Download presentation

Presentation is loading. Please wait.

1

Building a Collectable Tangible Personal Property Tax Roll

Presented by: John Power, CFCA Assistant Tax Collector, Alachua Co. Florida Jon Costabile Executive Dir. of Finance, Alachua Co. Florida

2

Appraiser / Collector Relationships

Working Together Building Public Trust & Confidence

3

Presentation Objectives

Stimulate thought regarding the Appraiser / Collector relationship as it relates to the TPP Roll. Point out key characteristics necessary for effective collection of the TPP Roll. Encourage the fostering of beneficial professional relationships b/w Appraisers & Collectors. Ultimately increase the public trust and confidence in our abilities to perform our duties via a unified effort.

4

Why are you Building a TPP Roll?

For the fair and equitable levy and collection of ad-valorem taxes. “Collection” is the key component. It’s the deal maker or deal breaker. Are you building your roll with 100% collectability in mind?

5

Importance of Collectable Roll

2012 Statewide Tax Roll < 2005 Tax Roll 2012 tax roll is less than 2005 tax roll.

6

Importance of Collectable Roll Taxes Levied 2012 < 2005

2012 tax levy is less than 2005 tax roll.

7

Importance of Collectable Roll Population Growing Revenues Declining

Tax Levy Declining Population Growing. Since 2005 Population Grew 6.34% while Taxes levied declined 4.84%. On a per capita basis taxes declined 10.5% since 2005

8

Importance of Collectable Roll

Every County/Taxing Authority has reduced budgets Less Budget = Less Staffing Property Appraiser & Tax Collector Must Cooperate Uncollectable Accounts Impact Rolled-back Rate Reduces County’s ability to Raise Revenue

9

Key Mindset The roll is not “finished” once it is compiled and delivered to the collector. The party has just begun. The “finished” product is once 100% collection is achieved.

10

Key Mindset cont. Does your roll stand the test of its intended use, “Collectability”? Are your processes constantly evolving to ensure a more accurate and collectable product?

11

Voluntary Collection Compliance

After voluntary compliance is your roll worthless? How would this affect the mindset and morale of your appraisers?

12

Selling Legitimacy Your Roll / Data is a pure demonstration of your professionalism and understanding of proper appraisal methodologies Your data has a direct correlation to the taxpayers’ compliance with, and respect for, your product and legal authority It is paramount that you use well defined valuation techniques Would you be willing to put your reputation on the line based on the account data? You are.

13

Data Components Vital to Successful Enforcement

Accurate owner information including contact name and phone number AKA names / DBA names / owner and business Fed ID Number, Corporate Declarations, etc. Accurate, detailed equipment inventories – bona fide return, photographs of equipment and location of assets Real Estate parcel number cross reference Business license cross reference Digital images of return and misc. documents

14

Non-Filers What percentage of accounts file returns?

What percentage of accounts have compiled with “industry standard” or estimated equipment / values?

15

Non-Filers cont. FS (3) Failure to file a return, or to otherwise properly submit all property for taxation, shall in no regard relieve any taxpayer of any requirement to pay all taxes assessed against him or her promptly. FS (2) If no tangible personal property tax return has been filed as required by law, including any extension which may have been granted for the filing of the return, the property appraiser is authorized to estimate from the best information available the assessment of the tangible personal property of a taxpayer who has not properly and timely filed his or her tax return. Such assessment shall be deemed to be prima facie correct, may be included on the tax roll, and taxes may be extended therefore on the tax roll in the same manner as for all other taxes.

Failure to file a return, or to otherwise properly submit all property for taxation, shall in no regard relieve any taxpayer of any requirement to pay all taxes assessed against him or her promptly. FS (2) If no tangible personal property tax return has been filed as required by law, including any extension which may have been granted for the filing of the return, the property appraiser is authorized to estimate from the best information available the assessment of the tangible personal property of a taxpayer who has not properly and timely filed his or her tax return. Such assessment shall be deemed to be prima facie correct, may be included on the tax roll, and taxes may be extended therefore on the tax roll in the same manner as for all other taxes.")

16

Non-Filers cont. Taxpayers often come forward with data once enforcement action begins Do you have a process in place to openly accept this newfound account data? What is the correction process for erroneous or inaccurate account data / values? Utilize your collector as an additional field agent

17

Collection Laws/Statutes/Legal Obligations

Once voluntary payment compliance ends legal compliance/enforcement begins. What are your collector’s legal obligations to collect? Florida has in excess of 20 state statutes pertaining to the “collection” of “Delinquent” TPP taxes.

