Download presentation

Presentation is loading. Please wait.

1

Welcome to National Landlord Day Conference and exhibition 6 November 2012 Sponsors:

2

Welcome and introductions Stephen Peasnall Chairman, Scottish Association of Landlords & Louise Batchelor Conference guest chair National Landlord Day 2012

3

National Landlord Day Conference and exhibition 6 November 2012 Sponsors:

4

Keynote speech Margaret Burgess MSP Minister for Housing and Welfare National Landlord Day 2012

5

National Landlord Day Conference and exhibition 6 November 2012 Sponsors:

6

Tenancy Deposit Scheme Rebecca Johnston & Alison MacDougall SafeDeposits Scotland Sponsors:

7

Tenancy Deposit Protection Rebecca Johnston Operations Manager SafeDeposits Scotland

8

5 working days

9

A not-for profit partnership of landlord, agent and tenant organisations, based in Scotland

10

From this…

11

To this… 2012 Inventory Check-out report Interim inspection reports Photographs and videos Estimates, invoices and receipts Any other correspondence

12

Fair wear and tear Alison MacDougall Depute Head of Adjudication SafeDeposits Scotland

13

An adjudicator’s experience of fair wear and tear…

14

Definitions ‘reasonable use of the premises by the tenant and the ordinary operation of natural forces’ the level of change expected by everyday use of a property throughout the length of the tenancy

15

Factors to consider Tenant’s obligation is generally to return the property in the same/similar condition at the end of a tenancy ‘fair wear and tear excepted’ Interpretation of reasonable use is not fixed Length of tenancy Type and number of occupants Location Quality

16

Fair wear and tear and betterment ‘ A landlord is not entitled to charge his tenants the full cost for having any part of his property, or any fixture and fitting,….put back to the condition it was at the start of the tenancy’ Not a ‘new for old’ insurance policy The most appropriate remedy

17

What the adjudicator looks for…. Evidence of condition (age and quality) at the start of the tenancy; Evidence of condition at the end of the tenancy; Length of tenancy; Number and type of occupants; Appropriate remedy – replacement, cleaning, compensation

at the start of the tenancy; Evidence of condition at the end of the tenancy; Length of tenancy; Number and type of occupants; Appropriate remedy – replacement, cleaning, compensation.")

18

Examples Scuffs on walls; Drawing on walls; Spots on carpets; Shading and fraying to carpets; Wooden floors and stiletto heels; Fading to curtains and upholstery; Unclean shower; Cracks in plaster; Burns or marks on worktops

19

To help you….

20

National Landlord Day Conference and exhibition 6 November 2012 Sponsors:

21

Universal Credit Graham Mowat Department for Work and Pensions Sponsors:

22

22 Universal Credit - Budgeting Support Scottish Association of Landlords Graham Mowat, UC Programme, DWP

23

23 Welfare Reform Universal Credit is part of a broader Welfare Reform programme I will not be covering other changes today but they are also important and many of them impact before UC e.g.: –The Work Programme –Sector size criteria –Localised Council Tax –Housing Benefit Cap –Main Benefit Cap –Social Fund moving to Local Authority administration

24

24 Preparing for Universal Credit What is Universal Credit? The Universal Credit service Supporting claimants Piloting, testing, pathfinder Universal Credit implementation

25

25 What is Universal Credit? A policy A benefit A gateway A platform An ambition that tackles welfare dependency, poverty and worklessness by making work pay that replaces a complex system of working-age benefits and credits with the Universal Credit and a single set of rules that together with our employment support programmes, helps people into work that will help us deliver an internet-age service whilst continuing face-to-face support for those who need it transforming lives and society through work

26

26 Housing costs under Universal Credit This is primarily about narrowing the gap between depending on benefits and being self-supporting in work: The Government wants people to manage their own budgets, including paying the rent, in the same way as other households. The introduction of Universal Credit is an opportunity to encourage more people to take control of their own housing costs. The Government believes that the benefit system should not treat people in a way that is materially different from the situation that they would experience whilst working. The greater the difference between the two, the more of a barrier there is to returning to a normal working life.

27

27 Universal Credit – a 21 st century service Universal Credit will be ‘digital by default’ with most claims made and managed online. Online service will be supported by a network of face-to-face and telephony support: A national service offering with targeted local flexibility from October 2013 – but ultimate goal remains a fully integrated Universal Credit service offering Achieving ‘digital by default’ by: Designing a compelling and easy to use service Working across government, private & voluntary sector to get more people online, e.g. with digital champions Supporting online channel through telephony, high street access

28

28 Claimants Time 2013 2017 Online Self Service Telephony Self Service Access to online Self Service provided by friends/family, High street 3rd Parties or Jobcentres Supported Service - Face to Face & Telephony Assisted Self Service - Telephony support for online transactions - High Street access - Support for online Claimants of DWP will become increasingly self-sufficient and prepared for the labour market, enabled through delivery of self service on every channel Digital by Default as part of channel strategy Claimants to be supported towards self-sufficiency over time Self - service

