Download presentation

Presentation is loading. Please wait.

1

The Effective Use of Capital Chapter 12

S. Scott MacDonald, Ph.D. President and CEO, SW Graduate School of Banking Foundation Director, Assemblies for Bank Directors Adjunct Professor, Dept. of Finance, Cox School of Business Southern Methodist University

2

The Southwestern Graduate School of Banking Assemblies for Bank Directors Southern Methodist University Cox School of Business PO Box Dallas TX Phone Fax S. Scott MacDonald, Ph.D. S. Scott MacDonald is president and CEO, SW Graduate School of Banking (SWGSB) Foundation, director of the Assemblies for Bank Directors, and Adjunct Professor of Finance, Cox School of Business, Southern Methodist University. He received his B.A. degree in economics from the University of Alabama and his Ph.D. from Texas A&M University. Dr. MacDonald joined the Southern Methodist University faculty as a visiting professor of Finance in 1997 and was named director of the SWGSB Foundation in Dr. MacDonald is a frequent speaker at professional programs, banker associations and banking schools. He is a nationally sought after strategic planning facilitator and consultant to the financial services industry. He has served as an expert resource witness before the Texas state Senate and is a former Chairman of the Board of Directors of a Texas financial institution. Dr. MacDonald is the co-author of the best selling textbook on banking, Bank Management, and the author of numerous articles in professional academic journals.

Foundation, director of the Assemblies for Bank Directors, and Adjunct Professor of Finance, Cox School of Business, Southern Methodist University. He received his B.A. degree in economics from the University of Alabama and his Ph.D. from Texas A&M University. Dr. MacDonald joined the Southern Methodist University faculty as a visiting professor of Finance in 1997 and was named director of the SWGSB Foundation in Dr. MacDonald is a frequent speaker at professional programs, banker associations and banking schools. He is a nationally sought after strategic planning facilitator and consultant to the financial services industry. He has served as an expert resource witness before the Texas state Senate and is a former Chairman of the Board of Directors of a Texas financial institution. Dr. MacDonald is the co-author of the best selling textbook on banking, Bank Management, and the author of numerous articles in professional academic journals.")

3

Why Worry About Bank Capital?

Capital requirements reduce the risk of failure by acting as a cushion against losses, providing access to financial markets to meet liquidity needs, and limiting growth Bank capital-to-asset ratios have fallen from about 20% a hundred years ago to around 8% today

4

Capital by size

5

Risk-Based Capital Standards

Historically, the minimum capital requirements for banks were independent of the riskiness of the bank

6

The 1986 Basel Agreement A bank’s minimum capital requirement is linked to its credit risk The greater the credit risk, the greater the required capital Stockholders' equity is deemed to be the most valuable type of capital Minimum capital requirement increased to 8% total capital to risk-adjusted assets Capital requirements were approximately standardized between countries to ‘level the playing field'