18

Collection Laws/Statutes/Legal Obligations cont.

On delinquent accounts does your collector use penalties, seizures, bank garnishments etc? Does your roll meet state law? Does your account data strengthen the case or weaken the case ? Will your data hold up in court?

19

Authority for Collection of TPP Taxes

All personal property in the state or belonging to residents of the state, if not exempt by statute, is subject to taxation. Art. 7 §9(a), Florida Constitution; § , Fla. Stat. See eg Bush v. State ex rel. Dade County, 140 Fla. 277 (Fla. 1937).

, Florida Constitution; § , Fla. Stat. See eg Bush v. State ex rel. Dade County, 140 Fla. 277 (Fla. 1937).")

20

Florida Statutes (1) All taxes imposed pursuant to the State Constitution and laws of this state shall be a first lien, superior to all other liens, on any property against which the taxes have been assessed and shall continue in full force from January 1 of the year the taxes were levied until discharged by payment or until barred under chapter 95. If the property to which the lien applies cannot be located in the county or the sale of the property is insufficient to pay all delinquent taxes, interest, fees, and costs due, a personal property tax lien applies against all other personal property of the taxpayer in the county. However, a lien against other personal property does not apply against property that has been sold and is subordinate to any valid prior or subsequent liens against such other property. An act of omission or commission on the part of a property appraiser, tax collector, board of county commissioners, clerk of the circuit court, or county comptroller, or their deputies or assistants, or newspaper in which an advertisement of sale may be published does not defeat the payment of taxes, interest, fees, and costs due and may be corrected at any time by the party responsible in the same manner as provided by law for performing acts in the first place. Amounts so corrected shall be deemed to be valid ab initio and do not affect the collection of the tax. All owners of property are held to know that taxes are due and payable annually and are responsible for ascertaining the amount of current and delinquent taxes and paying them before April 1 of the year following the year in which taxes are assessed. A sale or conveyance of real or personal property for nonpayment of taxes may not be held invalid except upon proof that: (a) The property was not subject to taxation; (b) The taxes had been paid before the sale of personal property; or (c) The real property had been redeemed before the execution and delivery of a deed based upon a certificate issued for nonpayment of taxes. Important that other personal property not listed in return may be attached but will be subordinate to other judgment liens. Makes collections much more difficult Ab initio – “from the beginning”

All taxes imposed pursuant to the State Constitution and laws of this state shall be a first lien, superior to all other liens, on any property against which the taxes have been assessed and shall continue in full force from January 1 of the year the taxes were levied until discharged by payment or until barred under chapter 95. If the property to which the lien applies cannot be located in the county or the sale of the property is insufficient to pay all delinquent taxes, interest, fees, and costs due, a personal property tax lien applies against all other personal property of the taxpayer in the county. However, a lien against other personal property does not apply against property that has been sold and is subordinate to any valid prior or subsequent liens against such other property. An act of omission or commission on the part of a property appraiser, tax collector, board of county commissioners, clerk of the circuit court, or county comptroller, or their deputies or assistants, or newspaper in which an advertisement of sale may be published does not defeat the payment of taxes, interest, fees, and costs due and may be corrected at any time by the party responsible in the same manner as provided by law for performing acts in the first place. Amounts so corrected shall be deemed to be valid ab initio and do not affect the collection of the tax. All owners of property are held to know that taxes are due and payable annually and are responsible for ascertaining the amount of current and delinquent taxes and paying them before April 1 of the year following the year in which taxes are assessed. A sale or conveyance of real or personal property for nonpayment of taxes may not be held invalid except upon proof that: (a) The property was not subject to taxation; (b) The taxes had been paid before the sale of personal property; or. (c) The real property had been redeemed before the execution and delivery of a deed based upon a certificate issued for nonpayment of taxes. Important that other personal property not listed in return may be attached but will be subordinate to other judgment liens. Makes collections much more difficult. Ab initio – from the beginning")

21

Liens Tax liens attached to TPP remain with that property and are superior to all other liens. Taxes on personal property do not create a personal obligation on the owner. Faber, Coe, & Gregg v Wright, 178 So.2d 51 (Fla. 3d DCA 1965). Thus, once there is a tax lien on personal property, it remains effective regardless of transfer of the property or the creation of other liens.

. Thus, once there is a tax lien on personal property, it remains effective regardless of transfer of the property or the creation of other liens.")