29

29 Six local authorities & housing associations are now trialling direct payments of Housing Benefit to selected tenants Oxford Direct Payments Demonstration Projects Edinburgh Wakefield Shropshire Southwark Torfaen Jun 12Projects started Jul 12First direct payments to selected tenants in LAs in England and Wales Jul 12First bi-monthly Learning Report produced – summary shared on Learning Network Aug 12First direct payments to selected tenants in Edinburgh Jan 13‘Learning the Lessons’ report published Jun 13Project completes Sep 13Final Project evaluation report published

30

30 2013 focus pilots - Twelve pilots will run from autumn 2012 to September 2013 to explore how local expertise can support residents to claim Universal Credit. 2013 focus pilots will look at: - encouraging claimants to access online support independently; - improving financial independence and managing money; - delivering efficiencies and reducing fraud & error; and - reducing homelessness. Post 2015 focus pilots – on the longer term role for local authorities in supporting Universal Credit claimants. North Dorset Rushcliffe Melton Bath & NES Oxford Lewisham West Lindsey Caerphilly Newport Birmingham North Lanarkshire West Dunbarton Local Authority-led Pilots Oldham Wigan Dumfries & Galloway Edinburgh Wakefield Shropshire Southwark Torfaen Key: LA-led pilots Pathfinder preparation projects Direct Payment Demonstration Projects

31

31 Pathfinder will take place from April 2013. It will test new payment system with local authorities, employers and claimants in a live environment – before national roll-out. Will target single, unemployed people, with or without rented housing costs, in specified areas in Tameside, Wigan, Oldham and Warrington local authority areas. North Dorset Rushcliffe Melton Bath & NES Oxford Lewisham West Lindsey Caerphilly Newport Birmingham North Lanarkshire West Dunbarton Pathfinder Oldham Tameside Dumfries & Galloway Edinburgh Wakefield Shropshire Southwark Torfaen Warrington Wigan Key: Pathfinder LA-led pilots Direct Payment Demonstration Projects

32

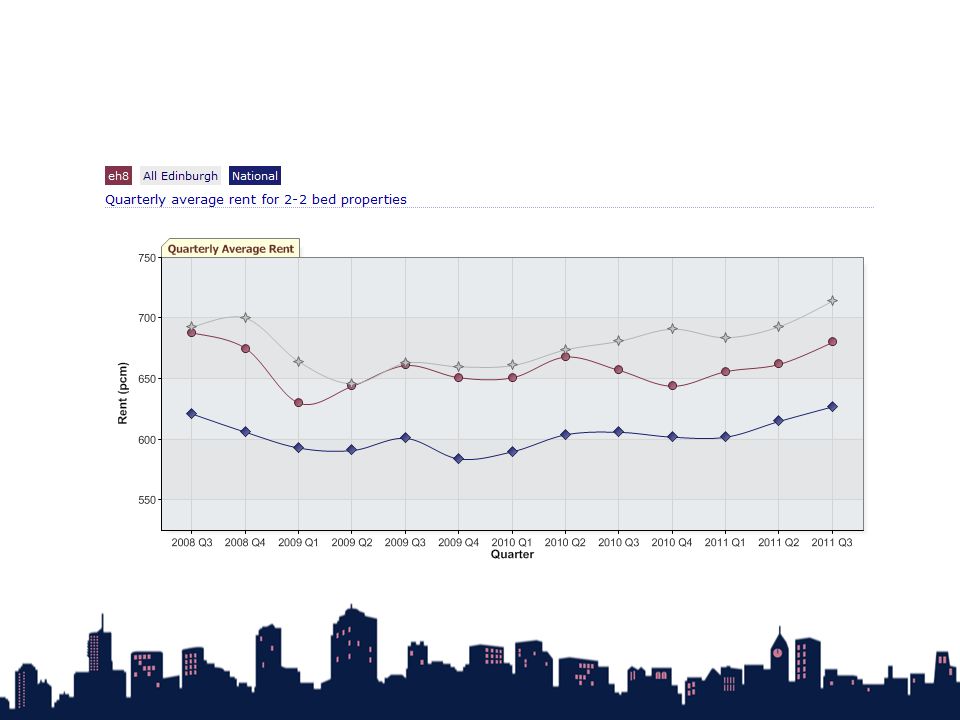

32 Implementing Universal Credit Universal Credit will go live in the Pathfinder area in Greater Manchester in April 2013. We are planning to begin the introduction of Universal Credit across Britain from October 2013. It will be introduced in stages – as is right and appropriate for such a large programme. The transition from the current system of benefits and tax credits is expected to be completed by the end of 2017.