7

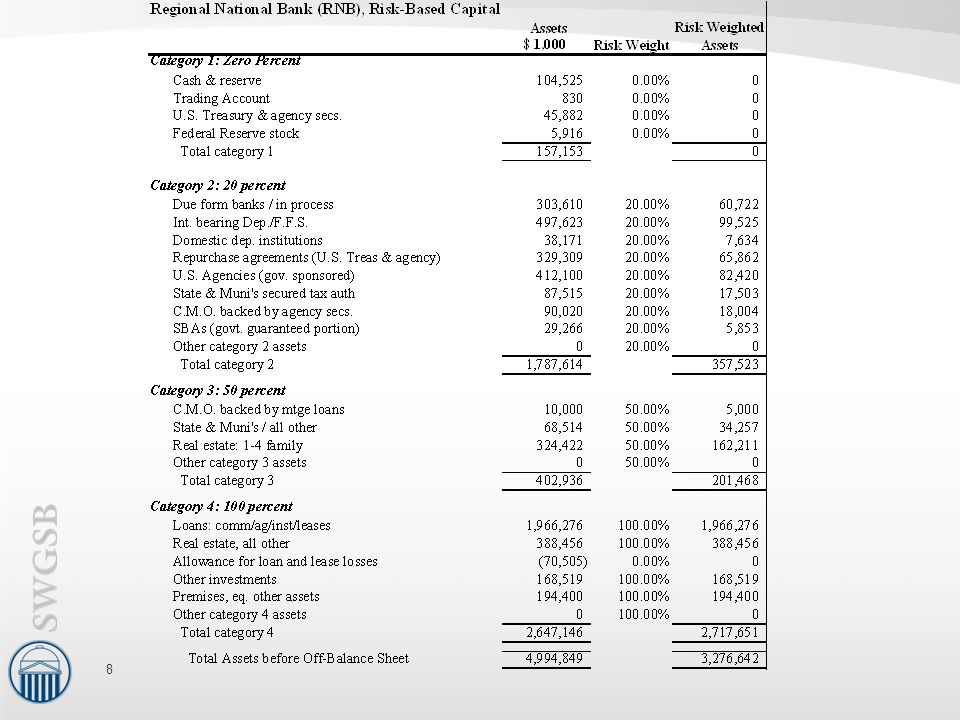

Risk-Based Elements of Basel I

Classify assets into one of four risk categories Classify off-balance sheet commitments into the appropriate risk categories Multiply the dollar amount of assets in each risk category by the appropriate risk weight This equals risk-weighted assets Multiply risk-weighted assets by the minimum capital percentages, currently 4% for Tier 1 capital and 8% for total capital

9

Risk-Based Capital Standards

10

General Description Of Assets In Each Of The Four Risk Categories

11

Off Balance Sheet Conversions

15

What Constitutes Bank Capital?

Capital (Net Worth) The cumulative value of assets minus the cumulative value of liabilities Represents ownership interest in a firm Total Equity Capital Equals the sum of: Common stock Surplus Undivided profits and capital reserves Net unrealized holding gains (losses) on available-for-sale securities Preferred stock

The cumulative value of assets minus the cumulative value of liabilities. Represents ownership interest in a firm. Total Equity Capital. Equals the sum of: Common stock. Surplus. Undivided profits and capital reserves. Net unrealized holding gains (losses) on available-for-sale securities. Preferred stock.")

16

Regulatory Capital Definitions

Tier 1 (Core) Capital Equals the sum of: Common stockholders equity Non-cumulative perpetual preferred stock Minority interest in consolidated subsidiaries, less intangible assets such as goodwill and disallowed deferred tax assets. Tier 2 (Supplementary) Capital, limited to 100 percent of Tier 1 capital Cumulative perpetual preferred stock Long-term preferred stock Limited amounts of term-subordinated debt Limited amount of the allowance for loan loss reserves (up to 1.25 percent of risk-weighted assets)

Capital. Equals the sum of: Common stockholders equity. Non-cumulative perpetual preferred stock. Minority interest in consolidated subsidiaries, less intangible assets such as goodwill and disallowed deferred tax assets. Tier 2 (Supplementary) Capital, limited to 100 percent of Tier 1 capital. Cumulative perpetual preferred stock. Long-term preferred stock. Limited amounts of term-subordinated debt. Limited amount of the allowance for loan loss reserves (up to 1.25 percent of risk-weighted assets)")

17

Regulatory Capital Definitions (continued)

Tier 3 Capital, applies only to larger institutions with consolidated trading activity is 10 percent or more of total assets for previous quarter. Minimum 8 percent ratio of total qualifying capital [the sum of Tier 1 capital, Tier 2capital, and Tier 3 capital allocated for market risk, net of all deductions] to risk weighted assets and market risk-equivalent assets

18

Leverage Capital Ratio

Regulators are concerned that a bank could acquire practically all low-risk assets such that risk-based capital requirements would be virtually zero To prevent this, regulators imposed a 3 percent leverage capital ratio equal to: Tier 1 capital divided by total assets net of goodwill and disallowed intangible assets and deferred tax assets