22

Liens However, even if properly established, a lien on this “other” personal property would be a general lien, not a superior lien and would be subject to the general rule governing priority interest of liens: “the first in time is the first in right.” Consequently, such liens against other personal property are subordinate to any valid prior or subsequent liens against such other property. US v City of New Britain, 347 U.S. 81, 85, 88 (1954); § (1), Fla. Stat.; Fla. Admin Code Rule 12D (1).

; § (1), Fla. Stat.; Fla. Admin Code Rule 12D (1).")

23

Obligation of Tax Collector

Florida Statutes It is the duty of the tax collector issuing a tax warrant for the collection of delinquent tangible personal property taxes to continue his or her efforts to collect such taxes for 7 years after the date of the ratification of the warrant. After the expiration of 7 years, the warrant is barred by this statute of limitation. A tax collector or his or her successor is not relieved of accountability for collection of any taxes assessed on tangible personal property until he or she has completely performed every duty devolving upon the tax collector as required by law.

24

Duty to Collect Florida Tax Collector’s authorized to contract with 3rd Party’s to collect TPP FS The tax collector has the authority and obligation to collect all taxes as shown on the tax roll by the date of delinquency or to collect delinquent taxes, interest, and costs, by sale of tax certificates on real property and by seizure and sale of personal property. In exercising their powers to contract, the tax collector may perform such duties by use of contracted services or products or by electronic means. The use of contracted services, products, or vendors does not diminish the responsibility or liability of the tax collector to perform such duties pursuant to law. The tax collector may collect the cost of contracted services and reasonable attorney’s fees and court costs in actions on proceedings to recover delinquent taxes, interest, and costs.

26

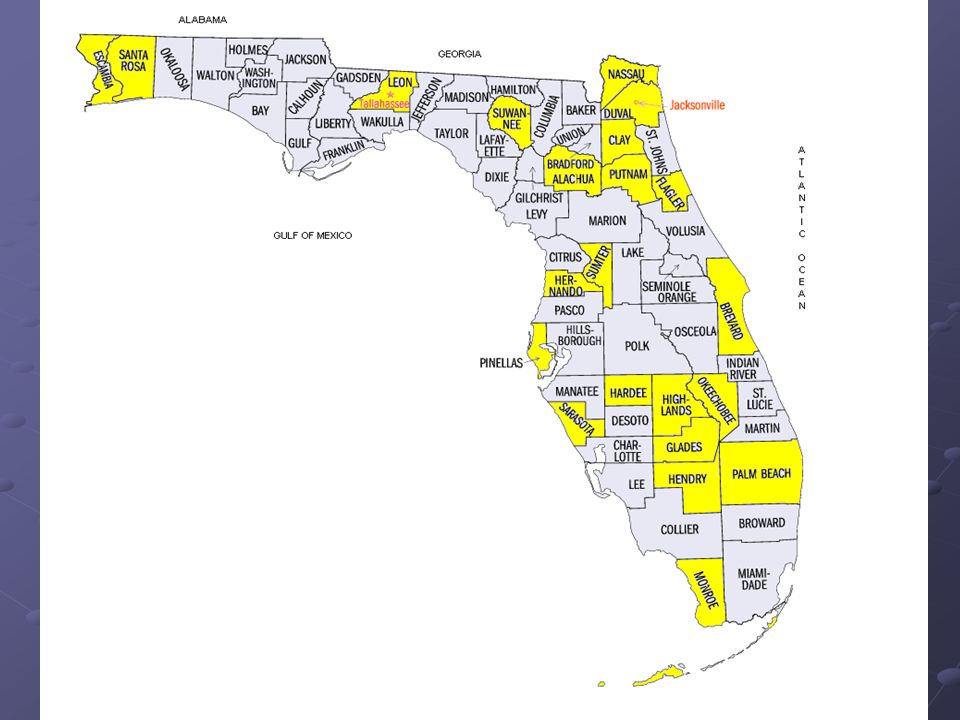

Duty to Collect Florida Tax Collector’s authorized to contract with 3rd Party to collect TPP FS Alachua, Brevard, Clay, Duval, Escambia, Flagler, Glades, Hardee, Hendry, Hernando, Highlands, Leon, Monroe, Nassau, Okeechobee, Palm Beach, Pinellas, Putnam, Santa Rosa, Sarasota, Sumter, Suwannee Property Appraiser’s are encouraged to use 3rd Party’s Field Data

27

Duty to Collect FS Delinquent personal property taxes; warrants; court order for levy and seizure of personal property; seizure; fees of tax collectors. (1) Prior to May 1 of each year immediately following the year of assessment, the tax collector shall prepare a list of the unpaid personal property taxes containing the names and addresses of the taxpayers and the property subject to the tax as the same appear on the tax roll. Prior to April 30 of the next year, the tax collector shall prepare warrants against the delinquent taxpayers providing for the levy upon, and seizure of, tangible personal property.