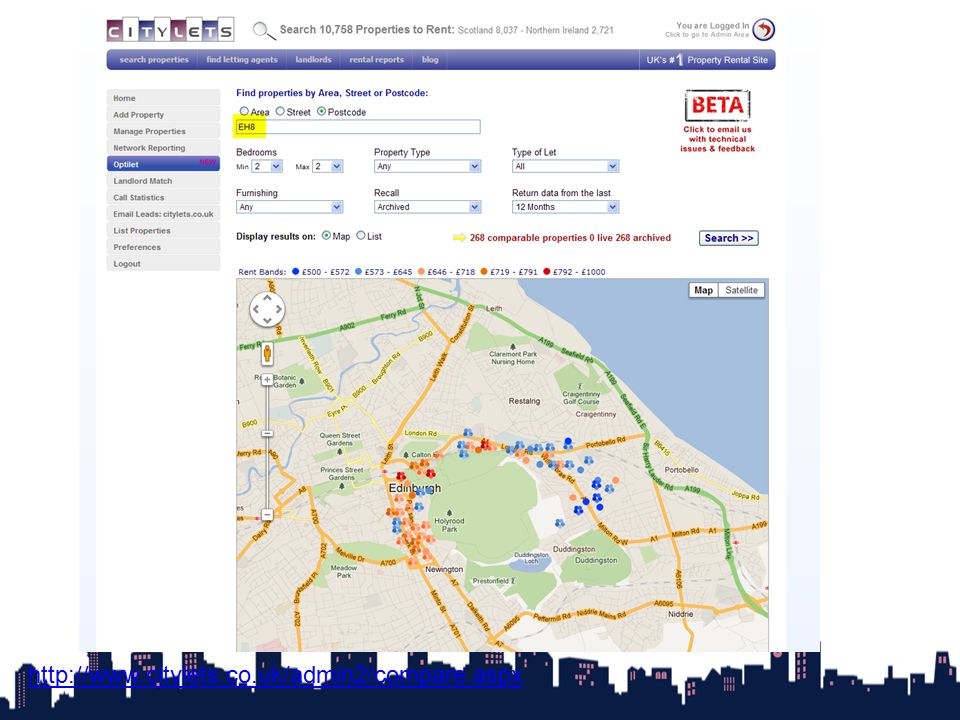

33

33 PERSONAL BUDGETING STRATEGY Claimant Preparation Work Focus Housing Costs Channels Financial Single payment Monthly Payment Claimants

34

34 Why change the way we pay claimants? Simplification Removal of barriers to work Tackling the poverty premium Working towards personal financial responsibility

35

35 Exploring more accessible financial services and accounts Supporting better budgeting Differentiation to recognise and respond to varying needs Financial Products working with financial product providers calling for a range of suppliers to explore feasibility of budgeting accounts Specific key features to support budgeting Tailored Support working with advice sector to ensure claimants are able to access appropriate budgeting support Exceptions developing an exceptions framework for those not able to manage Universal Credit, even with support Supporting claimants – financial inclusion

36

36 Budgeting Account - Service proposition Our key requirement is to ensure claimants have access to a range of suitable financial products that enable and support them to budget successfully. Essential features: –Ability to receive money from both UC and wages –Availability to people after they cease to receive UC –Direct debit and standing order facilities –ATM access –Clear transparent charge –No penalty charges (within reasonable parameters) –No overdraft

–No overdraft.")

37

37 Segmentation AbleMainly ableUnable Not worried 1.Ready & Able 2. Ready & Mainly Able 7. Not Worried & Unable Worried 3. Worried but able 4. Worried & Mainly Able 8. Worried & Unable Very worried 5. Very worried but able 6. Very Worried & Mainly Able 9. Very worried & unable Illustrative & draft

38

38 Matching support to services & channels Illustrative & draft

39

39 7. Work & Education 2. Agents & Appointees 3. Local Support Orgs 8. Financial Orgs 10. Govt. 6. Health & Social Care 4. Housing 5. Local Authority 1. Friends and Family 9. Utility Companies Third sector organisations such as CAB, CPAG, Gingerbread, MAS Etc Trusted intermediaries - Carers, POA, etc PO Banks & Building Societies Credit Unions Etc DWP, HMRC Jobcentres Work Programme UC Services inc Telephony and F2F GP Local NHS services Health workers Addiction / support schemes Landlords Housing Associations Local RSL services Supported Accom Hostels etc. Libraries Debts Advice Services On line schemes General benefit support services One stop shops Tell us Once Family Carers Other Claimant s – Word of mouth Etc Gas Water Electric Etc Suppliers E/Rs Local Education services Careers advice services Etc

40

40 Payment Exceptions - Vulnerability & Risk Factors Housing Costs for Payment Exceptions are built on the existing LHA guidance used by LA Benefits administration team today The framework, process and guidance has been developed in partnership with the Local Authorities and Housing Associations from the 6 Direct Payment Demonstration Projects and the Support & Exceptions Working Group, our external advisory group Private landlords are represented on the SEWG by the Scottish Association of Landlords/RLA partnership and the NLA.

