of the asset How will a right-of-way easement for land under a road normally be reported? ◦ Part of capital assets not being depreciated or amortized

59

59 Internally Generated Internally generated intangible assets (IGIA) are assets that are: ◦ Created or produced by the government or an entity contracted by the government; or ◦ Acquired from a third party but require more than minimal incremental effort to achieve expected service capacity Examples ◦ Computer software ◦ Patents ◦ Copyrights ◦ Trademarks

are assets that are: ◦ Created or produced by the government or an entity contracted by the government; or ◦ Acquired from a third party but require more than minimal incremental effort to achieve expected service capacity Examples ◦ Computer software ◦ Patents ◦ Copyrights ◦ Trademarks")

60

60 Internally Generated Statement provides a specified-conditions approach to recognizing outlays associated with IGIA Outlays incurred related to an IGIA that is considered identifiable should be capitalized only upon the occurrence of all three criteria on following slide.

61

61 Internally Generated Three capitalization criteria ◦ Determination of the specific objective of the project and the nature of the service capacity that is expected to be provided by the asset upon completion of the project; ◦ Demonstration of the technical or technological feasibility for completing the project so that the asset will provide its expected service capacity; ◦ Demonstration of the current intention, ability, and presence of effort to complete or, in the case of a multiyear project, continue development of the intangible asset Outlays incurred prior to meeting criteria should be expensed as incurred

62

62 Internally Generated Computer Software Specific guidance on applying the specified- conditions approach for recognition of internally generated computer software is provided Internally generated computer software includes software developed: ◦ By government’s own employees ◦ By third party on behalf of government ◦ Commercially but requiring more than minimal incremental effort to put into operations

63

63 Internally Generated Computer Software Guidance generally based on development stages similar to AICPA SOP 98-1 Three stages ◦ Preliminary project stage Needs and alternatives for software developed ◦ Application development stage Design, software configuration and interfacing, coding, and testing ◦ Post-implementation/operation stage Training and software maintenance

64

64 Internally Generated Computer Software Outlays associated with preliminary project and post-implementation/ operation stages should be expensed as incurred. Outlays associated with application development stage should be capitalized if: ◦ Preliminary project stage complete, and ◦ Management implicitly or explicitly authorizes and commits to funding.

65

65 Impairment of Internally Generated Intangible Assets Stoppage during development ◦ Stopping development of computer software Impaired intangible assets reported at lower of carrying value or fair value in statement of net assets.

66

66 Effective Date and Transition Effective date is fiscal periods beginning after June 15, 2009 Provisions generally should be retroactively applied

67

67 Effective Date and Transition Exceptions for retroactively reporting intangible assets: ◦ Permitted but not required for IGIA and intangible assets with indefinite useful lives at transition Right-of-way easements for land under roads not required to be retroactively reported. ◦ Required for all other intangible assets acquired in fiscal years ending after June 30, 1980 by phase 1 or 2 governments ◦ Encouraged but not required for all other intangible assets of phase 3 governments

68

68 GASB Statement No. 52 Land and Other Real Estate Held as Investments by Endowments

69

69 Purpose Establish financial reporting standards for land and other real estate held as investments by endowments Endowments include: ◦ Permanent and term endowments Principal generally maintained in perpetuity or for a stated period of time or until the occurrence of an event ◦ Permanent funds

70

70 Financial Reporting Reported at fair value in statement of net assets Changes in fair value reported as investment income Make applicable Statement 31, paragraph 15 disclosures ◦ Method to estimate fair value if not market prices

71

71 Effective Date For periods beginning after June 15, 2008

72

72 GASB Statement No. 53 Accounting and Financial Reporting for Derivative Instruments Issued June 2008

73

73 Examples of Derivatives Interest rate swap ◦ Variable-rate to fixed-rate ◦ Fixed-rate to variable-rate Basis swap ◦ Exchange payments based on the changes of two variable rates Swaption ◦ Gives the purchaser of the option the right, but not the obligation, to enter into an interest rate swap Commodity swap ◦ Reduce exposure to a commodity’s price risk

74

74 Principle Fair value with hedge accounting ◦ Changes in fair value of derivative are deferred for qualifying transactions ◦ Changes in fair value of derivative would not be deferred if The related asset (for example, investment) is reported at fair value The hedge does not meet the effective criteria How is that operationalized?

is reported at fair value The hedge does not meet the effective criteria How is that operationalized")