Prior to May 1 of each year immediately following the year of assessment, the tax collector shall prepare a list of the unpaid personal property taxes containing the names and addresses of the taxpayers and the property subject to the tax as the same appear on the tax roll. Prior to April 30 of the next year, the tax collector shall prepare warrants against the delinquent taxpayers providing for the levy upon, and seizure of, tangible personal property.")

28

Duty to Collect FS (2) Within 30 days after the date such warrants are prepared, the tax collector shall cause the filing of a petition in the circuit court for the county which the tax collector serves, which petition shall briefly describe the levies and nonpayment of taxes, the issuance of warrants, and proof of the publication of notice as provided for in s and shall list the names and addresses of the taxpayers who failed to pay taxes, as the same appear on the assessment roll.

Within 30 days after the date such warrants are prepared, the tax collector shall cause the filing of a petition in the circuit court for the county which the tax collector serves, which petition shall briefly describe the levies and nonpayment of taxes, the issuance of warrants, and proof of the publication of notice as provided for in s and shall list the names and addresses of the taxpayers who failed to pay taxes, as the same appear on the assessment roll.")

29

Duty to Collect FS (2) Such petition shall pray for an order ratifying and confirming the issuance of the warrants and directing the tax collector or his or her deputy to levy upon and seize the tangible personal property of each delinquent taxpayer to satisfy the unpaid taxes set forth in the petition. This proceeding is specifically provided to safeguard the constitutional rights of the taxpayers in relation to their tangible personal property and to allow the tax collector sufficient time to collect such delinquent personal property taxes before the filing of petitions in the circuit court and shall be conducted with these objectives in mind.

Such petition shall pray for an order ratifying and confirming the issuance of the warrants and directing the tax collector or his or her deputy to levy upon and seize the tangible personal property of each delinquent taxpayer to satisfy the unpaid taxes set forth in the petition. This proceeding is specifically provided to safeguard the constitutional rights of the taxpayers in relation to their tangible personal property and to allow the tax collector sufficient time to collect such delinquent personal property taxes before the filing of petitions in the circuit court and shall be conducted with these objectives in mind.")

30

Duty to Collect FS (6) If it appears to the circuit court that the taxes that appear on the tax roll are unpaid, the court shall issue its order directing the tax collector or his or her deputy to levy upon and seize so much of the tangible personal property of the taxpayers who are listed in the petition as is necessary to satisfy the unpaid taxes, costs, interest, attorney’s fees, and other charges.

If it appears to the circuit court that the taxes that appear on the tax roll are unpaid, the court shall issue its order directing the tax collector or his or her deputy to levy upon and seize so much of the tangible personal property of the taxpayers who are listed in the petition as is necessary to satisfy the unpaid taxes, costs, interest, attorney’s fees, and other charges.")

31

Obstruction of Justice

FS Whoever shall resist, obstruct, or oppose any officer as defined in s (1), (2), (3), (6), (7), (8), or (9); member of the parole Commission or any administrative aide or supervisor employed by the commission; county probation officer; parole and probation supervisor; personnel or representative of the Department of Law Enforcement; or other person legally authorized to execute process in the execution of legal process or in the lawful execution of any legal duty, without offering or doing violence to the person of the officer, shall be guilty of a misdemeanor of the first degree, punishable as provided in s or s

, (2), (3), (6), (7), (8), or (9); member of the parole Commission or any administrative aide or supervisor employed by the commission; county probation officer; parole and probation supervisor; personnel or representative of the Department of Law Enforcement; or other person legally authorized to execute process in the execution of legal process or in the lawful execution of any legal duty, without offering or doing violence to the person of the officer, shall be guilty of a misdemeanor of the first degree, punishable as provided in s or s")

32

What if a Business Moves?