41

41 Triggers - Internal Triggers – External High Level Process 1 Claimant 2 Claimant Representative 4 Business Knowledge – DWP, HMRC, LAs 3 Creditor e.g. Landlord or Utility Co. Apply for PE Budgeting Support Risk Scoring - Above Threshold Score? Y/N Decision Making Exception Yes or No? Implement Exception No yes Review until moving to BS yes No Refer for PE Joint data gather for assessment Assess Decide Review …of most interest to landlords…

42

42 Financial Support Summary - a differentiated support proposition Segment 1 – 4 Capable Segment 5 - 6 Some Capability Segment 7 – 9 Less capable Financial Product Current High street provision likely to be adequate. May benefit from a new UC budgeting account Will benefit from a new UC budgeting account Budgeting Support Any support needs they have can be met through on-line provision May need one-off support to get new account established Will need support to get new account established & ongoing Payment Exception Unlikely to be needed Will be needed by a sub-group. Channel Mainly on-lineMixed channelMainly F2F

43

43 What this means for private landlords In many ways you have already made the change via the Local Housing Allowance (LHA) Housing Costs for Payment Exceptions are built on the existing LHA guidance used by LA Benefits administration team today, based on enhancement agreed as part of the Direct Payment Demonstration Projects Arrangements as to how Landlords will be able to contact UC are yet to be finally determined – we are clear there will be a requirement for this e.g. in cases where the arrears trigger is reached

44

44 Next Steps Scottish Government have recently set up a Scottish equivalent of the SEWG I mentioned previously This is being administered by the SG’s Welfare Reform Division and supported by DWP Its inaugural meeting was on the 26 th of October We are arranging for SAL to join this group to make sure you are engaged moving forward

45

45 Universal Credit - Budgeting Support Scottish Association of Landlords Graham Mowat, UC Programme, DWP

46

National Landlord Day Lunch is served in the Stratosphere area Programme resumes 13.30hrs Please visit our exhibitors stands Sponsors:

47

National Landlord Day Conference and exhibition 6 November 2012 Sponsors:

48

Review of PRS market Dan Cookson Citylets Sponsors:

50

Today: Brief summary of independent research Citylets commissioned on PRS Key Findings from our Quarterly Reports Brief summary of Optilet our Web based research and analysis tool A review of Citylets growth

51

How well has your current rental property been managed by your letting agent / landlord? 79% quite well or very well (Agent managed) 86% quite well or very well (Landlord managed) How fairly do you feel you have been treated as a tenant during your tenure there? 88% quite fairly or very fairly These figures compare very favourably with equivalent surveys of social housing tenants. Independent Research commissioned by Citylets in 2011 (George Street Research Base 1003 PRS tenants in Scotland)

86% quite well or very well (Landlord managed) How fairly do you feel you have been treated as a tenant during your tenure there. 88% quite fairly or very fairly These figures compare very favourably with equivalent surveys of social housing tenants. Independent Research commissioned by Citylets in 2011 (George Street Research Base 1003 PRS tenants in Scotland).")

52

Size of Private and Social Rented Sectors PRS v Council (LA) v HAs PRS = HA = LAPRS = HA + LAPRS > 2 x (HA + LA)

v HAs PRS = HA = LAPRS = HA + LAPRS > 2 x (HA + LA)")

53

Market keeps management costs down Based on management fee of 10% of rent - Letting Agents are charging on average £806 per annum per property Housing Associations management fees are on average £1,024 per annum per property (and HA’s have less than a quarter of PRS new lettings volume to deal with) Source: The Scottish Housing Regulator Registered Social Landlord Annual Performance and Statistical Return 2010-11 and the Accounts Consolidation System 2011

Source: The Scottish Housing Regulator Registered Social Landlord Annual Performance and Statistical Return and the Accounts Consolidation System 2011")

54

Citylets Quarterly Report Bumper Issue 23 is just out Derived entirely from data entered by agents and landlords Empirical not sentiment based Continually evolving (e.g. Volume index) Expanding geographical coverage (e.g. Fife) Recognised as the definitive source of info. on the PRS and regularly covered in Press

Expanding geographical coverage (e.g. Fife) Recognised as the definitive source of info. on the PRS and regularly covered in Press.")

55

Our analysis is making the news..

56

Trends in Average Monthly Rent £672 is indeed a new high

57

Trends in Volumes of Lettings on Citylets UP

58

Trends in Scottish House Prices and Volumes VOLUMES FLAT PRICES FLAT

59

Trends in House Prices and Volumes Average Price for flats fell 4.3% in Q3 2012 while overall average house price fell 2.3% (source: Registers of Scotland)

")

60

Trends in Urban House Prices

61

Trends in House Prices and Rents UP FLAT

62

Rent UP 14% CPI and House Prices UP 24% Mind the Gap

63

FTSE up by just 3.9% since Jan 2006

64

Trends in TTL TTL FLAT

65

Trends in Aberdeen Rental Market TTL down

66

Trends in Edinburgh Rental Market

67

Edinburgh Rental Map

68

Glasgow Rental Map

69

OptiLet Something Gumtree doesn’t offer!!

