Download presentation

Presentation is loading. Please wait.

1

Natural Gas: An Overview

2

Ready Reckoner 4 MMSCMD (or 1 MMTPA LNG) is required to feed a 1000 MW modern power station for 1 year Crude oil at $100 per barrel is equivalent to $ 17 per MMBtu

is required to feed a 1000 MW modern power station for 1 year Crude oil at $100 per barrel is equivalent to $ 17 per MMBtu")

3

Gas supply scenario till 2011-12 (MMSCMD) Present*By 2011-12 ONGC60.851.0 OIL6.4 JVC/PVT.21.297.0 (RIL: 80) LNG28.652.0 Pipeline imports -- Total117.0200.0 * Provisional

Present*By ONGC OIL6.4 JVC/PVT (RIL: 80) LNG Pipeline imports -- Total * Provisional")

4

Gas Reserves 2007 BCM Onshore 270 Offshore 785 (incl. RIL KG Basin) TOTAL1055 (R/P ratio: 33 years) Major reserves claimed in KG Basin TCFBCMDGH approved so far RIL11.30400 GSPC 5.60200 56 ONGC 6.37220 70 Issues in establishing more reserves and development of fields/ infrastructure: Paucity of rigs, high hire charge for rigs, capital intensive.

TOTAL1055 (R/P ratio: 33 years) Major reserves claimed in KG Basin TCFBCMDGH approved so far RIL GSPC ONGC Issues in establishing more reserves and development of fields/ infrastructure: Paucity of rigs, high hire charge for rigs, capital intensive..")

5

Gas demand scenario till 2011-12 (MMSCMD) * Present consumption Short supply Fuel conversion/ stranded/ closed assets Greenfield projects Power33.030.010.062.0 Fertilizer27.09.024.016.0 Industry9.0N.A Captive/LPG15.09.0-16.0 Petrochemicals4.0 Transport/domestic3.0--21.0 Sponge iron units6.022.0N.A Misc.6.0 Total103.070.034.0115.0 Cumulative103.0173.0207.0322.0 Supply by 2012200.0 *Provisional

* Present consumption Short supply Fuel conversion/ stranded/ closed assets Greenfield projects Power Fertilizer Industry9.0N.A Captive/LPG Petrochemicals4.0 Transport/domestic Sponge iron units N.A Misc.6.0 Total Cumulative Supply by *Provisional")

6

Gas Demand scenario till 2024-32 (MMSCMD) 2024-252031-32 EIA 2004 Ref case High case Low case 195 225 155 IEA 2004259 IHV 2000391 PWC – BAU – HOG 488 738 IEP 2006 – Low – High 342 672 Current demand (met + unsatisfied): 207

EIA 2004 Ref case High case Low case IEA IHV PWC – BAU – HOG IEP 2006 – Low – High Current demand (met + unsatisfied): 207")

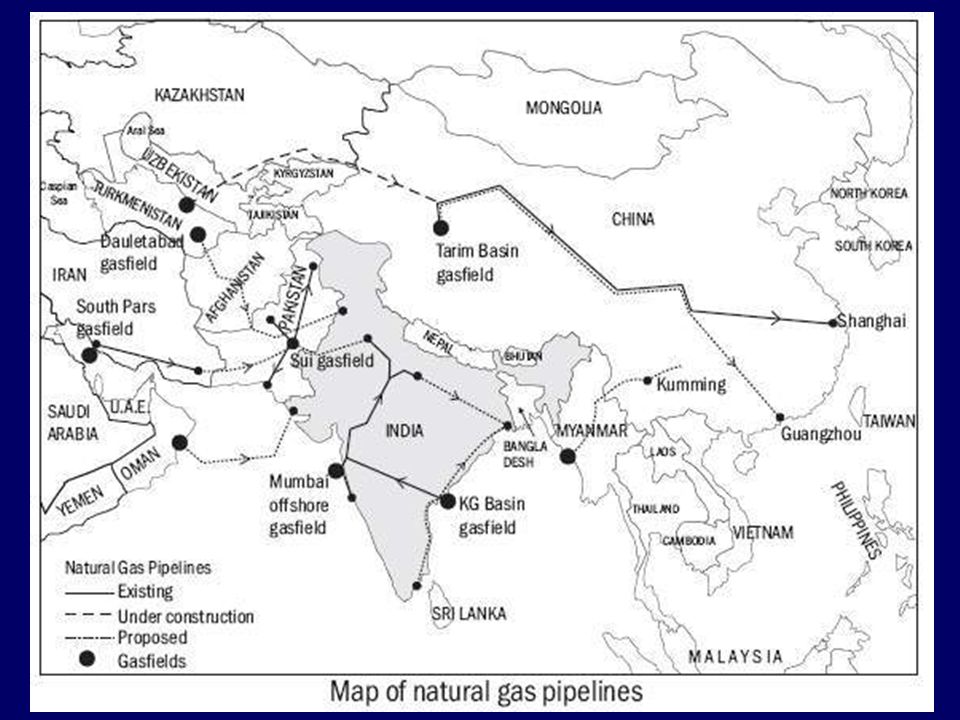

8

Transnational gas pipelines Issues: Gas reserves certification, field development, well-head price, construction/ ownership of pipeline, security, transportation & transit fees etc. Quantity MMSCMDPrice Myanmar-India 16Awarded to China. $4.279 per MMBtu well-head price + transit fee + 2,380 km pipeline by China Iran-Pakistan-India (IPI) Pakistan: 30 India: 30 60 $5.0 per MMBtu (2004, crude $60 per brl) at Indo-Pak border & tpt/ transit fees to Pakistan. Turkmenistan- Afghanistan- Pakistan-India (TAPI) Afghanistan: 14 Pakistan: 38 India: 38 90 $12.30 per MMBtu? Oman-India sub-sea pipeline 63Well-head price? Pipeline tariff $1.30 per MMBtu