Florida Statutes The tax collector of each county shall have the power, in the same manner and under the rules of law governing attachments of debts in other cases, to attach for taxes any tangible personal property that has been assessed at any time before payment if he or she has reason to believe that the property is being removed or disposed of so as to prevent or endanger the payment of taxes thereon. All taxes assessed upon tangible personal property shall have all the force of a judgment and execution at law against the owner of property from the date the taxes became due. If the property is still located within the county, the tax collector may issue a warrant authorizing the tax collector, the tax collector’s deputy, or the sheriff to collect the taxes or otherwise seize the property, and the tax collector, deputy, or sheriff shall proceed in the same manner as on an execution from the circuit court. If the property is located outside the county, the tax collector may issue a warrant authorizing the sheriff of the county where the property is located to collect the taxes, or otherwise seize the property in the same manner as property in the county where the property is assessed. Thereafter, the tax collector shall proceed pursuant to s

33

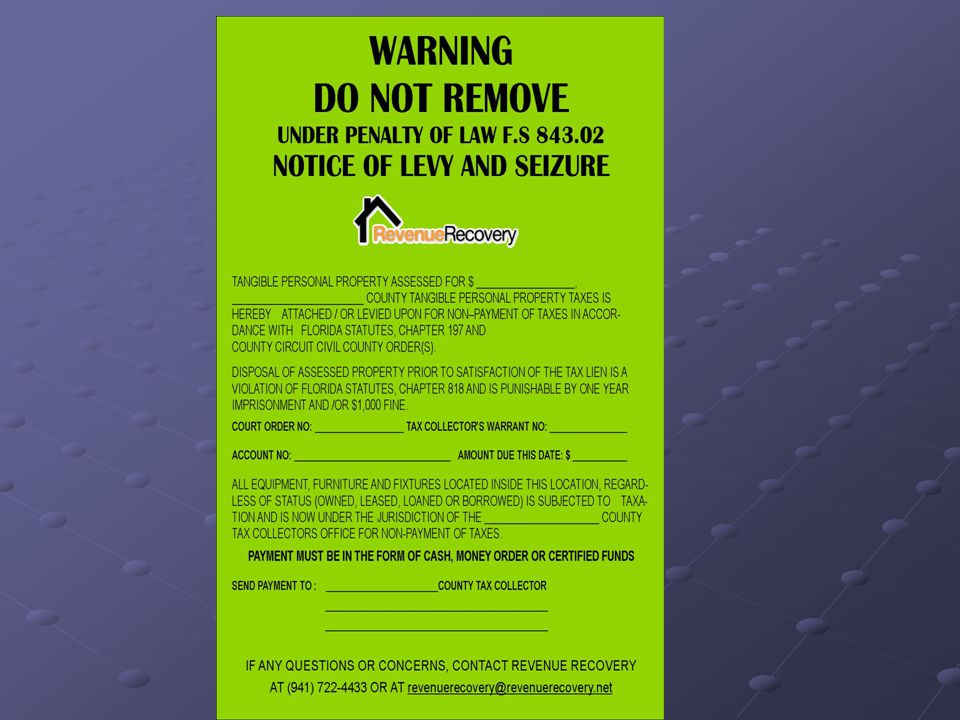

Seizures/Garnishments

Florida Statutes give tax warrants the same force as a writ of garnishment FS (8) A tax warrant issued by the tax collector for the collection of tangible personal property taxes shall, after the court has issued its order as set forth in subsection (6), have the same force as a writ of garnishment upon any person who has any goods, moneys, chattels, or effects of the delinquent taxpayer in his or her hands, possession, or control or who is indebted to such delinquent taxpayer.

A tax warrant issued by the tax collector for the collection of tangible personal property taxes shall, after the court has issued its order as set forth in subsection (6), have the same force as a writ of garnishment upon any person who has any goods, moneys, chattels, or effects of the delinquent taxpayer in his or her hands, possession, or control or who is indebted to such delinquent taxpayer.")

34

Seizures/Garnishments

Florida Statutes give tax warrants the same force as a writ of garnishment. Can your data support and defend the political repercussions of a seizure or bank garnishment?

35

Non-Filers QUESTION: How do non-filed tax returns or insufficient tax returns affect delinquent collections inclusive of seizure of equipment or garnishment of bank accounts? Ch 193 FS gives PA’s ability to assess non filers but it makes it difficult to levy garnishment without proper TIN, equipment lists, names etc..

36

Corporations FS Any Corporation of this state which has an outstanding tax warrant that has existed for more than 3 consecutive months is subject to the revocation of its charter as provided in s

37

Corporations FS – A majority of the incorporators or directors of a corporation that has not issued shares or has not commenced business may dissolve the corporation by delivering to the Department of State for filing articles of dissolution that set forth: (1) The name of the corporation; (2) The date of filing of its articles of incorporation; (3) Either: (a) That none of the corporation’s shares have been issued, or (b) That the corporation has not commenced business; (4) That no debt of the corporation remains unpaid; (5) That the net assets of the corporation remaining after winding up have been distributed to the shareholders, if shares were issued; and (6) That a majority of the incorporators or directors authorized the dissolution.