70

OptiLet gives you the tools to be the expert on the market Optilet designed to assist landlords and agents set the right rent using the most comprehensive analysis of the most recent market data. Online reporting engine provides similar analysis to our report but at local level. You are the expert As of today can be found in the client admin area for agents or landlords Come for a live demo at the Citylets stand

71

http://www.citylets.co.uk/admin2/compare.aspx

74

Growth in advertised properties

75

Visitor traffic now double 2009 figures & treble 2007 figures (source: Google Analytics) Growth is accelerating Over 3 million visitors per year (source: Google Analytics, Nov 11-Oct 12) Growth in site traffic

Growth is accelerating Over 3 million visitors per year (source: Google Analytics, Nov 11-Oct 12) Growth in site traffic")

76

Growth and Brand Development According to Global competitive intelligence agency, Experian Hitwise, we are officially the No.1 dedicated residential lettings site operating in the UK by visitor numbers

77

Growth and Brand Development STV reaches 93% of the Scottish adult population Around 1000 TV adverts aired by Citylets in 2012

78

Share of visitors to Scottish lettings sites 44% 37% 19% 36% 29% Citylets: Market leader in Scotland

79

‘Citylets’ is the No 1 search phrase ‘Citylets’ used more often than any generic phrase such as ‘flats to rent in Edinburgh’

80

Citylets recording almost 3 times more brand searches than nearest direct competitor

81

2012 has been a very ‘exciting’ year for Citylets and the sector. We look forward to helping you make 2013 even more successful. Thank you.

82

National Landlord Day Conference and exhibition 6 November 2012 Sponsors:

83

Property Factors Act Frances Murphy Scottish Government Sponsors:

84

Property Factors (Scotland) Act 2011 Frances Murphy Senior Policy Officer Private Housing Services Policy Team 6 November 2012

Act 2011 Frances Murphy Senior Policy Officer Private Housing Services Policy Team 6 November 2012")

85

What is the Property Factors Act? Who does it affect? What new obligations does it place on property factors? What new protections does it give homeowners? Current position on implementation of the Act Content

86

What is the Property Factors (Scotland) Act 2011? A Member’s Bill Royal assent April 2011, in force 1 October 2012 Aims: –Set minimum standards of practice –Protection for homeowners who use services Main elements: 1)Register of property factors 2)Code of Conduct 3)Homeowner Housing Panel.

Register of property factors 2)Code of Conduct 3)Homeowner Housing Panel..")

87

Who does the Act affect? Property Factors –Defined in section 2 –Private sector, housing associations, local authorities –Who manage common parts, owned by more than 1 person, used for residential purposes. Homeowners –Defined in section 10 –Would include owner-occupiers, private and social residential landlords –Not tenants

88

Property Factor Register What is it? Compulsory - operating unregistered is a criminal offence Business details, Responsible/Relevant Persons details, houses/flats/land factored to be specified Publicly available Fit and Proper Person test to be passed Application fees - £370 for larger factors, £100 for small – for 3 years Registration expires every 3 years.

89

Property Factor Register Current Progress Online system accessed through SG website 250+ organisations made initial application by 1 October Helping some to fully complete Checking and approval process well advanced About 85 now approved and on public register Remainder to be approved in batches asap

91

Code of Conduct Requirements and Progress Requirements in the Act: –Minimum standards of practice that all property factors must comply with –Ministers must prepare a draft Code and publicly consult on it –Final version to be brought into force by approval of Parliament Progress –Final version published 13 July 2012 (unchanged from April 2012 version) –Effective from 1 October 2012

–Effective from 1 October 2012")

92

Code of Conduct What’s in it? Written Statement of Services Communication and Consultation Financial Obligations Debt Recovery Insurance Carrying out Repairs and Maintenance Complaints Resolution

93

Homeowner Housing Panel What is it? New dispute resolution system Based on an expansion of the existing Private Rented Housing Panel (PRHP) Able to consider complaints from homeowners Free to homeowners Can issue “property factor enforcement orders” – non-compliance a criminal offence.

Able to consider complaints from homeowners Free to homeowners Can issue property factor enforcement orders – non-compliance a criminal offence..")