75

75 Hedge Effectiveness Consistent critical terms Quantitative techniques ◦ Synthetic instrument ◦ Dollar offset ◦ Regression ◦ Other qualifying quantitative methods

76

76 Effective Date and Transition Effective for financial periods beginning after June 15, 2009 Implementation guide approved by the Board at the January 2009 meeting

77

GASB Technical Bulletin No. 2008-1 Determining the Annual Required Contribution Adjustment for Postemployment Benefits 77

78

ARC Adjustment TB clarifies that actual amount of interest (and principal, if any) may be used to make ARC adjustment. ◦ That is, actual amounts may replace the estimate of ARC adjustment that comes from method described in: Statement 27, paragraph 13 Statement 45, paragraph 16 78

79

79 Effective Date For periods ending after December 15, 2008 (or for OPEB at least simultaneously with implementation of Statement 45)

")

80

80 GASB Statement No. 54 Fund Balance Reporting and Governmental Fund Type Definitions Issued February 2009

81

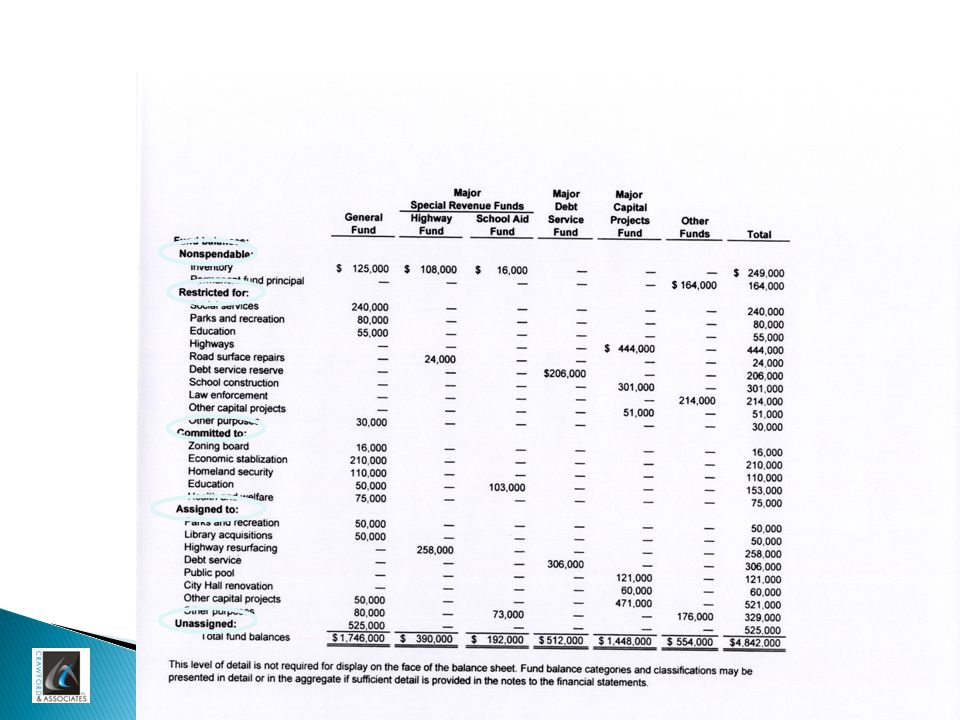

Fund Balance Components Nonspendable fund balance Restricted fund balance Committed fund balance Assigned fund balance Unassigned fund balance 81 Spendable

82

82 Fund Balance Components Nonspendable Fund Balance includes amounts that cannot be spent because they are either: (a) not in spendable form or (a) not in spendable form or ◦ Inventories, prepaids, long-term loans (b) legally or contractually required to be (b) legally or contractually required to be maintained intact. maintained intact. ◦ Principal of a permanent fund

83

83 Fund Balance Components Restricted Fund Balance: Amounts that are restricted to specific purposes, pursuant to the definition of restricted in paragraph 34 of Statement 34, as amended by Statement No. 46. ◦ External parties ◦ Constitution ◦ Enabling legislation

84

84 Fund Balance Components Committed Fund Balance: Amounts that are committed for specific purposes by formal action of the government’s highest level of decision-making authority.