19

Tangible Common Equity

In response to the financial crisis, bank regulators placed greater importance on how much tangible common equity a bank had. Tangible common equity equals a bank’s tangible assets minus its liabilities and any preferred stock outstanding. Regulators and analysts construct a tangible common equity ratio (TCE) defined as tangible common equity divided by tangible assets: It reflects what would be left over if a bank were to liquidate and use the proceeds to pay off claims from debtors and preferred stockholders. It assigns no value to intangible assets, such as goodwill, mortgage servicing assets, and deferred tax assets. Regulators and analysts construct a tangible common equity ratio (TCE) defined as tangible common equity divided by tangible assets:

defined as tangible common equity divided by tangible assets: It reflects what would be left over if a bank were to liquidate and use the proceeds to pay off claims from debtors and preferred stockholders. It assigns no value to intangible assets, such as goodwill, mortgage servicing assets, and deferred tax assets. Regulators and analysts construct a tangible common equity ratio (TCE) defined as tangible common equity divided by tangible assets:")

21

What Constitutes Bank Capital?

22

Basel III Capital Standards

In July 2013, federal regulators approved Basel III capital rules with the intent to increase bank capital requirements and upgrade the quality of bank capital. The new requirements impose higher minimum capital ratios and place a greater emphasis on common equity as a preferred form of capital. The Basel III rules apply differently to larger and small organizations. Generally, smaller organizations can count more items as capital and have more time to comply with the new requirements. The increased capital requirements arise from stricter rules on what qualifies as capital, as well as the introduction of a new minimum capital ratio, common equity Tier 1 (CET1). When fully implemented, banks must hold a capital conservation buffer in addition to the old RBC minimums.

. When fully implemented, banks must hold a capital conservation buffer in addition to the old RBC minimums.")

23

Capital Conservation buffer

Under Basel III, the minimum capital requirements, when the final rules are implemented in 2019 will be: The Capital conservation buffer (CET1) is:

is:")

24

Weaknesses of the Risk-Based Capital Standards

Basel I standards only consider credit risk Ignores interest rate risk and liquidity risk Banks subject to the advanced approaches of Basel II use internal models to assess credit risk and the “results” are reported to the regulators 94% of banks are considered “well capitalized” in 2007, not a binding constraint for most banks

25

What is the Function of Bank Capital

For regulators, bank capital serves to protect the deposit insurance fund in case of bank failures Bank capital reduces bank risk by: Providing a cushion for firms to absorb losses and remain solvent Providing ready access to financial markets, which provides the bank with liquidity Constraining growth and limits risk taking

26

Bank Capital Provides a Cushion for Absorbing Losses.

Albeit not very well. Manufacturing firm, 60% debt, 40% equity. Commercial bank operates with very few fixed assets and 92% debt.

27

Bank Capital Provides Ready Access to Financial Markets.

As long as a bank’s capital exceeds the regulatory minimums, it can stay open and has the potential to generate earnings to cover losses and expand. FDICIA demonstrates that banks with the greatest capital-to-risk asset ratios will have the greatest opportunities to operate without restraint and to enter new businesses. Capital enables the bank to borrow from traditional sources at reasonable rates. Consequently, depositors will not remove their funds and asset losses will be minimized.

28

Capital Constrains Growth and Reduces Risk.

