Download presentation

Presentation is loading. Please wait.

1

Legislative Audit and Implementation of 2014 House Bill No. 560

2

A constitutional amendment passed in 1994 changed the State Auditor to the State Controller and moved the financial audit function to the Legislative Services Office. This resulted in a single office that provided all legislative support functions. The Legislative Audit Division performs primarily financial/compliance audits.

3

Idaho Code Section 67-701 establishes the Legislative Services Office under the Legislative Council. Idaho Code Section 67-702 through 67-704 establishes the four divisions within the Legislative Services Office.

4

Legislative Council Legislative Services Office Eric Milstead, Director Financial/HR Officer Terri Kondeff Special Projects Coordinator Michelle O'Brien Capitol Services Committee & Capitol Tours Program Admin. Assistant Sara Bingham Legislative Information Center (Seasonal) Legislative Audits April Renfro, CPA Division Manager Budget & Policy Analysis Cathy Holland-Smith Division Manager Research and Legislation Mike Nugent Division Manager Information Technology Glenn Harris Division Manager

Legislative Audits April Renfro, CPA Division Manager Budget & Policy Analysis Cathy Holland-Smith Division Manager Research and Legislation Mike Nugent Division Manager Information Technology Glenn Harris Division Manager.")

5

Idaho Code Section 67-450(B-D) requires a financial audit be completed and submitted to the Legislative Services Office for the following entities based on a tiered set of requirements: 67-450B—Local Governmental Entities. 67-450C—Affiliated Organizations to State Governmental Agencies or Entities. 67-450D—Designated Entities.

6

Idaho Code Section 67-450B was added in 1993 and amended in 1996, 2009, and 2011. It has the broadest coverage of the three statutes, including all: Cities, counties, authorities and districts organized as separate legal and reporting entities under Idaho law, and Councils, commissions, and boards as appointed or elected and charged with fiscal management responsibilities.

7

Idaho Code Section 67-450C was added in 1997 and amended in 2009. This section was added to include entities that may not have met the requirements included under Idaho Code Section 67-450B. Affiliated organizations include state departments, commissions, institutions, and colleges and universities created pursuant to statute or the constitution and which receive an appropriation from the legislature.

8

Idaho Code Section 67-450D was added in 2010 and amended in 2011. This section specifically identified 21 commissions that are required to complete and submit a financial audit to the Legislative Services Office.

9

For all entities identified in the preceding statutes, the following guidelines were provided to determine when an audit was required: Entity annual expenditures (from all sources) in excess of $250,000 require an annual audit submitted no later than 9 months after the end of the fiscal year. Entity annual expenditures (from all sources) between $100,000 and $250,000 require a biennial audit (every two years) submitted no later than 9 months after the end of the second fiscal year. Entity annual expenditures (from all sources) less than $100,000 do not require an audit.

between $100,000 and $250,000 require a biennial audit (every two years) submitted no later than 9 months after the end of the second fiscal year. Entity annual expenditures (from all sources) less than $100,000 do not require an audit..")

10

House Bill No. 560 came about because legislators were concerned about the ability to access financial information related to all of the local governments and special districts across the state. Additionally, my office was fielding more and more questions from constituents asking for copies of audit reports or financial statements for these districts. In January of 2014 we issued a report that identified the problems with the current process for reporting.

11

This report identified several problems with “special districts”. Along with concerns raised prior to the audit by legislators, led to legislation in the 2014 session. 11

12

We identified three objectives for the review of special districts in Idaho: Identify how many special districts there are in Idaho. Determine how special districts are monitored, both operationally and financially. Determine compliance with Idaho Code Section 67- 450B.

13

No central registry exists. It is difficult to determine who should be submitting what type of audit, or even “what’s out there.” No budget data is submitted, making it difficult to determine whether districts are complying. There is no enforcement mechanism for non- compliance. http://legislature.idaho.gov/audit/locgovreports/specialdistrictreport2014.pdf 13

14

Establish a central registry to provide a comprehensive list of all special districts authorized to operate within the State of Idaho. Require all local governments and special districts to submit an approved budget. Amend the statute to include a notification and enforcement process for noncompliance.

15

We plan to issue a follow up report prior to the 2015 Legislative Session that will provide updated information on several issues identified in the report including: Compliance rates after release of the report. Progress implementing the registry portal. Future planned reporting.