85

85 Fund Balance Components Assigned Fund Balance: Amounts that are intended by the government to be used for specific purposes, but are neither restricted nor committed. ◦ All amounts in other governmental funds not restricted or committed. ◦ Amounts in general fund intended for specific use

86

86 Fund Balance Components Unassigned Fund Balance: Residual classification for the general fund ◦ Has not been assigned to other funds and is not restricted, committed, or assigned to specific purposes within the general fund. ◦ Residuals for expired purposes in other funds

89

Stabilization Arrangements Refers to economic stabilization, revenue stabilization, budgetary stabilization, and other similar intended “rainy day” funds. ◦ Authority to set aside Statute Ordinance Resolution Charter Constitution 89

90

Stabilization Arrangements General Fund ◦ Restricted or committed, if meet criteria ◦ Unassigned, if do not meet criteria Special Revenue Fund ◦ Only if resources derive from a specific restricted or committed revenue source 90

91

Note Disclosures Committed Fund Balance ◦ Government’s highest level of decision-making authority ◦ Formal action required to be taken to establish, modify, or rescind a fund balance commitment Assigned Fund Balance ◦ Body or official authorized to assign ◦ Governmental policy 91

92

Note Disclosures Disclose significant encumbrances by major funds and nonmajor funds in aggregate Nonspendable fund balance (if not separated on face) ◦ Amount not in spendable form ◦ Amount legally or contractually required to be maintained intact 92

◦ Amount not in spendable form ◦ Amount legally or contractually required to be maintained intact 92")

93

Note Disclosures Restricted, committed, or assigned fund balance ◦ If displayed in aggregate on face Disclose major restricted resources Disclose major commitments Disclose major assignments 93

94

Note Disclosures Stabilization arrangements ◦ Authority for establishing By statute or ordinance? ◦ Requirements for adding to stabilization amounts ◦ Conditions for spending amounts ◦ Stabilization balance, if not apparent on face 94

95

Note Disclosures Minimum fund balance policy ◦ May have in lieu of stabilization amounts ◦ Describe policy for determining minimum amount 95

96

Governmental Fund Type Definitions General fund ◦ Used to account for all financial resources not accounted for in another fund Capital projects funds ◦ Used to account for financial resources that are restricted, committed, or assigned to expenditure for capital outlays Unless financed by proprietary funds or assets to be held in trust for those outside government 96

97

Governmental Fund Type Definitions Debt service funds ◦ Used to account for financial resources that are restricted, committed, or assigned to expenditure for principal and interest Permanent funds ◦ Used to account for resources restricted with respect to “earnings” for support of government’s own programs 97

98

Governmental Fund Type Definitions Special revenue funds ◦ Account for proceeds of specific revenue sources that are restricted or committed to expenditure for specified purposes other than debt service or capital projects Not used for resources held in trust for those outside government. 98

99

Special Revenue Funds Restricted or committed resources should be “substantial” portion of inflows reported in fund. Restricted or committed resources should be “substantial” portion of inflows reported in fund. ◦ If not, should be reported in general fund. Investment earnings and transfers in may be reported if restricted, committed, or assigned to specified purpose of fund. 99

100

Effective Date and Transition For FYE June 30, 2011 and thereafter For fund balance reclassifications ◦ Restate fund balance for all prior periods presented ◦ Changes to fund balance information in statistical section may be applied prospectively 100

101

101 Other GASB Projects Current Projects ◦ Postemployment Benefits Accounting and Reporting ITC—Comment deadline is July 31, 2009 ◦ Public and Private Partnerships ◦ Reporting Units/Statement 14 Revisited ◦ Recognition and Measurement Attributes (Concepts Statement) ◦ Service Efforts and Accomplishments— Suggested Reporting Guidelines for Voluntary Reporting

◦ Service Efforts and Accomplishments— Suggested Reporting Guidelines for Voluntary Reporting")

102

Other GASB Projects Practice Issues ◦ Chapter 9 Bankruptcies ◦ Codification of AICPA Accounting Guidance included in Statements of Auditing Standards ◦ Comprehensive Implementation Guide ◦ Financial Instruments Omnibus ◦ GAAP Heirarchy 102

103

103 Other GASB Projects Research Agenda ◦ Chapter 9 Bankruptcy ◦ Economic Condition Reporting ◦ Electronic Financial Reporting ◦ FASB Pronouncements (pre-1989) ◦ Fair Value Measurement ◦ Investment Omnibus

◦ Fair Value Measurement ◦ Investment Omnibus")

104

104 GASB Resources

105

105 GASB Website—www.gasb.org Downloads and ordering information (Exposure documents, Statements, Q&As) Summaries of standards Project pages Technical inquiry form Staff contacts

Summaries of standards Project pages Technical inquiry form Staff contacts")

106

106 Questions?

Similar presentations

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or.>")

Presentation by Gregory S. Allison, CPA UNC School of Government.>")