94

Homeowner Housing Panel How do I access it? Two grounds: –Failure to comply with Code –Failure to carry out property factor’s duties Notify the property factor in writing Allow property factor reasonable opportunity to resolve issue – complaints procedure Useful info on HoHP website – application forms, guidance for applicants etc

95

Links & Contact Details Legislation - Property Factors (Scotland) Act 2011 and associated secondary legislation http://www.legislation.gov.uk/asp/2011/8/contents Scottish Government website – Property Factors Act pages - Links to: Code of Conduct Property Factor Register Homeowner Housing Panel (HoHP) http://www.scotland.gov.uk/Topics/Built- Environment/Housing/privateowners/propertyfactors/2011Act Frances Murphy Senior Policy Officer Private Housing Services Policy Team 0141 271 3783 frances.murphy@scotland.gsi.gov.uk

Act 2011 and associated secondary legislation Scottish Government website – Property Factors Act pages - Links to: Code of Conduct Property Factor Register Homeowner Housing Panel (HoHP) Environment/Housing/privateowners/propertyfactors/2011Act Frances Murphy Senior Policy Officer Private Housing Services Policy Team")

96

National Landlord Day Conference and exhibition 6 November 2012 Sponsors:

97

Yield: protection by it, retirement on it Stuart Law, Assetz Sponsors:

98

Presented by Stuart Law, CEO of Assetz plc Yield - how to retire on it and how it protected us all during the credit crunch

99

Agenda 1.Basic Principles of Sound Property Investment 2.Plan Ahead 3.Two Types of Investment Property – Income and Growth 4.Generators (purchased for income) 5.Accelerators (purchased for growth) 6.A Balanced Portfolio 7.Portfolio Stability How to build a safe, high-income property portfolio

5.Accelerators (purchased for growth) 6.A Balanced Portfolio 7.Portfolio Stability How to build a safe, high-income property portfolio")

100

Basic Principles of Sound Property Investment Keep to an income-centric, long-term and realistic strategy Have an end goal in mind Ensure your investments are underpinned by rental yield and demand Treat property as a long-term investment in order to reduce risk and maximise potential returns Investments should be cash flow positive wherever possible Buy with your head, not just your heart How to build a safe, high-income property portfolio

101

Plan Ahead Design a plan to meet your specific goals - Adopt a thought- through, well-directed strategy from the outset With careful planning, you can retire in a reasonable timeframe with a reliable, rental income-indexed income A plan saves time in the long run and reduces the chances of an unproductive investment Each property purchase can be evaluated for what value it brings to the ‘plan’ and for its level of risk Be realistic – start with a relatively modest level of income in mind Plan can then be modified in line with any windfalls How to build a safe, high-income property portfolio

102

Two Types of Investment Property – Income and Growth Property primarily purchased to generate long-term reliable income or yield (that we call Generators). If the rental income is based upon robust tenant demand then it can be highly predictable and can be classed as a true income-producing investment. Property primarily purchased for capital growth to potentially accelerate a retirement date (that we call Accelerators). As growth cannot be guaranteed, particularly in the short term, these are essentially speculative purchases. How to build a safe, high-income property portfolio

. As growth cannot be guaranteed, particularly in the short term, these are essentially speculative purchases. How to build a safe, high-income property portfolio.")

103

Generators (purchased for income) Capital value directly related to rental income Tend to be bought to provide a secure, hassle-free retirement income A reliable NET yield & minimal hands-on involvement are key Examples can include purpose-built student accommodation, hotel suites, commercial and industrial units, etc. Must generate strong enough net yield to service mortgage, pay other costs and tax, and repay the debt on the property in reasonable timeframe How to build a safe, high-income property portfolio

104

Generator with repayment mortgage How to build a safe, high-income property portfolio

105

Accelerators Typically offer higher growth rates but lower rental yields Usually require more involvement from investor / landlord Excellent return on capital invested over long term Rental income covers mortgage payments and on-going management and maintenance costs With today’s reduced prices and booming rents, high yields can also be achieved but potential for medium- to long-term capital growth remains UK residential properties - especially when bought at discounted prices in places with high demand Property trading or refurbishment profits How to build a safe, high-income property portfolio

106

Accelerator with interest only mortgage How to build a safe, high-income property portfolio

107

A Balanced Portfolio Build a balanced portfolio that reflects your risk profile and investment timescale Younger investors may take more risk through bias towards Accelerators Those with less time and greater need for certainty should bias towards good-quality Income Generators Carefully blend the two for a portfolio that performs well in growth years and provides good returns and safe income in periods of capital growth stagnation or falls How to build a safe, high-income property portfolio

108

A Balanced Portfolio How to build a safe, high-income property portfolio

109

A Balanced Portfolio How to build a safe, high-income property portfolio £ 1520

110

A Balanced Portfolio Key to reliable, index-linked income for retirement is a core of hands-off, high-income and relatively inflation-proof Income Generators Accelerators are intended to be sold off in future – capital used to repay remaining debt on generators early Any excess capital raised represents an additional lump sum Investor is left with a completely debt-free, income- generating portfolio How to build a safe, high-income property portfolio

111

Portfolio Stability Over-reliance on capital growth and Accelerators can produce little return and indeed losses in periods where property prices stagnate or fall – potentially disastrous Portfolio biased towards income-generating properties can sail through periods of property price weakness Owners of this type of property need not concern themselves with day-to-day property prices – No intention to sell A good mix will produce optimal results in minimal timeframe A 15-year timeframe, for example, will almost certainly produce some capital growth in order to repay the Generator debt early How to build a safe, high-income property portfolio