Pakistan: 30 India: $5.0 per MMBtu (2004, crude $60 per brl) at Indo-Pak border & tpt/ transit fees to Pakistan. Turkmenistan- Afghanistan- Pakistan-India (TAPI) Afghanistan: 14 Pakistan: 38 India: $12.30 per MMBtu. Oman-India sub-sea pipeline 63Well-head price. Pipeline tariff $1.30 per MMBtu.")

9

LNG terminals LocationCompanyCapacity (MMTPA) Comments DahejPetronet LNG6.5 (12.5 by 2010/11) Rasgas contracts HaziraShell/TOTAL2.5Spot LNG purchases. Merchant sales DhabolRatnagiri Gas Power Projects Ltd. 5.0Breakwater by 2011? Steep cost escalation. LNG terminal to be hived off? Spot purchases. KochiPetronet LNG2.5Negotiations with Exxon, Australia. Commissioning 2012/13. Total16.5 to 22.5

10

Natural gas prices at wellhead/landfall pt/fob $ / MMBtu APM priority customers2.10 (Rs.3200 per TCM) Other APM customers2.45 Pre-NELP/NELP (PSCs)3.50 to 5.75 Reliance KG Basin4.20 (5 years) Petronet LNG 5.0 MMTPA Addl.1.5 MMTPA Addl. 2.5 MMTPA 2.53 fob till 12/08 JCC adjusted from 1/09 Contract from 7/07 till 9/09. Price 8.50 fob till 12/08 JCC adjusted from 9/09 Spot LNG purchases: Petronet/ Shell etc. 20.00 to 25.00 fob GAIL pipeline tariff0.75

11

The Petroleum & Natural Gas Regulatory Board Bill 2005 Key Functions of the Board relating to Natural Gas Marketing Register entities to market gas, subject to contractual obligations of GoI LNG terminals Register entities to establish and operate Common or contract carrier pipelines Authorized entities to lay, build, operate Declare as Common or Contract carrier Regulate access and set terms for determining tariff City or local gas distribution networks Authorize entities to lay, build, operate Regulate access and set terms for determining tariff Monitor prices Technical standards & specifications (incl. Safety) Lay down above, including pipeline access code Key powers of Central Government May issue policy directives to the Board Final say on whether a question is one of policy or not

Lay down above, including pipeline access code Key powers of Central Government May issue policy directives to the Board Final say on whether a question is one of policy or not.")

12

Gas Utilization Policy of GoI 2008 Priority allocation Existing plants (incl. Stranded/ closed/ Fuel conversion) Greenfield projects Fertilizer17 LPG/ Petrochemicals28 Power311 City gas49 Refineries510 Industry (sponge iron/ ceramics etc.) 6?

Greenfield projects Fertilizer17 LPG/ Petrochemicals28 Power311 City gas49 Refineries510 Industry (sponge iron/ ceramics etc.) 6 .")

13

Overall comments Demand till 2012: Present consumption = unmet current demand = greenfield projects (approx. 100 MMSCMD each) Demand till 2024-32: Vary considerably. Some (foreign ones) unrealistically low. Utilization policy of GoI: Priority to existing plants. Drivers: fuel economics and the environment.. Some unanswered questions Supply: To reach 200 MMSCMD by 2012 if legal issues between RIL, RNRL & NTPC are sorted out. No gas for greenfield projects? Availability of rigs? All India gas grid: Organic growth vs. Master Plan. No plans for gas storage Transnational pipelines: Very slow progress Price/fee issues unresolved. Geo-political concerns. LNG: New supplies of LNG hard to find. Is India prepared to pay the price? Regulatory Board: Currently addressing city gas distribution issues. Work on pipelines in hand. India’s carbon footprint: Will reduce with extensive use of natural gas

Demand till : Vary considerably. Some (foreign ones) unrealistically low. Utilization policy of GoI: Priority to existing plants. Drivers: fuel economics and the environment.. Some unanswered questions Supply: To reach 200 MMSCMD by 2012 if legal issues between RIL, RNRL & NTPC are sorted out. No gas for greenfield projects. Availability of rigs. All India gas grid: Organic growth vs. Master Plan. No plans for gas storage Transnational pipelines: Very slow progress Price/fee issues unresolved. Geo-political concerns. LNG: New supplies of LNG hard to find. Is India prepared to pay the price. Regulatory Board: Currently addressing city gas distribution issues. Work on pipelines in hand. India’s carbon footprint: Will reduce with extensive use of natural gas.")

14

Thank you

Similar presentations