16

H496 – would have required an audit or internal controls, online posting and number of full time positions, total salary and benefits paid to employees, unpaid but accruing benefits, total retirement costs, average wage costs, benefit costs, retirement costs and accrued benefit costs per position. Failure to comply would have resulted in revenues withheld by state and county. Pulled by sponsor H474 – require registration, contact information, taxes, fees, assessments or charges imposed or collected and statutory authority for each; most recent budget, financial reports and audit report; dollar amount and term of bonds issued. Replaced by H523 16

17

H523 – similar to H474, but with more specifics as to what contact information, when posting was required, and comparison of budget to actual expenditures. Replaced by H560 H560 – final version that passed. House 68-0-2 Senate 35-0-0 Signed by the Governor March 26, 2014 effective 01/01/2015 17

18

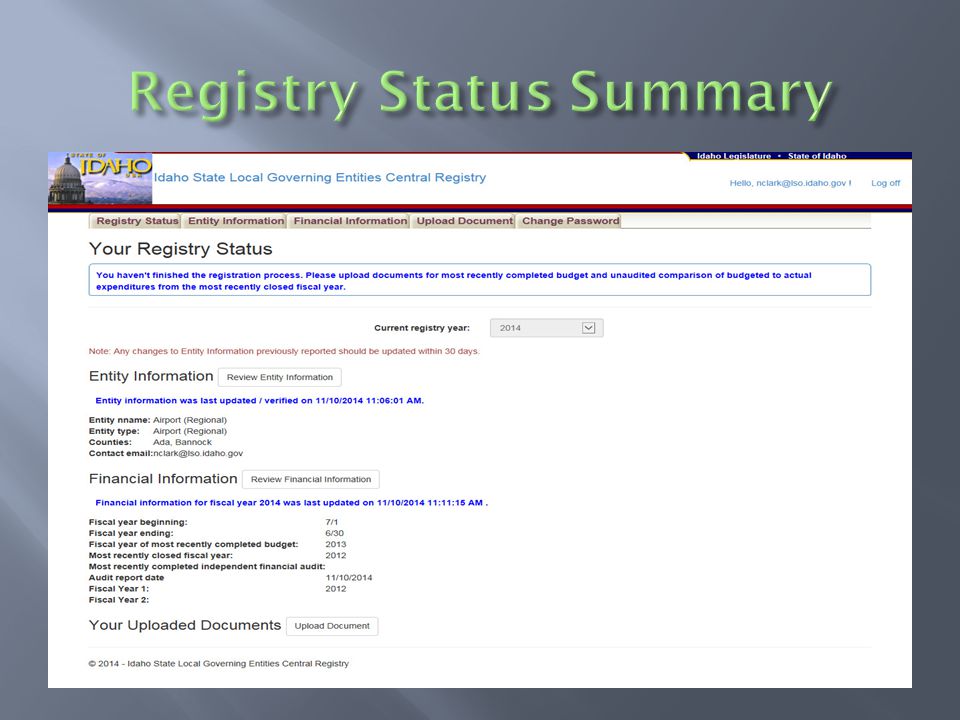

Establishes central registry in LSO. Website portal available on January 1, 2015. Local governments required to register by March 1, 2015. Counties and the Tax Commission to report known special districts by September 1, 2015. Audits Division will work with lists and registry to identify those entities that have not registered and notify them of the requirement. 18