112

Thank you www.portfolio.assetz.co.uk

113

National Landlord Day Refreshments are served in the Stratosphere area Programme resumes 15.15hrs Please visit our exhibitors stands Sponsors:

114

Energy efficiency in private rented homes Ewan Fisher Energy Saving Trust Sponsors:

115

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Green Deal and ECO in Scotland Ewan Fisher Energy Saving Scotland Green Deal Advisor 6th November 2012

116

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Scottish wider policy context Sustainable economic growth Climate Change (Scotland) Act 2009 Energy Efficiency Action Plan Fuel poverty – 2016 Sustainable Housing Strategy National Retrofit Plan Energy efficiency standard for social housing 116

Act 2009 Energy Efficiency Action Plan Fuel poverty – 2016 Sustainable Housing Strategy National Retrofit Plan Energy efficiency standard for social housing 116")

117

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Green Deal and ECO Framework set by Energy Act 2011 UK Government policies Operational Autumn 2012 Working closely with DECC to ensure Scottish circumstances taken into account DECC consultation response published 11 June 117

118

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Green Deal in Scotland

119

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Green Deal UK’s commitment to encourage energy efficiency improvements paid for by savings from energy bills Programme to encourage installation of energy efficiency technology in the home Launch of Green Deal in October 2012 – Agreement to package of measures that pays for itself over time – ‘Golden Rule’ 119

120

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 How will Green Deal work in Scotland? Available across Great Britain, including in Scotland Anyone can apply The Green Deal customer journey will remain the same 120

121

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 The “customer journey” 121 Remote Advice – is provided by the ESSac network Remote Advice Free impartial advice for consumers Assessment Up front survey and advice Finance No upfront cost Installation Accreditation standards Repayments Through energy bill savings Green Deal Energy Company Obligation

122

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 The “customer journey” – remote advice 122 Remote Advice – is provided by the ESSac network Remote Advice Free impartial advice for consumers Assessment Up front survey and advice Finance No upfront cost Installation Accreditation standards Repayments Through energy bill savings Green Deal Energy Company Obligation

123

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 The “customer journey” - example 123 Customer interest AssessmentQuoteAccept quote Installation & after Can happen at the same visit impartial assessors work out what households need Customers choose what work they want done Quotes are personal and include subsidies Installers Costs charged to electricity bill Stays with home if move

124

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 The “customer journey” – installation and after 124 Customer interest AssessmentQuoteAccept quote Installation & after Can happen at the same visit Installation Accredited installers carry out work to clear standard. Sign off work once complete and inform GD Provider that repayments can begin. Repayments and follow up Payments collected through energy bills with Green Deal charge a separate line on the bill Continuing support from the Green Deal Provider throughout Customer is free to switch energy supplier

125

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Approval and the Green Deal Quality Mark DECC Oversight Body BSI PAS Installer Standard / Advisor Standard Green Deal Code of Practice UKAS Accrediting standards (Accredited) Certification Bodies Approved (Certified) Advisors & Installers Issues Quality Mark

Certification Bodies Approved (Certified) Advisors & Installers Issues Quality Mark")

126

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 What fails the Golden Rule... Under-heating households (who are poor or vulnerable) Hard to treat properties

Hard to treat properties.")

127

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Energy Company Obligation

128

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Energy Company Obligation (ECO) UK Government places obligations on energy suppliers to meet targets ECO replaces CERT & CESP Could be worth around £120m to Scotland each year Split into 3 separate targets 128

UK Government places obligations on energy suppliers to meet targets ECO replaces CERT & CESP Could be worth around £120m to Scotland each year Split into 3 separate targets 128")

129

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Energy Company Obligation (ECO) Target 1: Affordable Warmth Heating & insulation for poor & vulnerable Target 2: Carbon Saving Communities Loft, cavity & other insulation measures for poorest areas Includes social housing Target 3: Carbon Saving Solid wall & hard to treat cavities, plus packages 129

Target 1: Affordable Warmth Heating & insulation for poor & vulnerable Target 2: Carbon Saving Communities Loft, cavity & other insulation measures for poorest areas Includes social housing Target 3: Carbon Saving Solid wall & hard to treat cavities, plus packages 129")

130

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 ECO Scored in terms of carbon or bill savings over the lifetime of the measures installed No interim target Hard to treat cavities Affordable warmth measures District heating Role of Ofgem

131

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 ECO subsidy for low income communities and fuel poor households providing heating and insulation measures ECO carbon subsidy and Green Deal will deliver measures to hard to treat housing Green Deal supports the measures that meet the ‘golden rule’ - further loft insulation - cavity wall insulation GREEN DEAL £ ECO £ Green Deal and ECO Interaction

132

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Green Deal in private rented sector 46 per cent of landlords say they are aware of the Green Deal and 56 per cent of those landlords aware of it, are considering taking advantage of the energy initiative. Research carried out by the Scottish Association of Landlords September 2012 132