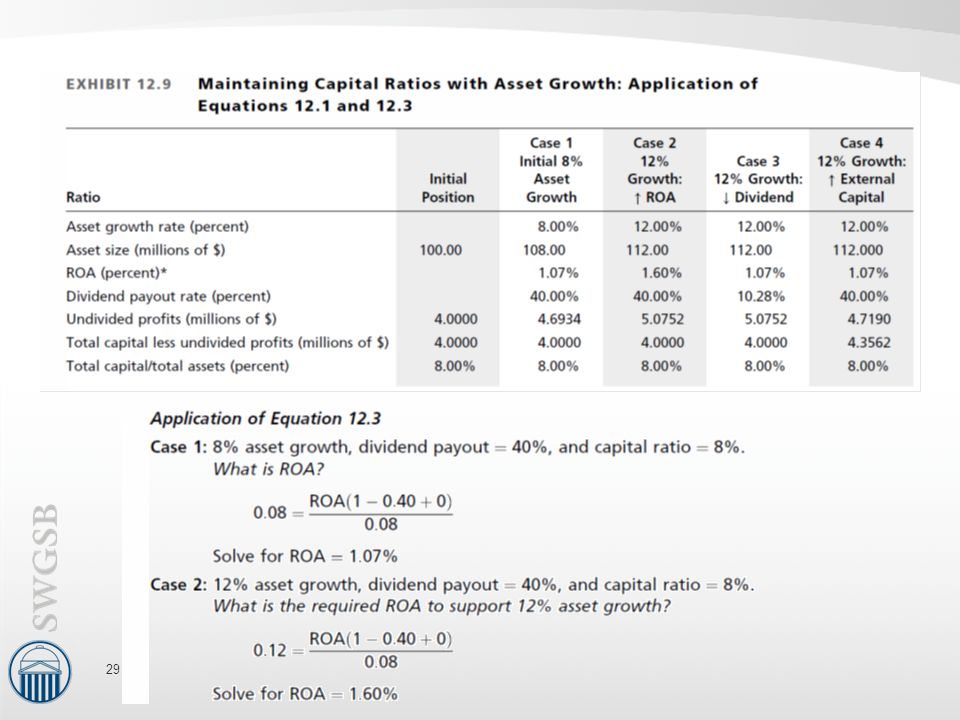

Capital constraints require that the asset growth rate equal the rate of growth in equity capital: TA /TA1 = EQ / EQ1 If not, the capital asset ratio will change. The change in total bank assets is restricted by the amount of bank equity where TA = Total Assets EQ = Equity Capital ROA = Return on Assets DR = Dividend Payout Ratio EC = New External Capital

31

The Effect of Capital Requirements on Bank Operating Policies

Changing the Capital Mix Internal versus External capital Change Asset Composition Hold fewer high-risk category assets Pricing Policies Raise rates on higher-risk loans Shrinking the Bank Fewer assets requires less capital

32

Characteristics of External Capital Sources

TARP Capital Purchase Program The Troubled Asset Relief Program’s Capital Purchase Program (TARP-CPP), allows financial institutions to sell preferred stock that qualifies as Tier 1 capital to the Treasury Qualified institutions may issue senior preferred stock equal to not less than 1% of risk-weighted assets and not more than the lesser of $25 billion, or 3%, of risk-weight assets

, allows financial institutions to sell preferred stock that qualifies as Tier 1 capital to the Treasury. Qualified institutions may issue senior preferred stock equal to not less than 1% of risk-weighted assets and not more than the lesser of $25 billion, or 3%, of risk-weight assets.")

33

TARP Recipients

34

Depository Institutions Capital Standards

The Federal Deposit Insurance Improvement Act (FDICIA) focused on revising bank capital requirements to: Emphasize the importance of capital Authorize early regulatory intervention in problem institutions Authorized regulators to measure interest rate risk at banks and require additional capital when it is deemed excessive The Act required a system for prompt regulatory action It divides banks into categories according to their capital positions and mandates action when capital minimums are not met

focused on revising bank capital requirements to: Emphasize the importance of capital. Authorize early regulatory intervention in problem institutions. Authorized regulators to measure interest rate risk at banks and require additional capital when it is deemed excessive. The Act required a system for prompt regulatory action. It divides banks into categories according to their capital positions and mandates action when capital minimums are not met.")

35

Depository Institutions Capital Standards

36

Basel III Capital Requirement Phase in Period.

Similar presentations