19

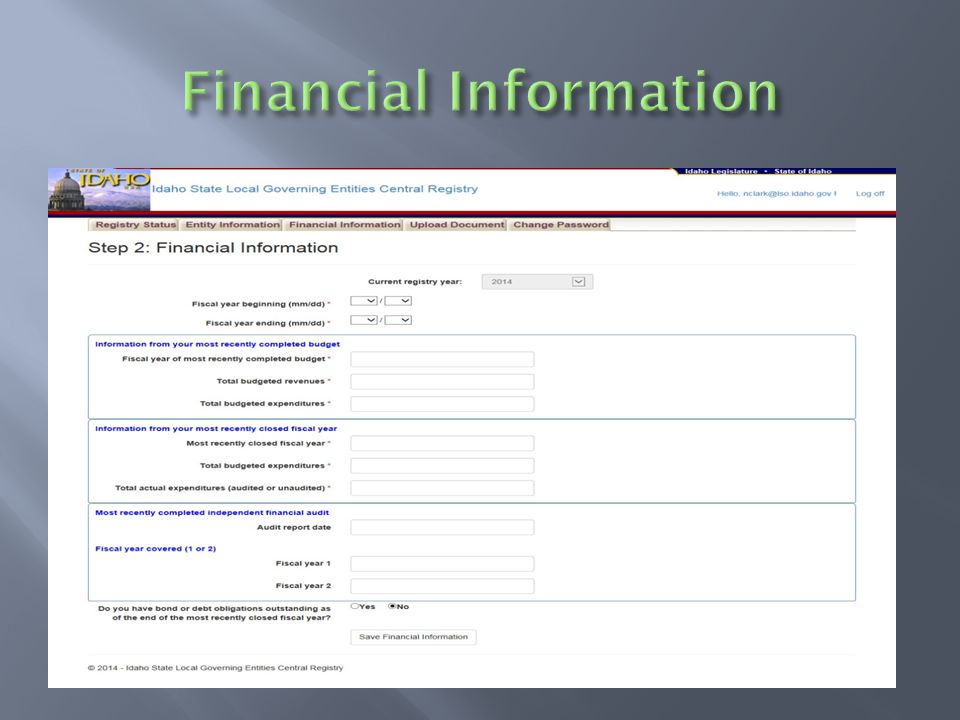

Information required through the portal registration: Contact information. Terms of membership and appointing authority for the governing board (if applicable). Fiscal year for the entity. Authority by which entity was established (N/A for cities and counties). Most recent adopted budget (which will include a line to enter total revenues and total expenditures and an upload feature for a PDF of the complete document).

. Fiscal year for the entity. Authority by which entity was established (N/A for cities and counties). Most recent adopted budget (which will include a line to enter total revenues and total expenditures and an upload feature for a PDF of the complete document)..")

20

Information required (continued): Unaudited comparison of budget to actual revenues and expenditures for the most recent fiscal year (PDF). Total dollar amount of bond and other debt obligations issued (outstanding) by the entity, with the average term and average interest rate. Date of the last independent audit. Audit reports as required by Idaho Code Section 67-450B must be submitted via the online portal. After initial submission of registry information by March 1, 2015, subsequent submissions required by December 1 of each year. If the entity has an appointing authority, notification that the registry was complete should occur within five days after filing Changes (i.e. contact information) must be updated within 30 days after the change. Entities can request County assistance; counties can charge reasonable expenses. 20

by the entity, with the average term and average interest rate. Date of the last independent audit. Audit reports as required by Idaho Code Section B must be submitted via the online portal. After initial submission of registry information by March 1, 2015, subsequent submissions required by December 1 of each year. If the entity has an appointing authority, notification that the registry was complete should occur within five days after filing Changes (i.e. contact information) must be updated within 30 days after the change. Entities can request County assistance; counties can charge reasonable expenses. 20.")

21

21 March 1, 2015June 30,2015July 2015September 2015December 1,2015 Registration on Online Portal by entity must be complete Notify the Idaho Tax Commission and counties of entities failing to comply— Sept 1 Audit reports are due for entities with Sept. 30 2014 year end LSO will notify registered entities one month prior to when the audit report is due, and within the first five days of the month after the audit report was due but not received. Upon notification, counties will place a public notice indicating the entity is noncompliant. Re-certification of information submitted to the registry is required Tax Commission and counties will supply LSO a listing of all known local governments and special districts

22

If the entity fails to report, Legislative Services will notify the entity, then they have 30 days to submit or notify LSO when the information will be submitted. If information is not submitted, Legislative Services notifies County Commissioners and Idaho Tax Commission not later than September 1 of any given year. The county publishes notice in official newspaper of non-compliance (entity will pay publishing costs). Failure to comply bars entity from increasing property taxes and state revenue sharing funds are withheld until compliance is achieved. For non-taxing districts (i.e. urban renewal agencies), County Commissioners may assess $5,000 fine and require special audit. 22

. Failure to comply bars entity from increasing property taxes and state revenue sharing funds are withheld until compliance is achieved. For non-taxing districts (i.e. urban renewal agencies), County Commissioners may assess $5,000 fine and require special audit. 22.")

23

Intent of the changes is to improve transparent access to information, identify governing entities operating within the State, and ensure compliance with reporting requirements. Avoided burdensome wage and benefit reporting that was included in H496. Legislative intent for the future could include a one-stop portal for local government financial information. 23

24

Registry portal is almost complete and we will begin testing this week through the end of November 2014. Portal will be operational on January 1, 2015 to allow for registration to meet the March 1, 2015 deadline.

25

Link will be located on our website @ www.legislature.idaho.gov

35

Registry@lso.idaho.gov Legislative Services Office 208-334-4875

Similar presentations

Financial Disclosure Training.>")