The name of the corporation; (2) The date of filing of its articles of incorporation; (3) Either: (a) That none of the corporation’s shares have been issued, or. (b) That the corporation has not commenced business; (4) That no debt of the corporation remains unpaid; (5) That the net assets of the corporation remaining after winding up have been distributed to the shareholders, if shares were issued; and. (6) That a majority of the incorporators or directors authorized the dissolution.")

38

Corporations FS (4) A director, officer, or agent of a corporation dissolved pursuant to this section, purporting to act on behalf of the corporation, is personally liable for the debts, obligations, and liabilities of the corporation arising from such action and incurred subsequent to the corporation’s administrative dissolution only if he or she has actual notice of the administrative dissolution at the time such action is taken; but such liability shall be terminated upon the ratification of such action by the corporation’s board of directors or shareholders subsequent to the reinstatement of the corporation under ss

39

Corporations FS (1) Whoever shall pledge, mortgage, sell, or otherwise dispose of any personal property to him or her belonging, or which shall be in his or her possession, and which shall be subject to any written lien, or which shall be subject to any statutory lien, whether written or not, or which shall be the subject of any written conditional sale contract under which the title is retained by the vendor, without the written consent of the person holding such lien, or retaining such title; and whoever shall remove or cause to be removed beyond the limits of the county where such lien was created or such conditional sale contract was entered into, any such property, without the consent aforesaid, or shall hide, conceal or transfer, such property with intent to defeat, hinder or delay the enforcement of such lien, or the recovery of such property by the vendor, shall be guilty of a misdemeanor of the first degree, punishable as provided in s or s A court may hold that an officer is personally liable for the amount of a statutory lien on property that is sold by the officer. In this case, the lien is the amount of the taxes. If an officer disposed of assets of the corporation which were subject to a lien, the officer could be personally responsible for the amount of the lien to the creditor. Littman v Commercial Bank & Trust Company, 425 So. 2d 636 (3rd DCA 1983). We can notify officer of corporation that we may proceed against him or her personally if they do not pay taxes. Additionally we can also file a criminal complaint against him or her with appropriate local law enforcement agency.

. We can notify officer of corporation that we may proceed against him or her personally if they do not pay taxes. Additionally we can also file a criminal complaint against him or her with appropriate local law enforcement agency.")

41

Florida Statute Uncollectible personal property taxes; correction of tax roll - A tax collector who determines that a tangible personal property account is uncollectible may issue a certificate of correction for the current tax roll and any prior tax rolls. The tax collector shall notify the property appraiser that the account is invalid, and the assessment may not be certified for a future tax roll. An uncollectible account includes, but is not limited to, an account on property that was originally assessed but cannot be found to seize and sell for the payment of taxes and includes other personal property of the owner as identified pursuant to s. (8) and (9).

and (9).")

42

Appraiser Education Educate your appraisers on the Florida collection laws and DOR Rules. Determine if your collector use penalties, seizures, bank garnishments etc. Inform appraisers that data inaccuracies can greatly reduce the enforceability of (their) roll. Promote office / roll procedures that will ensure legal enforcement of the lien. Inform appraisers of the final outcome (collection stats.)

roll. Promote office / roll procedures that will ensure legal enforcement of the lien. Inform appraisers of the final outcome (collection stats.)")

43

Public Outreach Are your taxpayers properly informed and educated on the TPP rules and laws affecting them? Are you properly training your taxpayers / filers? Do you employ effective outreach programs? Use Collector field agents to disseminate information.

44

Closing Points Communicate with your collector and determine your TPP Roll weaknesses. Collectively determine what is best for your County. Don’t let yourself or your collector trip over an ego, it’s a nasty fall.

45

Appraiser / Collector Relationships

Working Together Building Public Trust & Confidence

Similar presentations

, partner, Clifton Kok.>")

, Bob Sagel (Morgan), Linda Statz (Phillips), Wanda Lowery (Sedgwick)>")

845-7086.>")

572-4500 Direct: (253) 620-2537 1201.>")

Professor Charles H. Smith Creditors’ Rights and Remedies (Chapter 28) Spring 2009 Professor Charles H. Smith Creditors’ Rights.>")