133

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 John Blackwood, Policy and Parliamentary affairs director of the Scottish Association of Landlords, says: 'Whilst our research shows that many landlords are keen to take advantage of the Green Deal, a third of landlords are not yet aware of the initiative. We encourage landlords to become familiar with the Green Deal as the private- rented sector has a key role to play in ensuring Britain meets its energy targets 'Furthermore, it is imperative that landlords future-proof their properties and their investments. The Green Deal is their opportunity to improve the quality of their properties and demonstrate their ability to engage with government initiatives without the burden of further regulation.’ 133

134

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Green Deal in private rented sector 63 per cent of landlords say they are aware of the Green Deal and 56 per cent of landlords are considering taking advantage of the energy initiative. ***RESEARCH BY SAL*** 134

135

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 John Blackwood, policy and parliamentary affairs director of the Scottish Association of Landlords says: 135

136

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Where do I start? Contact us at the Energy Saving advice centre on 0800 512012

137

R 0 G 169 B 224 R 79 G 45 B 127 R 207 G 0 B 114 R 199 G 172 B 150 R 237 G 41 B 57 R 194 G 172 B 190 R 41 G 153 B 38 R 254 G 209 B 0 R 225 G 216 B 183 Green Deal and ECO in Scotland Questions? 137

138

National Landlord Day Conference and exhibition 6 November 2012 Sponsors:

139

Letting law update Andrew Cowan TC Young solicitors Sponsors:

140

HOUSING LAW UPDATE Andrew Cowan TC Young LLP

141

Notices of Repossession (s34) No requirement to serve a Form AT6 when repossessing a property under section 33 of the Housing (Scotland) Act 1988 (the “compulsory repossession” route) Previously was a grey area

No requirement to serve a Form AT6 when repossessing a property under section 33 of the Housing (Scotland) Act 1988 (the compulsory repossession route) Previously was a grey area")

142

Yet to come! Advertising Disqualification Orders Overcrowding Rights of access Tenant Information Pack Premiums

143

Advertising Must include landlord registration number on an advert to let property or state “landlord registration pending” Does not apply to a “To Let” board at or near the house concerned

144

Disqualification Orders Where a landlord is convicted of letting a property while unregistered or attempts to let while unregistered Court may impose a Disqualification Order Prohibits the landlord from being registered by any Local Authority Period of up to 5 years Right of appeal

145

Overcrowding LA can serve an Overcrowding Notice on landlord Notice specifies steps required to be taken by the landlord to resolve overcrowding and a time period in which to do so Must be “reasonable” and “proportionate” No definition of overcrowding LA looks at “adverse effects” on health or wellbeing of any person or on the amenity of the house or its locality

146

Rights of Access Application by a landlord to the Private Rented Housing Panel (PRHP) for assistance in gaining access to a property Part 9 of Housing (Scotland) Act 2006 Access to enter the house to view its state and condition or to comply with a Repairing Standard Enforcement Order Still need a warrant to enter which is applied for by the PRHP – quicker and easier than current court route

for assistance in gaining access to a property Part 9 of Housing (Scotland) Act 2006 Access to enter the house to view its state and condition or to comply with a Repairing Standard Enforcement Order Still need a warrant to enter which is applied for by the PRHP – quicker and easier than current court route")

147

Tenant Information Pack Consultation held in May 2012 Landlord’s duty to provide to tenant no later than the start date of the tenancy Tick list of items to be provided to the tenant and signed by both tenant and landlord Guidance notes also to be provided (to be found on the Scottish Government website) Failure to comply will be a criminal offence with a penalty of up to £500 fine

Failure to comply will be a criminal offence with a penalty of up to £500 fine")

148

Premiums Changes come into effect on 30 November 2012 Consultation was held in May Current definition of a “premium” under Section 90 of the Rent (Scotland) Act 1984 “Any fine or other sum and any other pecuniary consideration in addition to rent” Section 32 of the 2011 Act amends the definition to clarify that a “premium” means “Any fine, sum or pecuniary consideration, other than rent, and includes any service or administration fee or charge”

Act 1984 Any fine or other sum and any other pecuniary consideration in addition to rent Section 32 of the 2011 Act amends the definition to clarify that a premium means Any fine, sum or pecuniary consideration, other than rent, and includes any service or administration fee or charge")

149

HOHP COMPULSORY REGISTRATION CODE OF CONDUCT WRITTEN STATEMENT OF SERVICES HOHP – DISPUTE RESOLUTION

150

Any Questions?

151

Closing remarks Stephen Peasnall Chairman, Scottish Association of Landlords & Louise Batchelor Conference guest chair National Landlord Day 2012

152

National Landlord Day Thank you for coming See you next year Sponsors:

Similar presentations

Sharon Williams Housing Operations Manager.>")

June 2011.>")

Act 2014 Presented by Anne Rowland, Programme Manager.>")